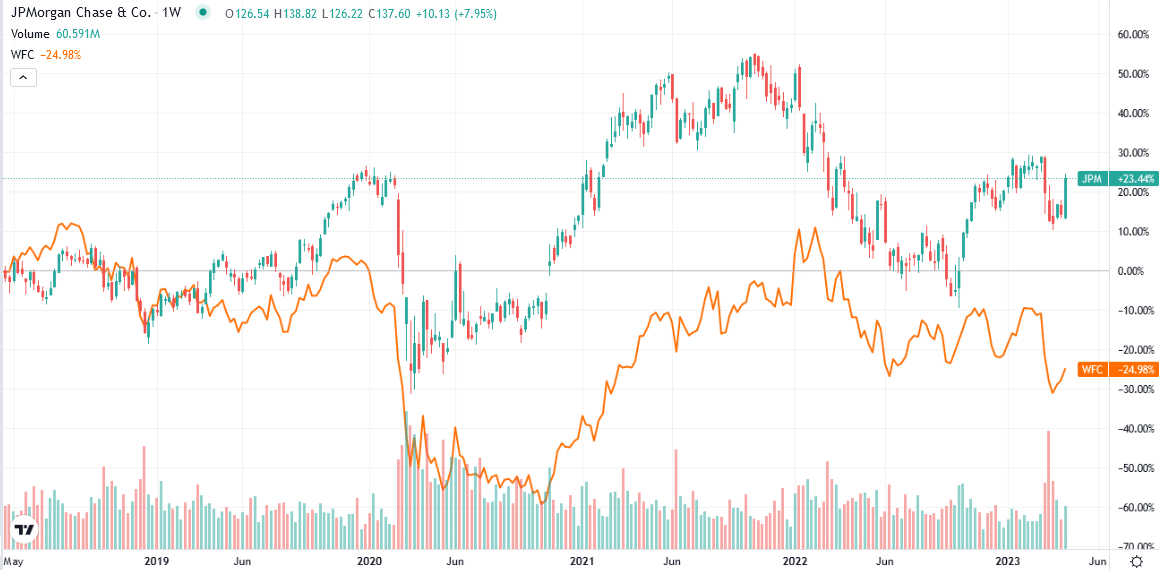

JP Morgan and Wells Fargo led off earnings season on Friday. Despite the woes hitting smaller banks, the big banks are in a highly profitable environment. The question facing big bank shareholders is how long such an environment lasts. Specifically, will the economy enter a recession, and what might that mean for credit losses and interest rates? To that end, JP Morgan added $1.1 billion to its loss reserves and another $1.1 in loan charge-offs. Wells Fargo added $1.2 billion to its loan loss reserves. The other factor facing big and small banks is how long interest rates will remain high, thus boosting their net interest margin and revenues.

Bloomberg reports that JP Morgan, Wells Fargo, and Bank America lost about half a trillion in deposits over the last year. That is not good, but there is a bright side to it. In its earnings report, JP Morgan notes that retail deposits paying near zero interest rose by 3%, while commercial deposits, often at higher interest rates, fell. So while net deposits fell, the funding margin may have improved for big banks. Small banks, with generally larger deposit losses, are forced to replace near zero percent funding (deposits) with the Fed’s BTFP program or financing from other banks. In either case, the more deposits lost, the more expensive replacement funds will dampen their net interest margin. Earnings from smaller banks over the coming week or two will shed more light on how the SVB crisis affected their earnings.

What To Watch Today

Economics

Earnings

- Many midsize regional banks are reporting this week, which should give us a better picture of bank stress.

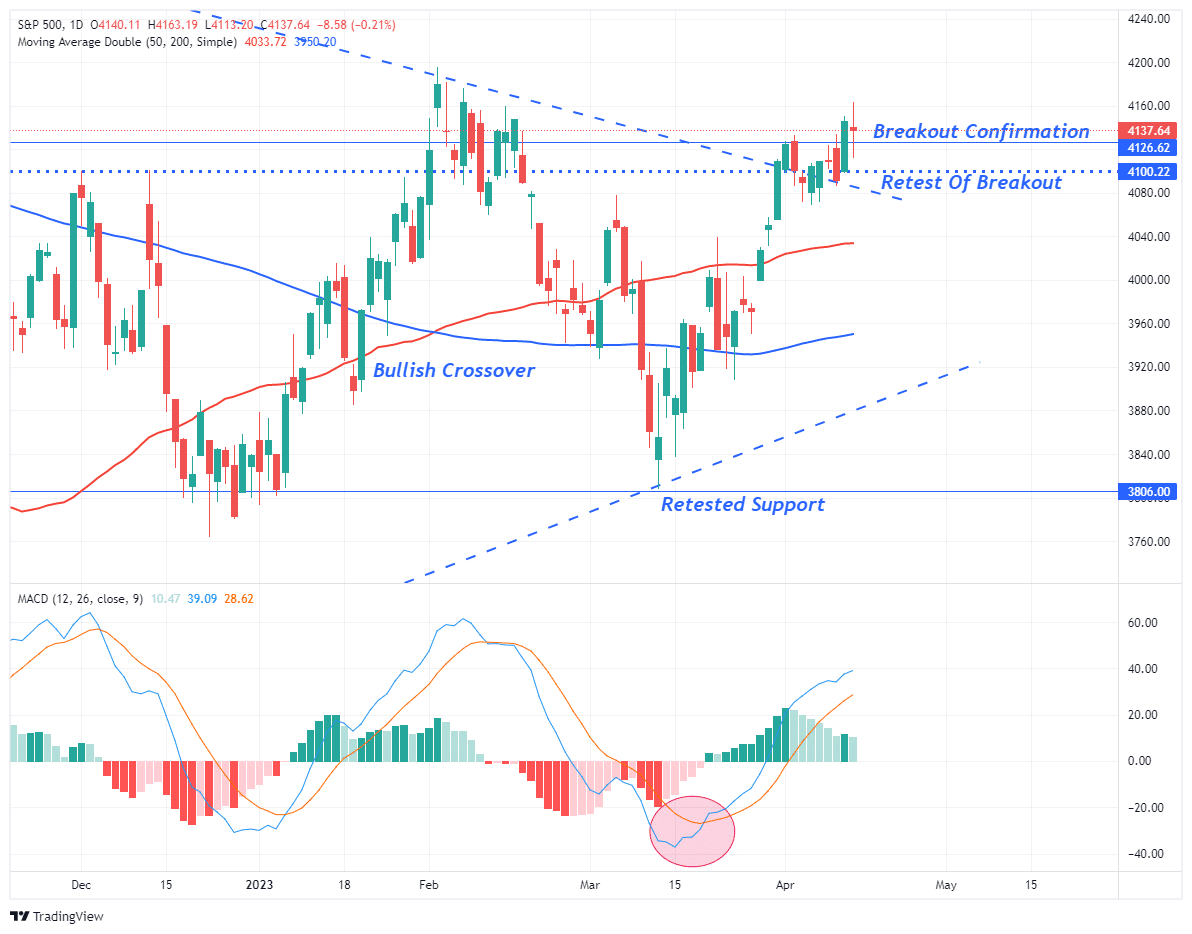

Market Trading Update

From a market perspective, not much changed. As noted last week:

“I would not be surprised to see more weakness next week, particularly given Friday’s employment report, which showed a slowing in the pace of hiring and suggests economic weakness is becoming more widespread.”

We saw this at the beginning of the week, but the market managed a rally on Thursday following a decline in the Producer Price Index, confirming that inflation eased in March. However, on Friday, disappointing retail sales sent the market lower. If you like volatile trading, this past week had plenty.

Nonetheless, after another retest of the downtrend line on Wednesday, the huge market rally on Thursday confirmed that bullish breakout by rising above the previous highs. The bull market is officially back, with the 50-DMA now well above the 200-DMA and BOTH moving averages trending higher. Notably, the MACD buy signals remain intact, which suggests that investors maintain increased equity exposures.

Even with all of the bullish signals confirming a move higher in the market is likely, such does NOT mean there won’t be 5 to 10% corrections along the way that can be used to increase equity exposure. Given the tug-of-war between market expectations and economic realities, I expect a continued increase in market volatility in the coming months. But, overall, the market action remains decidedly more bullish than bearish, and we must trade it as such.

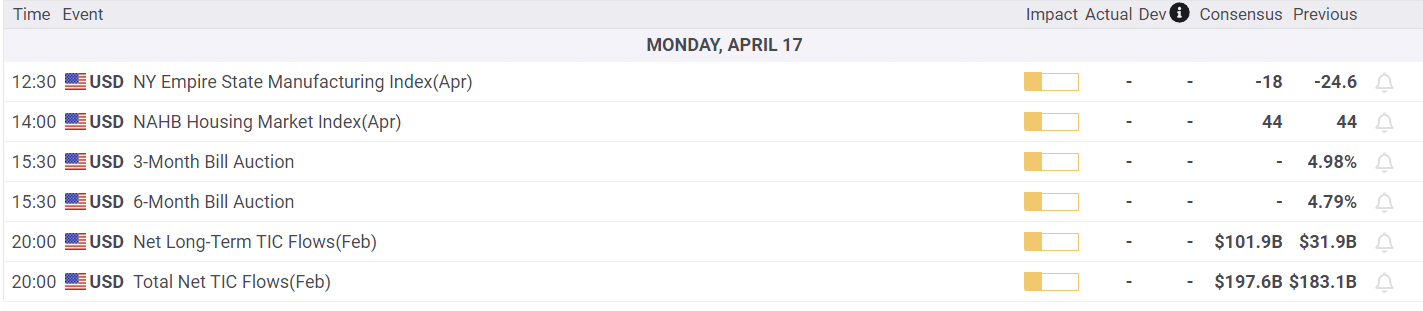

The Week Ahead

After the slew of inflation and retail sales data last week and the FOMC minutes, this week will be relatively quiet. The New York and Philadelphia Fed will release their manufacturing surveys. These tend to be decent leading economic indicators. Both surveys have been weak in recent months. Housing starts and building permits on Tuesday will provide some light on future homebuilder activity.

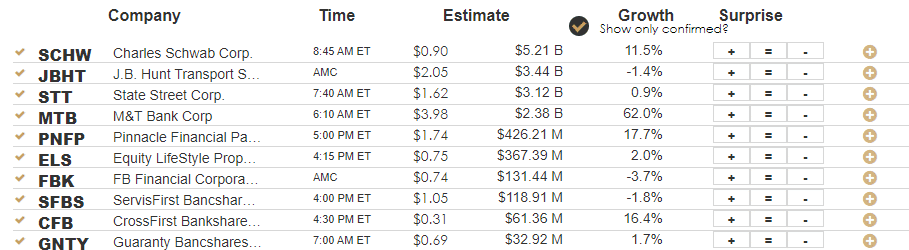

Corporate earnings will likely be a key driver of stock prices this week. Of importance will be a lot of the smaller regional banks. Charles Schwab, whose stock has been under considerable pressure due to its bank, will report this morning. Larger banks/brokers Bank America and Goldman Sachs, come out on Tuesday. Tesla, Proctor & Gamble, and several other prominent companies also release earnings.

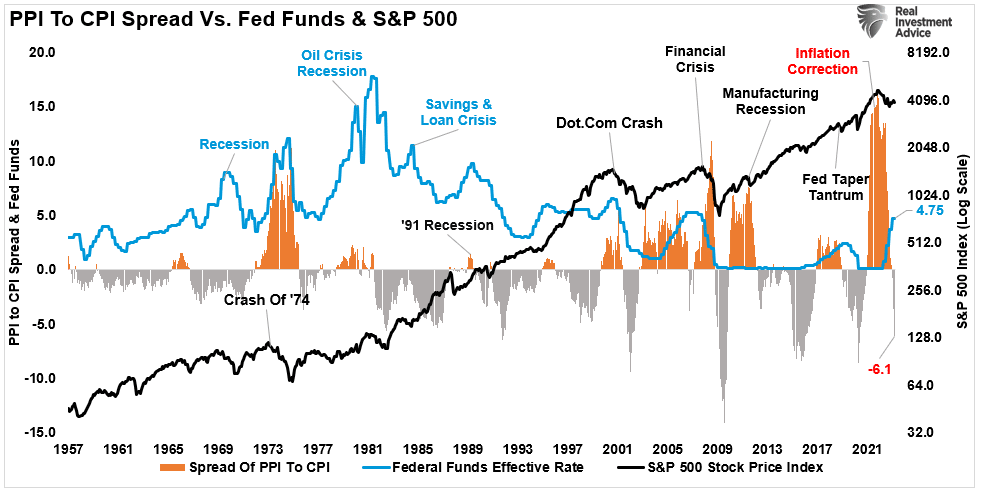

PPI-CPI Spread, Bullish, or Bearish?

PPI, often a leading indicator of CPI, fell by 0.5% while CPI rose by 0.1%. Year over year, PPI is running at 2.7% versus 5.0% for CPI. The widening gap between the two bodes well for inflation to continue to fall. But what does that mean for equities?

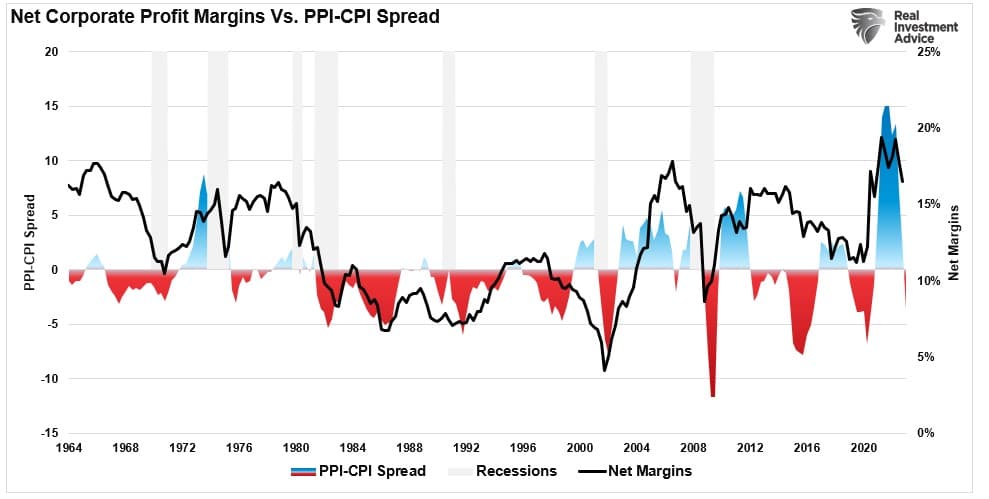

The first graph below shows that PPI/CPI spread typically goes negative near the end of corrections and bear markets. However, the end of corrections and bear markets also correspond with cuts in the Fed Funds rate, which we have yet to see. The second graph shows the correlation between corporate profit margins and PPI/CPI spread. Often declining spreads correlate with declining profit margins. There is something for the bulls and the bears in the graphs.

Retail Sales

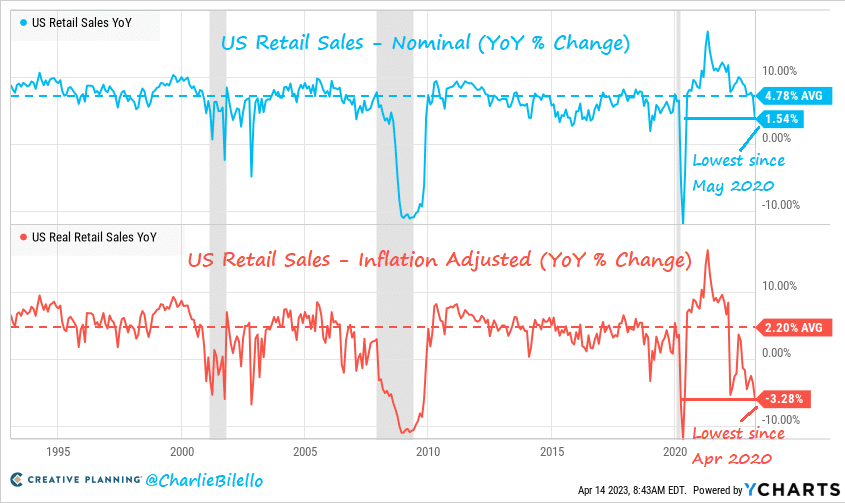

Retail Sales, a critical driver of economic activity, fell by 1% in March versus expectations for a 0.4% decline. Excluding autos and gasoline, retail sales fell by 0.5%. The graph below, courtesy of Charlie Bilello, shows the negative trend in annual retail sales. They are still growing but at the lower end of the pre-pandemic range. The second graph is more concerning. It shows that real retail sales (less inflation) are at levels associated with the prior three recessions.

Given that real wage growth has been negative for almost two years, it’s not surprising that consumers are struggling to spend realistically. Propping up retail sales in the prior two years was a significant savings drawdown and increased credit card usage. After nearly quadrupling with the pandemic stimulus in 2020 and 2021, personal savings are returning to pre-pandemic levels. Credit card growth is slowing but remains high. With buying power fading and some signs of weakness in the labor market, retail sales will likely remain weak.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.