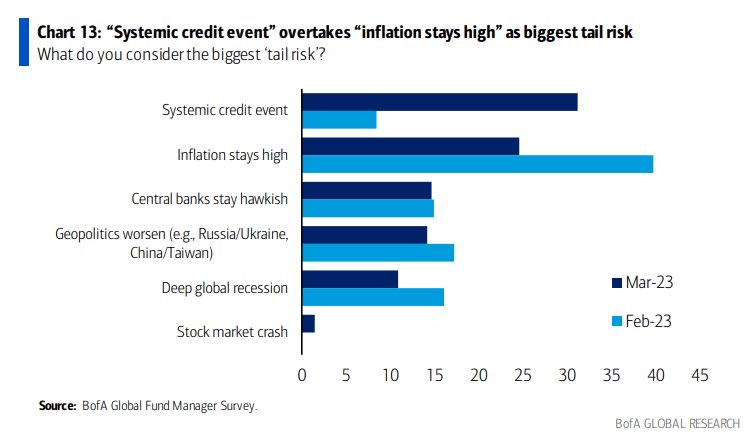

Courtesy of BofA, the survey results below show that professional money managers are now more concerned with credit risk than lingering high inflation. This survey also inadvertently points out the Fed’s delicate dance between financial stability and inflation. If rates stay high, money will continue to leak from banks to money market funds. Conversely, if the Fed lowers rates to take away the incentive to chase higher money market yields, inflation will stay higher than it would have.

While investors appear to fret over pending credit risks and high inflation, popular market-implied gauges provide no such warning. BB-rated corporate bond spreads, which are highly susceptible to credit risk contagion, trade near the average of the post-financial crisis era. Bond investors are clearly not worried about credit risk. Similarly, market-implied inflation gauges and the Cleveland Fed’s forecast of five-year and one-year inflation, respectively, are only slightly above average. The critical takeaway is that the survey asks whether credit risk or inflation is the biggest tail risk, not the probable outcome. Given the data we shared on credit risk and inflation expectations, investors are placing low odds on either becoming problematic.

What To Watch Today

Economy

Earnings

- No notable earnings releases

Market Trading Update

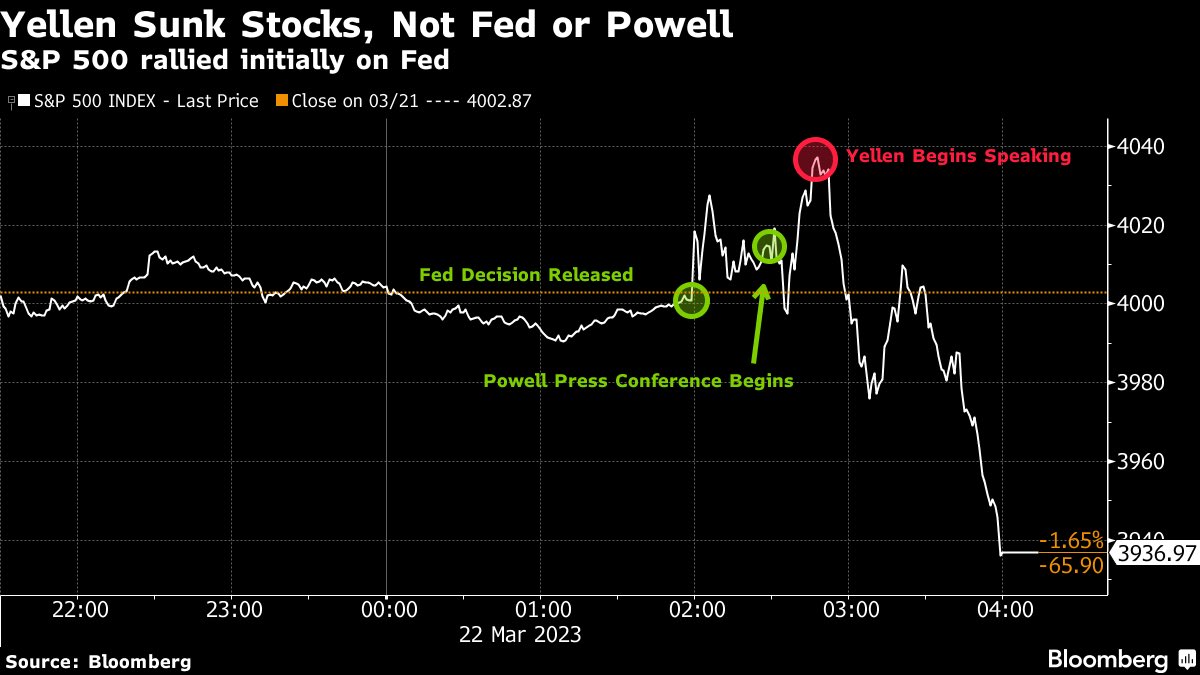

Yesterday, the market recovered some following Wednesday’s post-FOMC meeting selloff due to Janet Yellen’s remarks that the FDIC would NOT insure all depositors. Apparently, the FOMC and the Treasury are not on the same page, given that Powell stated the banking system was sound and there were tools to provide stability.

Nonetheless, buy signals remain in place for the stock market, but today I want to turn my attention to the bond market, which is extremely overbought, given the recent drop in yields. If you didn’t lock in yields above 4%, that “train has likely left the station.” However, we expect some pullback in rates short-term which will provide another entry point to add to bond duration in portfolios. If the tightening of lending standards, as noted by Powell, leads to a recessionary outcome, as they always have, the yields have further to fall. The opportunity to own bonds is likely just starting, but as we warned, when the rally begins, it will move quickly.

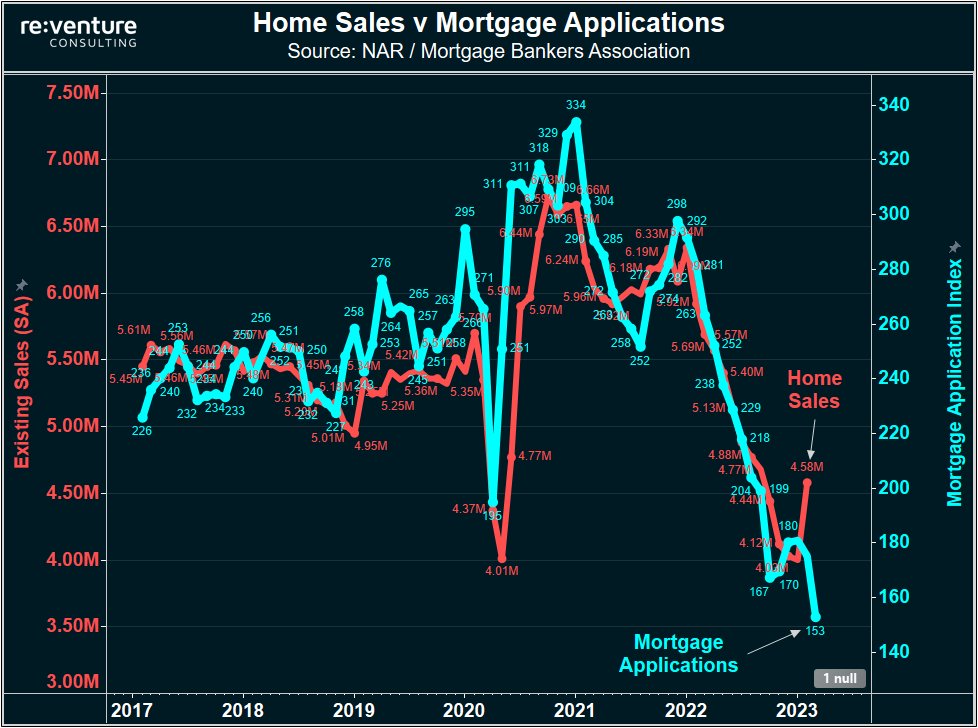

Home Sales vs. Mortgage Applications

The graph below from re:venture Consulting shows new home sales recently spiked, albeit historically low. At the same time, the MBA mortgage applications index plunged to a 20+ year low. So which is correct? Most homebuyers apply for a mortgage before buying a home. As you can see at some points in the graph, mortgage applications tend to lead home sales by one to two months. The uptick in home sales is not likely sustainable.

Pause is in the Eye of the Beholder

Powell clearly stated the Fed has no intention of lowering rates this year. Per his press conference: “In that most likely case, if that happens, participants don’t see rate cuts this year. They just don’t.“

The market thinks they will lower rates aggressively. Fed Funds futures are pricing a 1% cut in Fed Funds by year-end. Further, two-year Treasury notes yield 1% less than Fed Funds.

As we share below, courtesy of @BlacklionCTA, the spread between two-year note yields and Fed Funds is the most negative since 2008. If Powell is true to his word, two-year note yields will likely rise and close the divergence. If the Fed follows history, the Fed will probably pause for a while and then aggressively lower rates. The significant divergence between the market’s outlook and the Fed’s is important. The divergent views will correct. It’s just a question of when and how much volatility accompanies the transition.

Powell and Yellen are on Different Pages

On Wednesday, stocks traded well after the FOMC announcement despite the Fed raising rates and not signaling a pivot this year. However, deep into Powell’s press conference, the stock market started falling rapidly. As Jerome Powell told reporters, “and I think depositors should assume that their deposits are safe,” Janet Yellen was also making headlines. Yellen bluntly told Congress that the FDIC was not considering “blanket insurance” for deposits.

Per Yahoo:

Yellen told the Subcommittee on Financial Services and General Government that President Joe Biden’s administration was focused on stabilizing the banking system and improving public confidence in it. But she said the administration was not considering expanding bank deposit guarantees beyond the FDIC’s current $250,000 limit, seen as a major roadblock to swift action to stem a deeper crisis.

Such divergent public opinions on stabilizing the banking system did not sit well with investors. We suspect that if more banks struggle, their opinion on the matter will merge into the same opinion and likely remove any doubt of a Treasury/FDIC/Fed backstop for all $17 trillion of banking deposits.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.