The US and much of the global economy are driven by bank credit. Since debt has grown consistently faster than GDP for over 40 years, bank credit is critical in steering economic activity. Given the strong dependence on debt for growth, a pick-up in bank credit levels typically results in stronger GDP growth and vice versa. We show the correlation between bank credit with a six-month lead time and GDP to the left. Of the 180 quarterly data points dating back to 1976, there are only two instances where bank credit shrank annually.

As we wrote in Treasury Yield Curves, the steeply inverted yield curve sharply reduces the incentive for banks to lend. To wit: “Couple poor profit potential with fleeing deposits, and the banks’ ability or profit motivation to lend is minimal.” Not surprisingly, bank credit shrank last quarter by the greatest amount since at least 1975. It will likely continue shrinking due to tightening lending standards and poor lending incentives. Couple that with reduced loan demand due to high-interest rates. As the Fed maintains its “higher for longer” stance, yield curves will stay inverted, and borrowing rates will remain relatively high. Further, attractive interest rates in money market funds or Treasury securities will further drain deposits from the banking system, making banks even less likely to extend credit. Consequently, given the link between credit and GDP, a negative GDP in the fourth quarter would follow historical precedent.

What To Watch Today

Earnings

- No notable earnings reports today

Economy

Market Trading Update

The market traded slightly sloppily yesterday ahead of today’s inflation report but finished in the green. The 20-DMA continues to act as good support, and “dip buyers” continue to show up at minor support levels. The market is not overbought, and the MACD sell signal is still intact, suggesting the upside may be a bit limited near term. There is some rotation in the market, with sectors other than technology finally leading the way higher. The broader breadth of the rally is encouraging, but we still need a small correction to provide a better entry point. Earnings season might be the catalyst for such an opportunity.

DeCarley Thinks Bonds Are Attractive

In 5-Year Real Rates are Soaring, commentary from last week, we discussed the attractiveness of bonds on a real yield basis. The piece follows many commentaries, weekly newsletters, and longer-form blog posts we have written, touting the value of holding bonds at current yields. Instead of reiterating our bullish opinion, we thought it might be helpful to hear the views of DeCarley Trading. Their recent DeCarley Perspective lays out four reasons they think bonds are attractive. The commentary and charts below are from their linked report.

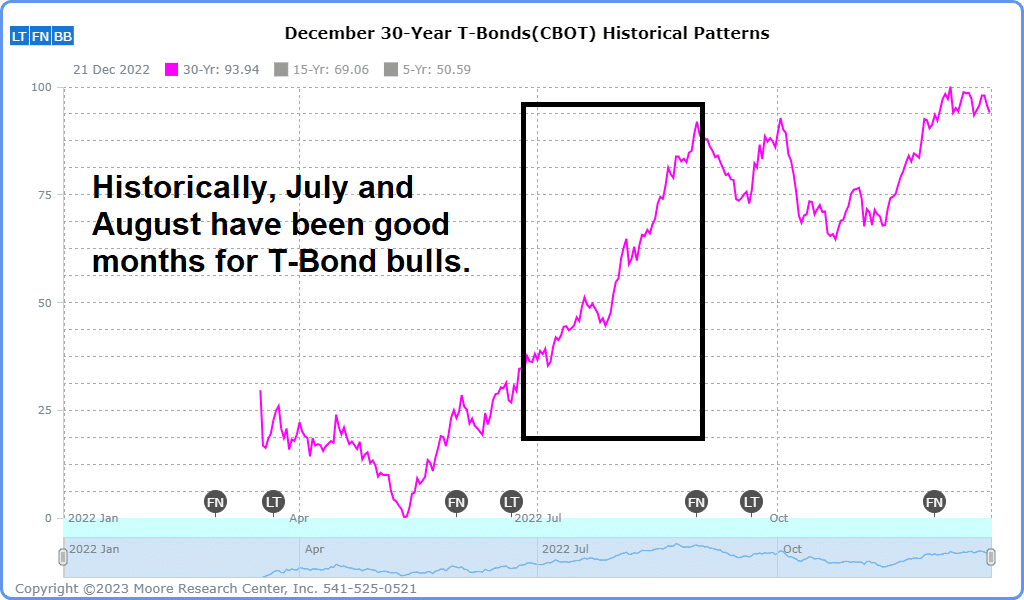

Seasonality

The Treasury market often relentlessly presses higher in July and August regardless of fundamentals. Thus far, the seasonal strength has been non-existent, but there are plenty of reasons for that to change.

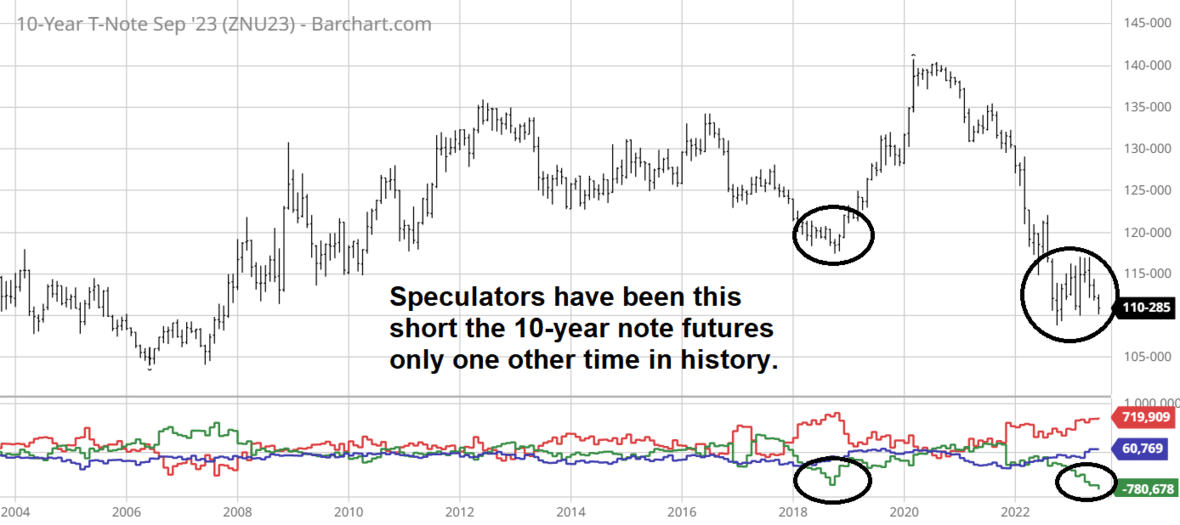

Futures Positioning

We are only aware of one other instance in which speculators in the futures markets were as aggressively short the 10-year note futures as they are today. In fact, according to the latest COT Report (Commitments of Traders) issued by the CFTC (Commodity Futures Trading Commission), large speculators are holding the largest net short position in history.

U.S. Dollar Weakness

A decline and weekly close below 100.00 would seal the deal for a weaker dollar. This would act as a tailwind for most assets, particularly Treasuries.

Inflation

The idea of runaway inflation ignited the original bond massacre of 2022. A year later, we know that inflation was peaking at precisely the time the markets were the most convinced the inflation cat was out of the bag and couldn’t be tamed. Inflation at 4% to 5% is still high compared to recent history, but in a world without aggressively loose monetary policy, 2% to 4% was considered acceptable. Perhaps we are simply falling back into a pre-Financial Crisis world of moderate inflation. With this in mind, it is fair to assume Treasuries are probably underpriced.

Fed QT Continues

The first chart below is a reminder that the Fed continues to do QT and is reducing its balance sheet. The spike in Fed’s balance sheet in March was due to its bank funding programs designed to support regional banks. As shown, the bank bailout-related liquidity bump has been completely undone. Barring further banking stress, we should see Fed assets decline by approximately $95 billion a month. The second graph separates securities from Fed lending programs to highlight the Fed has stuck with its QT program since early 2022.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.