As the stock market hit all-time highs this past week, there remains an interesting disconnect from the more dour economic concerns of the average American. A recent survey by Axios, a left-leaning website that supports the current Administration, addressed this issue.

“Poll after poll shows that the country is bummed out by the economy. Voters blame Biden. Nearly four in 10 Americans rate their financial situation as poor, according to a new Axios Vibes survey by The Harris Poll. In the language of our new Vibes series — which taps into the depth of Americans’ feelings — those surveyed feel sad about jobs and the economy.”

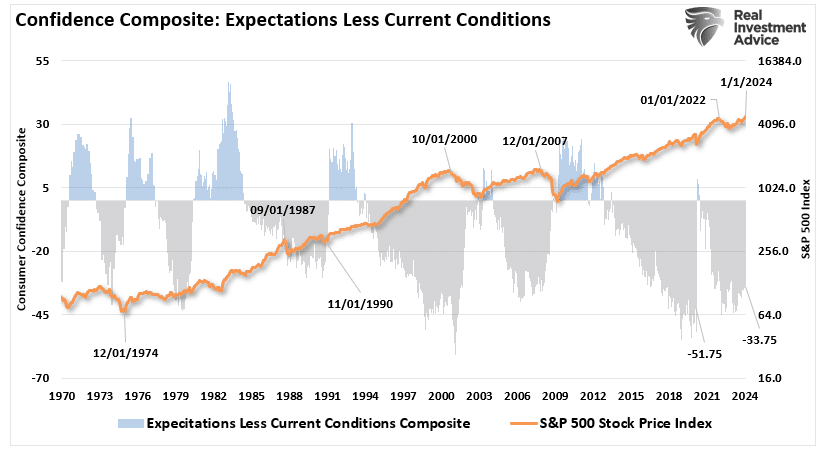

We compile a consumer sentiment composite index using the University of Michigan and Conference Board measures to confirm that assessment. Interestingly, while the stock market is hitting all-time highs, the gap between economic expectations and current conditions remains profoundly negative.

That gap should be unsurprising given the increases in borrowing costs directly impacting the average American. As shown, both the headline composite sentiment index and expectations are far off their highs as the Federal Reserve aggressively hiked borrowing costs.

However, the upside is that if the market can continue to register further all-time highs, which we will discuss why in a moment, such should translate into increased consumer confidence. Such is because even though the average household has very little money invested in the financial markets, the drumbeat of all-time highs from the media reduces economic concerns. Improvements in consumer confidence lead to increases in consumer spending, which translates into economic growth.

However, given that higher rates remain and consumers have drained most of their savings, there is likely only a limited impact on further improvements in confidence. While stocks are currently registering all-time highs, much of that gain is based on the assumption that the Federal Reserve will cut rates and reintroduce monetary liquidity.

Front-Running The Fed

The last paragraph is critical. We previously discussed how the Federal Reserve used “Pavlov’s experiment” to train investors over the last decade. To wit:

“Classical conditioning (also known as Pavlovian or respondent conditioning) refers to a learning procedure in which a potent stimulus (e.g., food) is paired with a previously neutral stimulus (e.g., a bell). Pavlov discovered that when the neutral stimulus was introduced, the dogs would begin to salivate in anticipation of the potent stimulus, even though it was not currently present. This learning process results from the psychological “pairing” of the stimuli.”

In 2010, then Fed Chairman Ben Bernanke introduced the “neutral stimulus” to the financial markets by adding a “third mandate” to the Fed’s responsibilities – the creation of the “wealth effect.”

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose, and long-term interest rates fell when investors began to anticipate this additional action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.” – Ben Bernanke, Washington Post Op-Ed, November, 2010.

Importantly, for conditioning to work, the “neutral stimulus,” when introduced, must be followed by the “potent stimulus” for the “pairing” to be completed. For investors, as each round of “Quantitative Easing” was introduced, the “neutral stimulus,” the stock market rose, the “potent stimulus.”

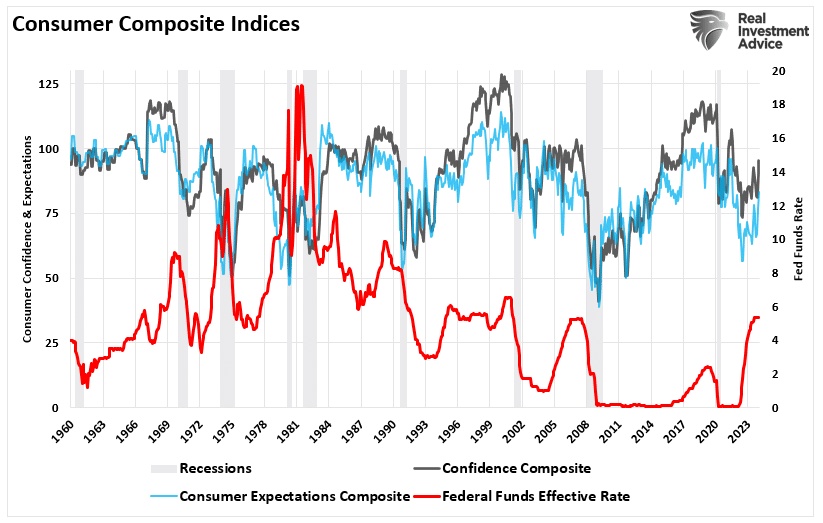

That analysis also corresponds to the Fed cutting rates as well. The chart below compares the Fed rate hiking cycle and its balance sheet contraction and expansion to the S&P 500 index. Since 2008, the Federal Reserve, through its messaging, has trained investors to respond to increased liquidity actions. Previously, markets tended to correct during periods of monetary tightening, as should be expected. However, this time, investors are front-running the Fed to get ahead of the reversal in monetary tightening.

While there has been previous debate on the impact of the Fed’s balance sheet changes on the markets, there is a very high correlation between the two, suggesting it is more than a coincidence. The correlation explains the Federal Reserve’s control over the financial markets.

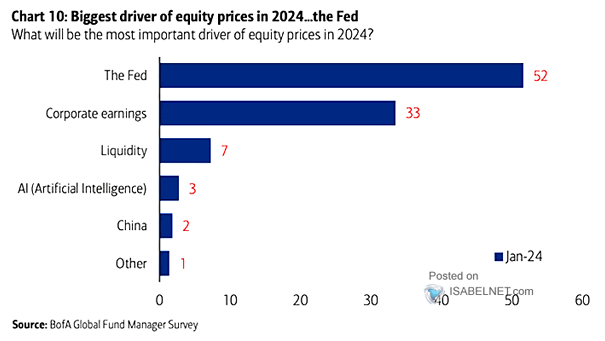

The influence of the Federal Reserve on the markets is evident in a recent BofA survey of professional managers on the “biggest driver of equity prices in 2024.” While fundamentals and corporate earnings should have been the top answer, 52 percent said “The Fed.” However, since “Liquidity” is controlled by the Fed, it was 59%.

Such makes it clear how the markets can obtain all-time highs despite the underlying view of the average American who has very little or no participation in it.

It’s A Narrow Market

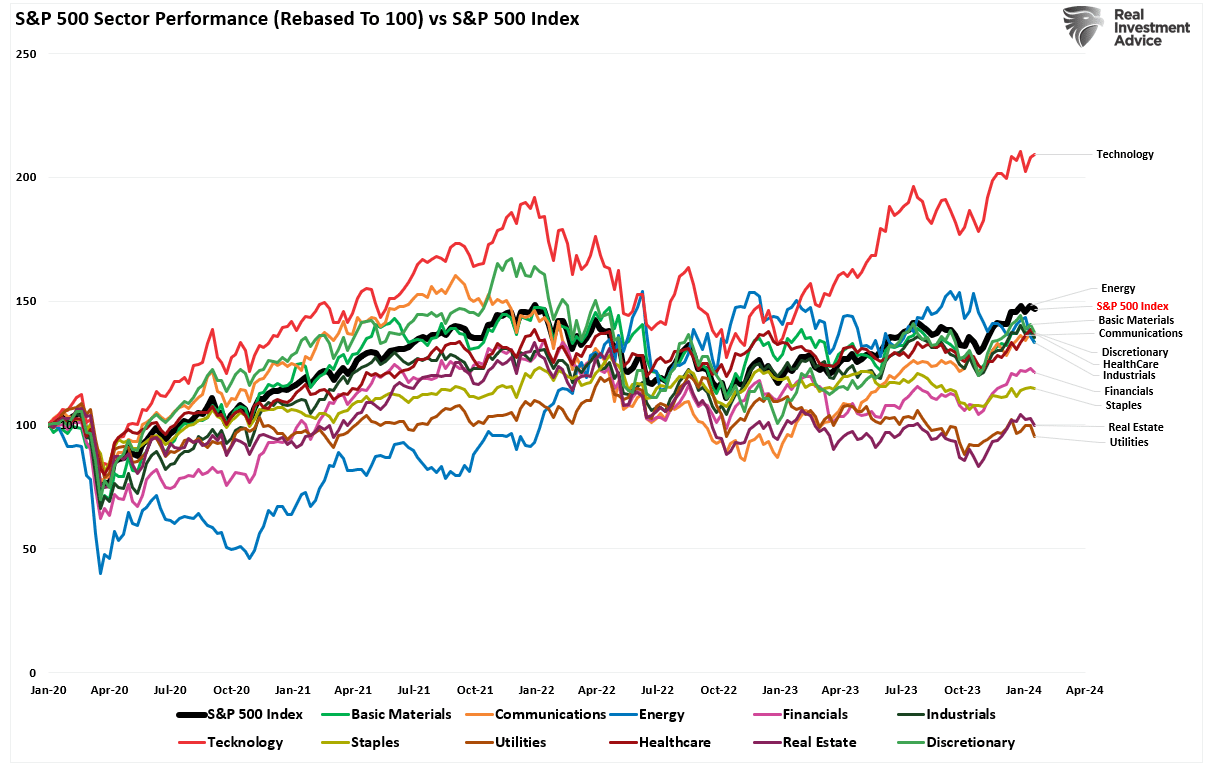

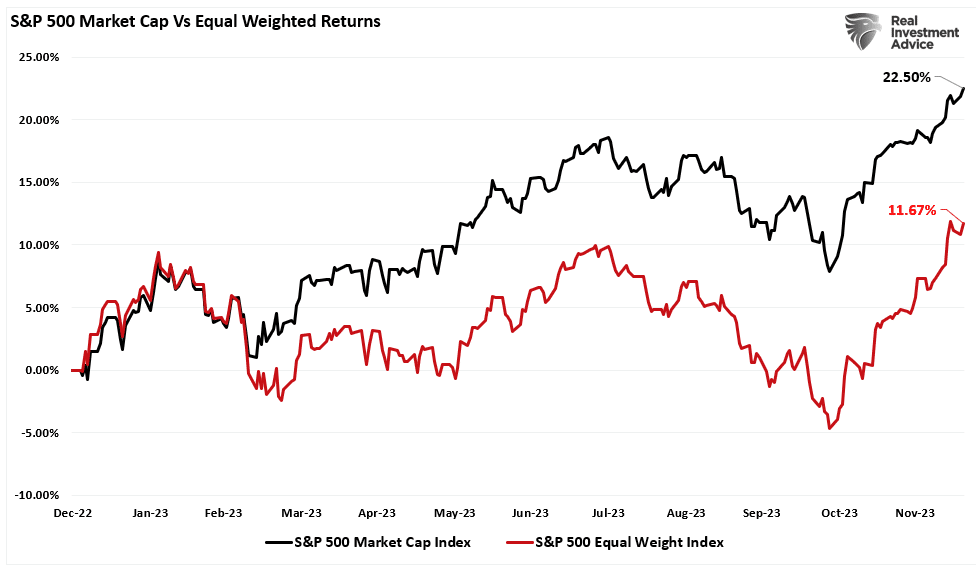

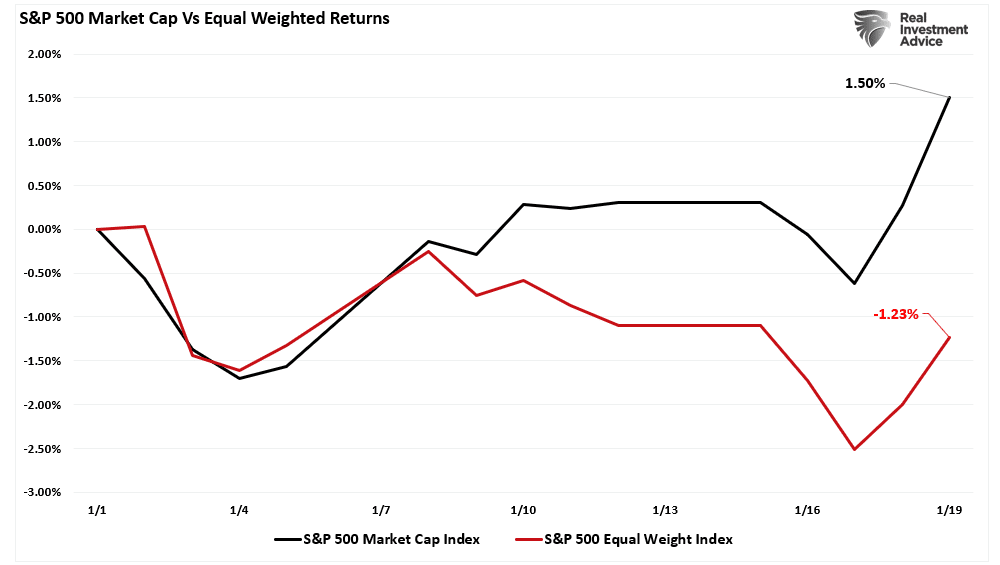

Another issue worth delving into with the market breaking out to all-time highs is the narrow participation in that rally. The chart below shows each market sector of the S&P 500 rebased to 100 as of January 2021. I have compared each to the S&P 500 itself. While the overall market is indeed reaching new all-time highs, it is the function of just one sector – Technology.

While the Technology sector can grow earnings in a slower economic environment, market liquidity has chased just a handful of stocks over the last year. Through the end of 2023, the S&P 500 market-capitalization weighted index doubled the return of the equal-weighted index. The reason is that the top-10 stocks in the index absorb more than 30% of all flows into passive indexes.

In 2024, that deviation continues as the chase for “artificial intelligence” dominates media headlines.

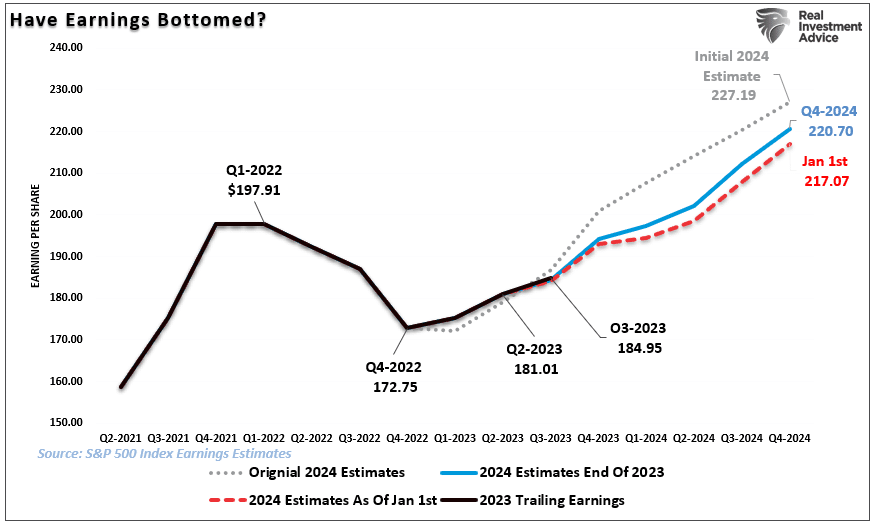

Given that Mega-capitalization stocks are a place of safety where major asset managers can place large amounts of capital, and the bulk of expected earnings growth will come from those companies, it is not surprising we are seeing the divergence again. However, while such a deviation is unsustainable long-term, the recent breakout to all-time highs may continue as “F.O.M.O” outpaces fundamentals and valuations. Given that the 24% advance in 2023 was primarily a function of valuation expansion, current valuation multiples are at risk of disappointment if earnings fail to achieve rather lofty expectations.

Earnings Are Key

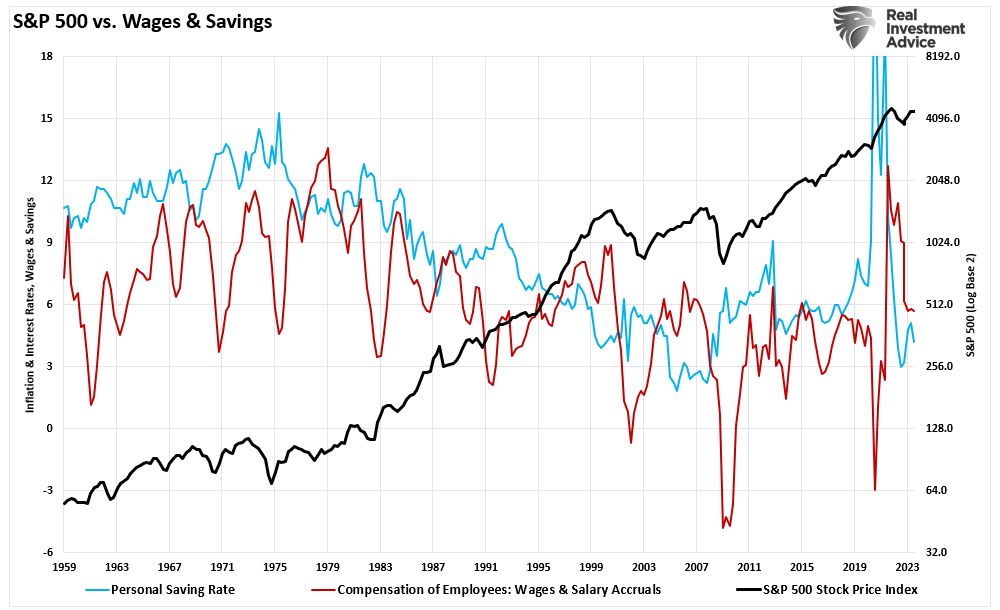

Economic activity generates the revenues, and ultimately earnings, for corporations. Therefore, the consumer’s return of confidence in the economy is the key to sustaining the all-time highs in the market. The overriding problem for the average American is the decline in savings and wages and increases in the cost of debt.

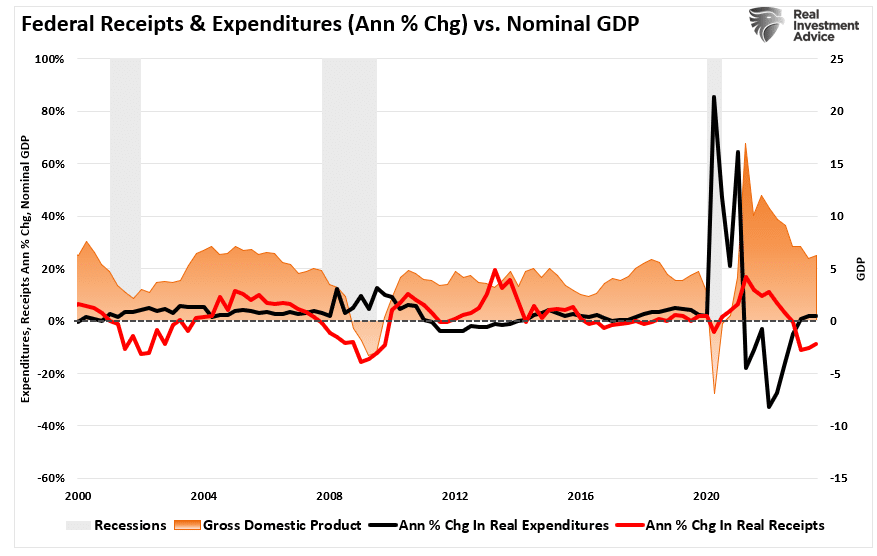

What most economists and mainstream analysts miss is that while the economy remains robust, it remains a function of massive increases in deficit spending. The problem, and why Americans are so sour on the economy, is that while deficit spending keeps the economy from recession, it is temporary and does not increase the wealth or prosperity of the average American.

The problem for the market is that as the monetary impulse from the 2020 stimulus campaign to the Inflation Reduction and CHIPs Act continues to support economic activity, the rest of the economy is slowing. Ultimately, such will show up in the reduction of rather lofty earnings expectations, which are already declining.

Lastly, given that most sectors are experiencing stagnating earnings growth because of slower economic activity, any risk arising that impacts the earnings of the handful of stocks driving the market could be significant. With valuations elevated, any disappointment, or worse, a potential recession, could lead to a considerable market repricing.

For now, the market’s breakout to all-time highs is bullish and will likely lead to further gains. However, the critical message is not to forget there is still substantial risk underlying the current economy and the market.

Narrow markets are fine until they aren’t.

The problem with that statement is that it is difficult to realize when something has changed. As is always the case with investing, market risks always occur “slowly, then all at once.”