This past weekend Saudi Arabia decided unilaterally to cut an additional million barrels of oil production per day starting in July. Thus far, it appears other OPEC nations will not follow Saudi Arabia’s lead and cut oil production. The cuts are scheduled for one month but may be extended. In April, OPEC cut production by 1.2 million barrels per day which followed a two million barrel cut in the prior October. Crude oil prices jumped on the news but remain well entrenched in its $65-$80 range. Saudi Arabia mentioned it was “fed up” that other OPEC members were not meeting their oil production cut goals.

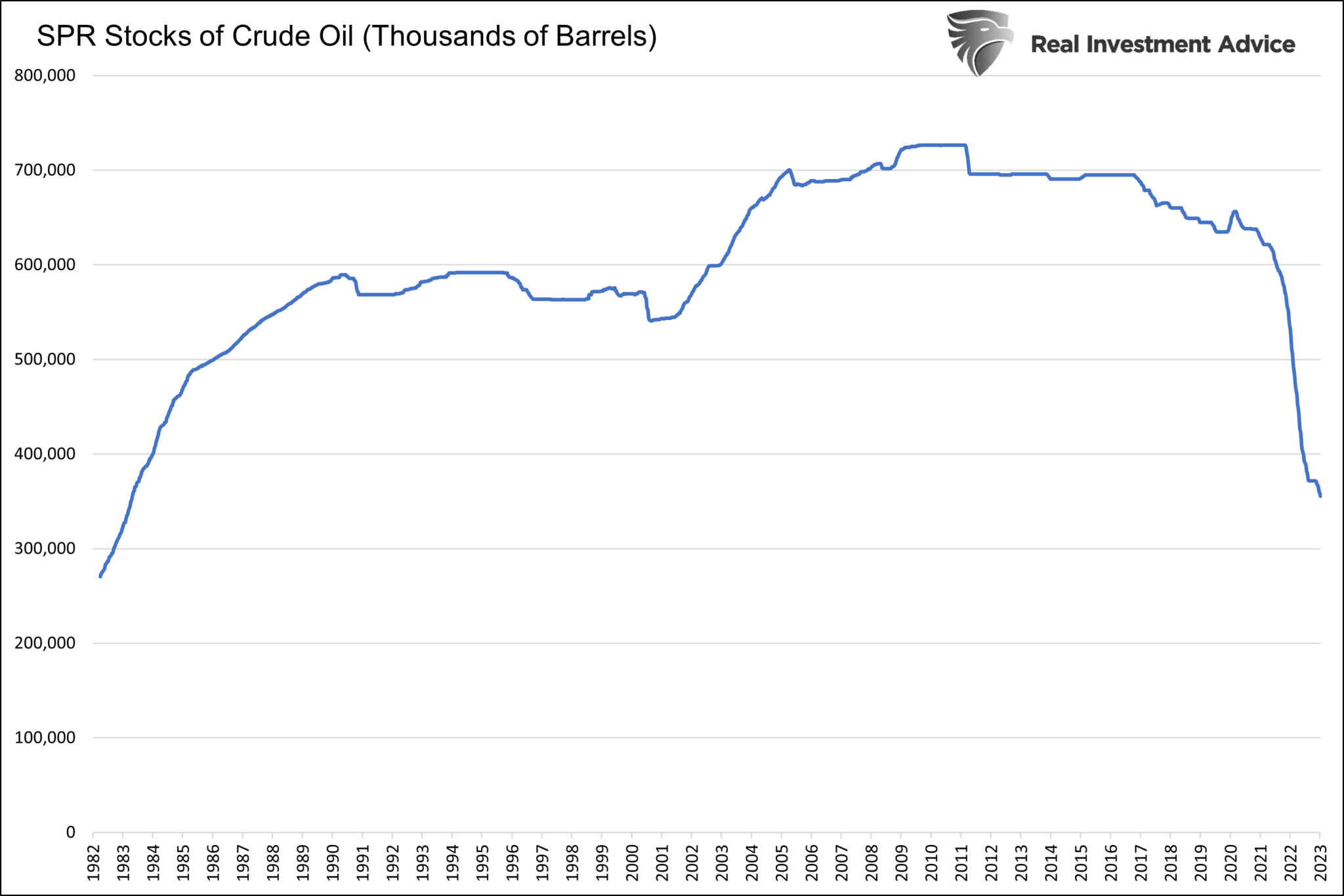

It appears Saudi Arabia would like to establish a floor for oil prices around the $70-$75/barrel level, with or without the help of fellow OPEC nations. Further, based on their comments, they are frustrated that Biden is not refilling the strategic petroleum reserve (SPR), as promised. In fact, despite Biden’s reassurances to Saudi Arabia, the SPR oil stocks are back to levels last seen in 1983. Lastly, the Saudi Arabian government has aggressive fiscal spending plans. Per the AP: “The International Monetary Fund estimates the kingdom needs $80.90 per barrel to meet its envisioned spending commitments, which include a planned $500 billion futuristic desert city project called Neom.“

What To Watch Today

Earnings

Economy

Market Trading Update

Yesterday, the ISM Services Index (or Non-Manufacturing) came in a bit weaker than expected, although it remained in expansionary territory. The subcomponents of the index were also weaker than expected across the board, with employment slipping into contractionary territory.

As I noted recently, services comprise nearly 80% of economic growth, and the decline in the ISM index suggests weakening activity in the biggest segments of the economy. Again, while ISM Services is still in expansionary territory, it is so just barely and suggests that weaker economic activity is occurring. Such is not a positive for currently overly-optimistic earnings expectations and a running bull market in stocks.

However, stocks rallied yesterday following the news as the data does suggest the Federal Reserve may continue to “pause” on further rate hikes despite the strong employment report last Friday. There is still a lot of “hope” on the market’s behalf, but the rally continues to push the market to the upper end of its trading range and is now extremely deviated from the 50-DMA. Next week’s Fed meeting could catalyze a short-term selloff in the market if the Fed is more “hawkishly” biased and hints at further rate hikes. Whatever the reason, the markets must work off the overbought conditions before advancing further.

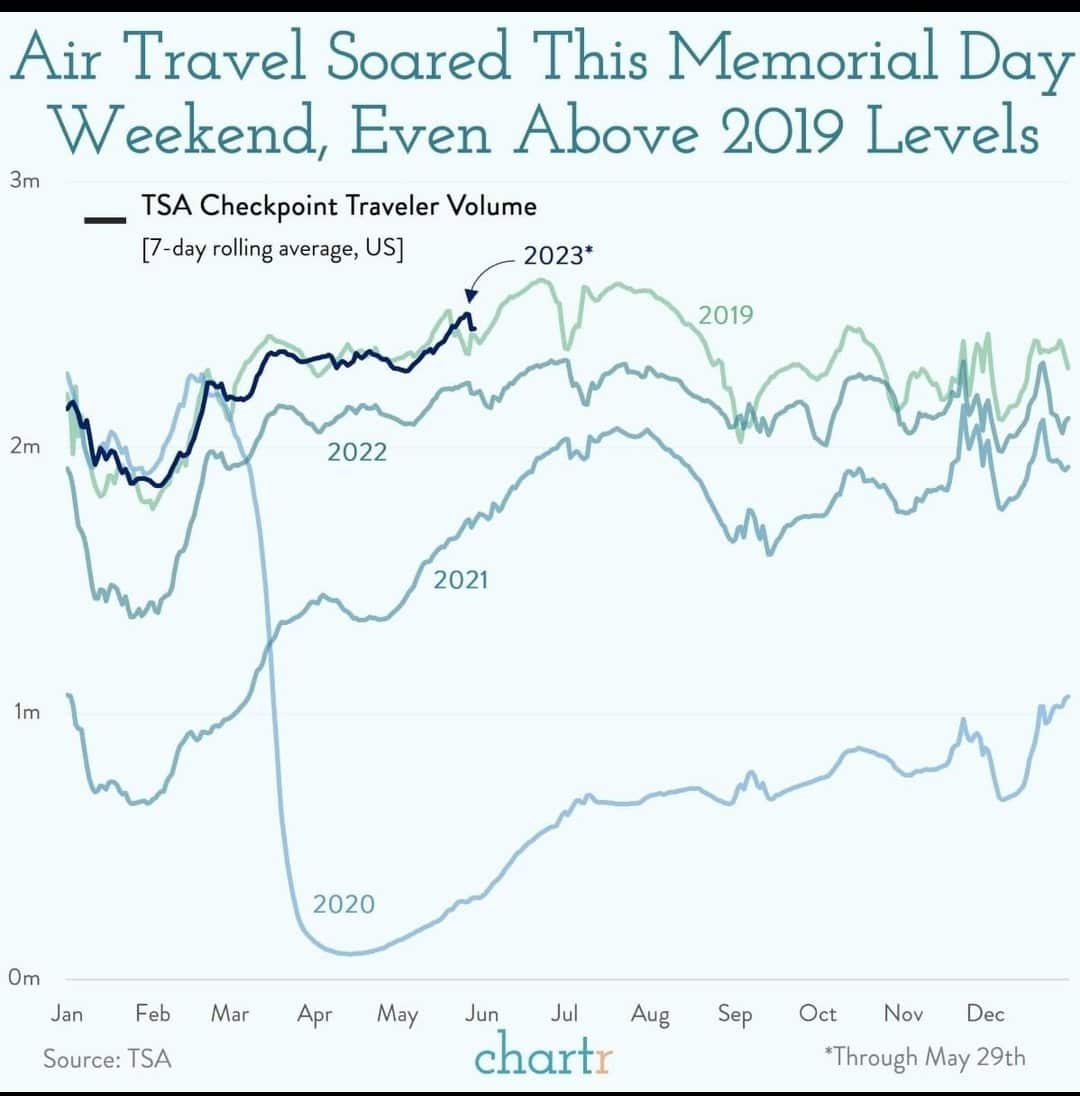

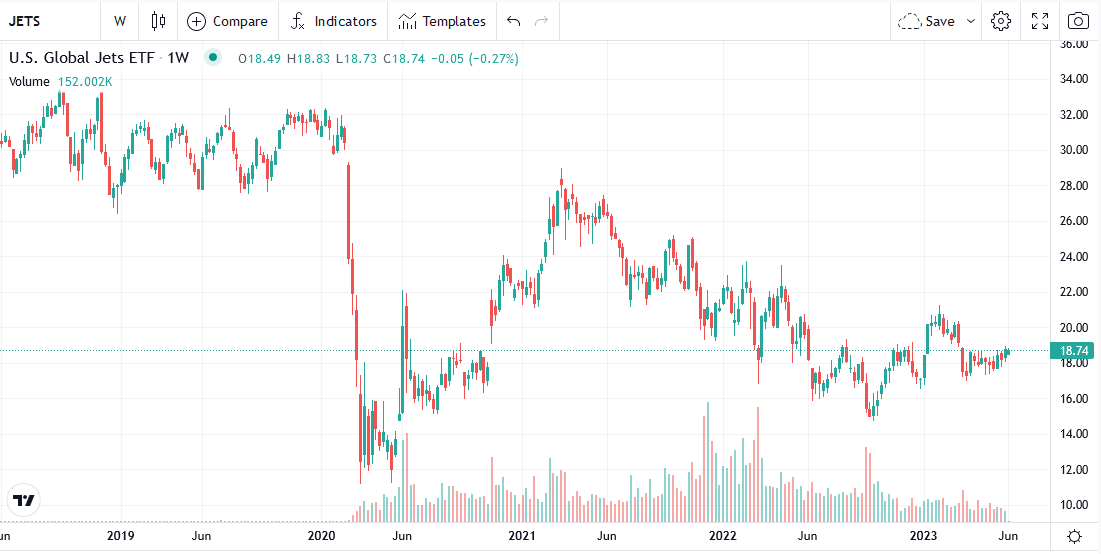

Air Travel is Back, But Not JETS

Courtesy of Chartr, the graph below shows air travel is finally back to pre-pandemic levels. Despite the recovery in air travel, airline stocks are still well below pre-pandemic levels. JETS is an ETF holding airline stocks. Its four top holdings, Delta, United, Southwest, and American, account for 40% of its assets. The graph shows that JETS fell from $32 to $12 per share in 2020. Since then, it has only recovered about a third of the loss.

Delta, the largest holding, has seen its revenue grow by almost 10% since the pandemic, yet its earnings (EBITDA) are still slightly below pre-pandemic levels. Despite the lower stock price, Delta’s price-to-earnings ratio is on par with pre-pandemic levels at 8. Before the pandemic, airlines were a challenging sector to invest in. With higher inflation and recession worries, valuations may stay at depressed levels.

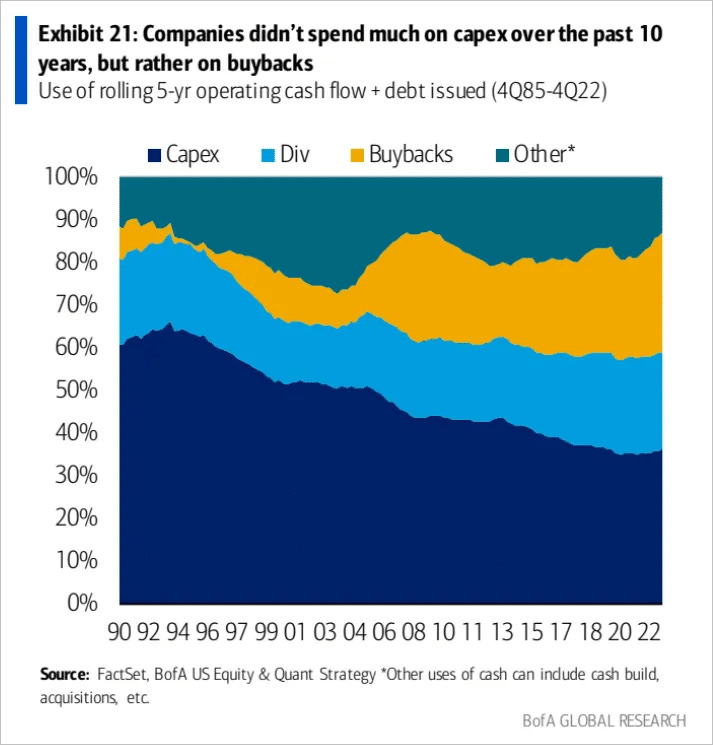

Less Capex, Less Productivity

The graph below shows that companies have increasingly provided more of their profits to shareholders via dividends and buybacks, leaving less for capital expenditures (CAPEX). Over the last decade, shareholders have favored stocks that buy back their shares. In turn, higher share prices have motivated stock-incentivized executives to buy back more shares. The future consequence, which executives do not acknowledge, is reduced productivity. Fortunately for executives, that is a future problem.

Total Factor Productivity (TFP) is a calculation of economic productivity by the San Francisco Fed. Productivity growth, along with economic growth, has been trending lower for thirty years. The five-year productivity growth rate is down to .72%. Productivity and demographics are the most critical factors determining economic growth. Given current demographic trends and the preference of companies to prop up their share prices with buybacks versus longer-term investments, we should expect the nation’s long-term economic growth rate to continue to decline as it has for the last thirty-plus years.

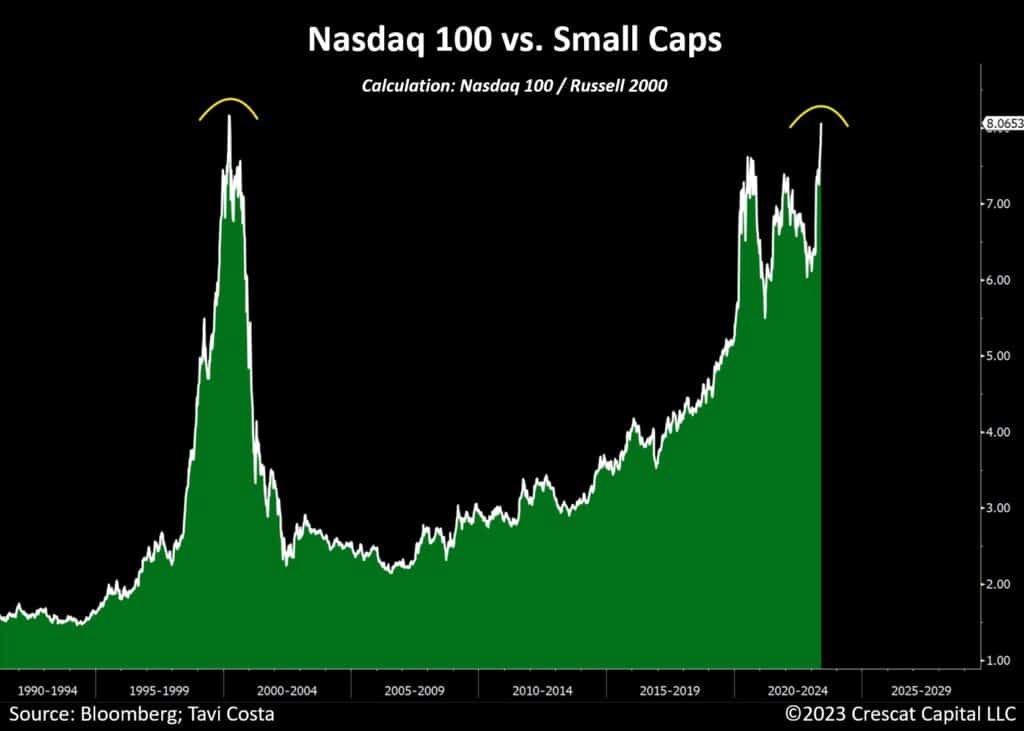

Small Caps vs. the Nasdaq Reminds Tavi Of The Dot Com Bubble

The following graph and commentary are courtesy of Tavi Costa of Crescat Capital.

The ratio of Nasdaq 100-to-Russell 2000 is now retesting the peak of the tech bubble levels. This situation, similar to today, where smaller companies perform poorly compared to large-cap companies, was a critical precursor of the tech bust. An important reminder: It’s not all about growth; it’s about the price one pays for that expected improvement in fundamentals.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.