President Biden and Republicans have agreed in principle to a debt ceiling deal. While news of a deal to increase the debt ceiling is positive, it must still pass both houses of Congress. Further complicating matters, the Treasury warned over the weekend that without a deal in hand by June 5th, the government would have to stop making payments. Most pundits think the President will sign the debt cap deal as the agreement stands. However, the markets may stay on edge until Biden signs it.

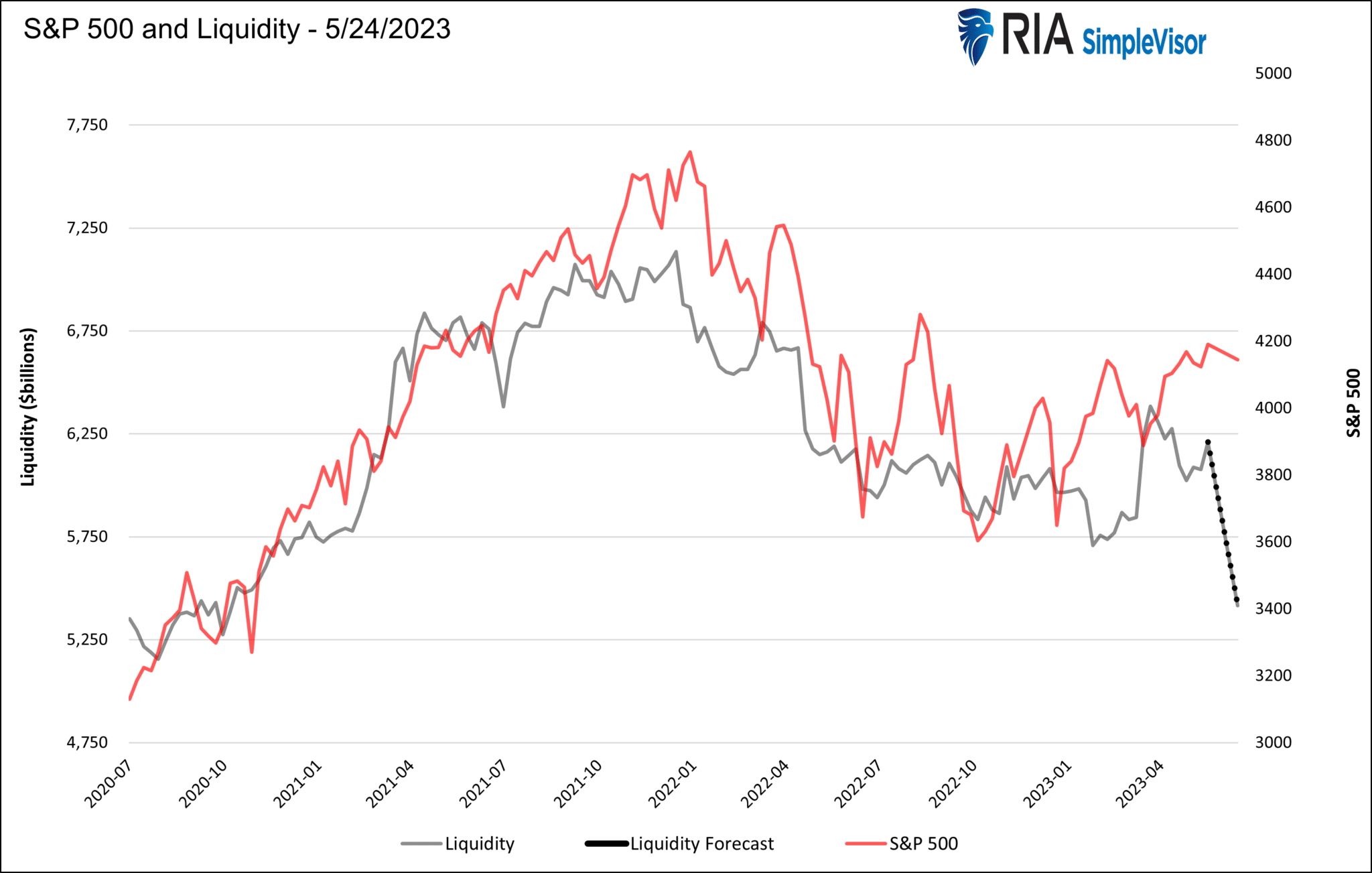

There are a few key takeaways from the proposal. The debt ceiling will be raised for two years, putting the next round of negotiations past the presidential election. Unlike prior increases, the current deal expires in two years and doesn’t put a specific ceiling on the amount of outstanding debt. This means that the amount of debt issuance is unlimited for the next year and a half. In the current environment, that likely means spending will be constrained. However, in the event of a recession, we could see another fiscal stimulus bonanza, as we witnessed during the pandemic. The other important thing to note is that once the President signs the bill, the Treasury will remove liquidity from the markets as it must issue significant amounts of short-term debt. Our Commentary from last Thursday provides more details on what this might mean for the well-followed Fed liquidity gauge.

What To Watch Today

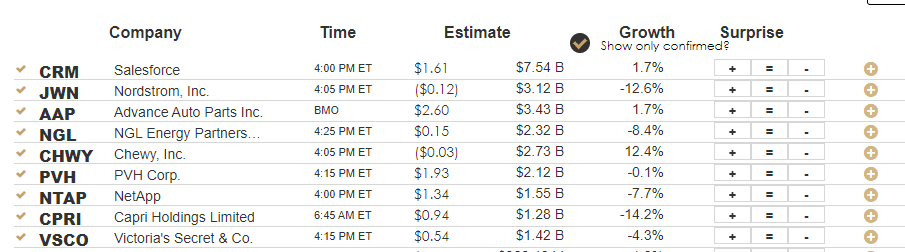

Earnings

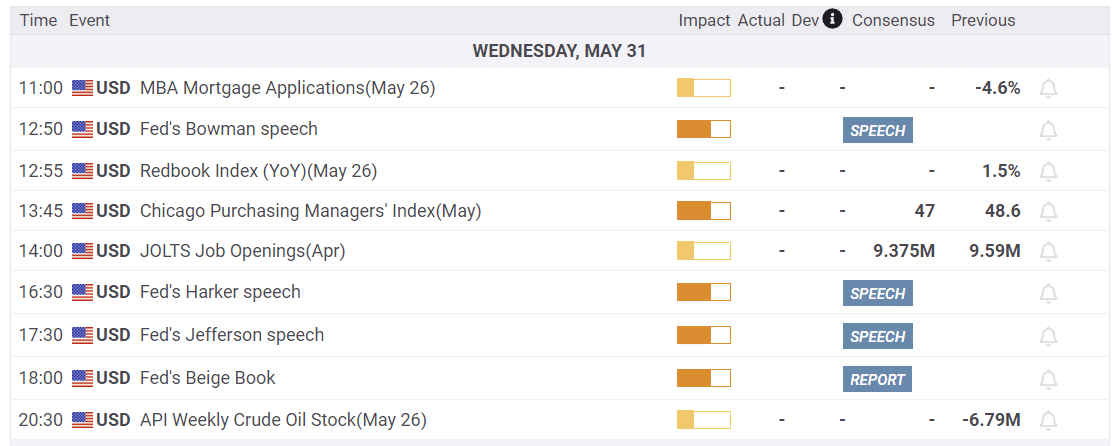

Economy

Market Trading Update

The market continues to trade bullishly for the moment, but as we have discussed previously, that performance remains substantially narrow. As discussed in an upcoming post, breadth remains the most troubling currently.

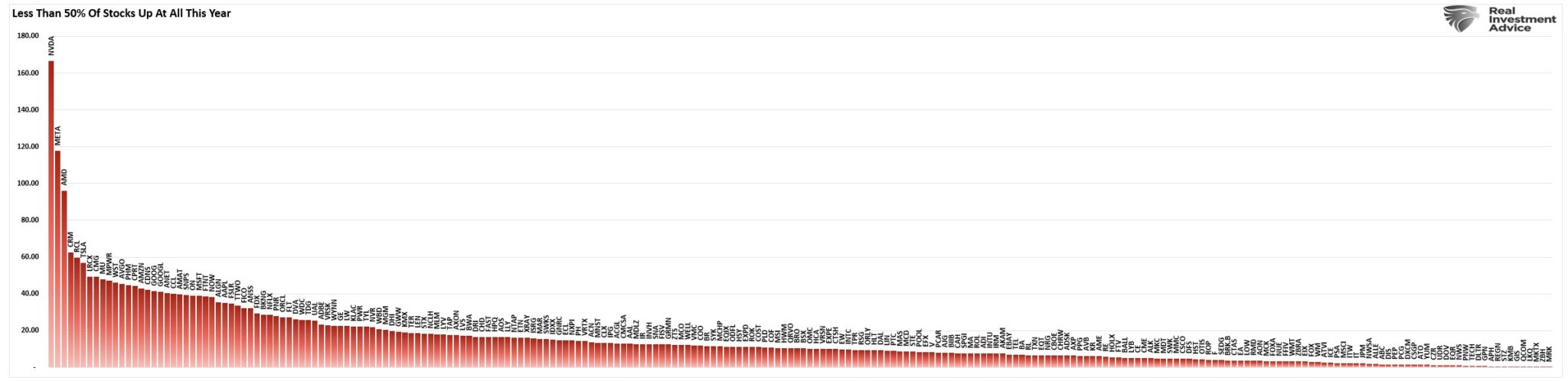

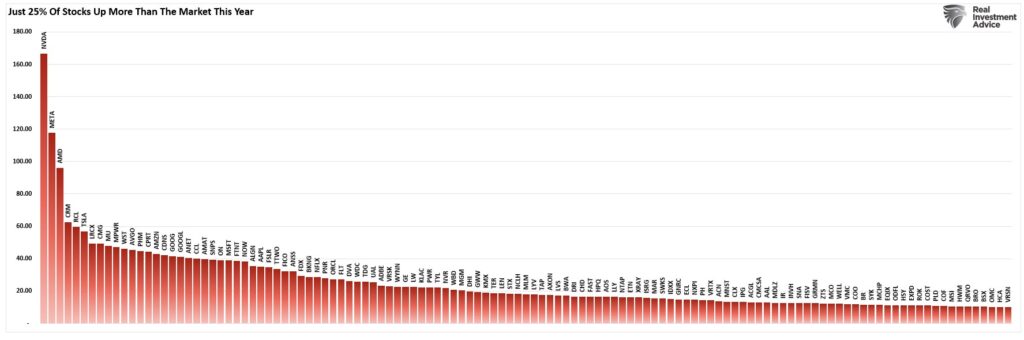

The chart below shows every stock in the S&P 500 and whether it is positive or negative for the year. As shown, quite a few stocks are positive for the year, but more than half are not. The horizontal red line shows the number of stocks with a return of greater than 10% year-to-date. This data is clearly different than what the Advance-Decline line suggests.

However, let’s drill down into the data a bit more. The next chart shows only the stocks in the S&P 500 that have positive returns (as of the end of May) for the year. (Click the chart to enlarge) As noted above, out of 500 stocks in the index, less than half are positive for the year, and many are just barely positive.

However, on a year-to-date basis, less than 25% of stocks are sporting returns greater than the market as of the end of May.

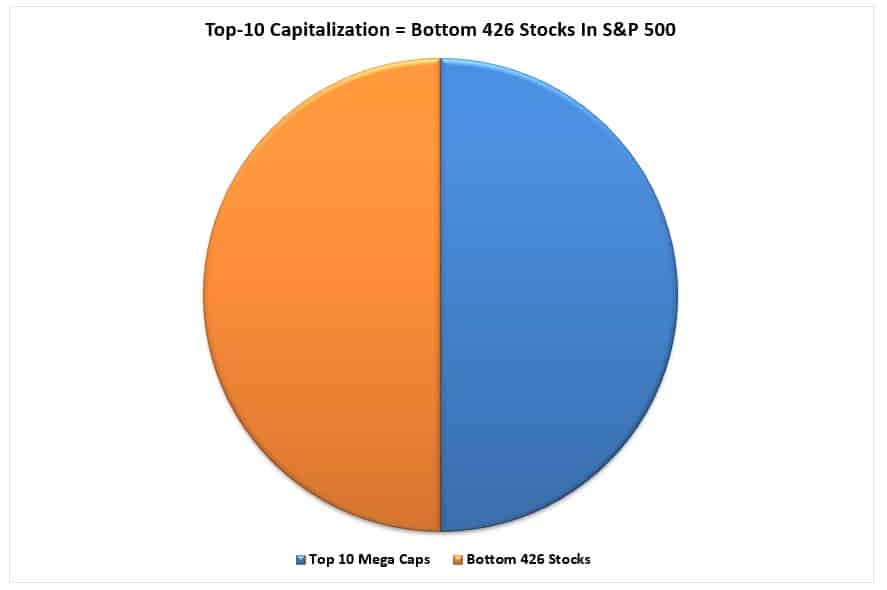

Of course, the mega-cap stocks are leading the returns for the year by a large margin. Such is an important fact when you consider the weights of these mega-capitalization companies within the S&P 500 index. Each percentage point gained in those stocks has an outsized impact on the index as a whole. As shown, each point gained by the top 10 companies in the index has the same impact as that gained by the bottom 426 stocks.

If the bottom 426 stocks gained one point each, but the top 10 stocks were flat, the market advance would be zero. In other words, the market breadth, as determined by the advance-decline line, would be strong, but the market would not advance.

See the problem?

The Nasdaq 93 Breaks Out

The graph below shows the Nasdaq 100 has been on a tear, led by a small handful of stocks. While its performance is very bullish, many technicians worry about the breadth of the market. The second graph shows the Nasdaq 93. These are the 93 other companies not leading the market higher. While its performance has been much weaker than the index, it is breaking out in a bullish pattern. Such bodes well for the market. Especially if the “others” in the S&P 500 and Russell also show bullish tendencies.

Citi Economic Surprise Index Back to 2022 Highs

The Citi Economic Surprise Index, shown below in blue, is back to levels last seen in January 2022, when the S&P 500 was at record highs. The index, which tends to oscillate, measures how economic forecasters over or underestimate economic data. A higher reading, as we have now, says forecasters have been underestimating economic activity. While at its highest level in a year and a half, the underestimating trend can continue.

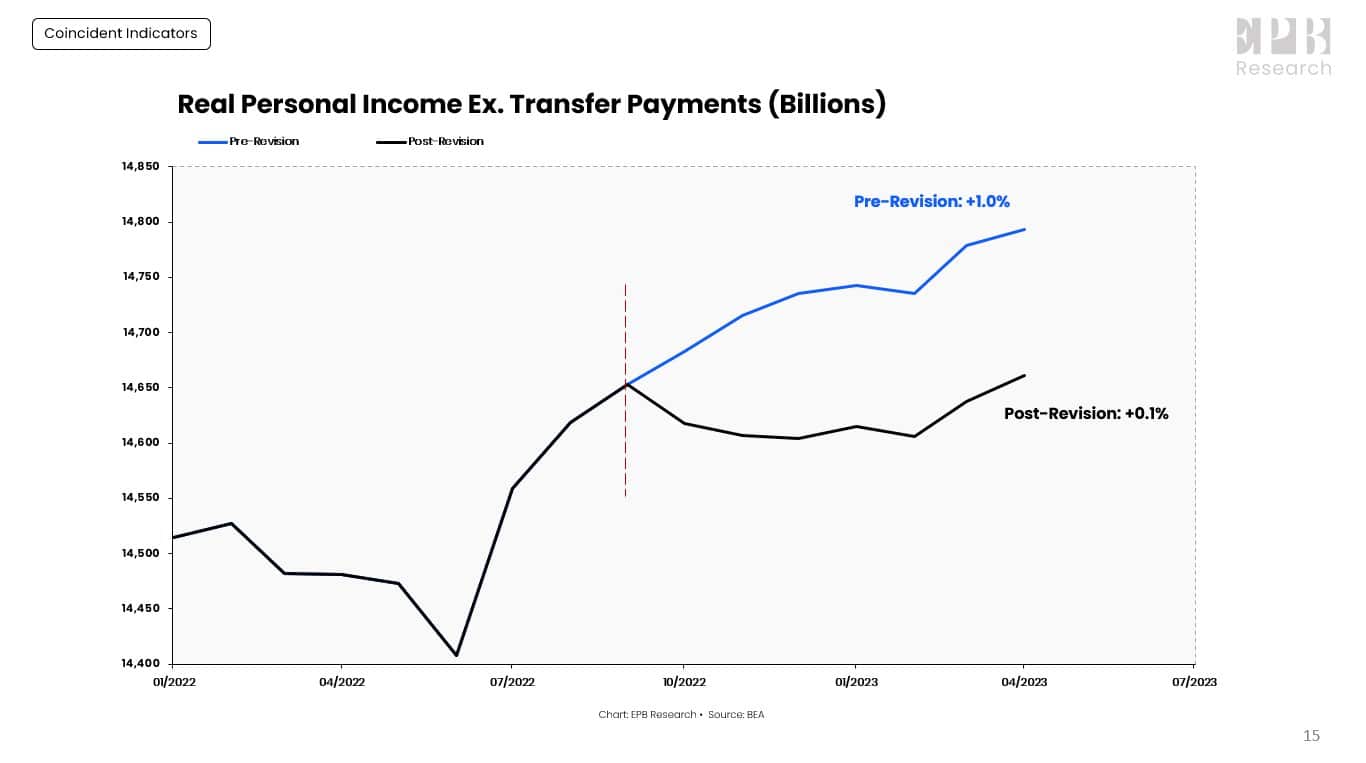

Two key factors make this index hard to assess. First, economic data is often revised, and the new data does not affect the Citi index. For example, a key economic indicator, real personal income excluding government transfer payments (graph courtesy of EPB Research), as shown in the second graph, highlights that what was initially reported at 1% growth was, has been revised since to show no growth. If an economist predicted flat growth, their forecast would have counted as a positive surprise in the index. In reality, such a forecast was not a surprise.

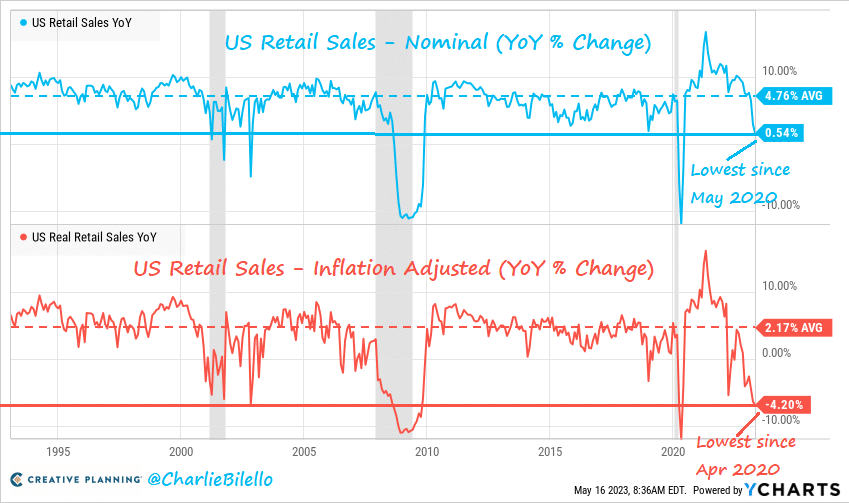

The second point is that high inflation skews many data points. Some economic data, like retail sales, do not account for inflation. Thus forecasting can be extremely difficult as an economist must forecast actual sales and inflation for many goods and services. Similar complications occur with data that do adjust for inflation. The third graph from Charlie Bilello shows retail sales adjusted for inflation have been much lower than the nominal data reported by the BLS.

Student Loan Payments Restart

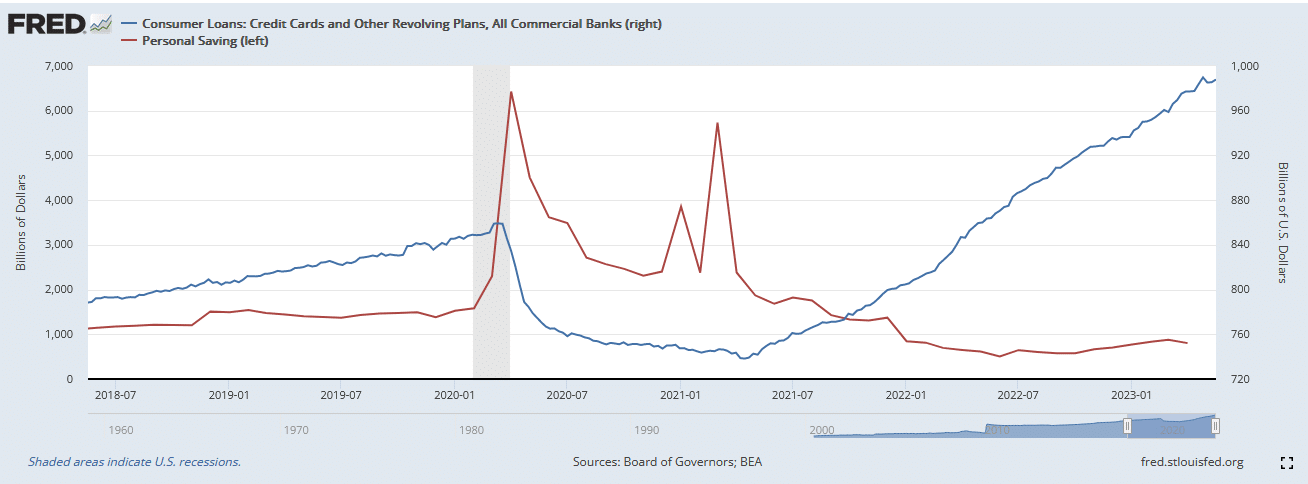

If the debt cap deal passes, student loan payments, which have been suspended for over three years, will resume on July 31st. That would be a month earlier than the previously announced date. Economists estimate that interest payments on the $1.6 trillion of student debt will account for approximately $5 billion in monthly interest payments. Think of this as another form of stimulus that will be taken away. The new debt payments are not necessarily large. Still, they are another financial burden for consumers, with record credit card balances, higher balances of other debt forms, and diminished savings accounts.

Through the fourth quarter of 2022, the New York Fed’s Report on Household Debt and Credit shares the following:

- Total household debt rose by $394 billion, or 2.4 percent, to $16.90 trillion.

- Credit card balances, shown below, are nearly $1 trillion, about 20% higher than pre-pandemic levels.

- Mortgage balances rose to $11.92 trillion.

- Auto loan balances increased to $1.55 trillion.

- Student loans are $1.60 trillion.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.