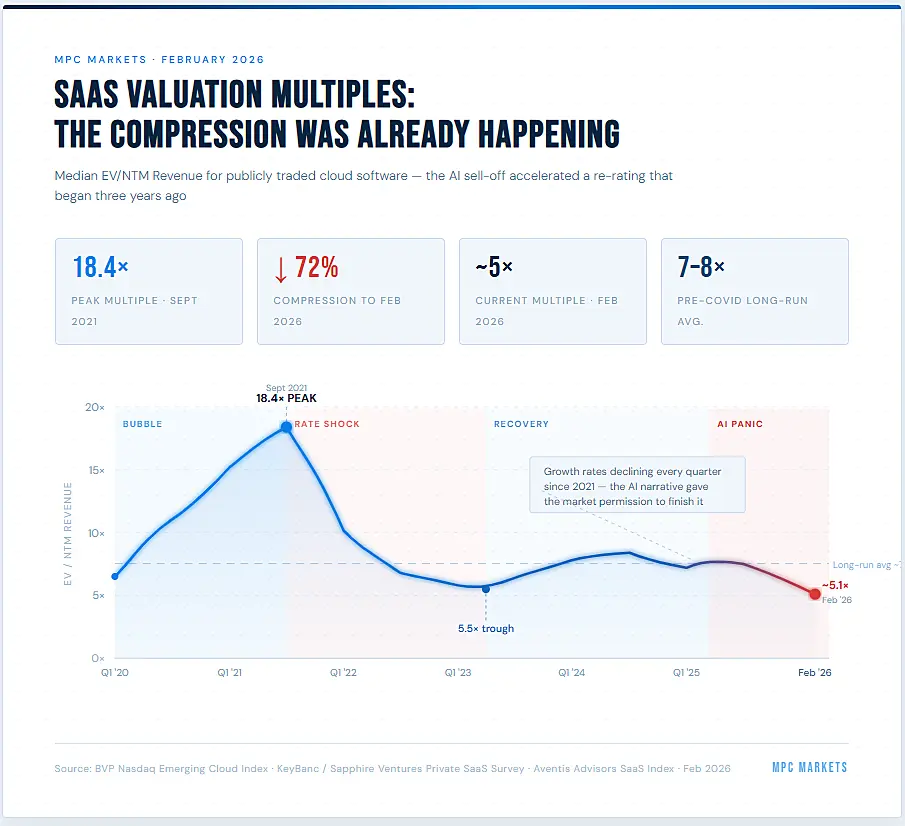

A specter is haunting Wall Street—the specter of the “SaaSpocalypse.” Since the iShares Expanded Tech-Software Sector ETF (IGV) peaked on September 19, 2025, it has fallen roughly 30%. For context, the broad technology indexes like XLK and QQQ are essentially flat over the same period, and the semiconductor ETF (SMH) is up 30%. Between mid-January and mid-February 2026 alone, approximately one trillion dollars was wiped from the collective value of software stocks, with the S&P North American Software Index posting its worst monthly decline since the 2008 financial crisis.

The catalyst was a series of AI product launches, most notably Anthropic’s Claude Cowork tool and OpenAI’s enterprise agent, Frontier, demonstrating that AI agents can now handle complex knowledge work autonomously. The market’s interpretation was simple. If AI agents can replicate what enterprise software does, then enterprise software is finished. That is the narrative that has taken hold in recent weeks. The consequence has been brutal. Workday is down 35% year-to-date. Adobe has shed 26%. Salesforce, 25%. Atlassian plunged 35% in a single week. Even Microsoft, the ultimate blue chip, fell by more than 10%.

The thesis is straightforward enough. Generative AI can now write code, automate workflows, and rapidly and cheaply create customized applications. Therefore, if enterprises can build their own “disposable software,” micro-apps tailored to specific workflows, instead of paying bloated subscription fees, then the traditional per-seat SaaS pricing model is dead. Potentially worse is that AI lowers barriers to entry, enabling more competitors to quickly replicate existing software. Such would compress margins and weaken the moats that once protected large software firms.

It is a compelling narrative. The question investors must answer is whether it is true.

Will AI Actually Kill Software Stocks? Not So Fast

Like most market narratives, the SaaSpocalypse contains some truth, a great deal of speculation, and several outright falsehoods. The most important rebuttal is that the value of enterprise software has never resided solely in its code. Enterprise software encodes institutional architecture. That architecture is the deep domain knowledge, compliance frameworks, workflow logic, and years of organizational customization that companies depend on to function. Think about it this way. If you are a medium to large enterprise dependent on data to service customers, maintain workflows, and fulfill orders, are you going to trust something that AI created that is potentially unreliable or error-ridden? Or, are you more likely to rely on software with deep local context, reliable outputs, and that has been rigorously tested and debugged over years of application use?

“Add deep workflow embedding to the mix and the picture becomes clearer still. When a SaaS platform is the system of record inside core banking, hospital EHRs, or government case management, replacement isn’t a technical decision, it’s an organisational trauma. Staff retraining, data migration, permission re-architecture, and regulatory re-certification make a rip-and-replace approach impractical, even when a cheaper AI-built alternative exists on paper.” – LiveWire

Furthermore, the underlying data does not support the skepticism either. Gartner’s February 2026 forecast projects worldwide software spending will grow 14.7% in 2026 to more than $1.4 trillion, accelerating from 11.5% growth in 2025. That represents roughly $180 billion in net new software spending in a single year. Global SaaS spending specifically is projected to rise from $318 billion in 2025 to $576 billion by 2029, according to Forrester. The reality is that enterprises are not abandoning software; they are spending more on it. As Mark Gardner recently noted:

“However, this sell-off is analytically lazy. And it’s being driven, at least in part, by the very technology it fears hallucinating on its own research. We believe the difference this time is that investors have the opportunity to look through the noise and identify the SaaS businesses where the structural moats are not just intact, they’re actually widening.

It was also fascinating to listen to Salesforce CEO Marc Benioff in CRM’s latest quarterly earnings report. He specifically addressed the panic, invoking the term “SaaSpocalypse” at least 6 times. His point was blunt: this is not Salesforce’s first existential scare, and AI is making their products more valuable, not less. The company introduced a new metric, agentic work units, designed to capture the output-driven value of its AI-enabled platform. More importantly, Gartner’s own analysts note that GenAI features are now ubiquitous across enterprise software and are increasingly costly. In other words, the cost of software is going up precisely because of AI, not in spite of it. There is a meaningful difference between a technology that changes how software works and one that makes software unnecessary.

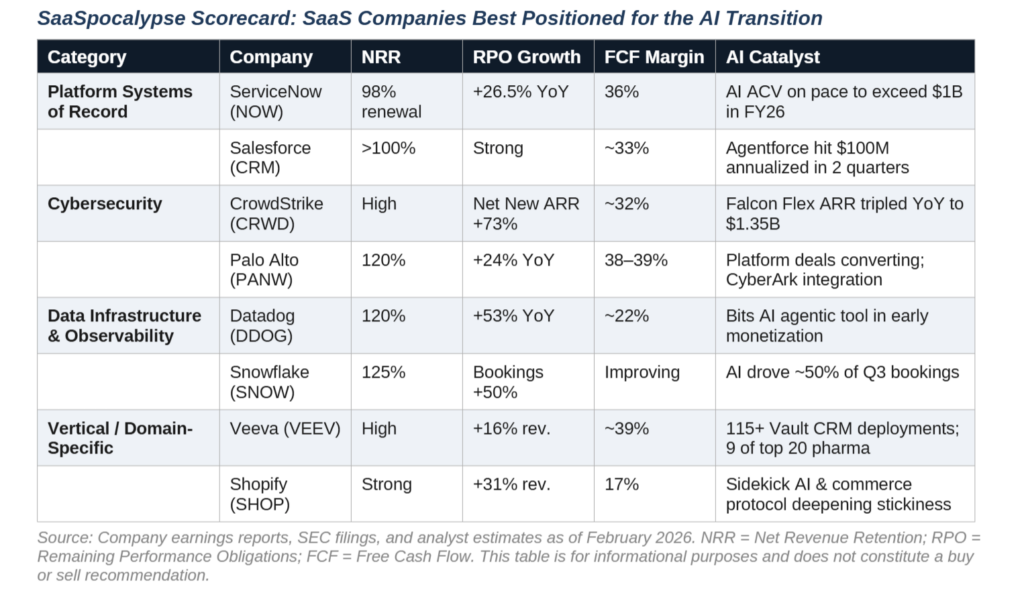

Survivors and Thrivers: Which SaaS Companies Have the Strongest Moats

If the SaaSpocalypse narrative proves to be more panic than prophecy, the critical task becomes identifying which companies will emerge stronger. Forrester’s research provides a useful framework: horizontal point-solution vendors with low switching costs and weak enterprise integration face genuine existential risk. But vertical- or domain-specific SaaS vendors, those addressing complex industries like healthcare, manufacturing, or financial services, or those controlling unique proprietary data, have a substantially greater chance of survival and even growth.

Furthermore, even before the “SaaSpocalypse” began, the revaluation of these companies was already well underway, and current prices are nowhere near the 2021 froth levels.

Therefore, as investors, we need to think about “separating the wheat from the chaff.” While valuations and fundamentals are important, the key will be finding the companies best positioned in the market. Those companies share several characteristics.

- First, platform-scale incumbents that serve as systems of record, Salesforce, Microsoft, Oracle, and ServiceNow, possess deep integration into enterprise workflows that cannot easily be replicated by a general-purpose AI agent. These companies are rapidly embedding AI agents alongside their existing deterministic processes, particularly for regulated industries.

- Second, cybersecurity firms like Palo Alto Networks and CrowdStrike occupy a category where AI is additive rather than substitutive. As enterprises deploy more AI systems, the attack surface expands.

- Third, data infrastructure and vertical SaaS companies that sit at the foundation of AI workloads or control proprietary domain data benefit directly from the same trend punishing commodity application vendors.

The table below highlights eight companies across four categories whose reported metrics most closely align with the characteristics that separate durable SaaS businesses from vulnerable ones.

So, where do you start your process?

Investor Playbook: Metrics That Matter and How to Position

For investors, the current dislocation presents both a challenge and an opportunity.

The biggest challenge is overcoming the “fear of loss.” Loss-avoidance is an emotional behavior that impedes our ability to “buy low,” as we fear prices will keep falling indefinitely. However, logic and fundamentals quickly refute that concern. However, it is a “barrier to entry” that keeps investors sidelined when prices decline, even as opportunities increase.

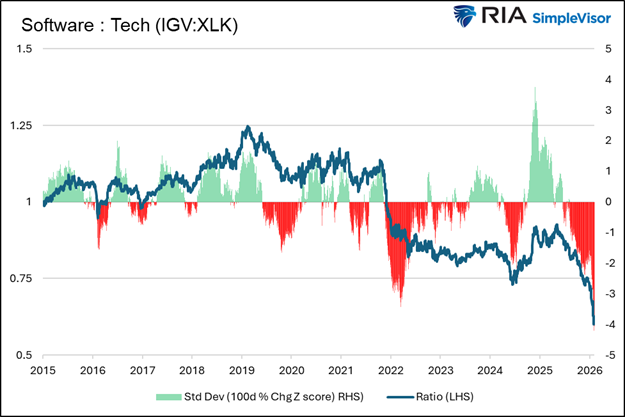

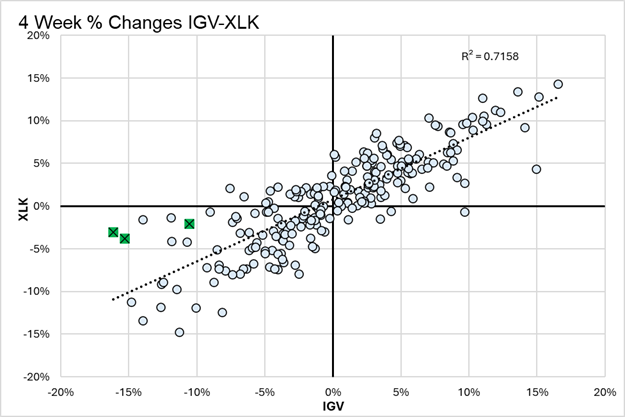

The statistical evidence of overshoot is significant. As Michael Lebowitz noted last week, the price ratio between IGV and XLK has diverged by nearly four standard deviations from historical norms over the past 100 days.

Based on the five-year relationship, either XLK is 10% overpriced, or IGV is 10% underpriced. When statistical relationships stretch this far, mean reversion eventually follows—though we caution that in environments where narratives are this powerful, divergences can persist longer than models suggest.

With this in mind, we suggest that doing your homework rather than listening to narratives is where the opportunity lies. Therefore, the right approach is to be surgical, rather than thematic. Rather than buying the entire beaten-down sector via IGV, which is okay if you only seek “average” returns, we think focusing on individual company fundamentals will yield better results. Therefore, here are a few metrics you can use to separate genuine AI beneficiaries from vulnerable incumbents. These metrics include:

- Price-To-Earnings Growth (PEG): Measures the current price of the shares relative to their expected growth rate of earnings in the future. PEG ratios of 1 or less are considered to be cheap valuations.

- Net Revenue Retention (NRR): Measures whether existing customers are spending more over time. Companies maintaining NRR above 120% demonstrate that AI features are expanding wallet share rather than cannibalizing it.

- Remaining Performance Obligations (RPO): Measures whether forward demand is accelerating or decelerating, cutting through the noise of quarterly revenue.

- Free cash flow margins: Reveals whether companies can fund their AI transformation internally or must dilute shareholders to compete.

- AI attach rates: Measures the percentage of customers adopting AI-powered product tiers. It provides a real-time indicator of whether the AI transition is generating revenue or merely generating press releases.

A sustained SaaS recovery, as EBC Financial Group’s analysis notes, will likely require at least two of three conditions:

- More accommodative financial conditions,

- Enhanced earnings visibility, and/or

- A shift in the narrative from viewing AI as a threat to recognizing its monetization potential.

We think the latter two are the most likely.

For now, investors should remain cautiously positioned. Make small bets, manage your risk exposure, and give yourself plenty of time. The recognition of value often takes longer than logic would suggest, particularly when negative momentum is strong.

The SaaSpocalypse makes for dramatic headlines, but the idea that AI agents will simply devour enterprise software whole ignores both the data and the institutional complexity of the businesses being disrupted. The real risk for investors is not that they are too slow to sell their SaaS holdings. It is that they eventually get stampeded by market panic into undervaluing companies whose competitive positions are, in many cases, strengthening.

Discipline, not panic, is the appropriate response.

.