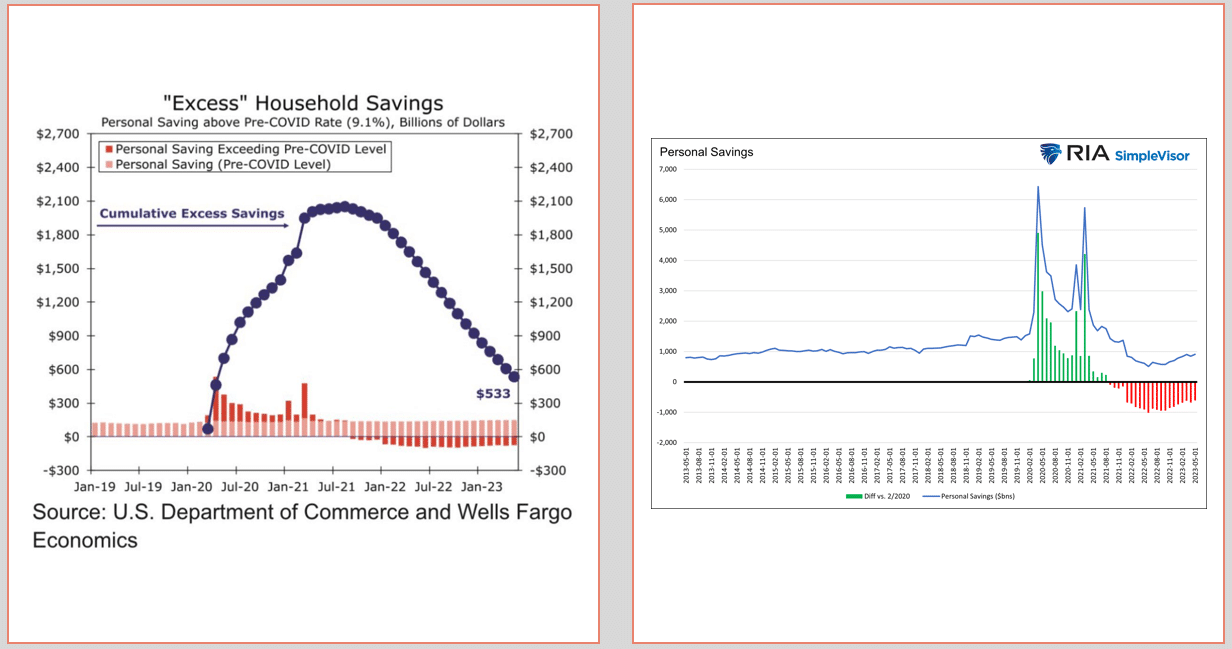

Since 2020, individuals and corporations have been provided significant funds from the government to combat the pandemic-related economic shutdown. Initially, as shown below, much of the money was saved. As the economy reopened, the excess of household savings was slowly spent. High-interest rates are not slowing the economy in part because consumers are spending down these excess household savings. The question is then how much money from prior stimulus remains as household savings and will continue to produce above-average spending. The answer is not simple. The graph on the right shows that the amount households save monthly is now less than before the pandemic. Yet, the Wells Fargo graph on the left shows a $533 billion excess of household savings.

The graph on the left highlights there is still excess savings if you net out the monthly data since 2020. The green bars on the graph to the right sum to more than the red. However, such fails to consider who is saving and who is spending. Wealthier citizens are not heavily reliant on savings. They likely pocketed the stimulus, which remains as household savings. Conversely, lower and middle-income citizens have little excess savings. As such, lower-income earners are the marginal consumers. Accordingly, their consumption habits tend to sway economic activity. The remaining excess savings that can boost the economy are now negligible. And, much of those savings are in the hands of higher income earners not as likely to spend it. As such, the benefits of yesteryear’s stimulus are likely on their last legs.

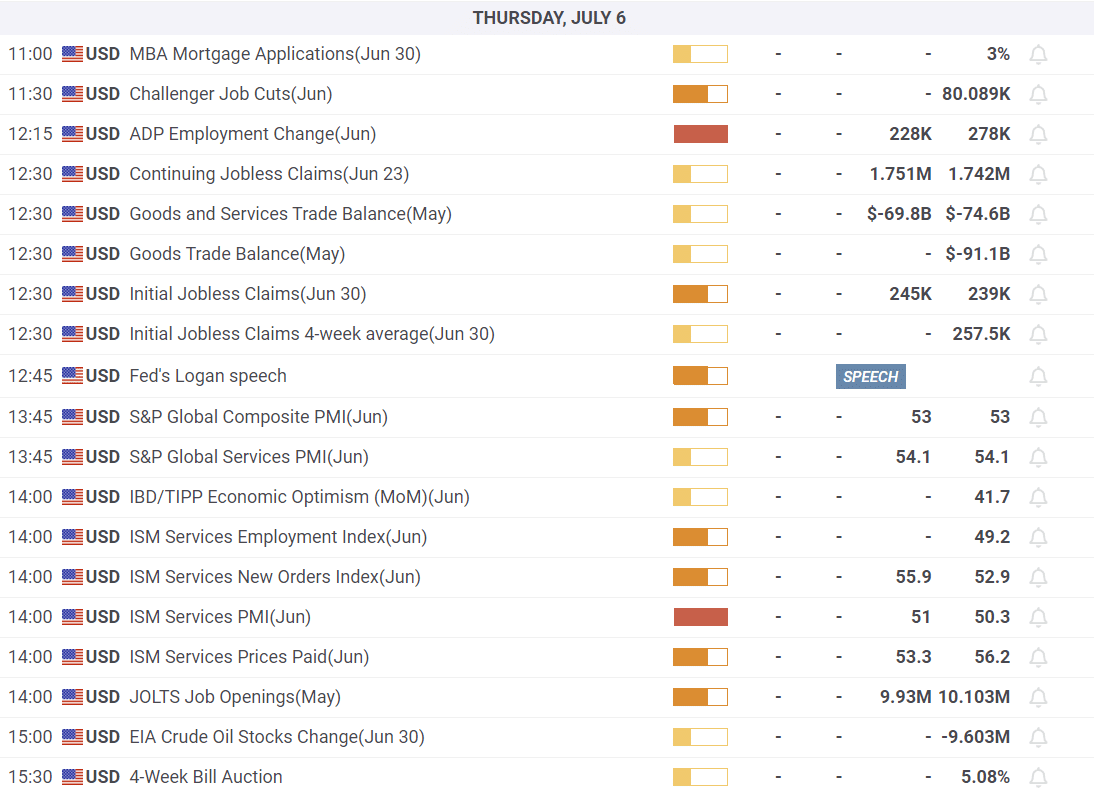

What To Watch Today

Earnings

Economy

Market Trading Update

The market struggled a bit yesterday to kick off the first full day of trading for the second half. Following the end of the quarter rebalancing, the sluggish start was unsurprising. Overall, it was a bit of a bifurcated move with some of the mega-caps leading the charge (namely GOOG, META, MSFT, and NVDA) along with Real Estate and Utilities. That latter was interesting given the selloff in bonds and rise in rates, most likely due to rebalancing heading into the remainder of the year.

There is not much to “read into” yesterday’s market action other than the recent rally from the 20-DMA has been sufficiently strong, and markets are back to more overbought short-term conditions. Upside may be somewhat limited until we get a bit more consolidation or corrective action in the markets. Volatility remains very depressed overall, which will likely rise coincident a 3-5% correction. However, for now, the MACD buy signal has been triggered, but at a high level, suggesting near-term upside may be limited.

Today’s Magnificent 7 was Yesterday’s Maleficent 7

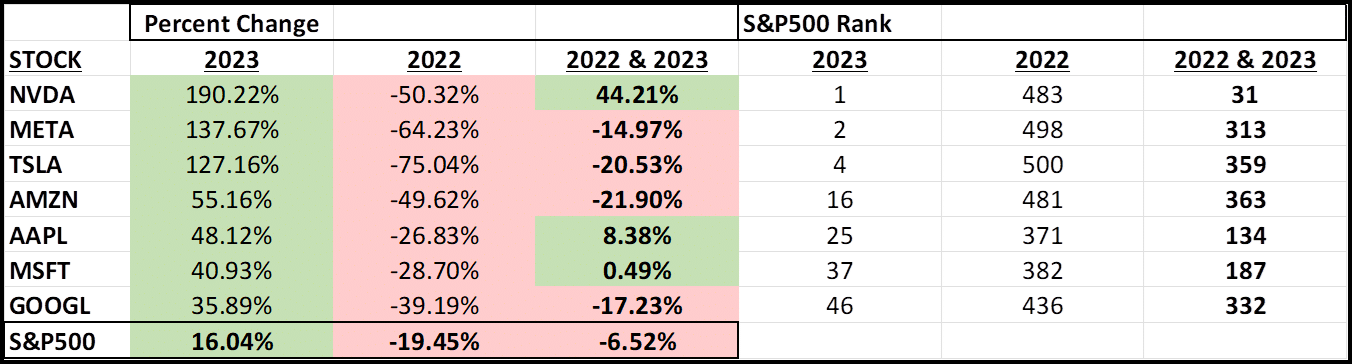

In a recent missive, Jeff Marcus of TPA Analytics points out that this year’s market leaders were last year’s duds. He notes that the problem of focusing on this year’s gains “and not the long term is that it ignores reality.” He writes:

Looking at the performance table below for 2022 and 2023, we can see that:

- The Magnificent 7 were among the worst performers in 2022.

- All of the Mag 7 stocks underperformed the S&P500 by a wide margin last year.

- NVDA, META, and TSLA, which rank 1,2, and 4 this year, ranked 483, 498, and 500 in 2022

- Only 3 of the Mag 7 stocks are positive over the 2022 and 2023 period

- The highest-ranked stock of the Magnificent 7 in the 2022 + 2023 period is NVDA at 31

- The average ranking of the Mag 7 stocks in the 2022 + 2023 period is 246 or right in the middle of the entire S&P500.

Jeff Marcus ends his piece with a bit of advice.

The largest cap stocks are the most liquid and, therefore the easiest to get in and out of. They are the first stocks investors pile into at the sign of a bull market and the first stocks they sell when there is trouble.

Jeff offers investment and portfolio advice through TPA Analytics, an add-on service to SimpleVisor. For more information, please click HERE.

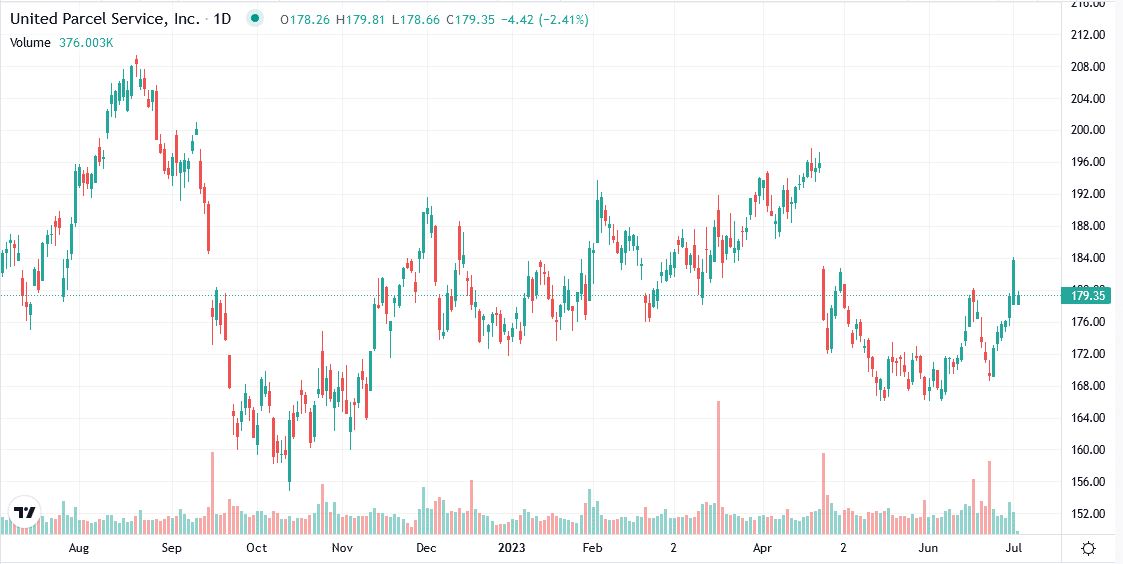

UPS Workers Set to Strike

Over 300,000 UPS workers are set to strike at month’s end if the union and company can not agree. Such a strike, especially if it is lasting, would threaten to upset the supply chain and could have temporary inflationary impacts. While the current labor agreement doesn’t end until August 1st, the situation is concerning. Per Bloomberg:

There is still time to reach a deal. The current labor contract — the largest private-sector union agreement in the US with 330,000 workers — expires at the end of July, but labor leaders have said they need a few weeks to educate their members and persuade them to ratify it. Union employees will not work beyond July 31 when the current contract expires, Teamsters spokeswoman Kara Deniz said. No more bargaining sessions are scheduled.

As shown below, UPS shareholders do not appear overly concerned by the growing potential for a strike.

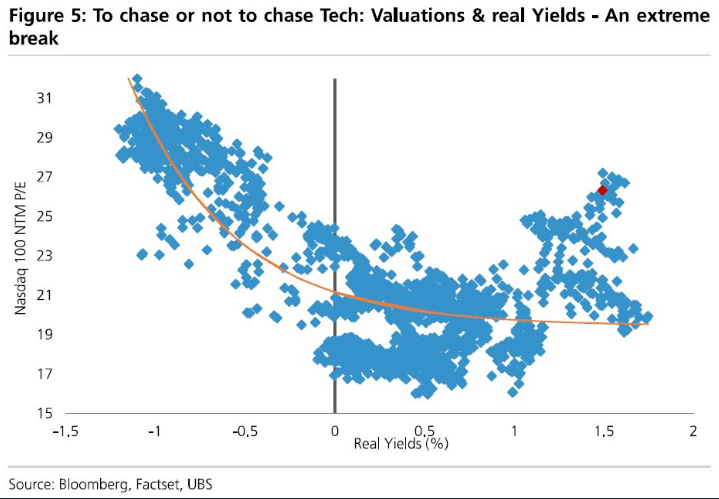

More on Hefty Valuations

In yesterday’s Commentary, we discussed how expensive the market is when looking at long-term valuations. The graph below from UBS provides further evidence. It plots the P/E of the Nasdaq 100 versus real yields. Currently, real yields are high, meaning that interest rates are above inflation rates, which tends to restrict economic growth. Often such a Fed policy stance is met with more conservative valuations.

The red dot shows that the current valuation is akin to real yields 2.5% below current levels. Conversely, one could say the P/E is about 7 above the norm.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.