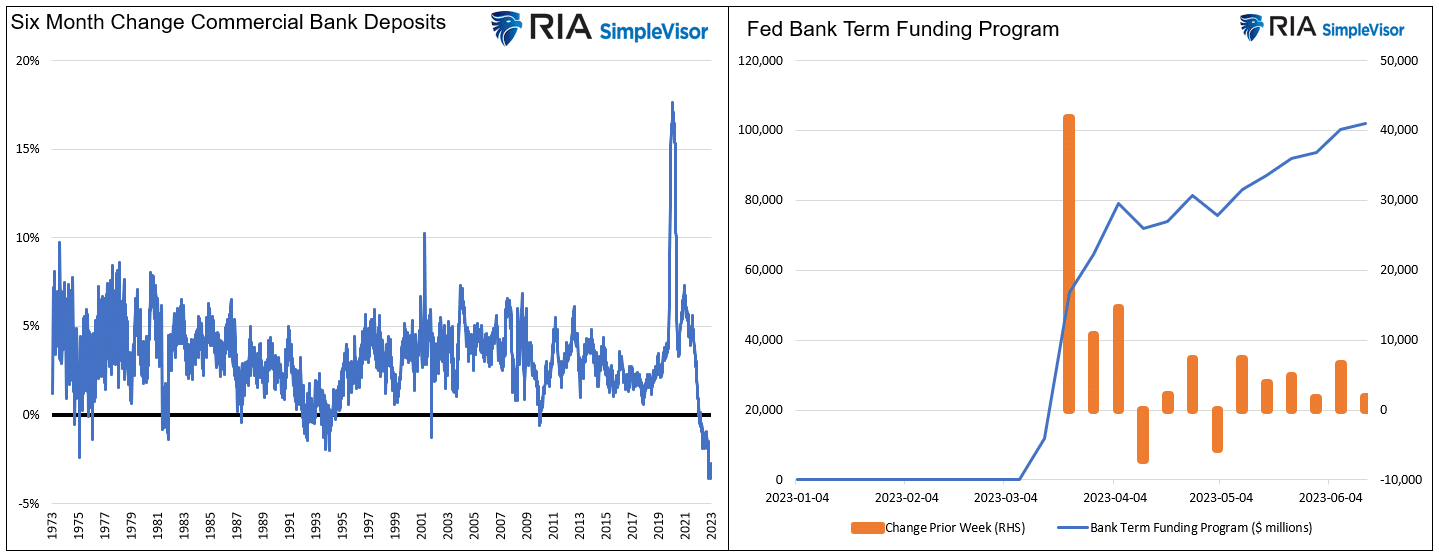

In mid-March, Silicon Valley Bank failed, and it appeared many smaller regional banks were facing the same bankruptcy-inducing problems. Large and smaller regional banks were losing deposits to higher-yielding money market funds. As a result, the regional banks had to recognize losses on loans and securities. The losses were predominately a function of higher interest rates, not credit related. The Fed reacted quickly, offering banks a line of credit to replace deposits. Banks could use the line of credit or borrow money, but either replacement has sharply steeper funding costs than the near-zero interest rate deposits they lost.

Over the last six months, deposits at commercial have fallen by 3%. Such may not seem like a lot, but it’s the largest decline in over 50 years. Also, consider that many banks are leveraged 8-10x or more. Consequently, for each 1% of deposits they lose and don’t replace, they must sell approximately 8-10% of its assets. Almost all bank assets are in a loss position. Recently, deposits have stabilized and started rising slightly. Also helping is that the Fed’s Term Funding Program has added over $100 billion to bank liabilities, largely offsetting the loss of deposits. While the crisis is suspended, banks still have sizeable unrealized losses on their balance sheets. The problem will fade if deposits stop fleeing banks and yields fall. However, banks will face rising credit losses if yields decline due to economic weakness.

What To Watch Today

- No notable reports today

Market Trading Update

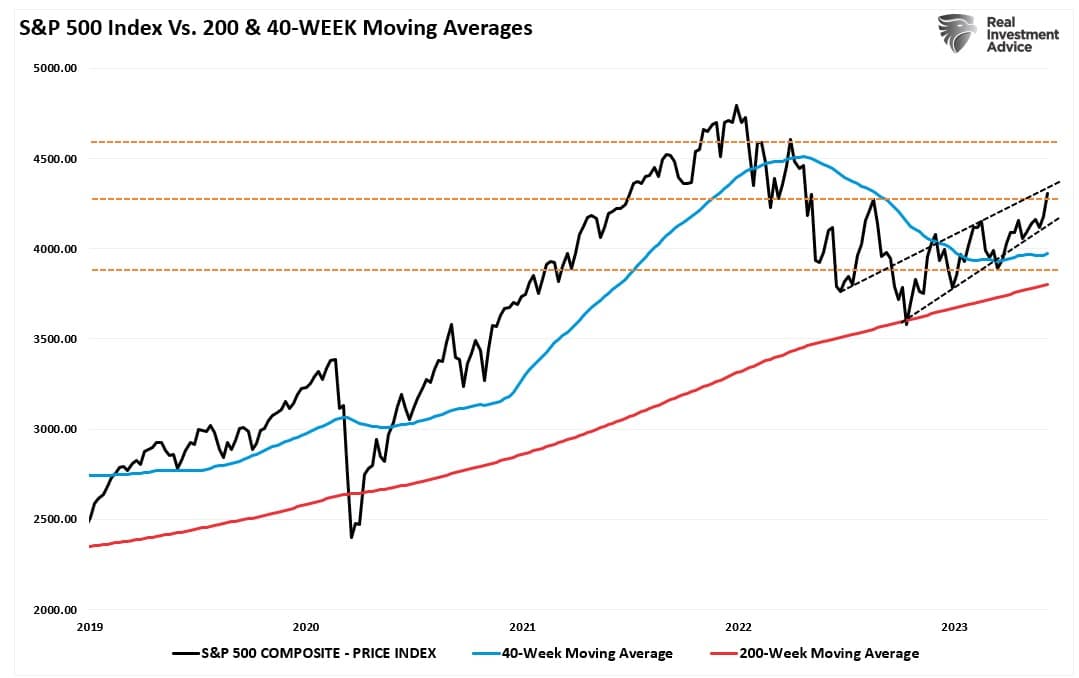

This bullish market is getting harder to deny as many indicators continue to improve. Last week, we reviewed our previous commentary discussing that the break above resistance would suggest a continued move to our target of 4300.

“The S&P 500 has scored seven weekly closes above its 40-week moving average, which is a positive sign. In addition, the market has cleared the 40-week DMA downtrend line from January and December 2022, suggesting a potential bullish turn in the trend. Assuming supports hold, the next major resistance beyond the post-FOMC peak at 4195 is the August 2022 peak at 4325 (orange dashed line).” – March 7th

This past week, the FOMC opted to “skip” a rate hike to monitor the lag effect of their previous actions on the economy. To wit:

“Nearly all committee participants expect it will be appropriate to raise interest rates somewhat further by the end of the year. But at this meeting, considering how far and how fast we’ve moved, we judged it prudent to hold the target range steady. The committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

While the statement is hawkish and suggests that the Fed could hike rates further to combat inflation, the markets have dismissed the impact of every rate hike this cycle. The break above 4400 removed minor resistance and put 4535 as the next major Fibonacci resistance level. After that, it’s essentially the all-time high as the last major roadblock.

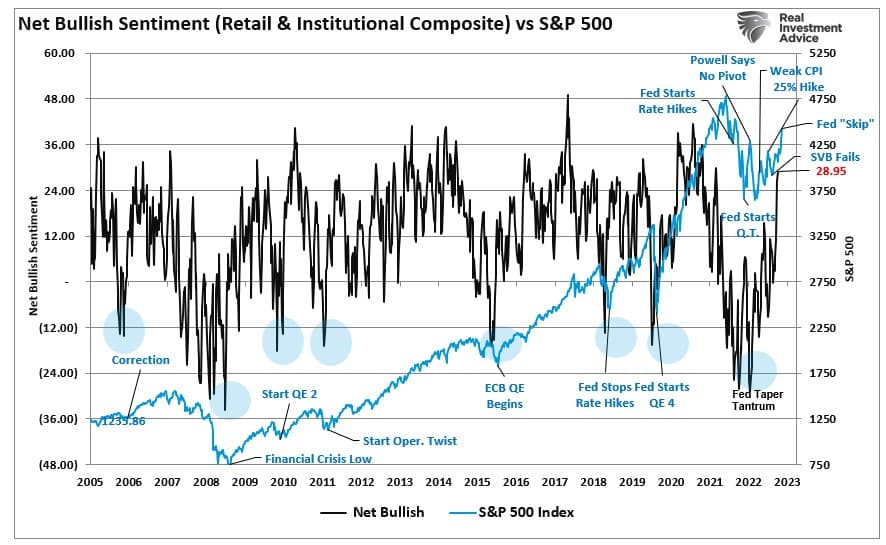

As noted on Tuesday, the rally has finally convinced the bears to come off the sidelines, with professional and retail investors getting substantially more “bullish” over the last two weeks.

As discussed previously, the Fed is in a difficult position as rising equity prices boost consumer confidence. With the Fed trying to reduce demand to cool inflation by tightening liquidity, rising stock market prices work against that agenda. Nonetheless, the market has found a new reason to be bullish on the “artificial intelligence” wave.

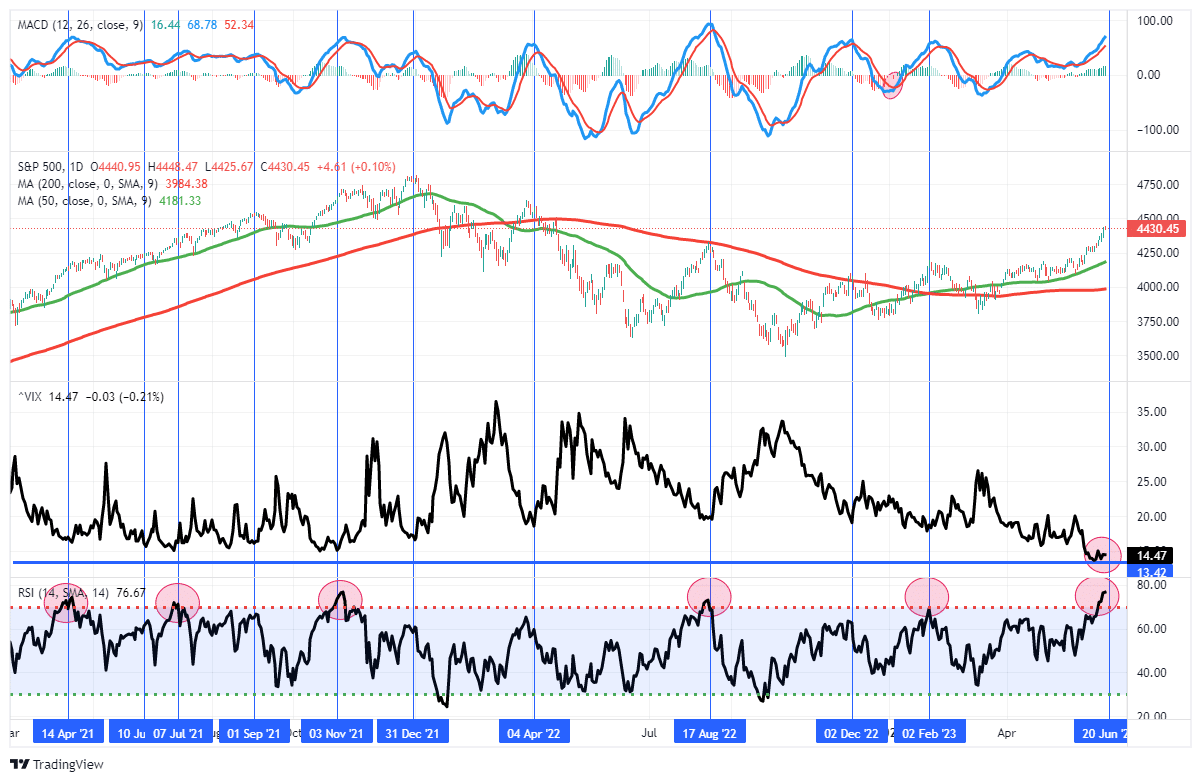

This past week, the market pushed well past our previous price target and is moving well into 3-standard deviations above the 50-DMA. Furthermore, the market is very overbought on multiple levels. Lastly, the volatility index is at extremely low levels, which has almost uniformly preceded corrections of 5-10% during both bull and bear markets.

However, what does that mean? While there are many reasons to be bearish, the bullish market environment suggests that such concerns are fading. For now, bullish market technicals appear to remain intact, and pullbacks are likely buying opportunities short term

The Week Ahead

The holiday-shortened week following last week’s plethora of economic data and Fed meeting leave little for this week. That said, Jerome Powell will testify to Congress on Wednesday and Thursday. We suspect he will elaborate on the rate hike pause and shine light on what economic data the Fed is using to inform its policy decisions.

Other than Powell and a host of other Fed members speaking, economic data will be light. As we recently noted, keep an eye on jobless claims data on Thursday, as it is a good leading indicator of the labor market.

The ECB Remains Well Behind the Fed

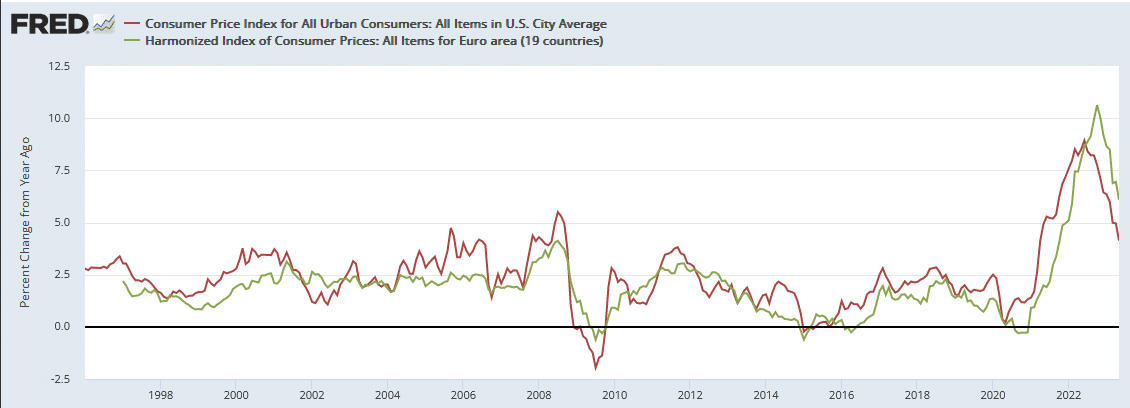

The ECB raised their key deposit rate by 25bps to 3.50%. The Eurozone, like the U.S., is trying to tame high inflation. The Fed has been among the most aggressive central banks raising rates by 5% in a year. The European Central Bank (ECB) has taken action but woefully lags the Fed, as the graph below shows. The ECB’s real interest rate (adjusted for inflation) has risen but is still more accommodative than the decade leading to the pandemic. On the other hand, the Fed has pushed real Fed Funds into restrictive territory.

Despite the big policy difference, inflation rates and trends between the U.S. and the eurozone are not that different. The U.S. CPI peaked at a lower level than the eurozone. However, they are both following the same path. Some may examine the graph and inflation data and question whether central bank monetary policy matters. They must consider that significant borrowing by eurozone companies and countries occurs in U.S. dollars. Therefore, Fed policy plays a significant role in European economic activity and inflation. The Fed has played a role in reducing global inflation, allowing banks, like the ECB, to run more stimulative policies.

El Nino Returns with Risks for Property Insurers

The El Nino weather pattern is back after a seven-year hiatus. Per Reuters: “The last time an El Nino was in place, in 2016, the world saw its hottest year on record.” The chart below, courtesy of Macrobond, measures the Southern Oscillation Index (SOI), a gauge of sea level pressure. The second chart measures global economic costs due to extreme weather. As the graph shows, there were outsized economic costs the last two times the SOI reached the current level or was lower. Per Macrobond:

The more negative the value (SOI), the more severe the El Nino – making the sudden shift in May concerning: the SOI plunged from 0 to -18.5.

The second table from Reinsurance News shows the top ten largest U.S. property and casualty companies ranked by 2021 net premiums. If the quickly declining SOI results in more property damage to the U.S., shares of the companies below may underperform.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.