The Fed raised rates by 25 basis points to 5.00-5.25%, hinting at a pause in future hikes. Weaker than expected Q1 GDP (+1.1%) and signs the labor market is finally cooling off argue the Fed may be done. However, higher inflation remains sticky, and the most recent ISM manufacturing survey shows the price paid component rose more than expected (from 49.2 to 53.2). Inflation and inflation surveys lead some economists to believe the Fed may not be done yet. However, as shown below, the Fed Funds market assigns low probabilities of another rate hike. Traders think the Fed is done and will be cutting rates aggressively starting in September.

If the Fed can look beyond inflation, they must consider the regional banking crisis, the lagged effect of previous hikes, and a barrage of coming Treasury issuance. In yesterday’s Commentary, we wrote: “Over the last 15 years, periods of excess Treasury supply were not problematic as the Fed helped the cause by keeping interest rates low and buying bonds via QE on multiple occasions. This time is different!” Is the Fed now done hiking rates, or does inflation trump the issues mentioned above? The answer to that question will be the predominant driver of markets in the coming months.

What To Watch Today

Economy

Earnings

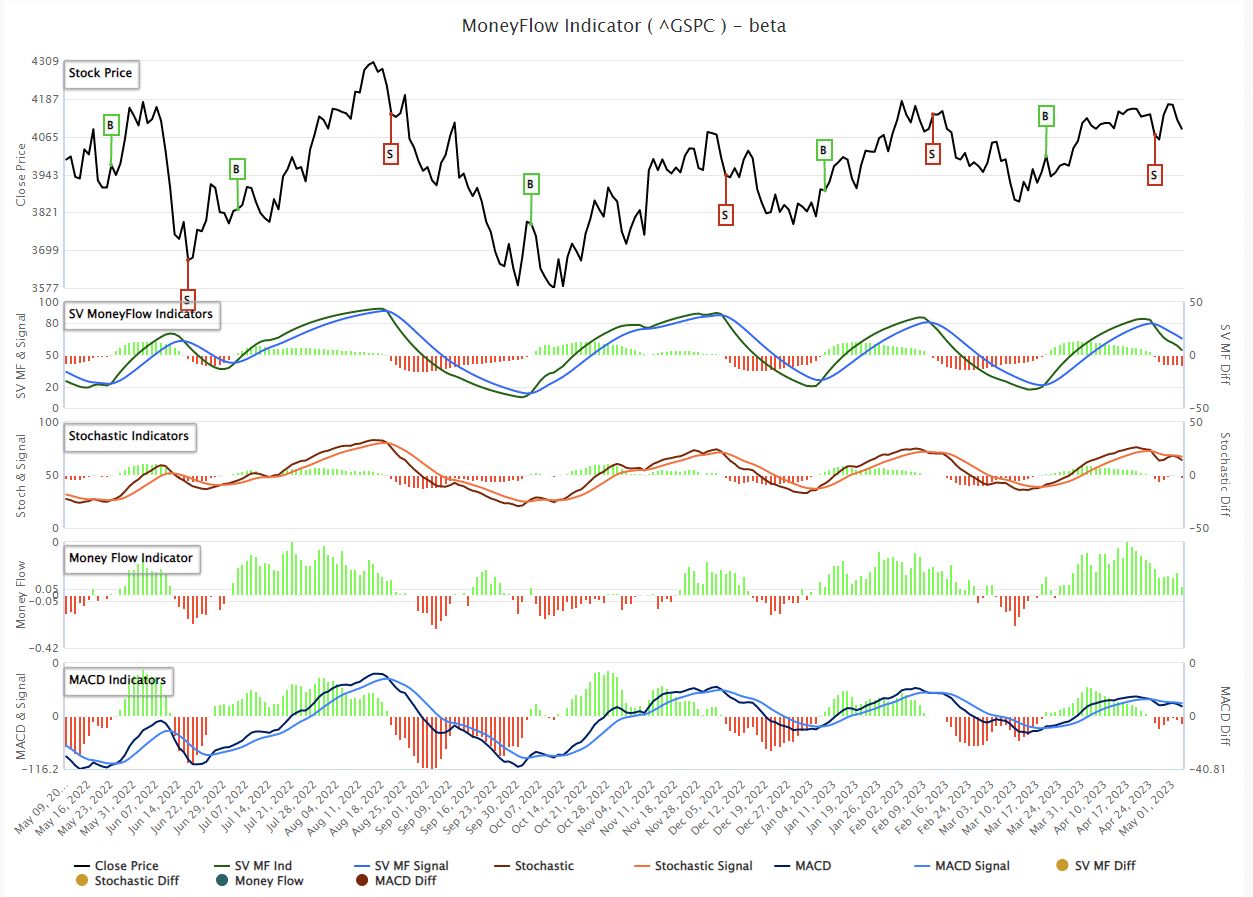

Market Trading Update

Yesterday, as noted above, the Fed made it fairly clear they are now done with hiking rates. As Sam Stovall noted:

“For me, the key was a change of a single word, saying that they believe that they will determine whether future raises are necessary, whereas last time, they said that they anticipate that further rate hikes will be necessary. With the word ‘determining’ in place of ‘anticipating,’ it is essentially telling the markets that the Fed is now on pause.”

While the market initially rallied on the news, stocks sold off into the close as the realization materialized that the Fed may indeed pause, but they are not “cutting” rates anytime soon. With bank lending standards tightening, that is also a defacto rate hike on the economy. As monetary conditions tighten, we will likely see more pressure on earnings and profits in the quarters ahead. Notability, we are already seeing oil pricing in an economic slowdown.

With the sell signal still intact, the market is holding up reasonably well as we work through the money-flow cycle. With that index about 1/3 of its way through its normal range, it suggests we could see additional downward pressure on stocks over the next few days and weeks. Of course, with Apple (AAPL) reporting earnings after the bell, it is hard to say what the market will do on Friday. Use rallies to reduce risk, raise cash levels, and rebalance portfolios.

Treasury Announces Buyback Program

Per the Wall Street Journal, the Treasury will embark on a bond buyback program in 2024. The last time the Treasury had such a program was in 2000. The details of the program are still in the making and, therefore, not specific. Such a program does not introduce liquidity as they must issue new bonds to buy back old bonds. However, it does allow the Treasury to influence yields. For instance, it could buy back longer-dated bonds to help minimize losses on bank balance sheets. At the same time, they might increase the issuance of short-term bills, which are in heavy demand.

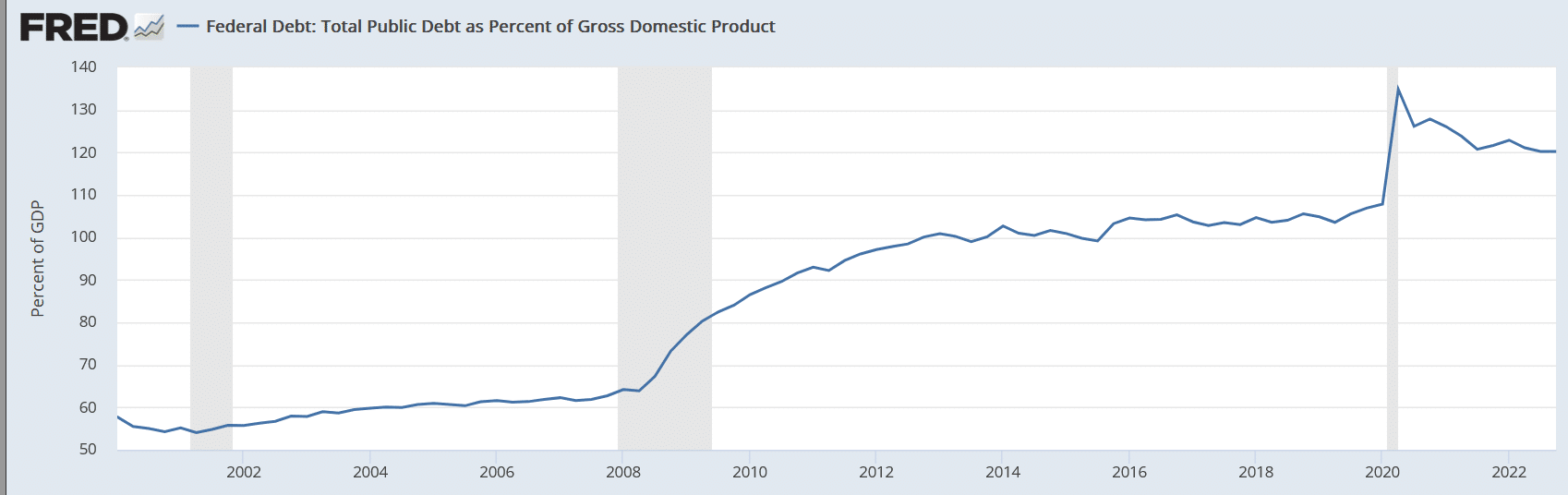

The program in 2000 was quite different than what the Treasury is considering. At the time, the government was running a surplus. Believe it or not, the Treasury’s concern was bond market illiquidity, as there would not be enough bonds outstanding. Today the problem is too many bonds, as the country has presided over 20 years of runaway deficits. The graph shows that Federal debt to GDP was only 60% in 2000.

Which Regional Bank is Next in the Bankruptcy Line?

To help consider which banks may follow First Republic Bank into bankruptcy, assess the year-to-date performance of some large regional banks, courtesy of the Kobeissi Letter:

US Regional Bank Stock Performance This Year:

- HomeStreet, $HMST: -75%

- PacWest, $PACW: -71%

- Metropolitan Bank, $MCB: -64%

- Zions Bank, $ZION: -51%

- Western Alliance, $WAL: -47%

- KeyCorp, $KEY: -45%

- HarborOne, $HONE: -39%

- Valley National, $VLY: -35%

- Truist, $TFC: -33%

- Citizens Financial, $CFG: -32%

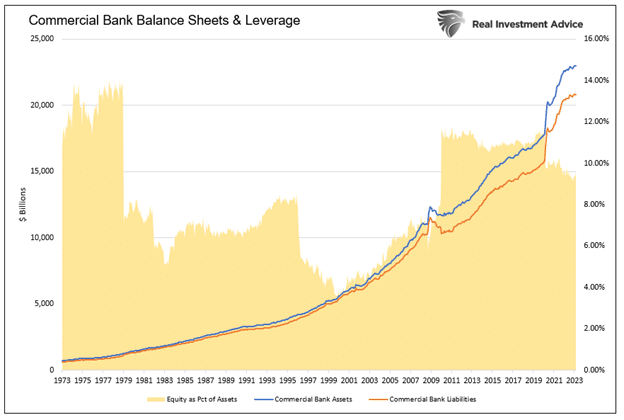

To better appreciate banking and why some regional banks are at risk, we just published Bank Stocks: Do the Rewards Warrant the Risks?

The article’s graph below shows that bank assets have less than 10% of an equity cushion in the aggregate. This means that if a bank’s assets lose more than 10% of their value, it is effectively bankrupt. Fortunately, banks do not recognize losses on most assets unless they sell them. This is where the rubber is currently hitting the road. As deposits shift from regional banks to larger banks or money market funds, banks must sell assets. In doing so, they must recognize crippling losses which can completely erase the equity cushion and force an FDIC takeover.

As we share in the article:

Many banks require cash to replace deposits. As such, they have options. They can raise new deposits, which entails paying customers over 4% versus the paltry near 0% they currently pay depositors. Or they can sell assets. A collective leverage ratio of 10 to 1 means it only takes a 10% loss on a bank’s assets to wipe out its equity cushion. Risk-free U.S. Treasury notes and mortgages lost about 20% of their value in 2022. Since getting new deposits was not feasible for Silicon Valley Bank, it had to sell assets and recognize losses more significant than its equity cushion.

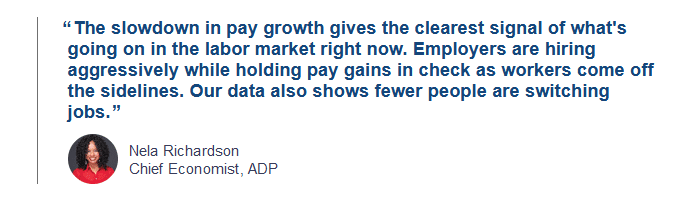

ADP Highlights Strong Jobs Market

Wednesday’s strong ADP report was at odds with Tuesday’s weaker JOLTs report. ADP shows the economy added 296k jobs in April, more than two times March’s figure and expectations. Further, it was the largest gain since July. Once again, leisure and hospitality jobs are the fastest growing sector, accounting for half of the job growth.

While job growth continues, wage growth normalizes. Per the quote from the report and commentary from ADP’s Chief Economist:

Pay growth continued its nearly year-long slowdown. Job changers in particular saw a dramatic decline, with pay slowing from 14.2 percent growth to 13.2 percent, the slowest pace of growth since November 2021.

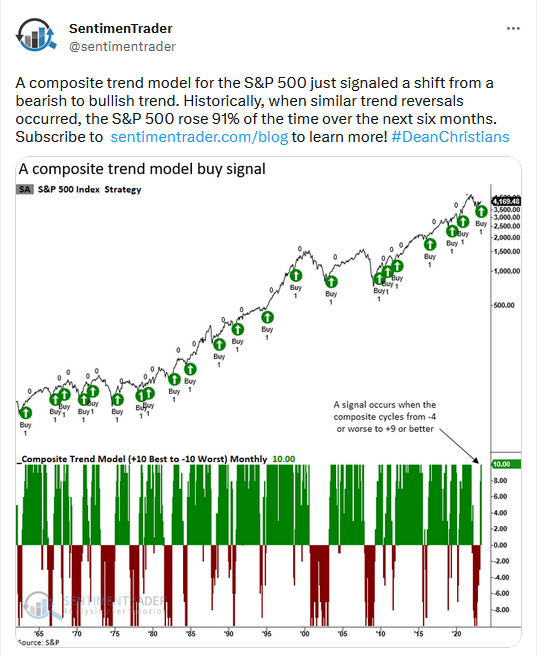

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.