“Despite the slowing recovery in tourism in the region overall, one contact highlighted that May was the strongest month for hotel revenue in Philadelphia since the onset of the pandemic, in large part due to an influx of guests for the Taylor Swift concerts in the city,”

The quote is courtesy of the Philadelphia Fed’s contribution to the latest Federal Reserve Beige Book. The Beige Book reviews economic conditions in the 12 Fed districts. It has been estimated that the Taylor Swift tour could add $5 billion to the economy. CBS notes, “In a survey of 596 people, QuestionPro found that Swift concertgoers spent an average of $1,300 per show on expenses like tickets, outfits, travel, and food — which was an average of $720 higher than their intended budget.”

The so-called “Taylor Swift effect” boosts hotel and restaurant revenue everywhere she performs, as her groupies, the “Swifties,” often travel to see her. Hotels, according to Booking.Com, have been able to double or even triple prices when she is in town. As the tweet highlights, Taylor Swift may have boosted the Colorado economy by $140 million, accounting for almost 3% of Colorado’s GDP. The Common Sense Institute estimates Taylor Swift’s tour could generate $4.6 billion in consumer spending. For context, Bosnia, Senegal, and the Bahamas have roughly $5 billion in GDP.

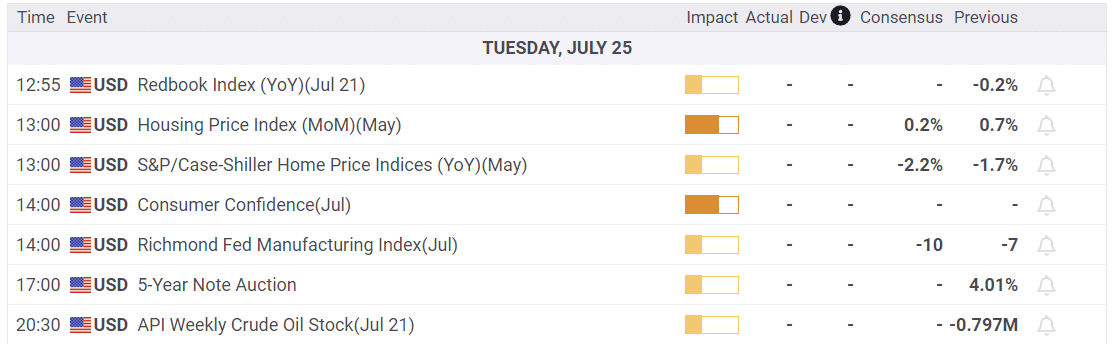

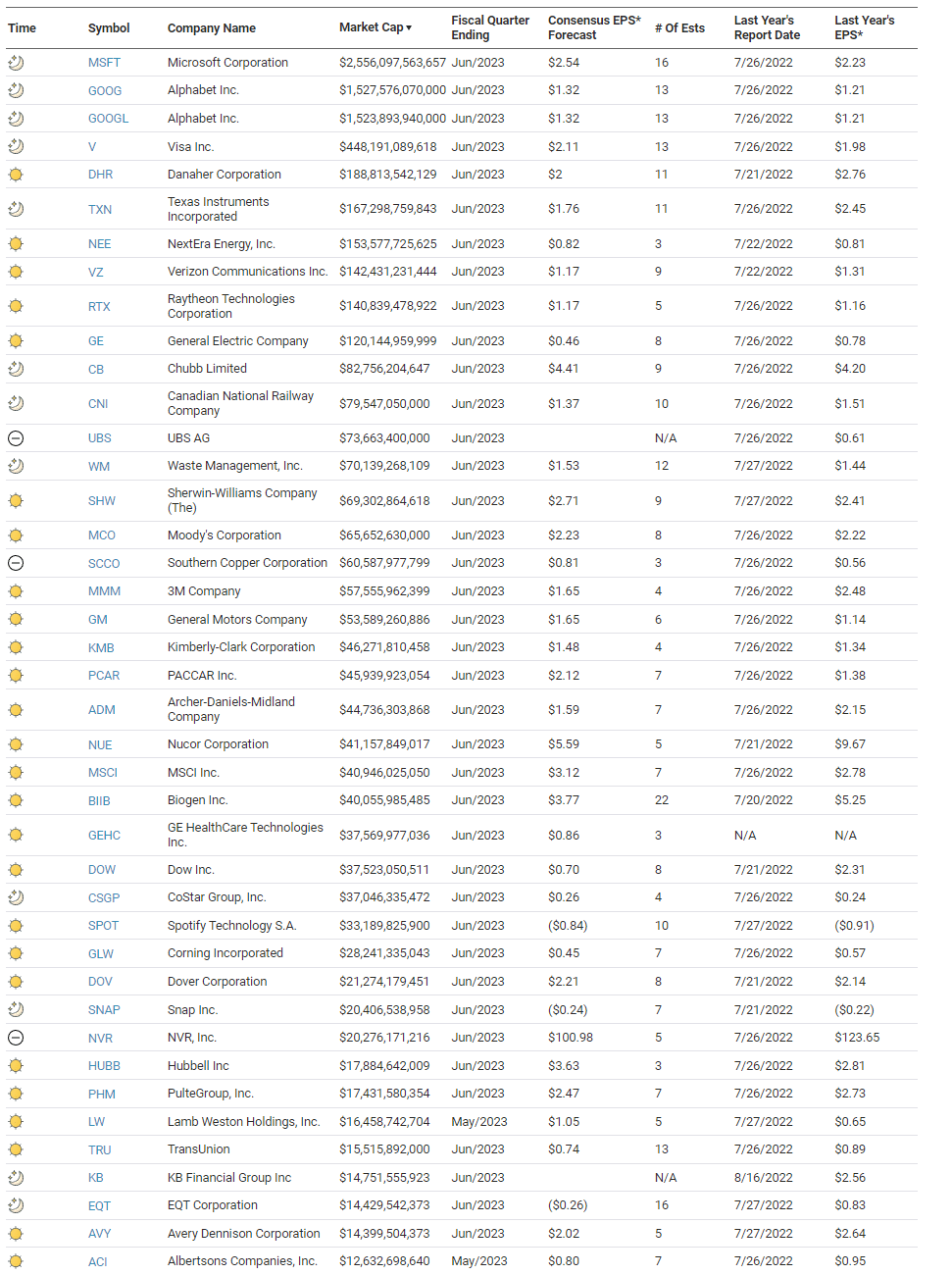

What To Watch Today

Economy

Earnings

Market Trading Update

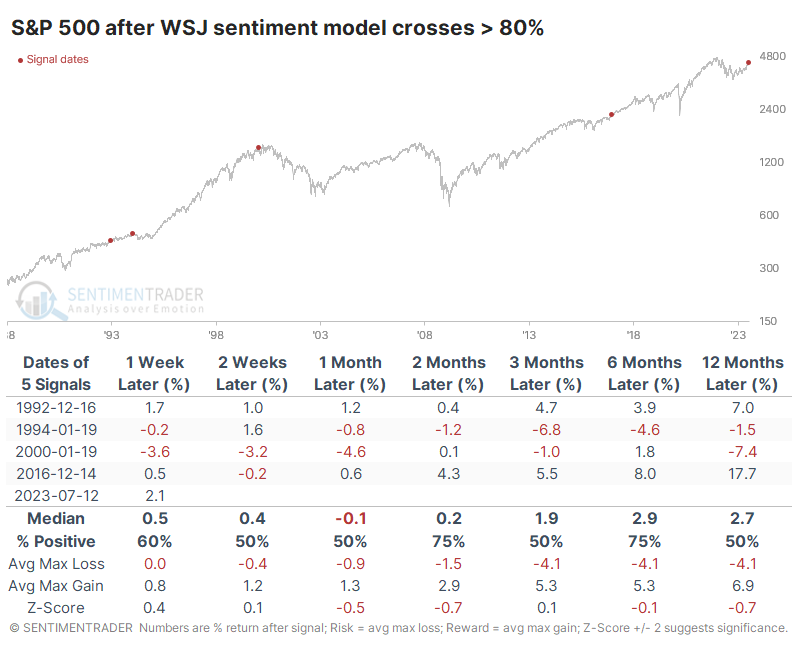

As expected, the Nasdaq rebalance yesterday was indeed a “nothing burger” despite the recent suggestions of a major break to the market. However, while the markets continue their bullish ways near term, there is little doubt that investor sentiment is getting rather extreme. Yesterday, Sentimentrader.com had a great note to this point.

“For the first time since at least 1988, the model is at 100%. That’s not a total surprise because the conditions in the article were selected specifically because they’ve just triggered. It’s also not a total surprise that it’s never happened before because most of the time, at least one indicator is off doing its own thing.

The arrows on the chart highlight those times when the model crossed above 80%, when five of the six indicators triggered excessive optimism. And it wasn’t too bad for stocks, though one ultimately led to the pricking of the internet bubble in 2000.

“The table below shows returns in the S&P 500 after the signals in the chart above. Gains were muted over the next six months, but so were losses. None of the signals preceded a loss of more than -8.5% for the S&P within the next six months, but none gained more than +8.5%, either. “

“At the risk of getting awfully repetitive, I’ll reiterate something I’ve noted for many months. After a year like 2022, investors will want to bail at the faintest hint of other investors getting optimistic. We’ve looked at an inordinate number of studies showing that behavior, as we’ve witnessed since October, would be extraordinarily rare during an ongoing bear market, so the probability we’re in a bull market environment is high and has been for more than seven months.

There is little doubt that sentiment has become optimistic, perhaps even excessively so. But the first bout of excessive optimism following a severe depression like 2022 tends to lead to higher prices, not lower ones. Gains are often muted, but so are losses. The indicators cherry-picked by the WSJ are no exception.”

This is a great piece of analysis. Importantly, the excessive optimism and more extreme deviations from longer-term moving averages suggest a likely 3-5% correction. However, that will be a buying opportunity as we head into the end of the year.

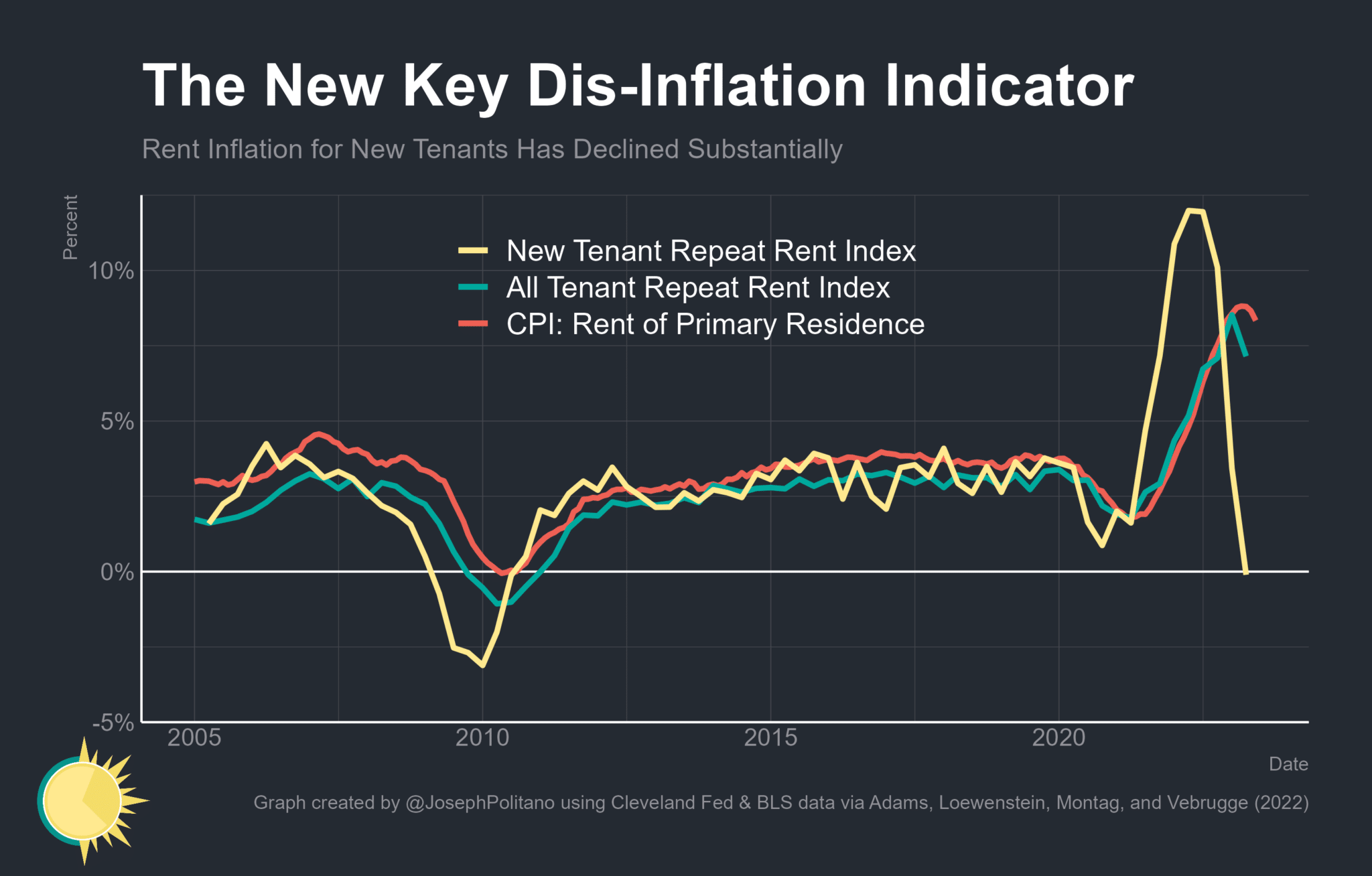

The Most Important New Disinflation Indicator

Joseph Plitano of Apricitas Economics wrote a thoughtful article that reviews what he believes is “the most important new inflation indicator.” As we have written numerous times, shelter prices constitute a third of the BLS CPI number, and the data often significantly lags real-time shelter data. Accordingly, accurately forecasting housing and rental prices is a critical component of inflation and, therefore, monetary policy.

Joseph notes that official inflation calculations measure average rents. Since most rents renew annually, inflation calculations heavily depend on rental costs not being up for renewal. For argument’s sake, it’s likely that less than 10% of rental prices are fresh. Ergo, they reflect prices from the last time the unit was up for a new lease. To help avoid this problem, the Cleveland Fed created the New Tenant Repeat Rent Index (NTRR). Unlike the current methods, the NTRR only uses the subset of lease renewals that are current.

Per the article:

The good news is that the NTRR has decelerated substantially over the last year—and that its deceleration is strongly corroborated by slowdowns in comparable private-sector data. Growth rates in the Zillow Observed Rent Index have decelerated to normal levels, while the NTRR and ApartmentList Median New Lease estimates show functionally zero growth over the last year. That deceleration is already starting to pass through to official CPI inflation—though with a longer lag than originally expected.

The bottom line, a third of CPI should decline rapidly. With wage growth normalizing and the prices of most other goods and services reverting to historical averages, we will likely soon once again hear the Fed bemoaning disinflation, not inflation.

New House Listings

New home sales are on fire mainly because there is a shortage of existing homes for sale. Higher mortgage rates make homeowners apprehensive about selling, losing their very low mortgage rates, and having to take on a new mortgage at 6%-7%. The graph below, courtesy of Lance Lambert, shows there are about 20-25% fewer houses on the market than is typical. More stunning, the number of homes on the market is running less than in 2020.

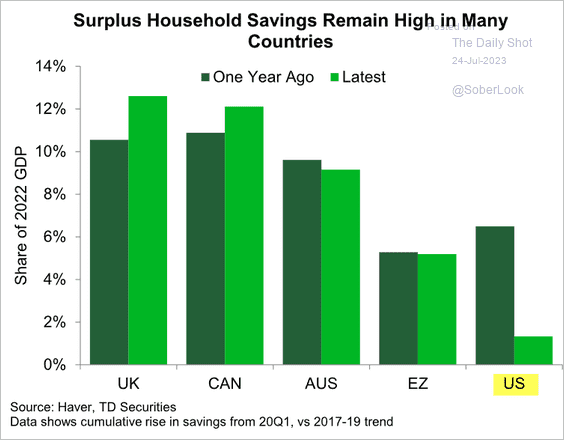

A Surplus of Savings Except in the U.S.

Massive fiscal stimulus sent to individuals during the height of the pandemic was primarily saved, as many felt insecure about spending on many traditional activities. In many cases, the inability or lack of desire to spend led to a surge in excess savings. Over the last year or two, those extra savings drove above-average economic growth as the pandemic waned. The graph below shows that the U.S., unlike the other countries shown, has very little surplus savings left. This one leg supporting economic growth will not be nearly as supportive as it was.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.