It is easy to suggest the economy is booming when your net worth is in the hundreds of millions, if not billions, of dollars, or when your business, and your net worth, directly benefit from surging asset prices. This was the consensus from the annual gaggle of the ultra-rich, politicians, and media stars in Davos, Switzerland this past week.

As J.P. Morgan Chase CEO Jamie Dimon told CNBC on Wednesday the stock market is in a “Goldilocks place.”

Of course, it is when you bank receives an annual dividend from the Federal Reserve’s balance sheet expansion. This isn’t the first time I have picked on Dimon’s delusional view of the world. To wit:

“This is the most prosperous economy the world has ever seen and it’s going to be a very prosperous economy for the next 100 years. The consumer, which is 70% of the U.S. economy, is quite strong. Confidence is very high. Their balance sheets are in great shape. And you see that the strength of the American consumer is driving the American economy and the global economy. And while business slowed down, my current view is that, no, it just was a slowdown, not a petering out.”

Jamie Dimon during a “60-Minutes” interview.

If you’re in the top 1-2% of income earners, like Jamie, I am sure it feels that way.

For everyone else, not so much. Here are some stats via the WSJ:

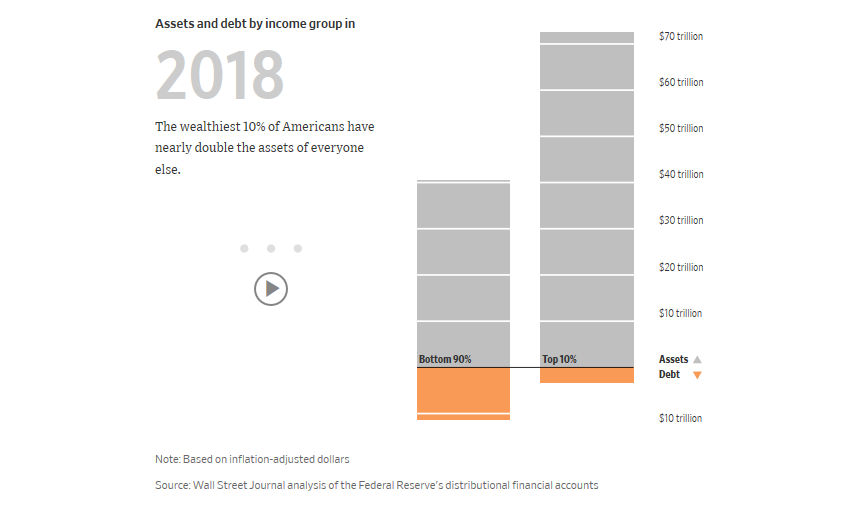

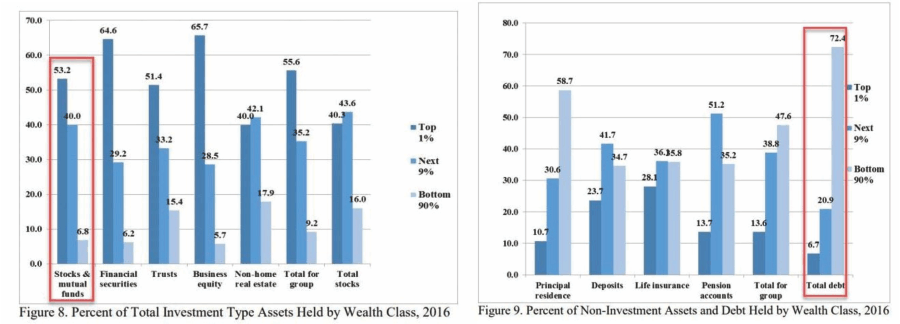

“The median net worth of households in the middle 20% of income rose 4% in inflation-adjusted terms to $81,900 between 1989 and 2016, the latest available data. For households in the top 20%, median net worth more than doubled to $811,860. And for the top 1%, the increase was 178% to $11,206,000.”

Put differently, the value of assets for all U.S. households increased from 1989 through 2016 by an inflation-adjusted $58 trillion. A full 33% of that gain—$19 trillion—went to the wealthiest 1%, according to a Journal analysis of Fed data.

The problem that is missed is that the “stock market” is NOT the “economy.”

This is a point President Trump misses entirely when he tweets:

“Stocks are hitting record highs. You’re welcome.”

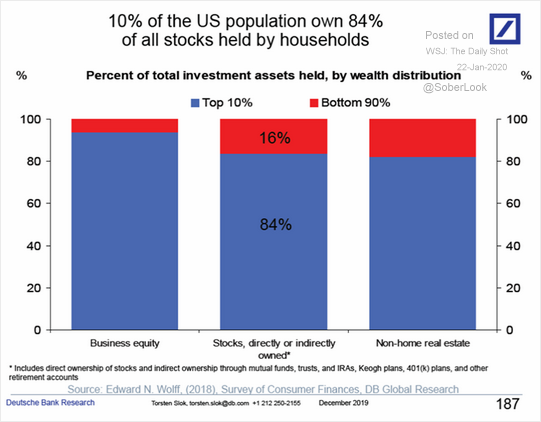

As discussed earlier this week, 90% of the population gets little, or no, direct benefit from the rise in stock market prices.

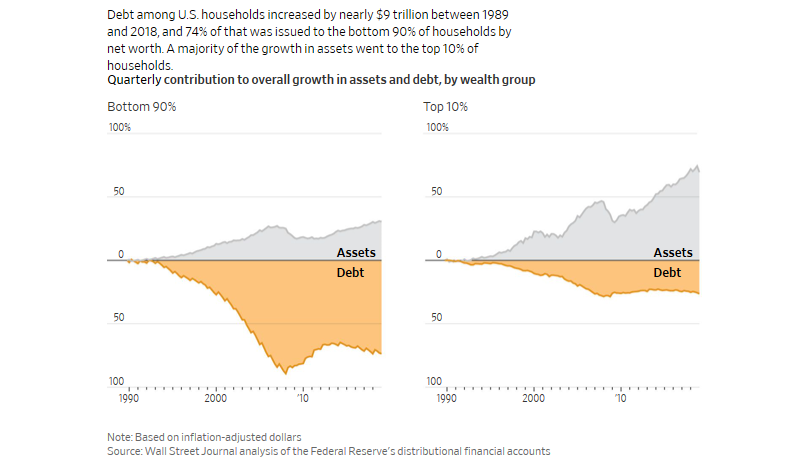

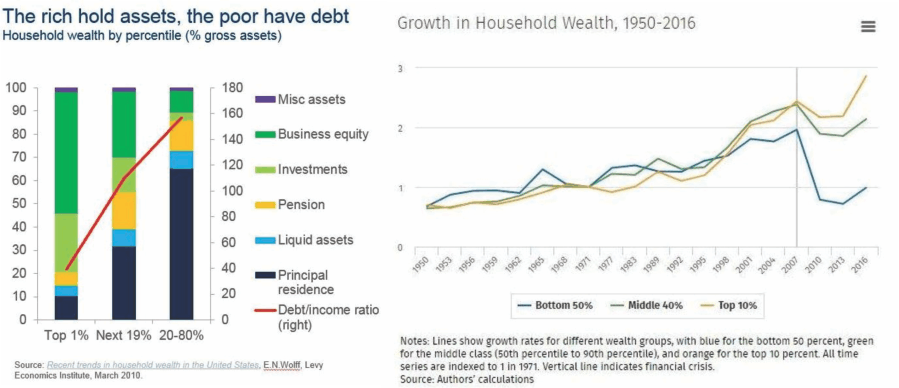

Another way to view this issue is by looking at household net worth growth between the top 10% and everyone else.

Since 2007, the ONLY group that has seen an increase in net worth is the top 10% of the population. This is not economic prosperity. This is simply a distortion of economics.

Another example of President Trump’s misunderstanding of the linkage between the economy and the stock market was displayed in his presser on Wednesday.

“Now, had we not done the big raise on interest [rates], I think we would have been close to 4% [GDP]. And I – I could see 5,000 to 10,000 points more on the Dow. But that was a killer when they raised the [interest] rate. It was just a big mistake.” – President Donald Trump via CNBC

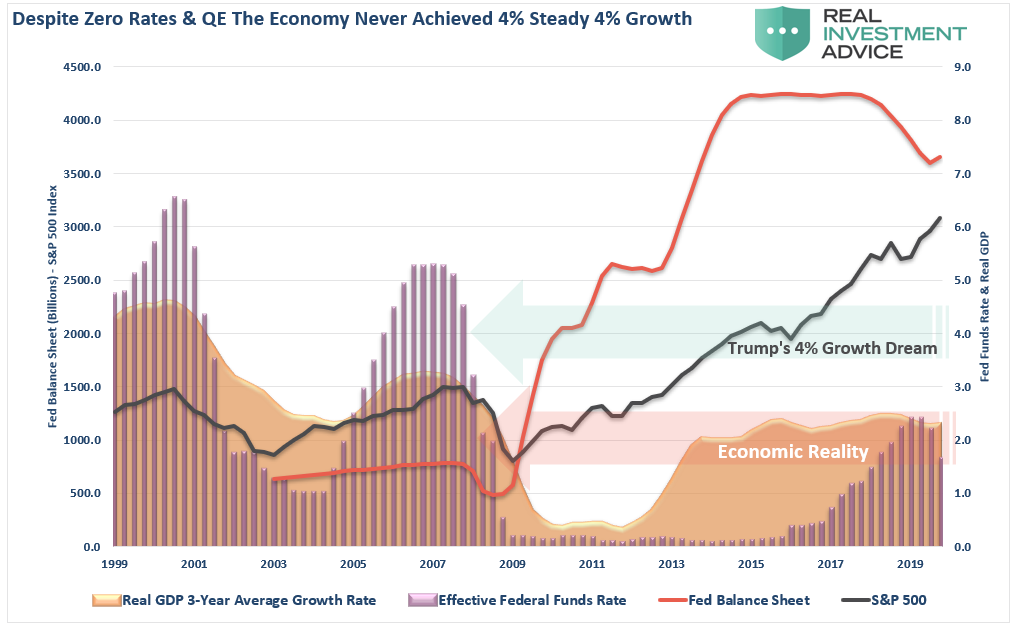

That is not actually the case. From 2009-2016, the Federal Reserve held rates at 0%, and flooded the financial system with 3-consecutive rounds of “Quantitative Easing” or “Q.E.” During that period average real rates of economic growth rates never rose much above 2%.

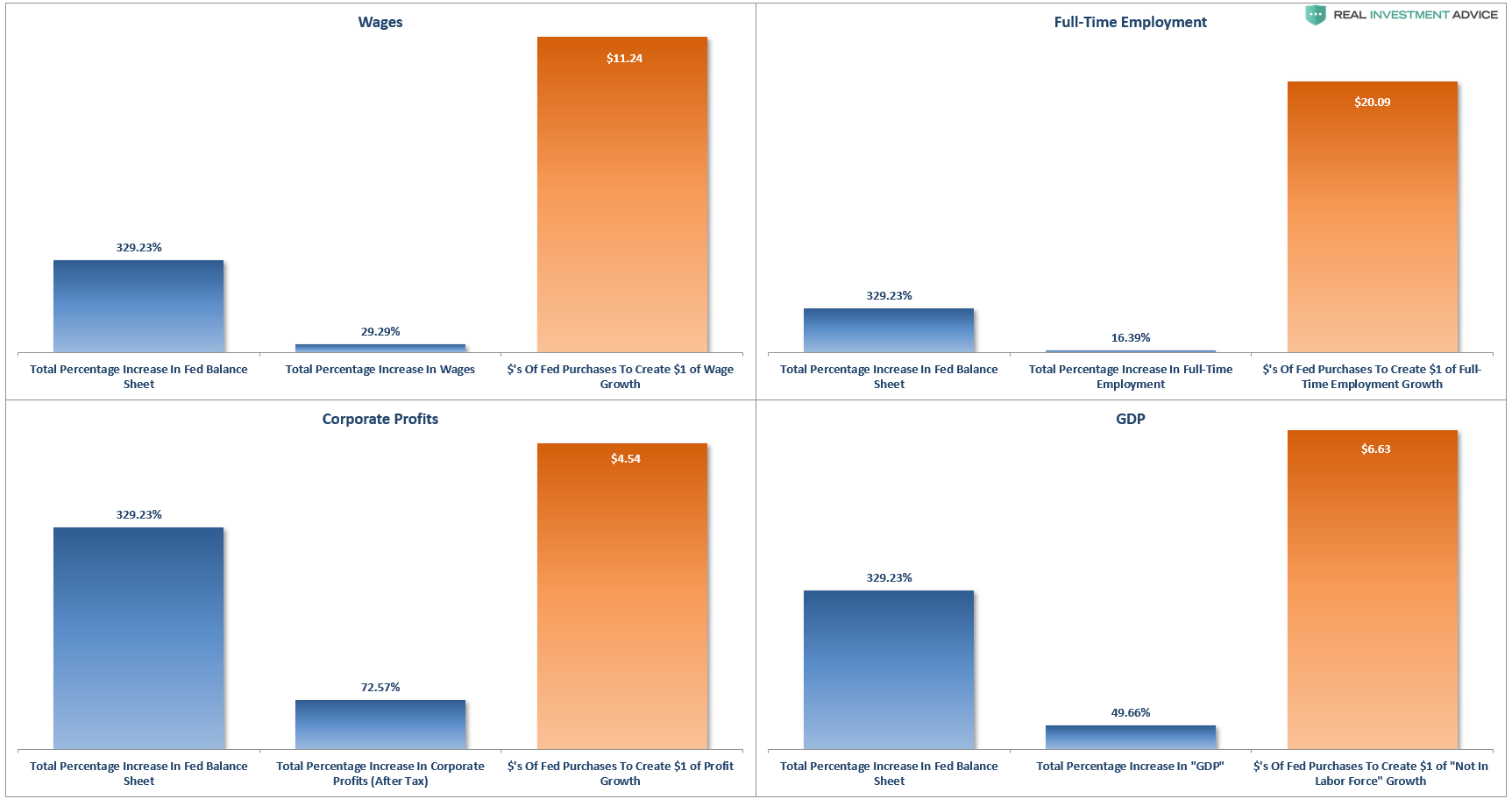

Yes, asset prices surged as liquidity flooded the markets, but as noted above “Q.E.” programs did not translate into economic activity. The two 4-panel charts below shows the entirety of the Fed’s balance sheet expansion program (as a percentage) and its relative impact on various parts of the real economy. (The orange bar shows now many dollars of increase in the Fed’s balance sheet that it took to create an increase in each data point.)

As you can see, it took trillions in “QE” programs, not to mention trillions in a variety of other bailout programs, to create a relative minimal increase in economic data. Of course, this explains the growing wealth gap which currently exists. Furthermore, while the Fed did hike rates slightly off of zero, and reduce their bloated balance sheet by a negligible amount, there was very little impact on asset prices or the trajectory of economic growth.

Not understood, especially by the Fed, is that the natural rate of economic growth is declining due to their very practices which incentivize non-productive debt. While QE and low rates may boost growth a little and for a short period of time, they actually harm future growth.

The Goldilocks Warning

While Jamie Dimon suggests we are in a “Goldilocks economy,” and President Trump says we are in the “Greatest Economy Ever,” such really isn’t the case. Despite a severe economic slow down globally, Dimon believes the domestic economy will continue to chug along with not enough inflation to push the Fed into hiking rates, but also won’t fall into a recession.

It is a “just right” economy, which will allow corporate profits to grow at a strong enough rate for stocks to continue to rise at 8-10% per year. Every year, into eternity.

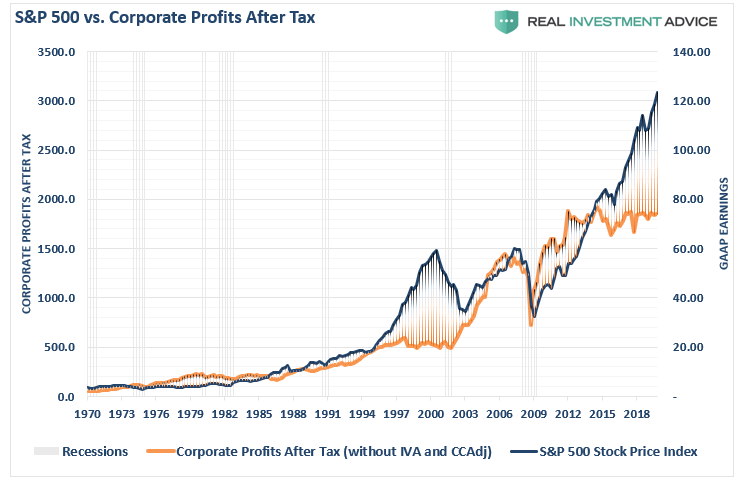

This is where Jamie’s delusion becomes most evident. As shown in the chart below, since 2014, the S&P 500 index has soared to record heights, yet corporate profits for the entire universe of U.S. corporations have failed to rise at all. This is the clearest evidence of the disconnect between the markets and the real economy.

Note: It is worth mentioning the last time we saw a period where corporate profits were flat, while stock market prices surged higher was from 1995-1999. Unfortunately, as is repeatedly the case throughout history, prices “catch down” with profits and not the other way around.

Interestingly, in the rush to come up with a “bullish thesis” as to why stocks should continue to elevate in the future, many have forgotten the last time the U.S. entered into such a state of “economic bliss.”

“The Fed’s official forecast, an average of forecasts by Fed governors and the Fed’s district banks, essentially portrays a ‘Goldilocks’ economy that is neither too hot, with inflation, nor too cold, with rising unemployment.” – WSJ Feb 15, 2007

Of course, it was just 10-months later that the U.S. entered into a recession, followed by the worst financial crisis since the “Great Depression.”

The problem with this “oft-repeated monument to trite” is that it’s absolute nonsense. As John Tamny once penned:

A “Goldilocks Economy,” one that is “not too hot and not too cold,” is very much the fashionable explanation at the moment for all that’s allegedly good. “Goldilocks” presumes economic uniformity where there is none, as though there’s no difference between Sausalito and Stockton, New York City and Newark. But there is, and that’s what’s so silly about commentary that lionizes the Fed for allegedly engineering “Goldilocks,” “soft landings,” and other laughable concepts that could only be dreamed up by the economics profession and the witless pundits who promote the profession’s mysticism.

What this tells us is that the Fed can’t engineer the falsehood that is Goldilocks, rather the Fed’s meddling is what some call Goldilocks, and sometimes worse. Not too hot and not too cold isn’t something sane minds aspire to, rather it’s the mediocrity we can expect so long as we presume that central bankers allocating the credit of others is the source of our prosperity.”

John is correct. An economy that is growing at 2%, inflation near zero, and Central banks globally required to continue dumping trillions of dollars into the financial system just to keep it afloat is not an economy we should be aspiring to.

The obvious question we should be asking is simply:

“If we are in a booming economy, as supposedly represented by surging asset prices, then why are Central Banks globally acting to increase financial stimulus for the market?”

The problem the Fed and other central banks confront is that, when market levels are predicated on ever-cheaper cash being freely available, even the faintest threat that the cash might become more expensive or less available causes shock waves.

This was clearly seen in late 2018, when the Fed signaled it might increase the pace of normalizing monetary policy, the markets imploded, and the Fed was forced to halt its planned continued shrinking of its balance sheet. Then, under intense pressure from the White House, and still choppy markets, they reduced interest rates to bolster asset markets and stave off a potential recessionary threat.

The reality is the Fed has left unconventional policies in place for so long after the “Financial Crisis,” the markets can no longer function without them. Risk-taking, and a build-up of financial leverage, has now removed their ability to “normalize” financial policy without triggering destructive convulsions.

Given there is simply too much debt, too much activity predicated on ultra-low interest rates, and confidence hinging on inflated asset values, the Fed has no choice but to keep pushing liquidity until something eventually “pops.”

Unfortunately, when trapped in a “Goldilocks” economy, realities tend to become blurred as inherent danger is quickly dismissed. A recent comment from another “Davos elite,” Bob Prince, who helps oversee the world’s biggest hedge fund at Bridgewater Associates, made this clear.

“The tightening of central banks all around the world wasn’t intended to cause the downturn, wasn’t intended to cause what it did. But I think lessons were learned from that and I think it was really a marker that we’ve probably seen the end of the boom-bust cycle.”

No more “booms” and “busts?”

Thomas Palley had an interesting take on this:

“The US is currently enjoying another stock market boom which, if history is any guide, also stands to end in a bust.

For four decades the US economy has been trapped in a ‘Groundhog Day’ cycle in which policy engineered new stock market booms to cover the tracks of previous busts. But as each new boom ameliorates, it does not recuperate the prior damage done to income distribution and shared prosperity.”

Well, except for those at the top, as Sven Henrick concluded last week:

“In a world of measured low inflation and weak wage growth easy central bank money creates vast price inflation in the assets owned by the few making the rich richer, but also enables the taking on ever higher debt burdens leaving everyone else to foot the ultimate bill.

There are two guarantees in life: The rich get obscenely rich, everybody else gets to carry ever more obscene public debt levels.”

“That is the measured outcome of the central bank easy money dynamic that has been with us now for decades, but has taken on new obscene forms in the past 10 years with absolutely no end in sight.”

While the elites are certainly taking in the “view through market colored” glasses, the reality is far different for most.

It is true the bears didn’t eat “Goldilocks” at the end of the story, but then again, there never was a sequel either.