Inside This Week’s Bull Bear Report

- Buy Signals Trigger, But Financial Stress Continues

- If It Looks Like Q.E.

- How We Are Trading It

- Research Report – Consensus View Of “No Recession.” Could It Be Wrong?

- Youtube – Before The Bell

- Stock Of The Week

- Daily Commentary Bits

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

Buy Signals Trigger But Bank Crisis Weighs

Despite concerns of a banking crisis, the markets triggered multiple buy signals as the market rallied for a second week.

These buy signals follow our early February article discussing the “sell signals” at that time.

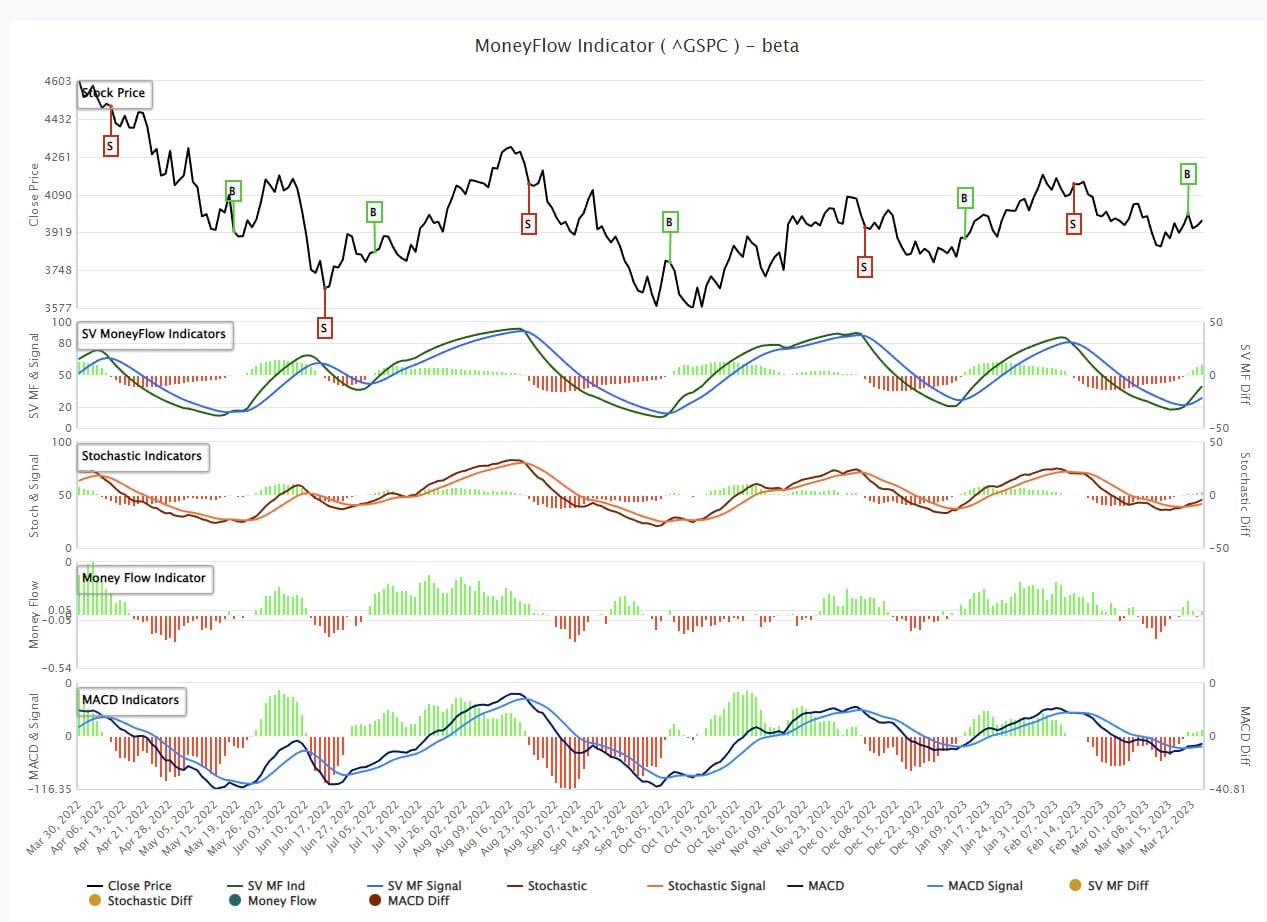

“That commentary remains vital as our primary short-term ‘sell’ indicator has triggered for the first time since early December. Such has previously provided excellent signals of corrections and rallies. The chart below is courtesy of SimpleVisor.com and shows our proprietary money-flow indicator and the Moving Average Convergence Divergence (MACD) signal.

While that sell signal does NOT mean the market is about to crash, it does suggest that over the next couple of weeks to months, the market will likely consolidate or trade lower. Such is why we reduced our equity risk last week ahead of the Fed meeting.”

Following that article, the market declined, taking out the 200-DMA and breaking the critical uptrend support from the October lows. The market did hold support at the December lows keeping the bullish trend intact. However, this past week, those sell signals reversed to buy signals.

The MoneyFlow chart is updated below, showing the new “buy signal” that occurred on Tuesday.

It isn’t just the MoneyFlow signal suggesting the bulls have regained control, but also the Moving Average Convergence Divergence indicator (MACD), triggering a confirming “buy signal.” Furthermore, the market defended the 200-DMA, repeatedly confirming support despite the negative headlines.

With these buy signals in place, investors should modestly increase equity exposure, as the most likely path for stock prices is higher over the next couple of weeks to months. However, with the banking crisis unfolding, such could limit any upside to equity prices near term until the crisis is “contained” or the Fed reverts to monetary accommodation.

While there is a lot of “headline noise” surrounding the recent banking troubles, the markets ultimately respond to monetary support. The current Fed and Treasury interventions are the first steps to more accommodation. While the supports don’t liquify markets directly, the question is whether investors will step into risk on expectations of more accommodation to come.

A look back at the history of bailouts and accommodative actions by the Fed, and its shaping of investor behavior, can give us some clues as to potential market reactions.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

If It Looks Like A Duck

“If it looks like a duck, quacks like a duck, and walks like a duck…it’s probably a duck.”

In Tuesday’s “Not Q.E.” blog, we discussed the Treasury and Federal Reserve’s recent intervention to shore up the banking sector.

“The additional funding will be made available through the creation of a new Bank Term Funding Program (BTFP), offering loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. These assets will be valued at par. The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.“

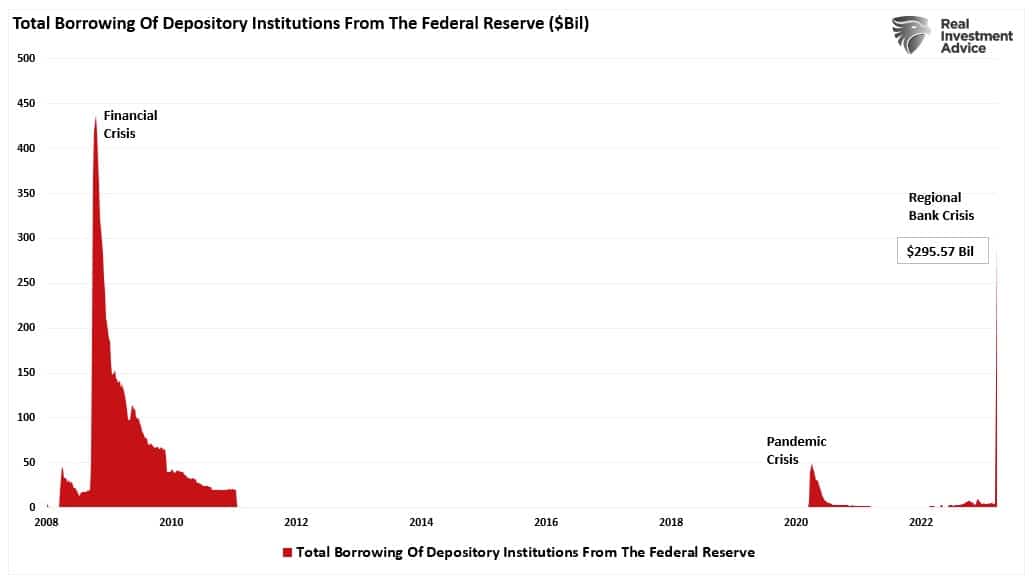

Banks quickly tapped the program, as shown by the $152 billion surge in borrowings from the Federal Reserve. It is the most significant borrowing in one week since the depths of the Financial Crisis.

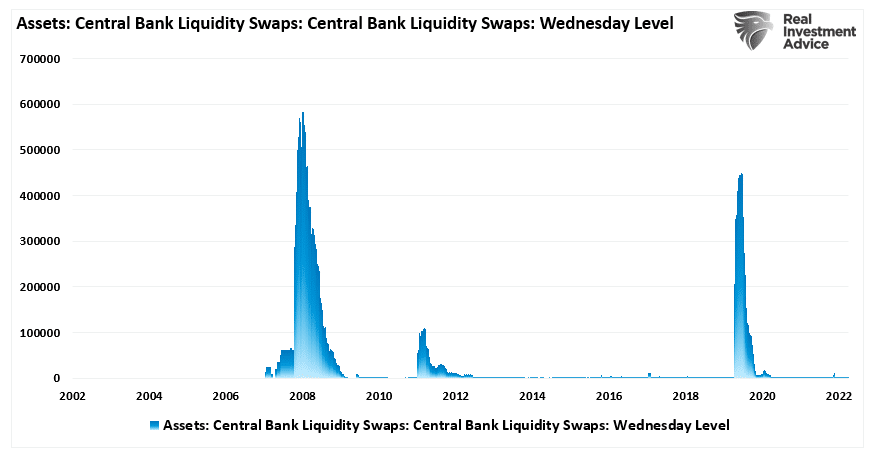

In addition to that program, the Fed also reopened its “Dollar Swap Lines” for international banks to provide additional liquidity in the wake of the failure of Credit Suisse.

“The Fed announced they will offer daily currency swaps as part of the CS bailout. These swaps are essentially collateralized dollar loans to foreign central banks. From the Fed’s perspective, the loans stop central banks from having to sell U.S. Treasury securities to raise cash. They also provide central banks with needed dollar funding to pass on to their local banks. The bottom line is the Fed is indirectly helping or bailing out foreign banks. At the same time, they are making sure U.S. Treasuries do not get sold in mass and the dollar retains its value.”

The graph below provides a history of the usage of the swap lines. Comparing what will occur to what occurred in 2020 and 2008 may guide us on the seriousness of foreign banking problems. (Note: The data only updates on Wednesday of each week; therefore, we won’t know the usage of the dollar swap lines until next week.)

Market Hopes It’s A Duck

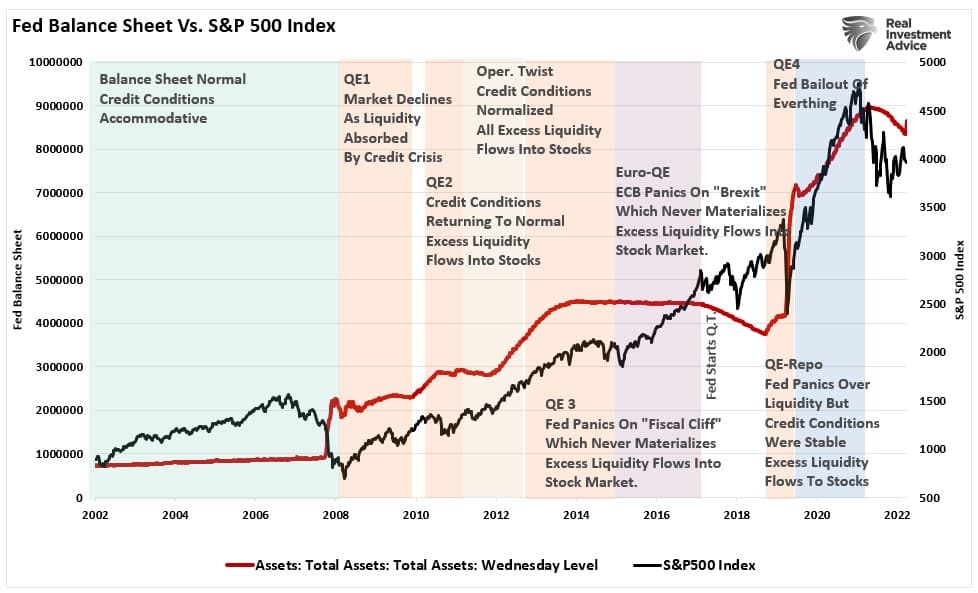

While none of this liquidity is “Q.E.,” the Fed trained markets for over a decade to have a “pavlovian response” to interventions.

“Classical conditioning (also known as Pavlovian or respondent conditioning) refers to a learning procedure in which a potent stimulus (e.g., food) becomes paired with a previously neutral stimulus (e.g., a bell). Pavlov discovered that when he introduced the neutral stimulus, the dogs would begin to salivate in anticipation of the potent stimulus, even though it was not currently present. This learning process results from the psychological “pairing” of the stimuli.

Importantly, for conditioning to work, the “neutral stimulus,” when introduced, must get followed by the “potent stimulus” for the “pairing” to complete. For investors, as the Fed introduced each round of “Quantitative Easing,” the “neutral stimulus,” the stock market rose, the “potent stimulus.”

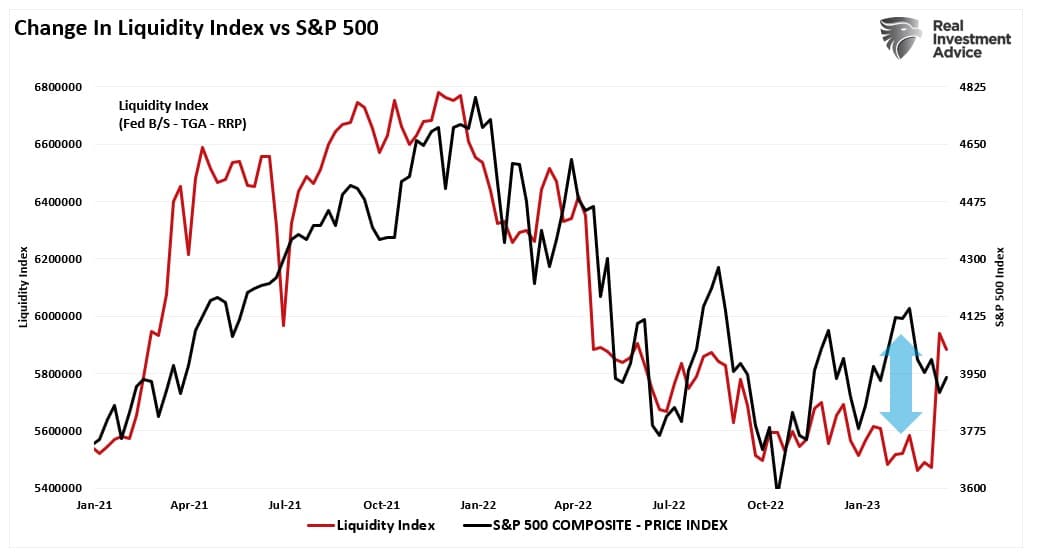

Another way to look at this is through the liquidity measure of the Fed’s balance sheet, less the Treasury general account, less the Fed’s reserve program. That combined measure has a decent correlation with changes in the market.

Furthermore, the preceding interventions, combined with statements by Treasury Secretary Janet Yellen, were essentially “verbal easing.”

- U.S. Treasury Secretary Yellen said U.S. aggregate deposit outflows from regional banks have stabilized. At the same time, she noted that Fed, FDIC, and Treasury actions reduce the risk of further bank failures that would’ve imposed losses despite insurance. Similar actions to protect depositors could be warranted if smaller firms suffer deposit runs that pose a risk of contagion.

- U.S. Treasury Secretary Yellen said the banking system is sound despite recent pressures and is committed to taking actions to mitigate financial stability risks. In contrast, Deputy Treasury Secretary Adeyemo said the Treasury is mulling what steps can be taken to strengthen U.S. financial stability further.

These verbal assurances are unsurprising as the Fed is trapped between saving banks and fighting inflation. We repeatedly stated over the past year that the Fed’s rate hike campaign would eventually “break something.” To wit:

“There have been absolutely ZERO times in history the Federal Reserve began an interest-rate hiking campaign that did not eventually lead to a negative outcome.“

We know now that the Fed’s aggressive rate hikes strangled banks by reducing reserves and “breaking” the financial sector.

The bailout of banks, and the Fed’s opening of the dollar swap lines, have always previously preceded further monetary accommodations. As such, the markets ran higher ahead of the FOMC meeting announcement assuming the Fed would hint at a “pivot.”

Which is essentially what they did.

What The Fed Said

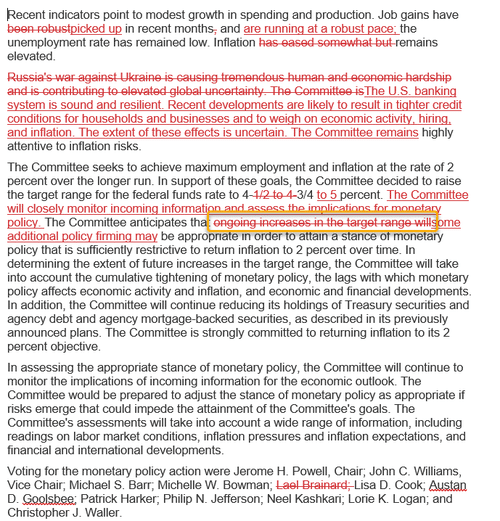

On Wednesday, the Federal Reserve hiked interest rates by 0.25%. While many hoped for a “pause,” given the massive support given to the financial markets this past week, such would have sent a message that the financial sector was in more trouble than communicated.

As Mike and I stated over the last two weeks, we expected a rate hike with a nod to the “stability of the banking sector.” We were not disappointed.

- FED RAISES BENCHMARK RATE 25 BPS TO 4.75%-5% TARGET RANGE

- FED WILL CONTINUE THE SAME PACE OF REDUCING TREASURY, MBS HOLDINGS

- FED: US BANKS SOUND, RESILIENT BUT EVENTS TO WEIGH ON GROWTH

Specifically, given the current liquidity programs noted above, the Fed stated the central bank would use all its tools to safeguard the banking system.

“Our banking system is sound and resilient, with strong capital and liquidity. We will continue to monitor conditions in the banking system closely and are prepared to use all of our tools as needed to keep it safe and sound. In addition, we are committed to learning the lessons from this episode, and to work to prevent episodes from events like this from happening again.”

Of course, given that the Fed’s rate hikes caused the banking issue, it will be interesting to see what lessons were learned. Nonetheless, they removed much of the previously existing “hawkish language,” suggesting only one more rate hike this cycle.

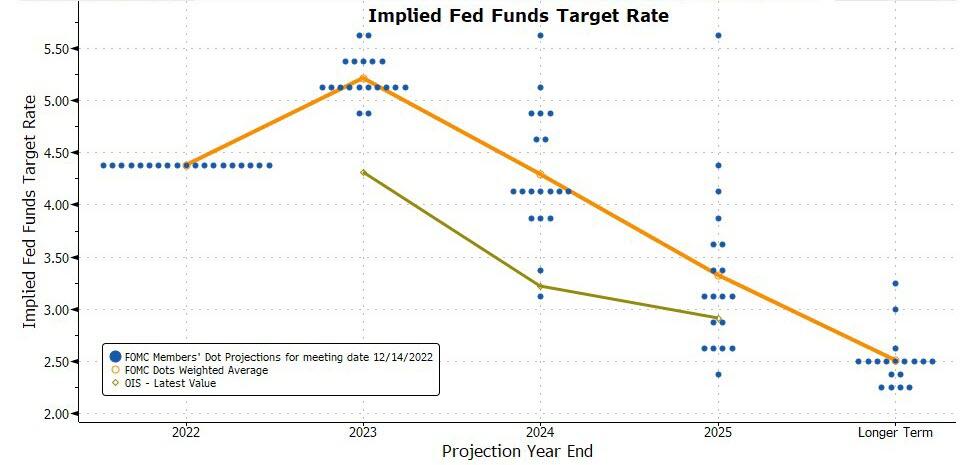

The Fed’s famous “Dot plot” also got a bit of a “dovish” makeover from where it stood in December.

While the bulls got a “mild pivot,” the Fed maintains its “image” of fighting inflation. However, simultaneously, they are “sticking fingers” in the “financial dike,” springing multiple leaks from U.S. banks to Credit Suisse and now potentially Deutsche Bank.

During Powell’s presser, he repeatedly stated his commitment to fighting inflation. Interestingly, he did note the “banking crisis” would further tighten credit conditions. Such acts as an “effective rate hike” and tighter credit conditions always precede recessions.

We will soon find out whether Powell’s comment the “banking system is sound and resilient” is the modern version of Ben Bernanke’s infamous declaration before Congress in 2007:

“We do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system.”

If it does, then such will have enormous impacts on the economy.

How We Are Trading It

As noted last week, as the banking crisis unfolded, we started raising additional cash and eliminating economically sensitive sectors for now. While we like the companies that we own fundamentally, in the short term, fundamentals won’t protect capital when the market recognizes either a financial or recessionary event materializing. When things stabilize, we will revisit adding these sectors to our portfolios.

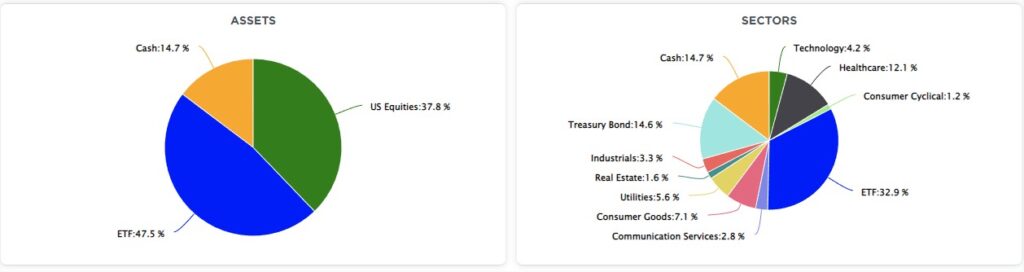

We are currently underexposed to equities. As such, we increased those levels as buy signals triggered. It is a challenge given that recessionary risks have recently increased, but we must follow our discipline accordingly. (The ETF allocation comprises short-duration Treasury bonds, floating rate, and long-dated Treasuries. You can view our models in real-time at SimpleVisor.com)

As noted last week, you can increase exposure accordingly if you are underweight equity risk.

- Move slowly. There is no rush to make dramatic changes.

- DO NOT try and fully adjust your portfolio to your target allocation in one move. Again, after significant declines, individuals feel like they “must” do something. Think logically about where you want to be and adjust to those levels.

- Begin by selling laggards and losers. These positions were dragging on performance as the market rose, and they led on the way down.

- Move “stop-loss” levels up to recent lows for each position.

- Be prepared to sell into the rally and reduce overall portfolio risk. As the rally ensues, you will start to second-guess selling. Avoid that emotional trap and follow through with your plan.

- If these rules make no sense, please consider hiring someone to manage your portfolio. It will be worth the additional expense over the long term.

While increasing exposure near-term, we are cautiously allowing the market to dictate these changes. However, we will reverse this process when “sell” signals re-emerge.

Have a great week.

Research Report

Subscribe To “Before The Bell” For Daily Trading Updates (Formerly 3-Minutes)

We have set up a separate channel JUST for our short daily market updates. Be sure and subscribe to THIS CHANNEL to receive daily notifications before the market opens.

Click Here And Then Click The SUBSCRIBE Button

Subscribe To Our Youtube Channel To Get Notified Of All Our Videos

Stock Of The Week In Review

Protection in Technology Stocks

While investors are worried about the banking and financial sectors and the growing odds of a recession, they remain enamored with the technology sector. Companies like MSFT, NVDA, and META have recently led the way with positive returns in down markets. As we show with four of the five stocks, smaller, lesser-known technology companies are also having a great year.

Year to date, technology (XLK) is up over 16%, while the S&P and Financials (XLF) are up 3.34% and down 8.86%, respectively.

This scan is purely based on technical studies. We are looking for technology companies that did well in the last few weeks and have consistently outperformed the broader markets over the previous few years.

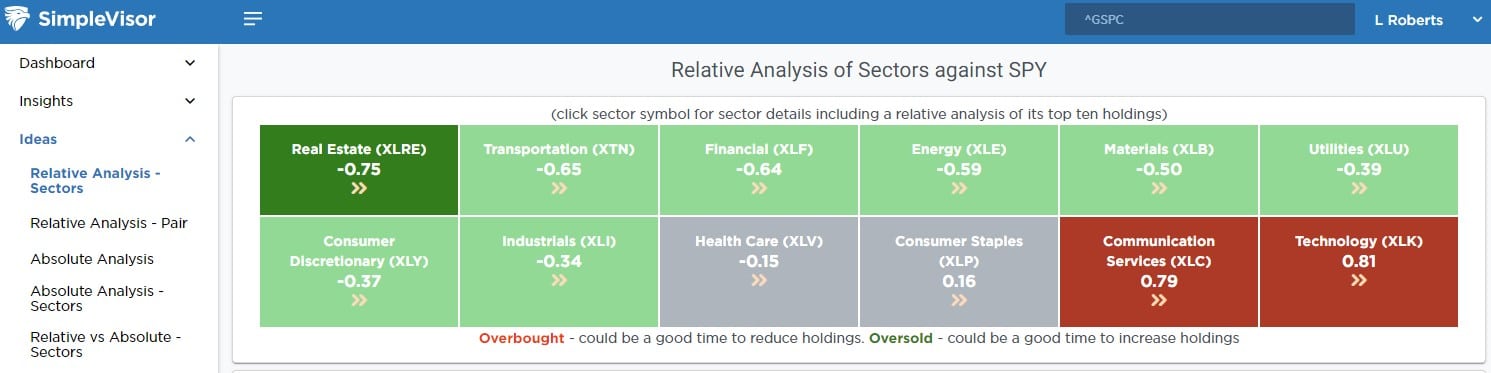

Our relative sector analysis on SimpleVisor is a great tool for figuring out which sectors are hot in the short term. The table below shows the Technology sector is grossly outperforming, while Real Estate and Financials lag.

Here is a link to the full SimpleVisor Article For Step-By-Step Screening Instructions.

Login to Simplevisor.com to read the full 5-For-Friday report.

Daily Commentary Tidbits

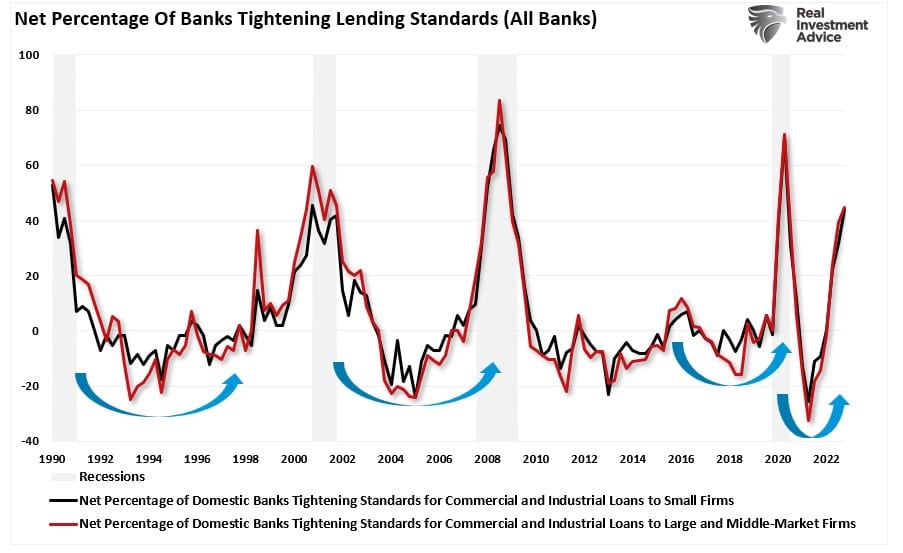

Long before Silicon Valley Bank failed, the banking sector was experiencing a silent bank run. Unlike the Great Depression, where lines of people clamoring for their money were blocks long, this silent bank run, as its name portends, has been out of sight until recently. There are a couple of reasons for this. First, online banking allows for split-second transfers from one bank to another bank or financial institution. Second, unlike the Depression, this silent bank run has been gradual and lacks media coverage.

Until the last week, the silent bank run has not been about solvency concerns such as the Depression. Instead, customers moved money from banks to higher-yielding options outside the banking sector. The graph below from Pictet Asset Management shows that money market assets and domestic bank deposits have trended in opposite directions since the Fed started hiking interest rates. As a result of the silent bank run, banks must tighten lending standards and sell assets. This is already happening. To wit: “The primary loan market feels like a Scooby Doo ghost town – recently deserted and a bit haunted.” – Scott Macklin -AllianceBernstein. Because the economy heavily depends on increasing amounts of credit to grow, this silent bank run will likely lead to a recession.

(Subscribe To The Daily Market Commentary For A FREE Pre-Market Email)

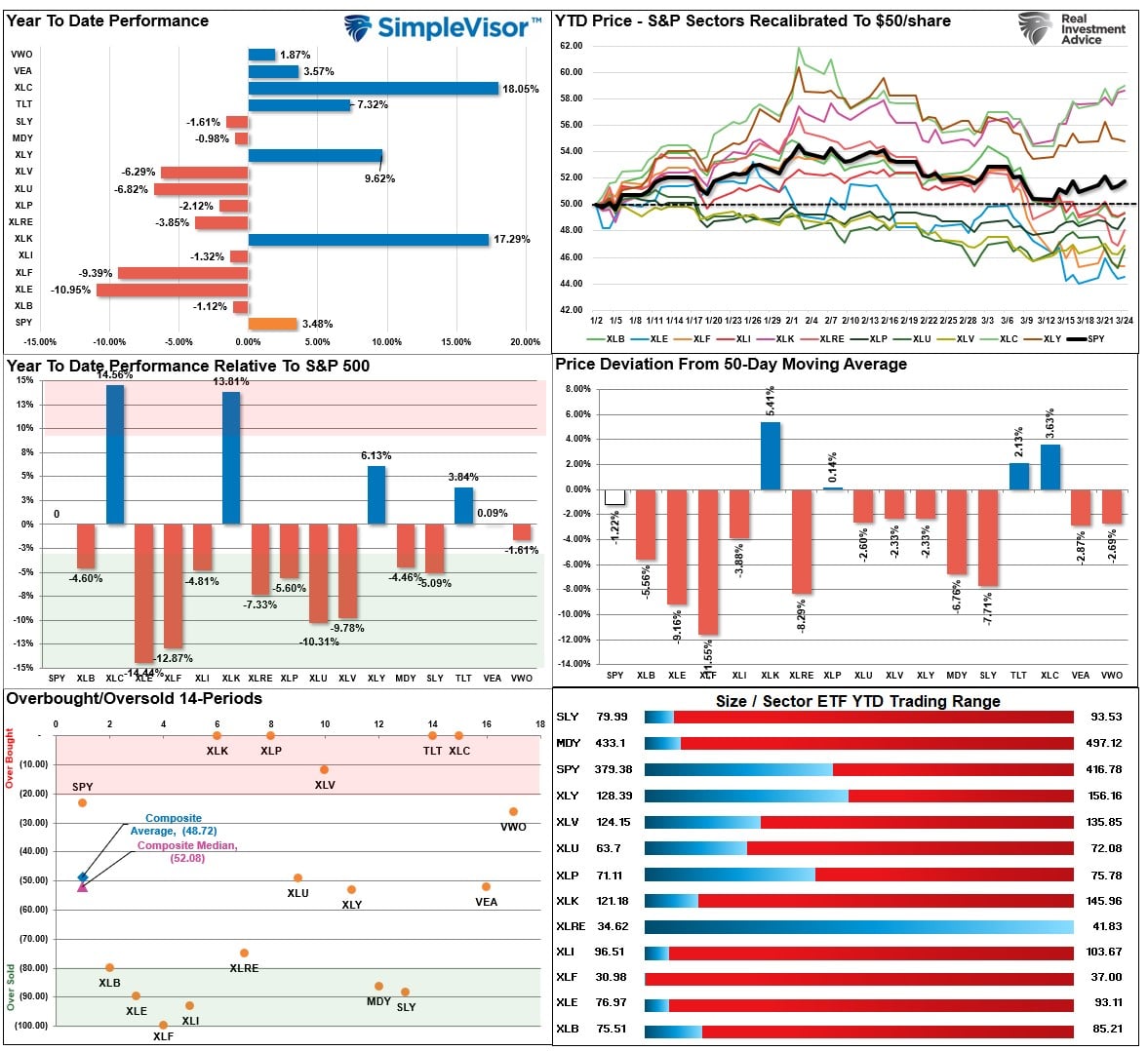

Bull Bear Report Market Statistics & Screens

SimpleVisor Top & Bottom Performers By Sector

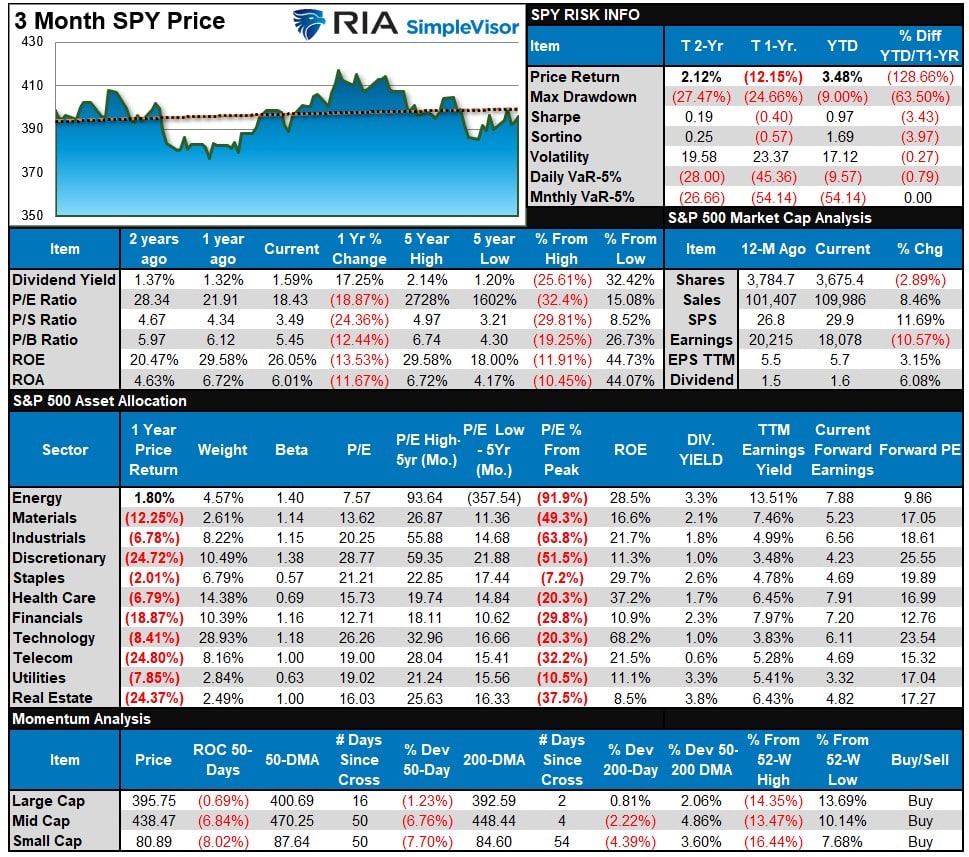

S&P 500 Weekly Tear Sheet

Relative Performance Analysis

Despite the headline risk of a banking crisis, the markets remained stable all week. Money has been crowding into Technology and Communications, which are now EXTREMELY overbought on both an absolute and relative basis. Last year’s most loved sector, Energy, is this year’s biggest loser and the most hated, the biggest winners. Such is how markets tend to work. Over the next couple of weeks, look for a rotation from the most overbought to the most oversold.

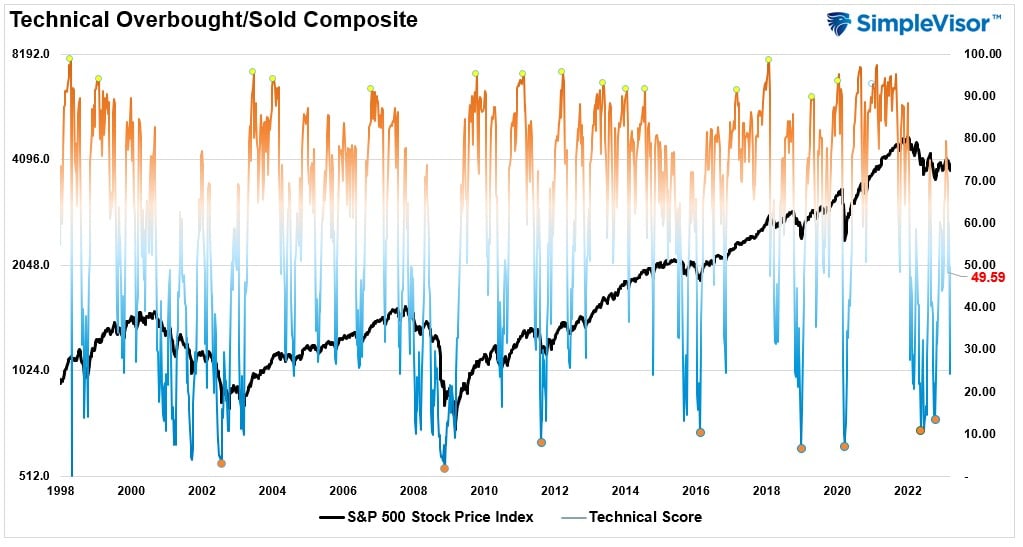

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. Markets peak when those readings are 80 or above, suggesting prudent profit-taking and risk management. The best buying opportunities exist when those readings are 20 or below.

The current reading is 49.59 out of a possible 100.

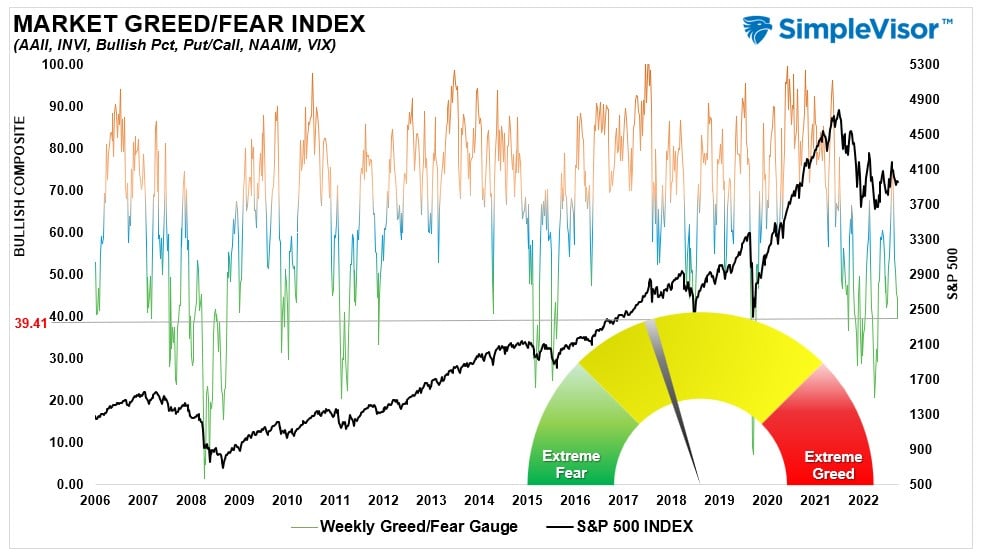

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” Gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, the more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 39.41 out of a possible 100.

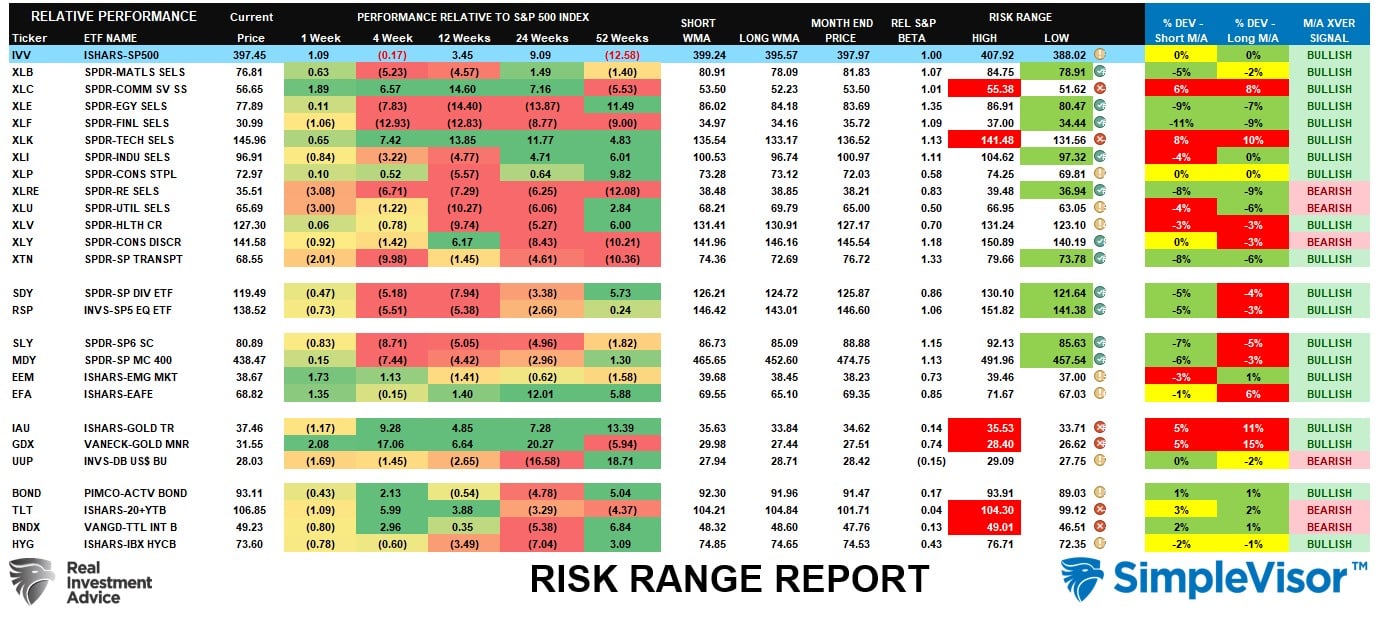

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “M” XVER” “Moving Average Cross Over) is determined by the short-term weekly moving average crossing positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

As noted above, Technology and Communications are highly overbought and well outside their monthly risk ranges. I would suggest taking profits in these sectors along with bonds, gold, and gold miners. The market will likely rotate to the laggards over the next few weeks and see a pick-up in the more defensive market sectors.

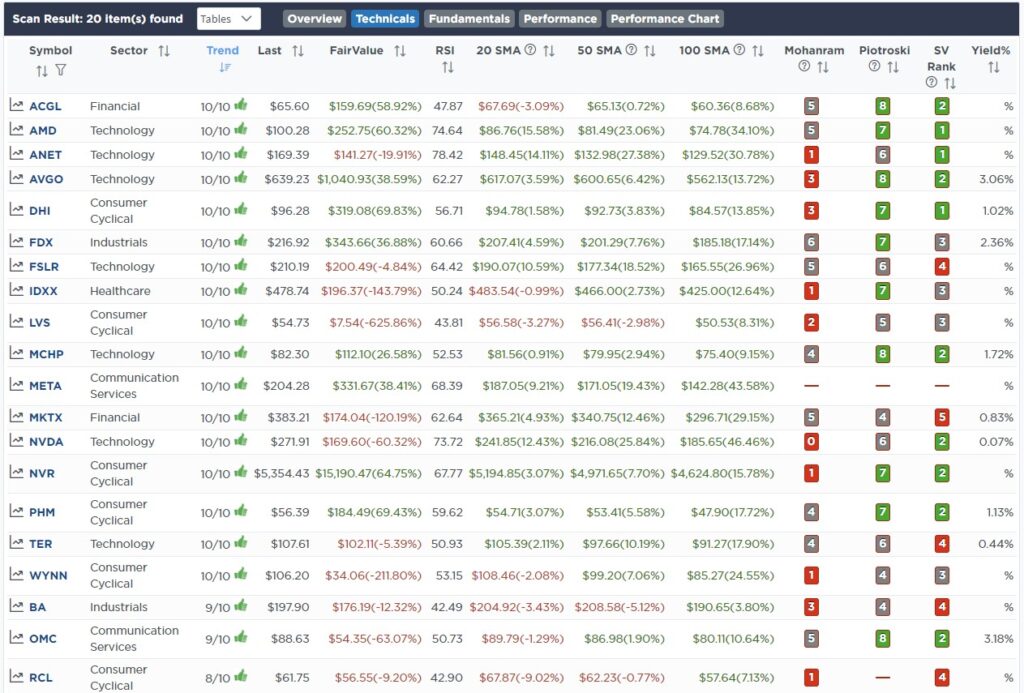

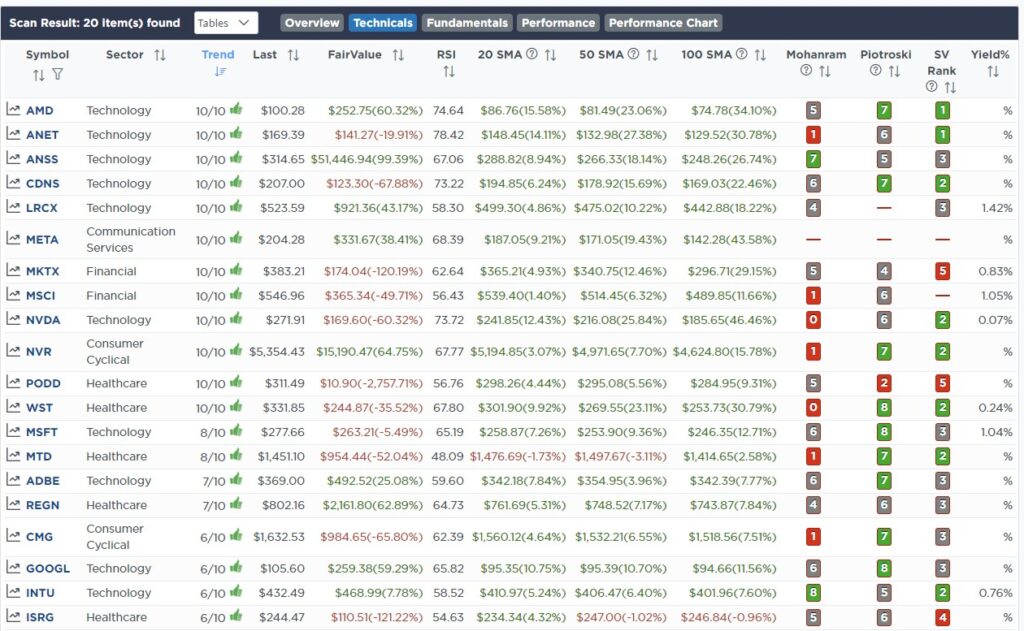

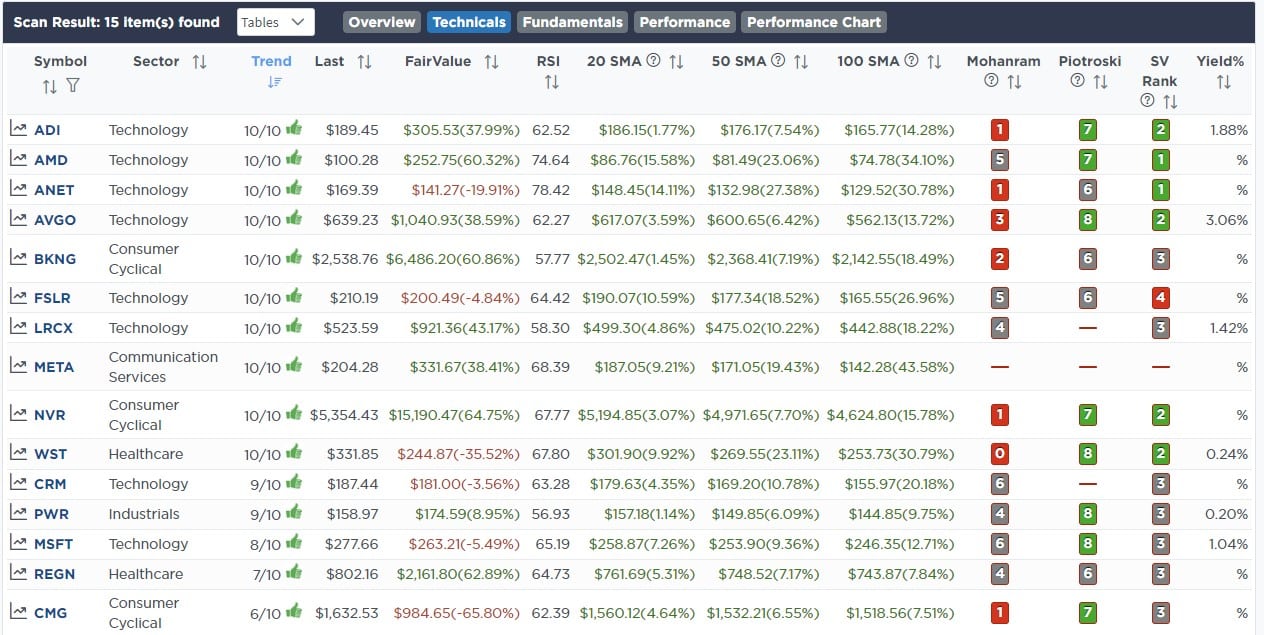

Weekly SimpleVisor Stock Screens

We provide three stock screens each week from SimpleVisor.

This week we are searching for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Fundamental And Technically Strong Stocks

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Fundamental Stocks With Strong Technicals

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

March 22nd

Following Powell’s press conference, we added 2.5% of QQQ and RSP to both models. Powell successfully walked the delicate balance between the banking crisis and tackling inflation. It appears a pause in rate hikes is coming soon, but not the pivot the market is pricing in.

Technically, the market is giving us good buy signals, and the relatively tepid, not bearish, reaction to the Fed is somewhat optimistic. We have precise stop-out levels below the 200dma, which is only a few percent lower on the S&P 500. We will have much more on the Fed and Press Conference in tomorrow’s Commentary.

These are starting positions for a trading holding in portfolios.

Both Models

- Initiate a 2.5% position in the Invesco S&P 500 Equal Weight ETF (RSP)

- Add a 2.5% position in the Invesco Nasdaq 100 Trust (QQQ)

Lance Roberts, CIO

Have a great week!