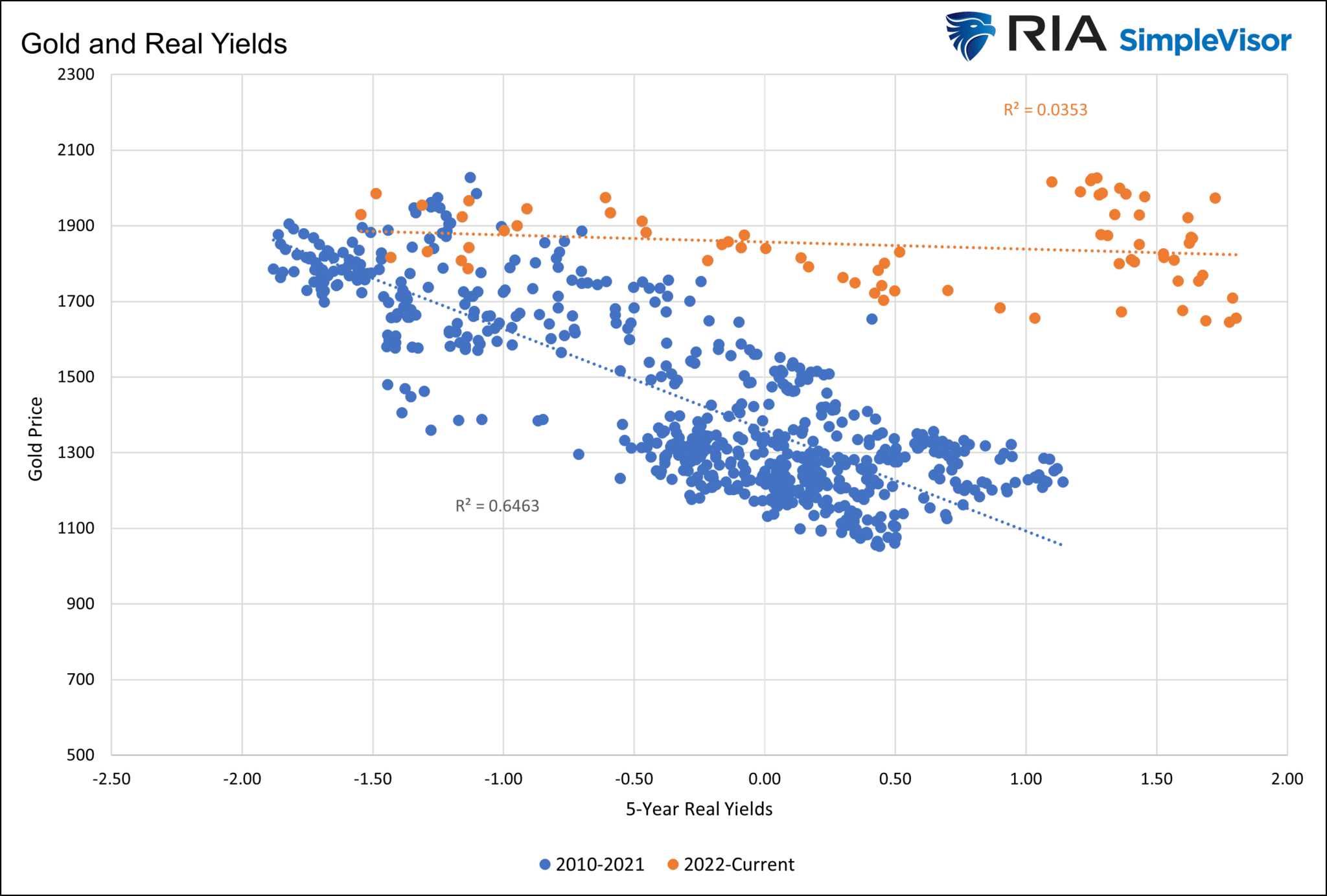

In March and April, the price of gold rose by 15% as the debt cap was hit, and the banking crisis accelerated. Since early May, gold has given up a third of those gains. Recent volatility in gold prices corresponds inversely with the dollar and with the news surrounding debt cap negotiations. At first glance, such price behavior sounds perfectly normal. However, looking back over time, the price of gold is highly correlated to the level of real yields, and at other times, like today, it gyrates with markets, economic data, and political events. Understanding what is and isn’t driving gold prices is crucial for those trading or investing in gold. In Gold Investors are Betting on the Fed, we quantify how monetary policy greatly affects gold prices.

“gold prices are highly correlated with real yields when real yields are near or below zero. The correlation is negative, meaning that as real yields fall, gold prices rise.”

The correlation between gold and real yields is robust when the Fed pushes interest rates below their natural rate (below expected inflation), as they did through much of the post-Financial Crisis era. In such an environment, gold traders and investors can predominately take their cue from the Fed and inflation expectations. However, when the Fed is hawkish, gold prices are much more unpredictable. The graph below shows the strong correlation (r2 =.64) between gold prices and real yields when Fed administered an easy policy. Conversely, there is no relationship between prices and real yields when their policy is hawkish. Gold is currently untethered and may continue to be volatile as debt cap negotiations and fear-mongering continue.

What To Watch Today

Earnings

Economy

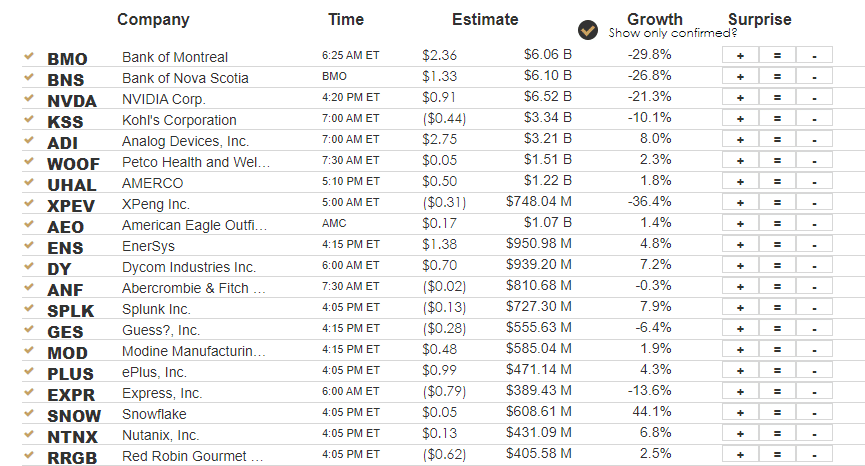

It’s Nvidia Earnings Day

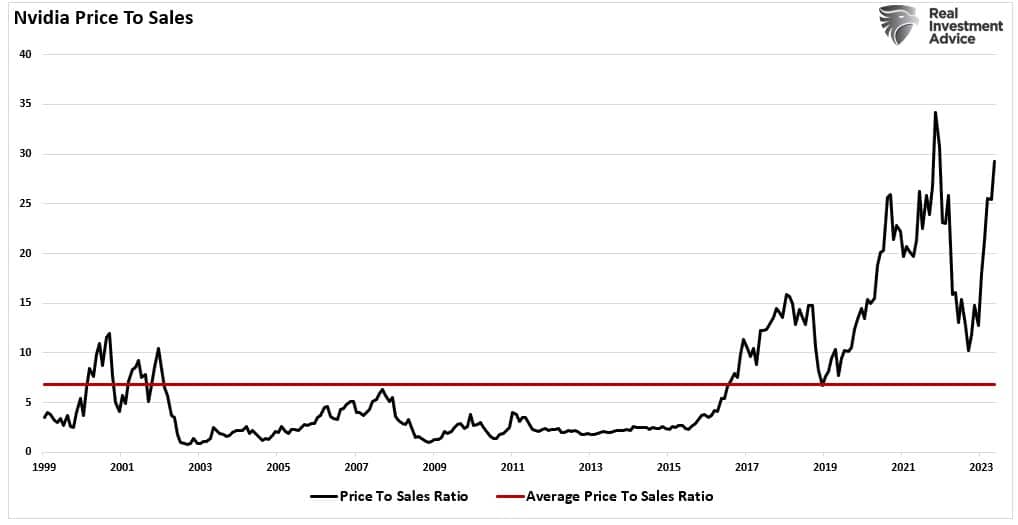

As I discussed in Tuesday’s blog, “A.I., Narrow Markets, And The New TINA,” the darling stock of the A.I. movement is Nvidia (NVDA) which has been on a stellar run this year. The question is whether or not their earnings report today will be enough to justify a 29x price-to-sales ratio.

Nvidia has a long history of trading above and below high valuations, with its long-term average running at roughly 9x sales.

As I noted in that article:

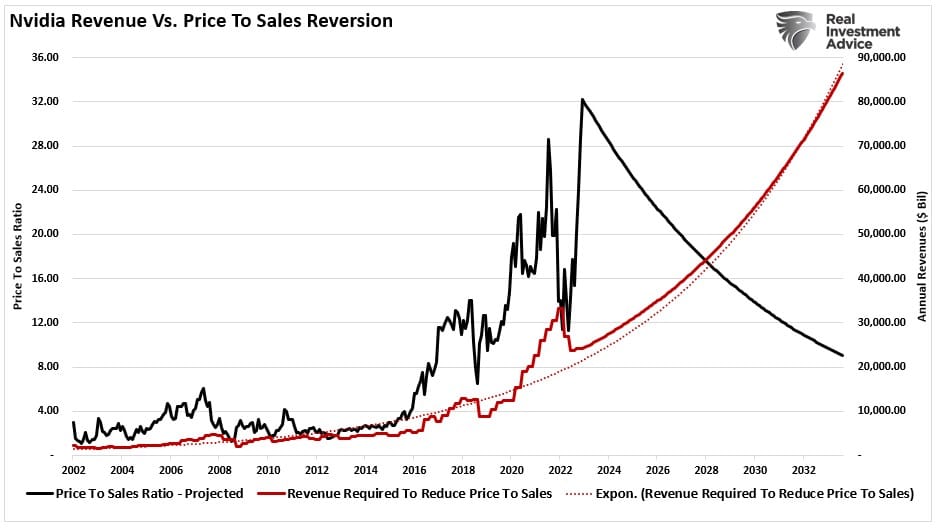

“The problem with 29x price to sales is that between now and the end of 2033, Nvidia will need to grow sales by 1% every month for the next ten years, and the stock price can not change during that period. There are two problems with this. First, since 2002, Nivida has had a monthly sales growth of just 1.26%. It is far different to grow sales at that pace when sales are $2 billion versus $33 billion today. Secondly, even if Nvidia can maintain that pace of uninterrupted growth, which means Nvidia will own 100% of the GPU market, it would only reduce its valuation to a still expensive 9x sales.”

All eyes will be focused on today’s earnings report and, most importantly, the guidance they provide about the recovery of the semiconductor space and its footprint in the “Generative A.I.” space. We will likely see a sharp price movement in NVDA in one direction or the other. If it is higher, I would take profits as the good news is mostly priced in. However, a downside break will be an opportunity to pick up shares of a “momentum trade” at a better entry point.

Whatever the outcome, it will be interesting to watch.

PMI Surveys Argue Higher for Longer

The Fed got unwelcome news from the latest round of PMI surveys. The PMI manufacturing survey fell to 48.5, putting it in economic contractionary territory. At the same time, the services survey rose to 55.1, pointing to robust growth in the services industries. Manufacturers are retrenching, which will result in less production and layoffs. Less production will limit supply which can be inflationary. Manufacturing accounts for less than 10% of the workforce. Therefore, any layoffs in the sector will not be significant. The services sector, which appears to be doing well, will likely continue hiring people, adding to inflationary pressures. The sector should easily offset manufacturing job losses.

While only one survey and for one month, the data argue the Fed is now more likely to keep interest rates higher for longer.

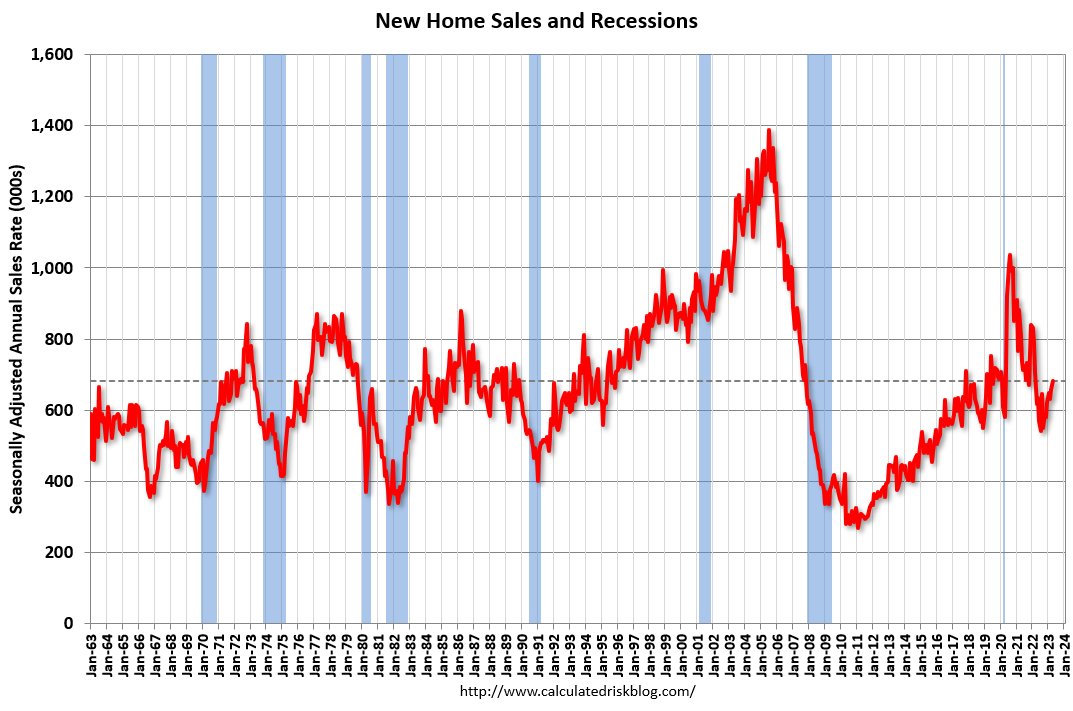

Home Sales Beat Expectations, But Revisions Matter

The latest home sales data show why we must be skeptical of initial economic data. Most economic reports, which make the headlines and steer markets, can be faulty. For this reason, the NBER relies on revised economic data before making judgments about recessions.

The latest example is new home sales. New home sales grew 4.1% in April, well above the expected -2% decline and in line with last month’s 4% reading. At first blush, that sounds good. What most media outlets fail to tell you is the prior reading of 4% was reported as 9.6% last month.

The graph below from calculated risk shows that new home sales have ticked up over the last few months, likely due to lower mortgage rates. The Freddie Mac 30-year mortgage rate is still high at 6.39% but well off its 7.08% peak. While U.S. Treasury yields have ticked higher due to debt cap concerns, mortgage rates remain steady.

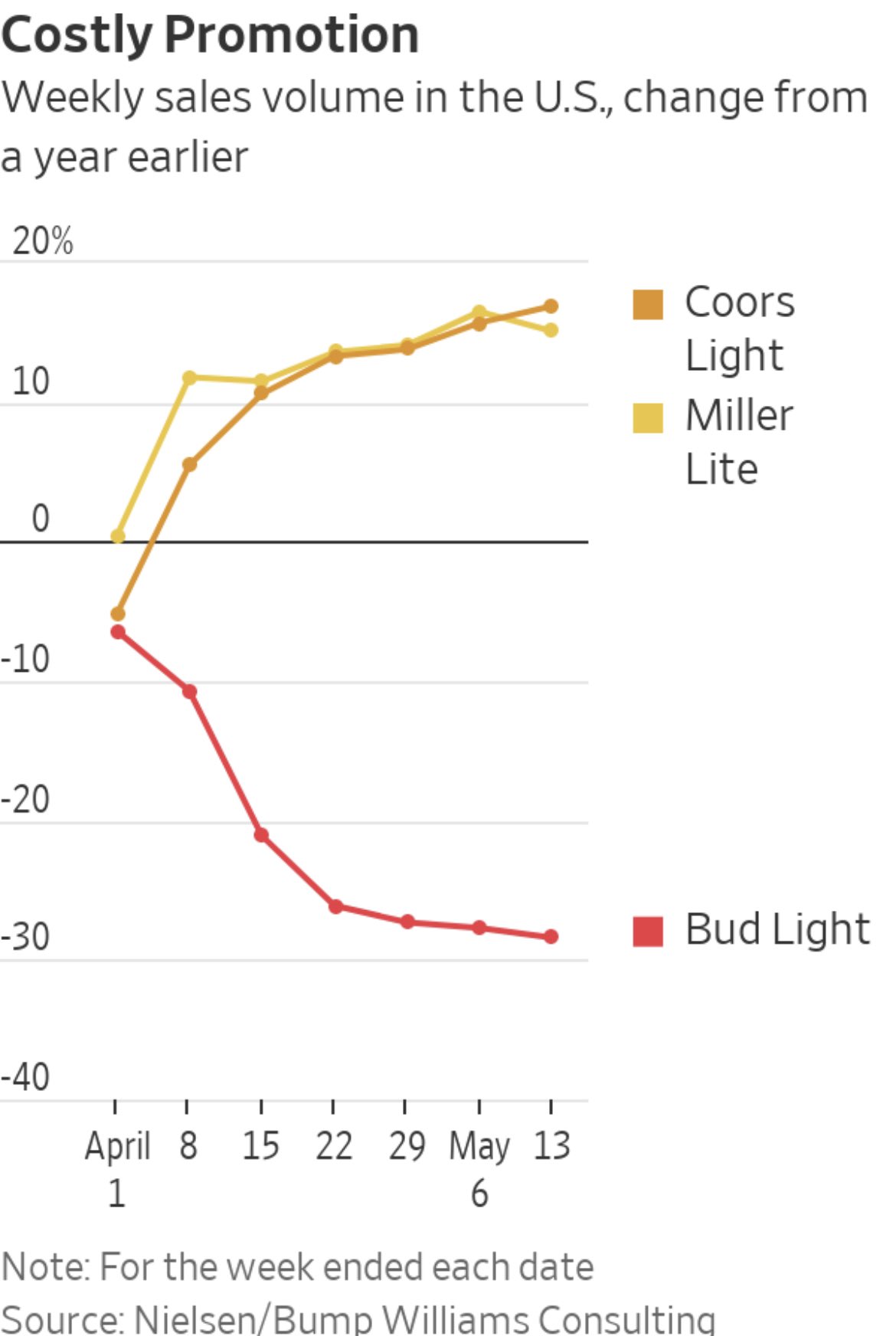

Bud Light Makes a Costly Marketing Decision

Two months ago, Bud Light placed a picture of Dylan Mulvaney, a transgender influencer, on its beer cans. Per the Wall Street Journal, the purpose was as follows:

Alissa Heinerscheid, the first woman in Bud Light’s four-decade history to run its marketing, had devised a strategy to combat the beer’s long-declining sales by appealing to a wider swath of customers, including more women and younger adults.

The graph below from the article shows some drinkers of Bud Light were not happy with the marketing campaign and, in many instances, have chosen to boycott Bud Light and instead buy Coors Light and Miller Lite. Per the Journal, InBev, the parent company of Bud Light, is returning to its more traditional marketing targets.

The company now plans for the first time to include Bud Light in the brewer’s long-running sponsorship of a veterans organization, wholesalers said. Bud Light is also leaning back into television commercials on themes like football and country music.

The second graph below shows that since Bud Light’s marketing campaign, InBev stock is down about 15%, while Molson Golden (TAP), which owns Coors and Miller, is up about 22%.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.