“Fed Tiptoes Toward Dialing Back Key Channel of Monetary Tightening,” by Nick Timiraos, appeared in Tuesday’s Wall Street Journal. Author Nick Timiraos, a.k .a. the Fed Whisperer, is often the recipient of Fed leaks. Tuesday’s article alludes that the Fed may soon slow down the pace of QT. As we have written, the Fed’s overnight repo program, designed to absorb excess liquidity, is drying up rapidly, as shown below. Pandemic-related liquidity is exiting the financial system, and risks are increasing. Consequently, as we wrote a few days ago, the combination of QT and declining repo balances is forcing repo rates higher and, with it, liquidity warnings.

The quote below from the article best articulates how dislocations in the repo markets are market signals the Fed is keying on. Given recent pricing issues in the repo market, QT is likely to be tapered well before the Fed reaches its inflation target. The Fed doesn’t want liquidity problems to force them to lower rates prematurely or flip QT to QE. They also recognize they are not good at predicting when liquidity will dry up. Accordingly, they appear willing to taper QT and possibly cut rates earlier than initially thought to ensure the financial markets remain liquid.

Officials say they are going to rely more on market signals in identifying the right level of reserves. “Last time, we had lots of estimates of where we thought that terminal level of reserves was, and our estimates were too low,” Philadelphia Fed President Patrick Harker said in an October interview. “At the end of the day, the market will dictate where we are.”

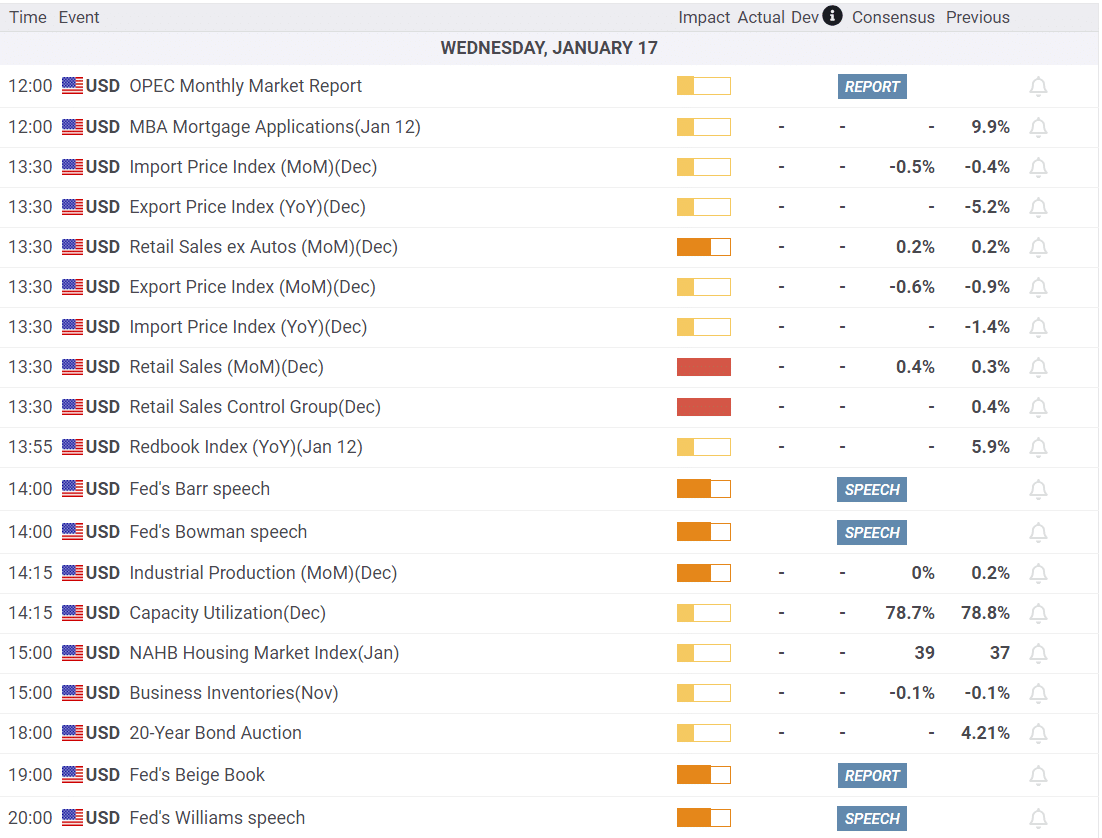

What To Watch Today

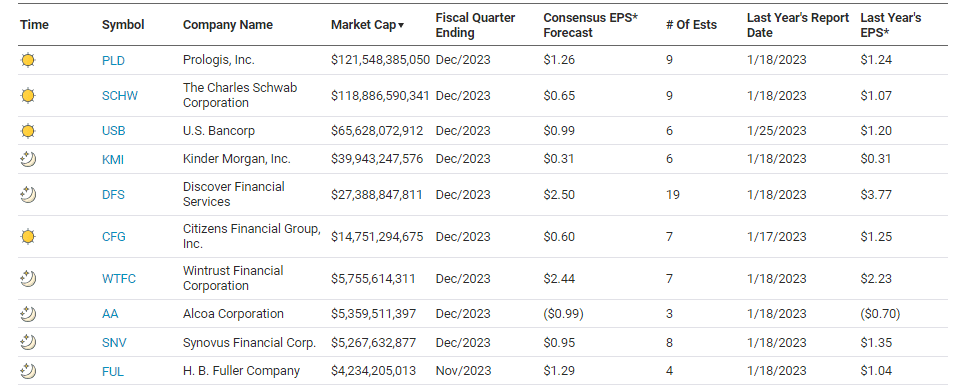

Earnings

Economy

Investing Summit: Early Bird Registration Available Now

January 27th, we are hosting a live event featuring Greg Valliere to discuss investing in the 2024 presidential election. What will a new president mean for the markets, the risks, and where to invest through it all? Greg will be joined by Lance Roberts, Michael Lebowitz, and Adam Taggart for morning presentations covering everything you need to know for the New Year.

Register now, as there are only 150 seats. The session is a LIVE EVENT, and no recordings will be provided.

Market Trading Update

With the market closed on Monday in observance of Martin Luther King, trading resumed on Tuesday, with stocks selling off following a disappointing read from the New York Fed District Manufacturing Index and more hawkish tones from Federal Reserve speakers. Today, as noted in the calendar above, we have several Fed speeches that will likely lean more hawkish in terms of pushing out expectations for rate cuts.

Technically, not much has changed from last week. The market remains on a broader MACD “sell signal,” and the Relative Strength Index (RSI) continues to decline from overbought levels. The market has remained in a fairly tight consolidation since late December and has recently started establishing a double top. A failure of the early January low will market the top for the current rally, and the 50-DMA will become primary support. However, if the market can break to the upside, all-time highs will quickly be challenged.

For now, remain allocated toward equity risk. Bonds are starting to look more attractive but, like the stock market, have more work to do to confirm the bottom is in. Patience remains key.

Europe At Economic Risk From Red Sea Attacks

PiQSuite.Com quantified the sector/industries most exposed to disruption from Red Sea attacks. They lead by noting the following:

“Automakers Tesla, Geely-owned Volvo Car, and Suzuki Motor said they were suspending some production in Europe due to a shortage of components in the first clear sign that the attacks are hitting manufacturers.”

Europe appears most at risk for shortages of certain goods. S&P Global quantifies that approximately 15% of Europe’s imports come through the Suez Canal. For example, 47% of toy imports to Europe, 39.5% of household appliances, and 58.2% of palm oil go through the canal. Exports from Europe to Asia or Gulf destinations are also affected, but to a lesser degree (8.6%). The most affected include spirits (49.1%), passenger vehicles (41.3%), and milk products (40.4%).

If the disruptions continue, Europe may witness higher inflation and slower growth. Thus far, the effect on the United States is minimal. The graphic below is courtesy of Reuters.

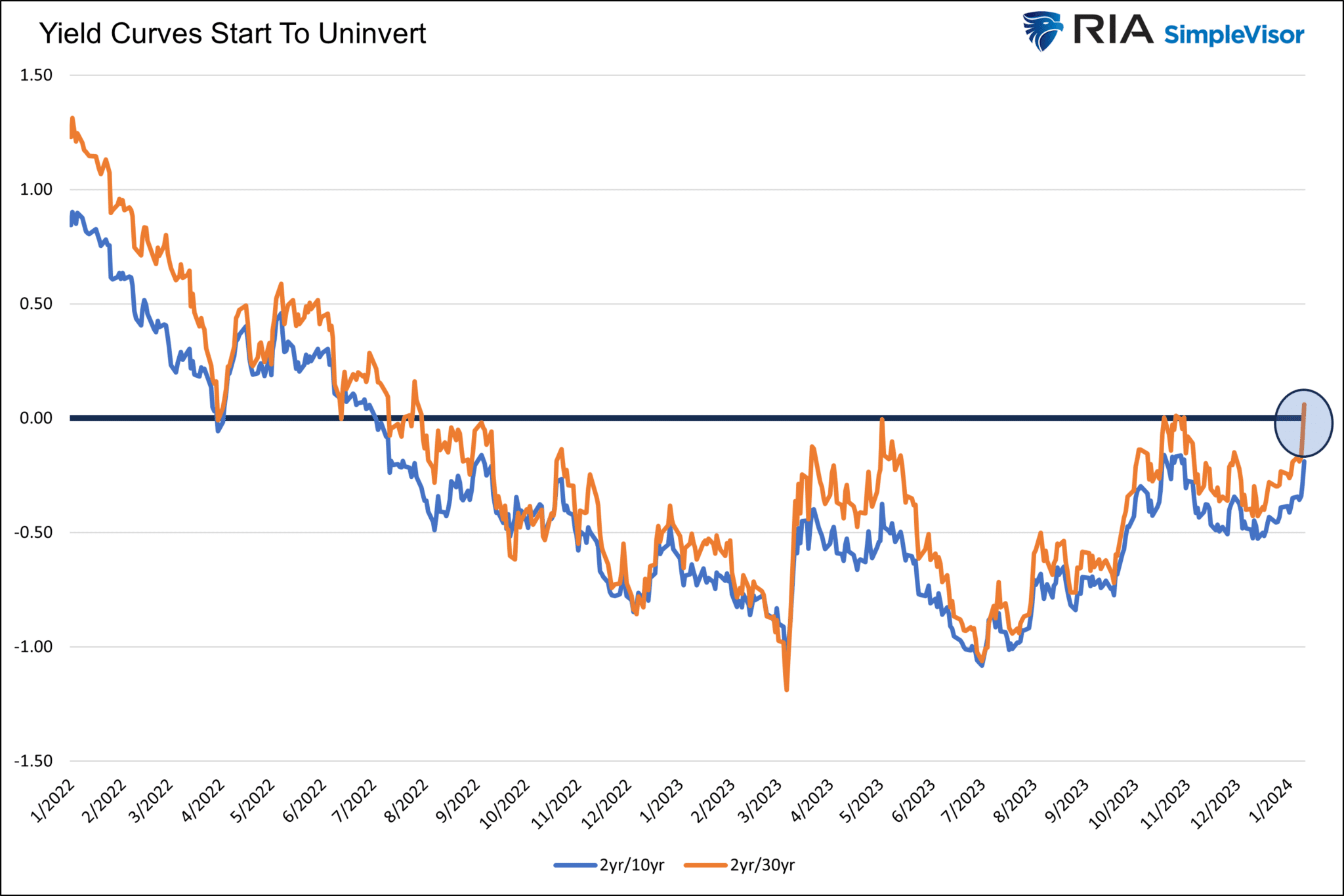

Treasury Curves Starting To Uninvert

The graph below shows that the 2-year Treasury note yield is now lower than the 30-year Treasury bond yield. After being inverted since mid-2022, the 2/30yr yield curve has resumed its standard shape. Driving the rapid uninversion is growing market anticipation that the Fed will cut rates aggressively. The more widely followed 2yr/10yr yield curve (blue) is still inverted but only 19bps from uninverting.

While a normal-shaped curve supports more bank lending, which is positive for the economy, uninversions have a robust history of signaling imminent recessions.

New York Fed Manufacturing Sinks

The January New York Fed Manufacturing Index was shockingly lower at -43.7 versus a -5 consensus. The index is at its lowest level since May 2020! New Orders, a great leading economic indicator, led to the decline. 12.2% of those surveyed are seeing a pick up in orders, while 61.5% are experiencing a decline in orders. Importantly, the index is volatile, and the post-Christmas consumption hangover may be largely behind the sharp decline. If other regional indexes show similar declines, then more concern is warranted.

Interestingly, despite the sharply lower index, expectations of those surveyed are not nearly as dour, as shown with the red line below. Per the report:

While firms expect some pickup in activity in the months ahead, optimism remained subdued, with the index for future business conditions climbing seven points to 18.8. The capital spending index increased ten points to 13.7, pointing to some improvement in investment plans.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.