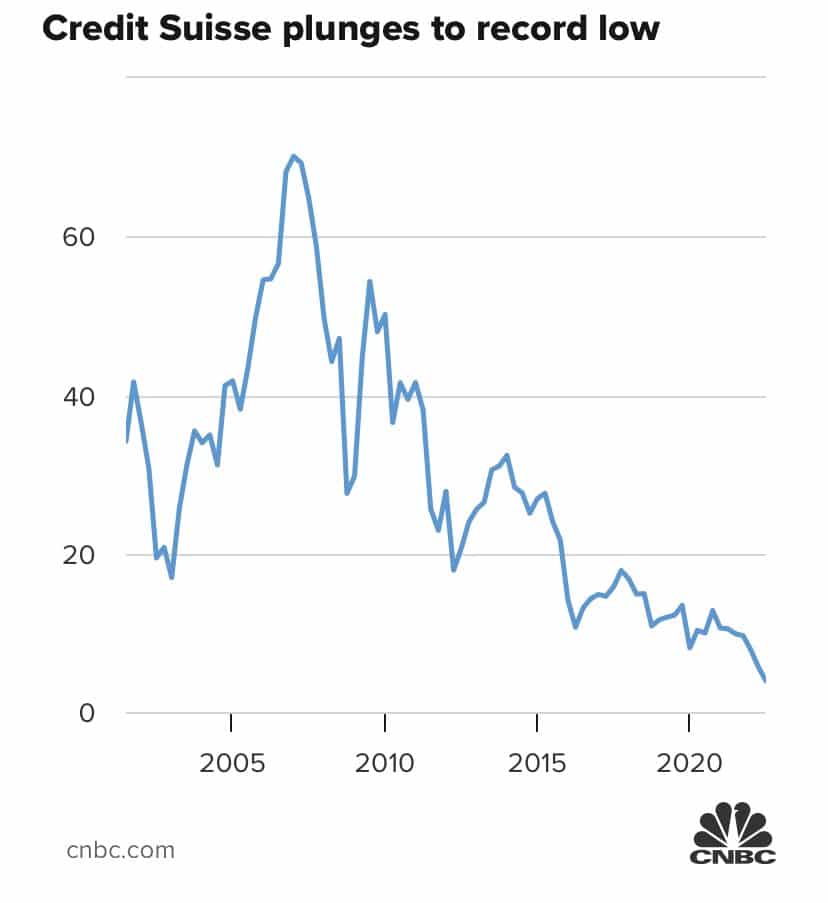

Rumors are floating around that Credit Suisse, Switzerland’s second-largest bank, is having financial difficulties. Accordingly, many investors are starting to look to the Swiss National Bank (SNB) and ECB to bail them out. The credit default swap markets can quantify how serious the market thinks the situation is. Currently, a five-year CDS contract on Credit Suisse costs 2.5% per year. Therefore, a bondholder can pay 2.5% yearly to hedge against default. At that level, CDS is pricing in approximately a 17% chance the bank defaults, assuming bondholders recover 25 cents on the dollar. As a point of reference, Citi and Goldman Sachs trade around 135bps, or about half of Credit Suisse’s level.

The more significant issue here is not Credit Suisse but increasing signs of broader financial instability rising throughout the European banking sector. Therefore, keep a close eye on central banks and treasury departments for signs of willingness to step in and arrest the growing problems.

What To Watch Today

Economy

- 10:00 a.m. ET: Factory Orders, August (0.0 expected, -1.1% prior)

- 10:00 a.m. ET: Factory Orders Excluding Transportation, August (0.2% expected, -1.0% prior)

- 10:00 a.m. ET: Durable Goods Orders, August final (-0.2% prior)

- 10:00 a.m. ET: Durables Excluding Transportation, August final (0.2% prior)

- 10:00 a.m. ET: Non-defense Capital Goods Orders Excluding aircraft, August final (1.3% prior)

- 10:00 a.m. ET: Non-defense Capital Goods Shipments Excluding Aircraft, August final (0.3% prior)

- 10:00 a.m. ET: JOLTS Job Openings, August (11.088 million expected, 11.239 million prior)

Earnings

Market Trading Update

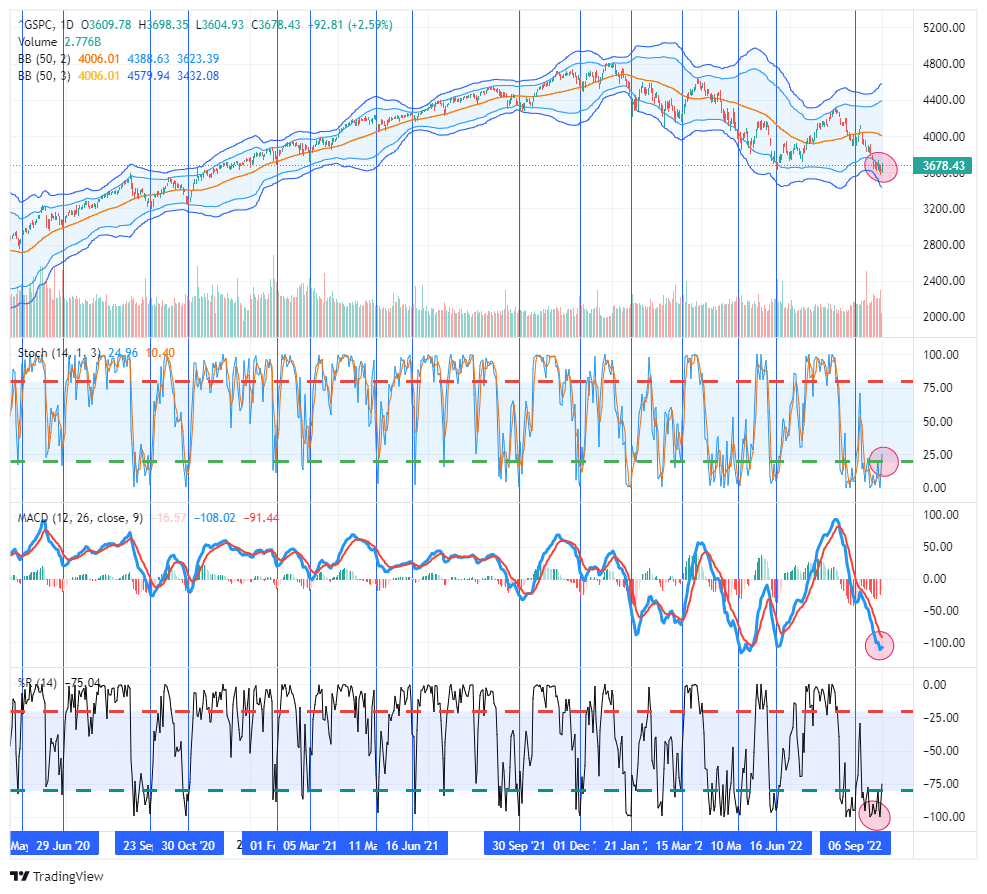

“Stocks and bonds were bid on Monday after the September decimation for both assets, perhaps on oversold conditions but there are also murmurings of investors bracing for a Fed pivot – although this is very speculative, but the US data on Monday was also weaker than expected. Fed speakers have noted they are keeping an eye on events abroad and the potential impact it has on the US, although Fed Vice Chair Brainard on Friday did stress she is committed to avoiding pulling back prematurely while Williams noted inflation is far too high and the Fed’s job is not done. The talk of a Credit Suisse collapse has led to a jump in the Credit Suisse CDS and a tumbling share price, exacerbating these concerns despite pushback from management but nonetheless adding to woes about financial stability.” – Newsquawk

While there were a lot of reasons presented by the media for the rally on Monday, the truth was simple. Last Tuesday’s blog post, “The Big Short Squeeze,” and this past weekend’s Newsletter laid out the case for a reflexive rally given the extreme oversold conditions. To wit:

As noted, every technical indicator is now screaming oversold. As shown by the vertical lines, when the market had previously hit such lows across indicators, such was typically near a short-term bottom. We suspect that as we enter into October, we could see a more sustainable reflexive rally to roughly 3850 on the S&P 500. Investors should continue to use such rallies to raise cash and rebalance risk accordingly.

Such is likely a tradeable rally so that short-term traders can add exposure. For longer-term investors, until proven otherwise, treat this rally as a “bear market rally” and rebalance risk accordingly.

OPEC Leads Oil Prices Higher

Crude oil was over 5% higher on Monday as OPEC mulls production cuts of around 1 million barrels daily. One million barrels is equivalent to approximately 1-2% of the global supply. OPEC’s decision could come on Wednesday after it meets. The New York Times reports that Saudi Arabia wants to bring oil prices back up to $90 a barrel.

ISM Sparks Rally

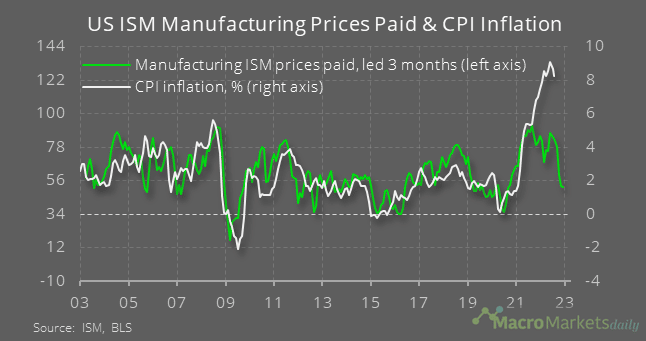

The ISM manufacturing survey came in weaker than expected at 50.9. A reading below 50 signals economic contraction. Within the index, the employment sub-component was 48.7, weaker than expectations of 53.0. Prices paid were slightly more fragile than expectations at 51.7. New orders, a forward-looking sub-component, suggest an economic contraction is underway at 47.1. The graph below shows the strong correlation between ISM prices paid and CPI. The current divergence is massive, but if the correlation holds, we should expect a sharp drop in inflation.

The Fed purposely tries to slow economic activity and increase the unemployment rate to bring inflation down. While the ISM data is not good from an economic or corporate earnings perspective, the market is rejoicing as it is a sign the Fed may be getting what they want. That means the most hawkish Fed era in over 40 years might be in its latter innings. The Fed will need a few months of similarly weak data before it considers changing its tone. However, as we note in the opening, financial instability, not the economy or inflation, might be what gets the Fed to take its foot off the brakes.

Sectors- Bearish Deviations

The graph below shows how far each sector trades below its 20, 50, and 200-day moving averages. The distance is measured in standard deviations. Often, trading two or more standard deviations (sigmas) below a moving average denotes an oversold situation. Three or more is uncommon and often results in a decent counter-trend move. Staples, one of the better-performing sectors this year, is the only sector with all three moving averages below negative two standard deviations. Utilities, which has also outperformed the market this year, is trading over three standard deviations below its 200 dma.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.