Could monetary conditions be supportive of the “soft landing” scenario? While the “recession” versus “no recession” debate rages, there is a precedent for a “soft landing” scenario. Such is where the economy slows substantially but avoids a deeper contraction. However, the problem with that is that it works against the Fed’s mission of bringing down inflation.

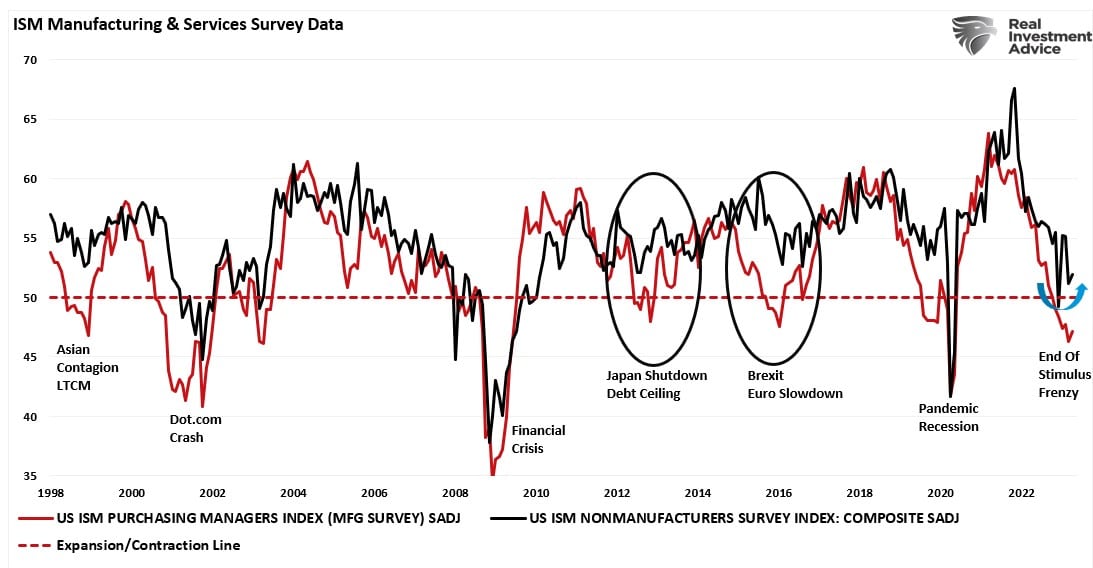

In 2011, the world faced a manufacturing shutdown as Japan was shuttered by an undersea earthquake creating a tsunami. The flooding of Japan also sparked a nuclear meltdown. Simultaneously, the U.S. was entrenched in a debt ceiling debate, a debt downgrade, and threats of default. Given the combination of events, the economy’s manufacturing sector contracted, convincing many of an impending recession.

However, as shown, that recession never happened.

The reason such was possible is that the service sector of the U.S. economy kept the economy afloat. Unlike in the past, where manufacturing was a significant component of economic activity, today, services comprise nearly 80% of each dollar spent.

This isn’t the first time we have seen the manufacturing side of the economy contract, but services remained robust enough to keep the overall economy out of recession. The economy similarly avoided a “recession” in 1998, 2011, and 2015.

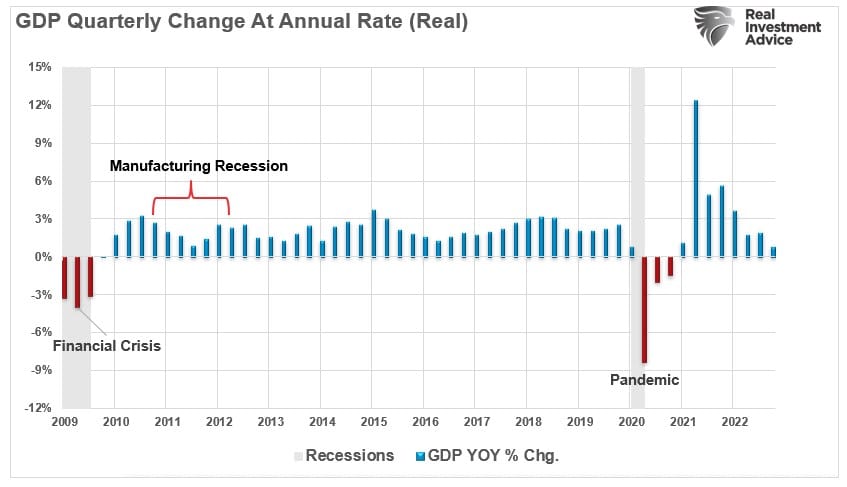

Another consideration is that the economy has already contracted sharply. A recession would be assured if the economy ran at its previous 2% rate. The difference is the contraction occurred with the economy at nearly 12% due to $5 Trillion in liquidity. The contraction from the peak is as significant as the Pandemic recession and the “Financial Crisis.”

Such will keep inflation above the Fed’s target rate without an economic contraction.

Monetary Conditions Providing Support

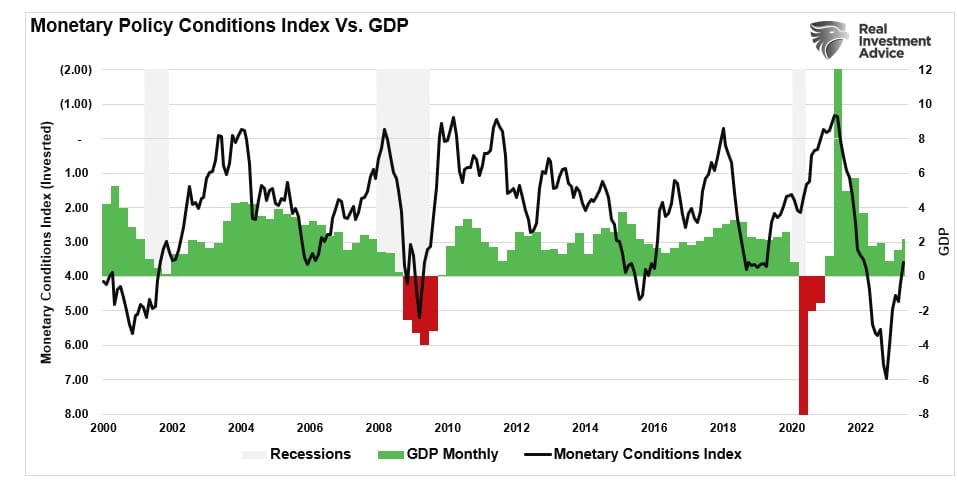

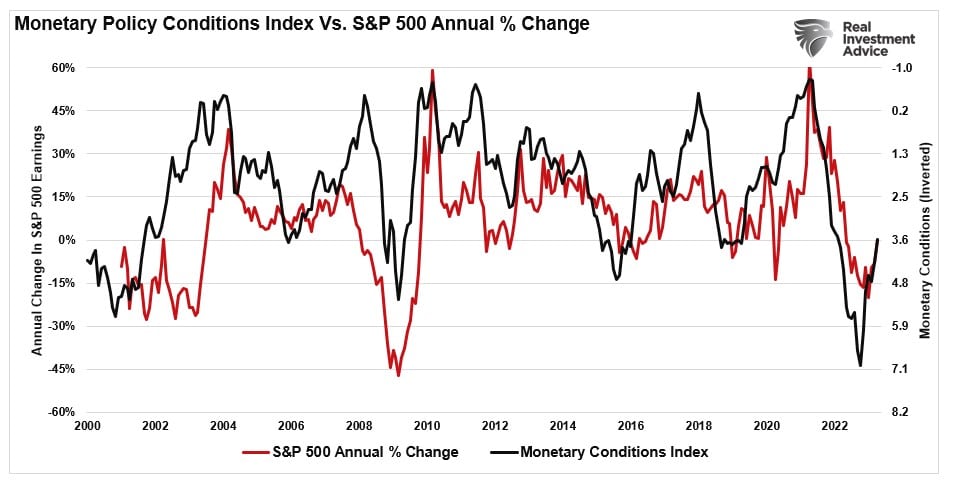

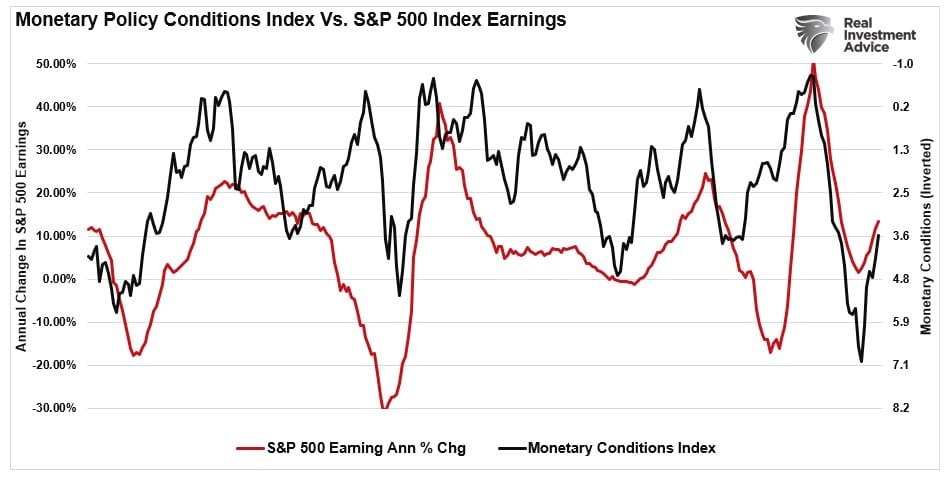

There is another problem facing the Fed. In a previous article on why the “Bulls May Not Like The Pivot,” I introduced a composite index that tracks changes to monetary conditions. Monetary conditions tightened significantly in 2022 as the Fed hiked rates and inflation surged from massive tranches of monetary support.

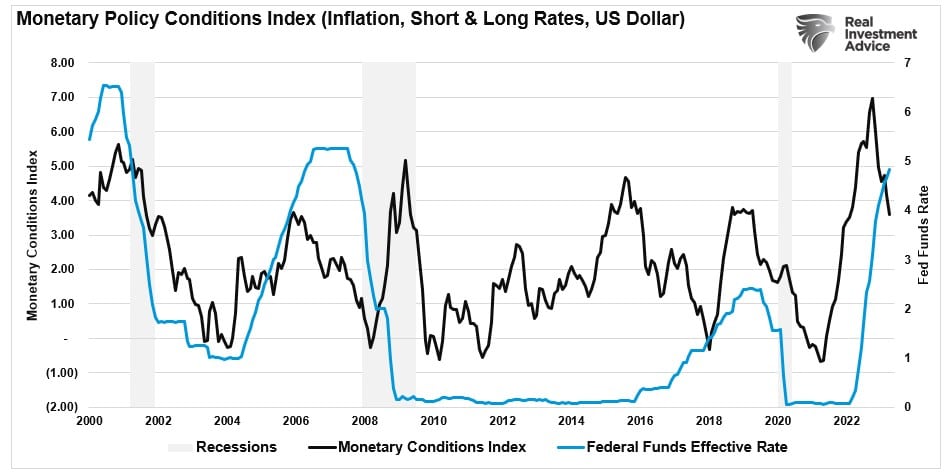

The “monetary policy conditions index” measures the 2-year Treasury rate, which impacts short-term loans; the 10-year rate, which affects longer-term loans; inflation which impacts the consumer; and the dollar, which impacts foreign consumption. Historically, when the index has reached higher levels, it has preceded economic downturns, recessions, and bear markets. To visualize the correlation, I have inverted the monetary conditions index so that “easier” monetary conditions correspond to rising economic growth.

It is worth noting that the monetary conditions index typically precedes Federal Reserve rate cuts.

Importantly, if the monetary conditions index suggests that economic growth will pick up later this year, such does explain the rally in the stock market since October of last year. As shown, there is a decent correlation between the monetary conditions index and the annual change in the S&P 500.

The reason for the optimism in the stock market is the expectation that earnings will increase over the next year. If monetary conditions point to strong economic growth, earnings should follow. Already, Wall Street analysts are boosting earnings expectations for 2023 and 2024.

The problem for the Fed is that higher asset prices ease monetary conditions, which will keep inflation elevated. Such works against the Fed’s goal of slowing economic growth, increasing unemployment, and reducing economic demand.

Working Against The Fed

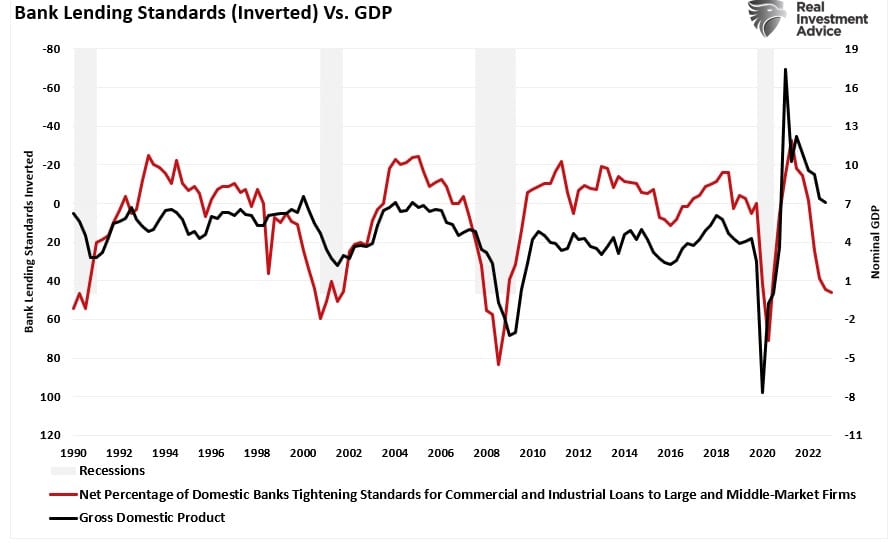

At the next Fed meeting, the Federal Reserve is widely expected to “pause” on hiking rates. Such was what the Fed alluded to at the last FOMC meeting suggesting the tighter bank lending standards are doing the work of additional rate hikes to slow economic growth. The chart below, which inverts the bank lending standards index, shows that tighter lending standards precede slower economic activity.

As noted above, the monetary conditions index suggests that financial conditions are indeed easing in the economy. Such is problematic for the Fed, which needs the opposite tighter conditions to bring down inflation towards their target rate.

From the market’s perspective, it has been rallying since October, hoping the Fed would pause its rate-hiking campaign and start cutting rates in the latter half of this year. However, the bullish case hinges upon:

- The economy avoiding a recession.

- Employment remains strong, and wages will support consumption

- Corporate profit margins will remain elevated, thereby supporting higher market valuations.

- The Fed will “pause” the tightening campaign as inflation falls.

So far, those supports have allowed investors to chase stock prices higher this year despite higher rates from the Fed. However, there is also a problem with those supports.

If the economy avoids a recession and employment remains strong, the Fed has no reason to cut rates. Yes, the Fed may stop hiking rates, but if the economy is functioning normally and inflation is falling, there is no reason for rate cuts.

However, sustained economic growth and low unemployment will keep inflation elevated, such leaves the Fed little choice but to become more aggressive in tightening monetary accommodation further.

I don’t know who eventually wins this particular tug-of-war, but the Monetary Conditions Index suggests that the Fed’s fight is far from over.