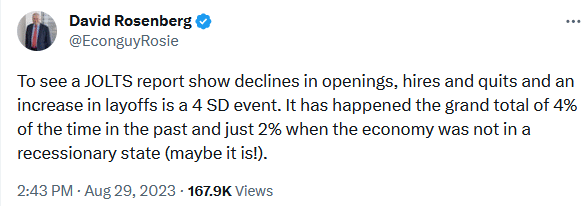

Tuesday’s JOLTS report and Wednesday’s ADP point to a sudden weakening of the labor markets. The JOLTS report (Job Openings and Labor Turnover Survey) produced by the BLS showed the number of job openings fell by 338k to 8.8 million. As shown below, job openings are falling almost as rapidly as they rose in 2020 and 2021. Per ZeroHedge: “The 3-month drop in job openings was 1.5 million, the 2nd highest on record surpassed only by the total economic shutdown during the covid crash.” Also, within the JOLTS report was another decline in the quit rate. This measures how many employees, as a percentage of the workforce, voluntarily quit jobs. The quit rate increases when employees are confident they can attain higher wages or a better job. Confidence appears to be waning as the quits rate, at 2.3%, is back to pre-pandemic levels.

ADP, like JOLTS, provided the markets with negative surprises. ADP reported the economy added 177k new private-sector jobs last month. While still a decent number, it is well off the prior two months, which averaged about 400k new jobs each month. Per ADP’s chief economist: “This month’s numbers are consistent with the pace of job creation before the pandemic. After two years of exceptional gains tied to the recovery, we’re moving toward more sustainable growth in pay and employment as the economic effects of the pandemic recede.” Both JOLTS and ADP show a sharp slowdown in the pace of hiring. While neither indicates declining job growth, the strong employment trend is finally normalizing. Jobless Claims this morning and the BLS report on Friday will provide more data on the labor market.

What To Watch Today

Economics

Earnings

Market Trading Update

More bad news was good news for the market yesterday, as investors hope the Fed will stop hiking rates. A weak ADP number suggests further weakness in Friday’s much-anticipated employment report, a down revision to Q2 GDP, and a trade deficit surge all contributed to the “bad news = buy stocks” meme.

Setting all of the media-driven narrative aside, after a 5% decline from the recent peak, the market was sufficiently oversold for a bounce. As noted yesterday, with the “buy signal” now registered, the market rallied yesterday, and investors put capital back to work. The market is starting to move back to more overbought short-term territory, so use pullbacks to the 50-DMA as an opportunity to add trading positions as needed. While we could see a rally that lasts for a few days, September is certainly a month that typically brings some volatility. So, if you are overweight equities and need to rebalance some risk, this rally is likely a good opportunity to do so. Once we get into October, we will have a better sense of what the end of the year will look like, and we can allocate accordingly.

More On The Quits Rate

As noted, the quits rate is a good measure of employee confidence. When confidence is high, employees feel more emboldened to ask for raises or quit and seek higher-paying jobs. The recently high quits rate concerned the Fed as they feared it could fuel a price wage spiral. Such occurs when higher wages drive prices higher, which drives wages higher, and so on. With the quits rate back to more normal levels, the Fed can breathe a sigh of relief that wage pressures are likely behind us. The graph below, from Liz Young at SOFI, shows the quits rate tends to lead the Atlanta Fed Wage Growth Tracker by about nine months.

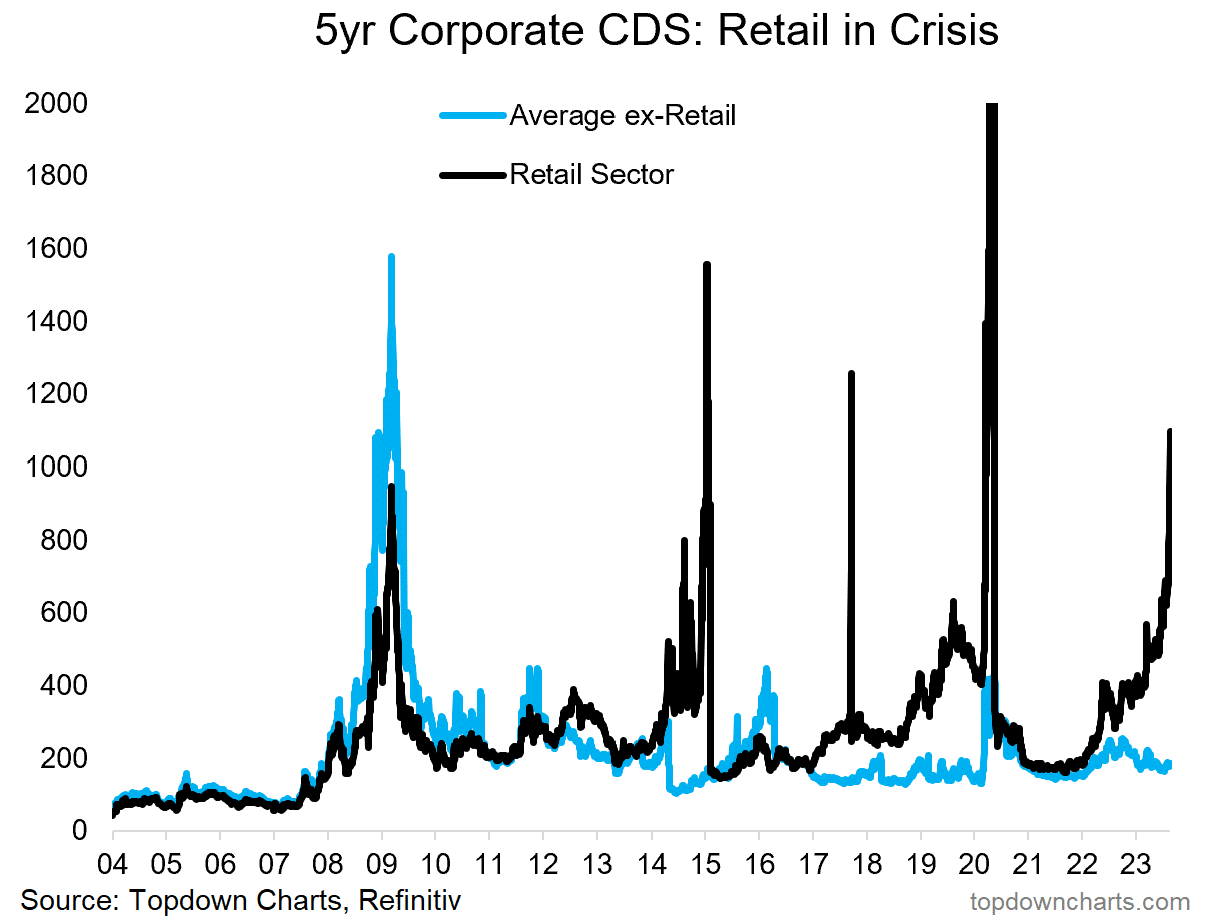

Retailers In Trouble Part 2

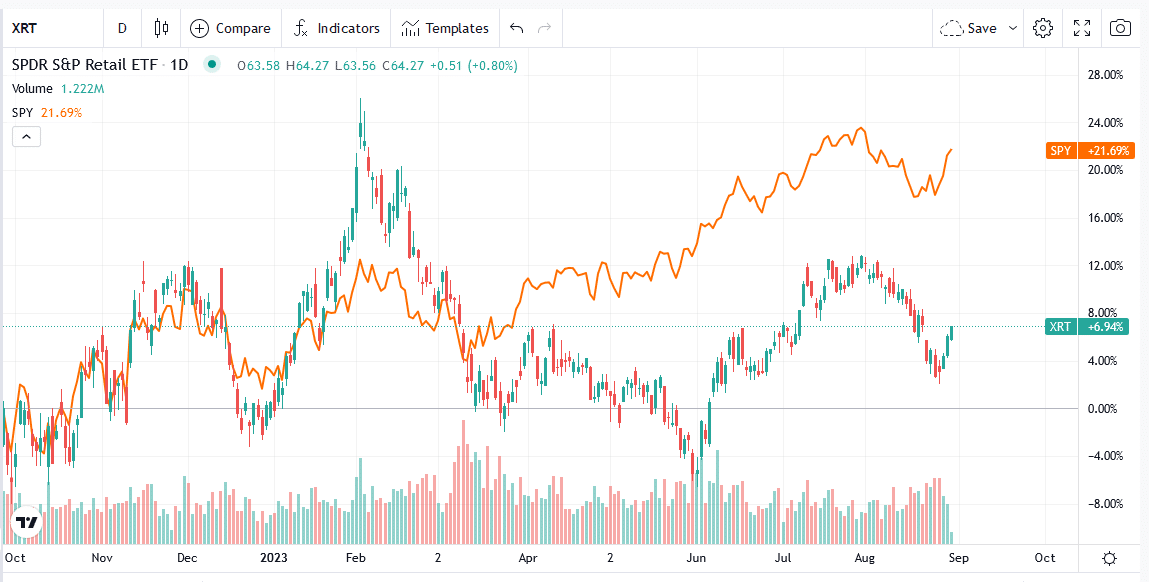

Yesterday’s Commentary led with a discussion on slowing personal consumption and its effect on retailers. The graph below shows the market is concerned for the retailers’ financial viability. CDS, or credit default swaps, are insurance contracts for bondholders. As shown, CDS on the retail sector has spiked, while non-retailers show no such change. Keep in mind CDS for retailers tend to be much more volatile than the broader market. The second graph further confirms investors are wary of the retail industry. It shows that since the lows last October, the retail ETF (XRT) has underperformed the S&P 500 by about 15%.

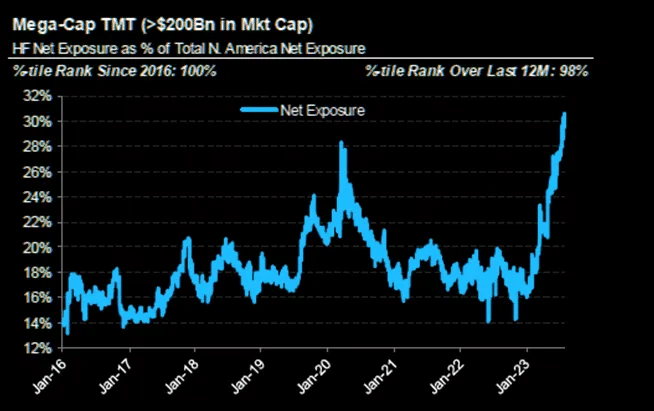

Hedge Funds Love MegaCap Stocks

Hedge funds now allocate about a third of their stock exposure to mega-cap stocks (>200 billion market cap). Such an increase in their exposure over the year helps explain the strong outperformance of the magnificent seven and a few other very large-cap stocks. With such a high allocation, the odds of hedge funds adding more exposure to mega-cap stocks are low. If those stocks falter, the hedge funds will likely trip over each other to sell. For now, mega caps are the right place to position. But, the imbalance raises concern that such positioning may not be a good long-term position.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.