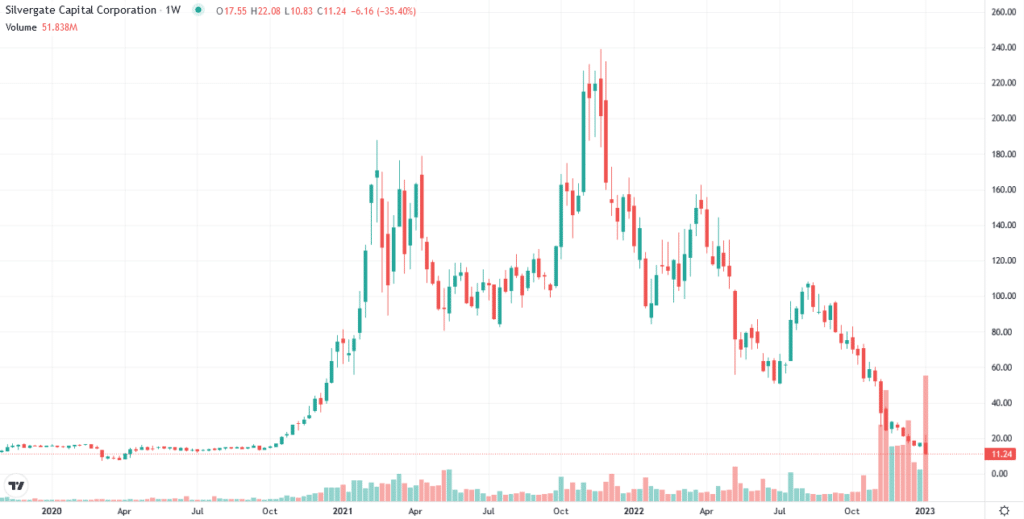

Silvergate Capital (SI) fell 40% on Thursday and is down by nearly 80% over the last six months. Silvergate is a crypto-friendly bank. Driving its shares significantly lower was an announcement the bank’s deposits tumbled by over $8 billion to only $3.8 billion, in what it calls a “crisis of confidence.” Further, Silvergate is laying off 40% of its employees and writing off a $196 million investment to create its own digital currency.

While the news may not be shocking in the wake of the problems with FTX and other crypto firms, Silvergate, unlike the other embattled crypto firms, is an actual bank. It is regulated under traditional banking legislation and regulators. Its deposits are FDIC insured. Silvergate highlights how crypto-related problems are creeping into more traditional financial firms. At this point, a default will not likely be a big event. However, we must consider the possibility that other, more traditional banks have financial exposure to Silvergate. Silvergates woes may spread up the banking food chain.

What To Watch Today

Economy

- 3:00 p.m. ET: Consumer Credit, November ($25.000 billion expected, $27.078 billion prior)

Earnings

Market Trading Update

Friday’s more robust employment report led to a massive surge in stocks as wages showed some initial weakness. Once again, and having failed to learn their lesson, the bulls piled into stocks hoping for a “Fed pivot.”

The good news is that the rally broke the market out of the recent consolidation range from the last half of December and pushed prices into the cluster of resistance around 3900. Notably, the market held support at the rising trend line from the October lows. While the market has surged into short-term overbought territory, a rally toward the 200-DMA is possible as the MACD “buy signal” crosses higher.

On SimpleVisor.com, we provide a proprietary indicator that tracks money flows into and out of the market. That signal also confirms the MACD “buy signal” as well, adding further support to a short-term rally.

Furthermore, sentiment remains negative enough to support a short-term rally.

However, the FOMC has not changed its tone about tightening monetary policy. We have previously seen these “pivot hope” rallies that Jerome Powell and the Fed repeatedly swat down. While we will likely have a tradeable rally, it remains worth selling into and trading accordingly. The headwinds of higher rates, quantitative tightening, and a drain of “stimulus” from the economy have not changed. If it wasn’t a good idea to “fight the Fed” during QE, it probably remains a good idea not to do so during QT.

For now, trade accordingly as we drift from one “pivot hope” report to the next, even though the Fed remains clear that no “pivot” is coming.

The Week Ahead

Q4 earnings season kicks off this week. Of note will be the big banks, with JPM, Wells Fargo, and Citi releasing reports on Friday. Some of the homebuilders and airlines also report this week.

Fed members will likely continue to fill the airwaves with their thoughts on monetary policy for the year ahead.

The Fed and investors will closely follow CPI on Thursday morning. Current expectations are for a .1% decline in the monthly rate. Such would bring the year-over-year down from 7.1% to 6.7%. However, the core rate is expected to rise by 0.2% monthly. Other than CPI, there is little else on the economic calendar.

BLS Jobs Report

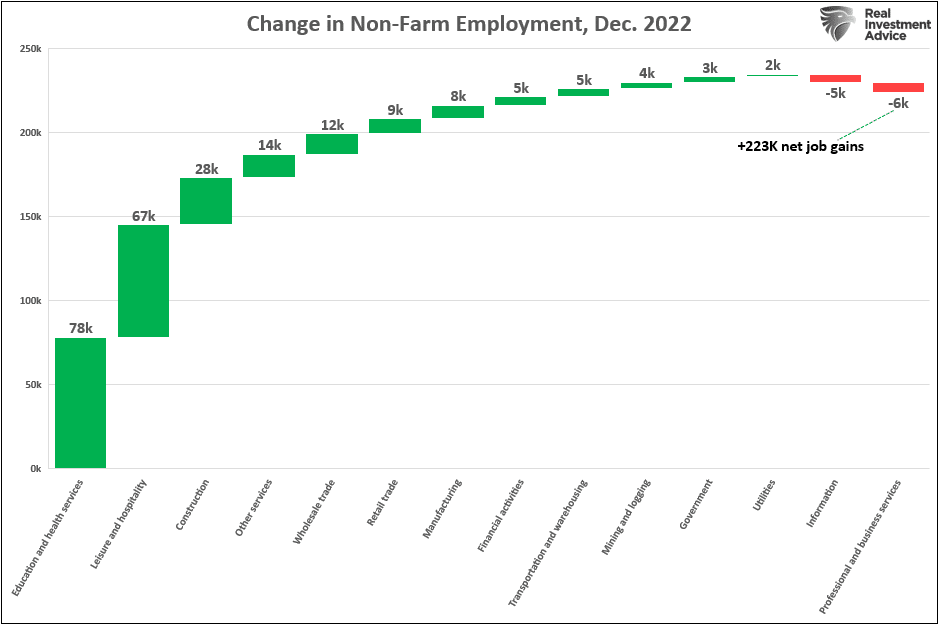

The headline data investors typically follow within the BLS labor report point to a robust jobs market with few signs of weakening. For instance, job growth was 223k, higher than expectations for 200k. The unemployment rate fell to 3.5% from 3.7% despite an increase in the labor force participation rate. Lesser followed data points to some potential weaknesses. For example, average hourly earnings only rose by 0.3% and were revised lower from prior months. Hours worked also fell a little short of expectations. Given the Fed’s deep concern about a price-wage spiral, weaker-than-expected wage growth provides some hope that employees do not have quite the leverage they had in 2022. The graph below shows that job growth predominates in sectors that tend to offer lower-paying jobs.

Also within the report, the number of part-time workers rose by 679k, while full-time workers fell slightly. The headline BLS establishment survey polls employers, not employees. As such, they count a person with two part-time jobs as two jobs. Ergo, if someone leaves a full-time job for two part-time jobs, the change can result in job growth, even though nothing has really changed. The household survey will show the employee as employed with one job, not two.

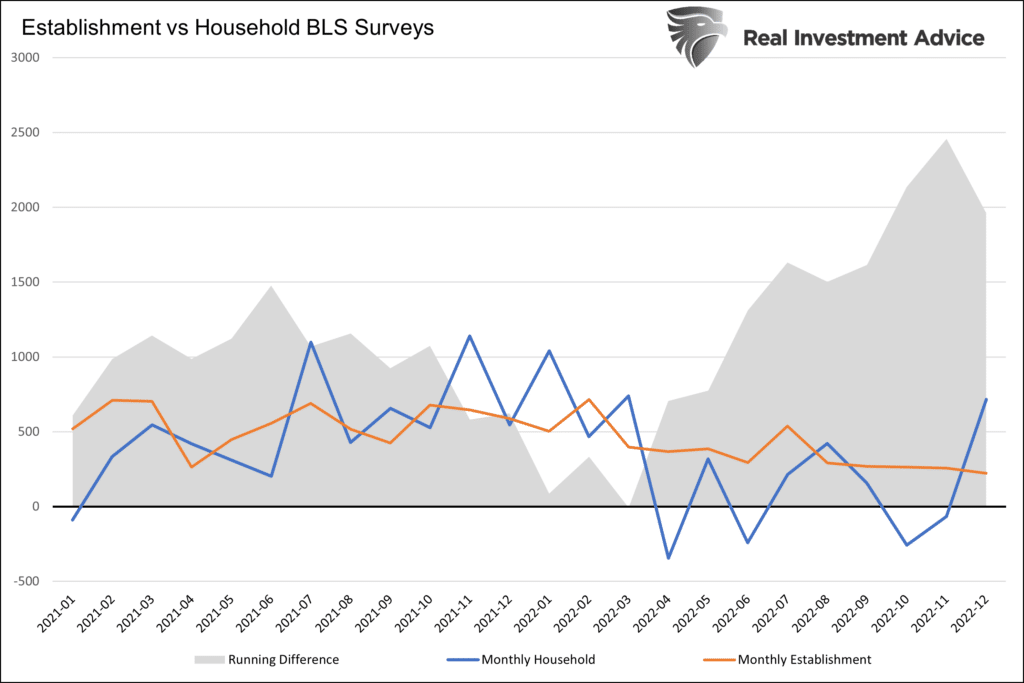

The household survey came roaring back with a huge gain of 700k jobs. The graph below compares the well-followed BLS establishment data with the household survey. As shown below, the household survey has been lagging behind the establishment survey, adding credence to the idea that employees are working multiple part-time jobs instead of full-time jobs. It is tough to have a strong read on the health of the labor market without looking through the entirety of the BLS data.

ISM Services- Yet Another Recession Warning

ISM Services fell sharply from 55.0 to 49.6, the first contractionary print since May 2020. This is yet another leading indicator of economic activity, screaming a recession is in sight. Further concerning, new orders fell from 56 to 45.2. The prices paid subcomponent fell but remains at a very high 67.6. With ISM services now below 50 and in economic contraction territory, it confirms warnings from the ISM manufacturing survey, which has been below 50 for over six months. As shown below, each of the last three recessions started when ISM services were above the current level. Lending further importance to the decline in services, the following graph shows that service-related jobs represent about three-quarters of all jobs.

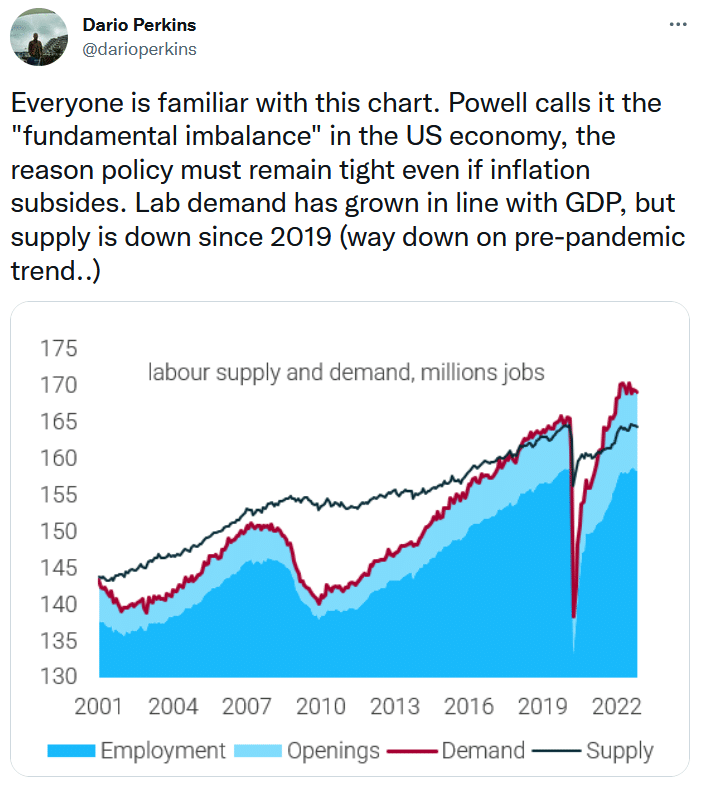

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.