Rate increase expectations for the Fed are starting to fall rapidly as recent evidence suggests inflationary pressures are starting to wane. On Friday, stocks jumped more than 2% during the day after the University of Michigan’s gauge of longer-term consumer inflation expectations settled back from an initially reported 14-year high. That drop in inflation expectations potentially reduces the urgency for faster rate increases. St. Louis Fed President Bullard, who is considered the biggest hawk among Fed officials, said worries over a US recession are overblown.

Traders are starting to price out any Fed action on rate increases beyond the December meeting. The scaling back of the additional rate increases was supportive but it was the expectation of rate cuts by February 2023 that sent stocks rallying. Of course, there is still a lot of work for stocks in the intermediate term, particularly around what happens if an economic downturn takes hold.

What To Watch Today

Economy

- 8:30 a.m. ET: Durable Goods Orders, May preliminary (0.2% expected, 0.5% prior)

- 8:30 a.m. ET: Durables Excluding Transportation, May preliminary (0.3% expected, 0.4% prior)

- 8:30 a.m. ET: Non-defense Capital Goods Orders Excluding Aircraft, May preliminary (0.1% expected, 0.4% prior)

- 8:30 a.m. ET: Non-defense Capital Goods Shipments Excluding Aircraft, May preliminary (0.2% expected, 0.8% prior)

- 10:00 a.m. ET: Pending Home Sales, month-over-month, May (-3.9% expected, -3.9% prior)

- 10:00 a.m. ET: Pending Home Sales NSA, year-over-year, April (-11.5% prior)

- 10:00 a.m. ET: Dallas Fed Manufacturing Activity, June (-6.5 expected, -7.3 prior)

Earnings

Pre-market

- No notable companies are set to report.

Post-market

- Nike (NKE) to report adjusted earnings of $0.83 on revenue of $12.14 billion

- Jefferies Financial (JEF) to report adjusted earnings of $0.51 on revenue of $1.26 billion

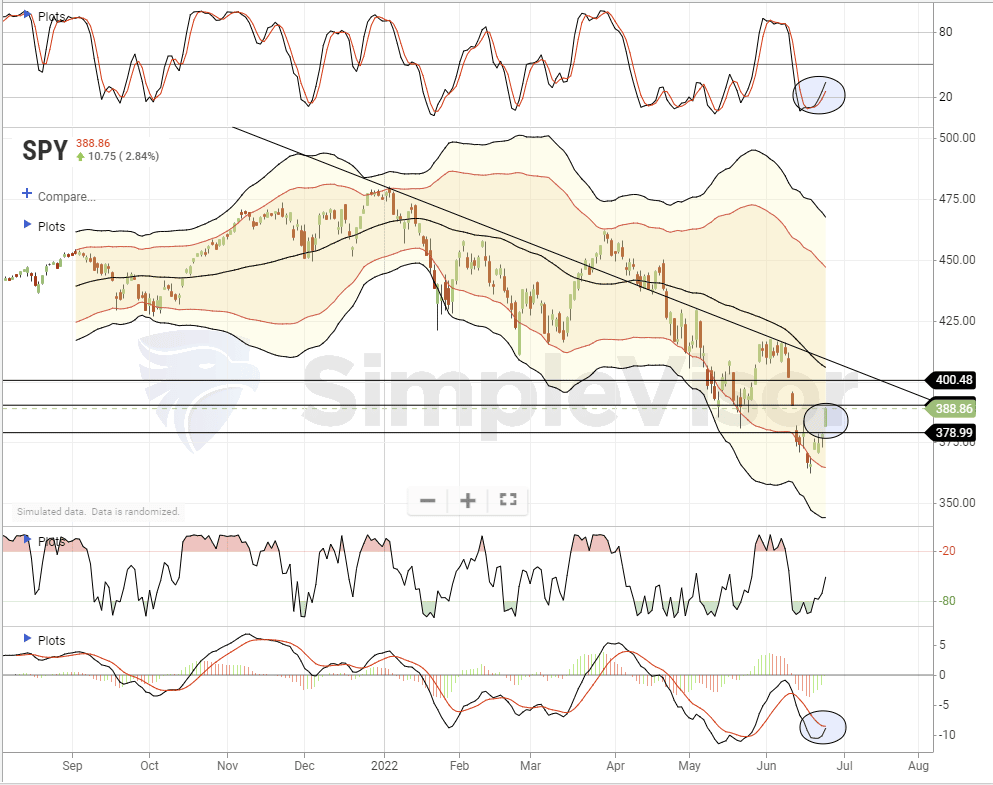

Market Trading Update – Stocks Rock

On Friday, stocks surged after the latest UofM Sentiment Survey saw a drop in inflation expectations. Such suggests the Fed will have to be less aggressive on rate increases which stoked the bulls. As noted on Friday, the rally cleared the first resistance level and began to approach the second. Those “gaps” during the waterfall selloff previously are going to provide resistance to the rally. However, we are very close to triggering a MACD buy signal which could provide the support needed for a retracement to the top of the downtrend channel. Our current target for the rally is 4000 where we can rebalance exposures and add back our short S&P 500 index position if needed.

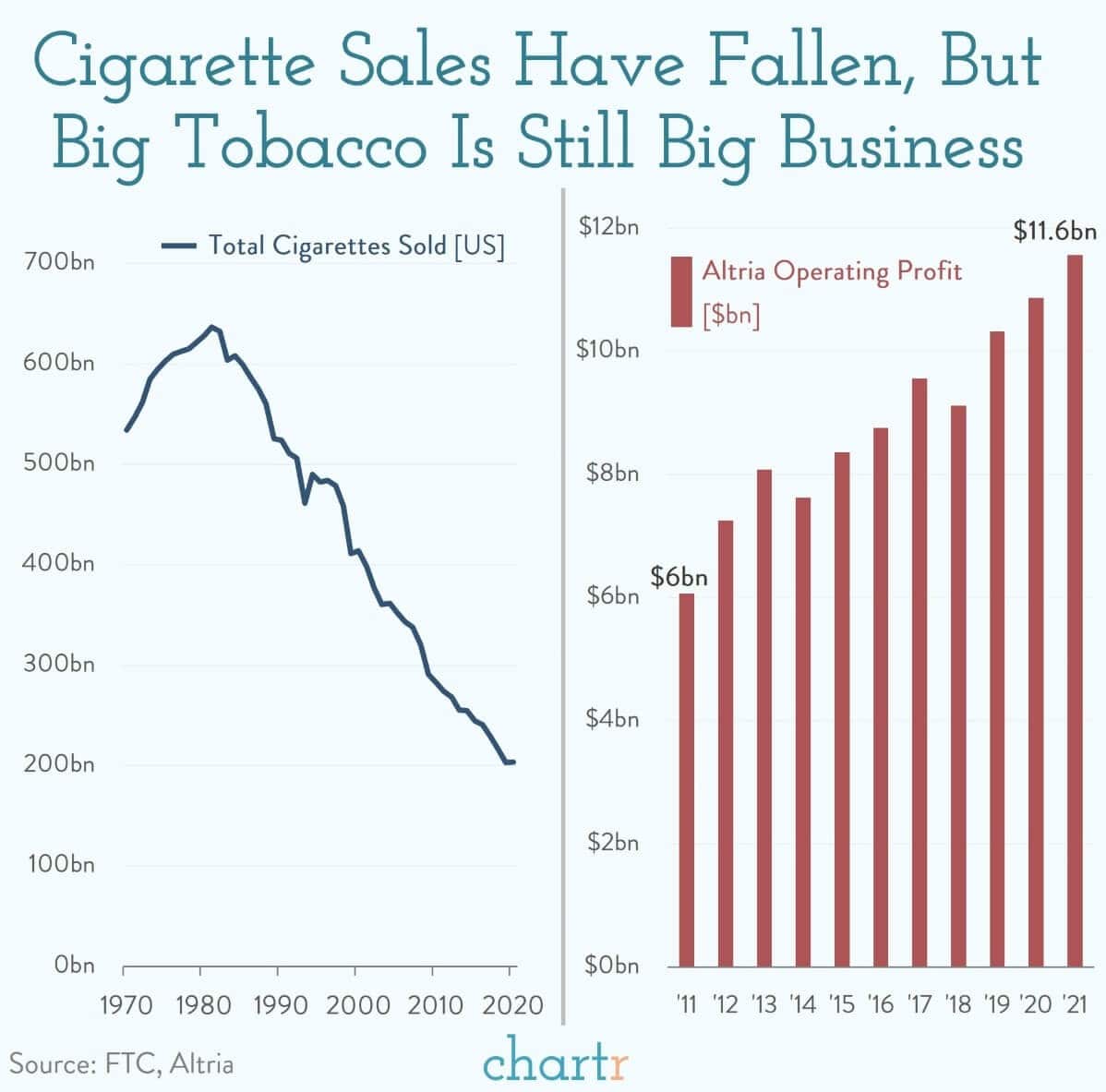

No One Smokes Anymore, But It’s Still Big Business

“After 40+ years of declining cigarette sales and graphic public health warnings about the damage that smoking causes, it might be easy to think of big tobacco as a frail industry on its deathbed — it’s anything but. In fact, even in the wake of falling sales, Altria has eked out record earnings over the last decade. The $12-13bn that it has presumably lost on the Juul deal is an enormous sum… but it’s one that Altria can — quite easily — afford. It’s racked up operating income of more than $10bn for the last 3 years in a row. Big tobacco is still just that… big.” – Chartr

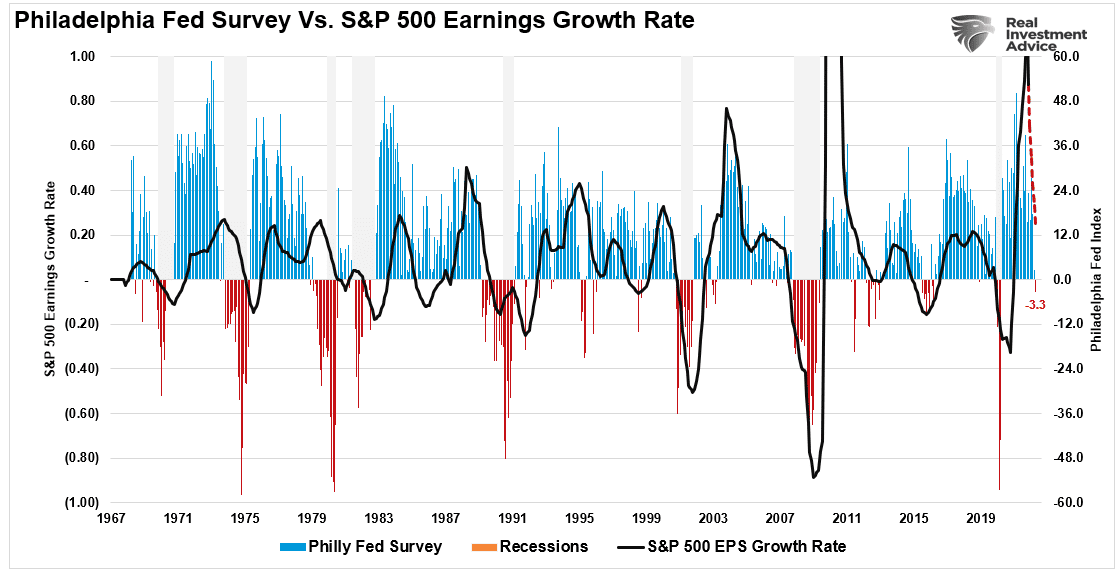

The Philly Fed Survey Suggests An Earnings Recession Is Coming

Between Fed rate increases, rising inflation, and the reversal of liquidity, it is not surprising to see economic indicators coming in weaker than many economists expected. We have written previously about what would happen when the “Sugar Rush” subsided.

That outcome has arrived and was recently noted by the collapse in the Philadelphia Federal Reserve survey. Importantly, earnings expectations remain elevated and have yet to get reduced to compensate for much slower economic growth and a potential recession. Those downgrades are coming which will require further adjustments to stock prices to fully accommodate.

The Week Ahead

This week kicks off this morning with durable goods orders, pending home sales, and The Dallas Fed Manufacturing index. Expectations are for durable goods orders to decline 0.3% MoM in May. Tomorrow we’ll get the Conference Board’s Consumer Confidence index and some regional Fed data. Wednesday morning we’ll hear from Chair Powell again before getting a look at May’s PCE data on Thursday. Expectations are for the core PCE price index to increase 4.7% YoY and 0.4% MoM in May. We’ll cap off the week Friday morning with the ISM manufacturing index for June. The consensus is for a slight decrease to 55, down from 56.1 in May.

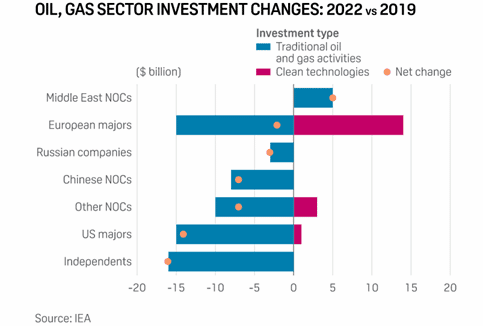

Energy Prices Could Stay Elevated Longer Than You Think

Underinvestment has plagued the oil & gas industry since the 2015 price downturn and subsequent rise in green agendas. Now Russian sanctions and low inventories are exacerbating the situation but things aren’t showing signs of improvement. Per Bloomberg:

“Investment is set to be below the $441 billion spent in 2019 for a third straight year, endangering future energy security, according to the IEF. The consultant said in a December report with IHS Markit, a research unit of S&P Global Platts, that spending needs to be sustained at about $525 billion a year through 2030 to meet global demand for crude and products.”

A recession would likely soften demand enough to cause a temporary pullback in prices. However, industry underinvestment raises the likelihood that demand quickly overwhelms supply after global central banks inevitably restart QE. The spending landscape isn’t likely to improve either, since the Biden administration had a clear bias against the industry prior to skyrocketing prices. You’re not fooling anyone, Joe. Underinvestment will likely continue, and we could see elevated energy prices after a slowdown. Even when most other supply chains have recovered.

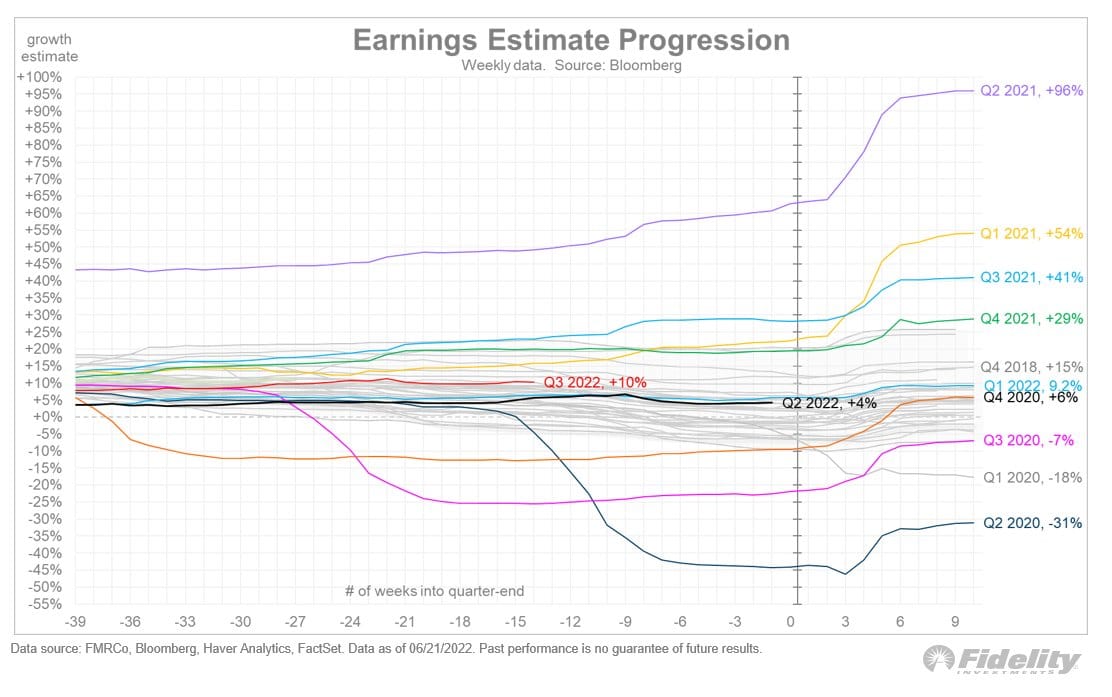

The Looming Risk: Estimate Revisions

Forward valuations look enticing, but that’s only because analysts haven’t revised their estimates lower despite worsening economic conditions. As shown below, analysts still expect earnings growth to accelerate in the third quarter. Meanwhile, Chris Williamson noted in last Thursday’s Flash PMI report that a contraction could begin as soon as Q3. Investors will be in store for more pain when analysts revise estimates lower, as valuations won’t look so rosy anymore.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read