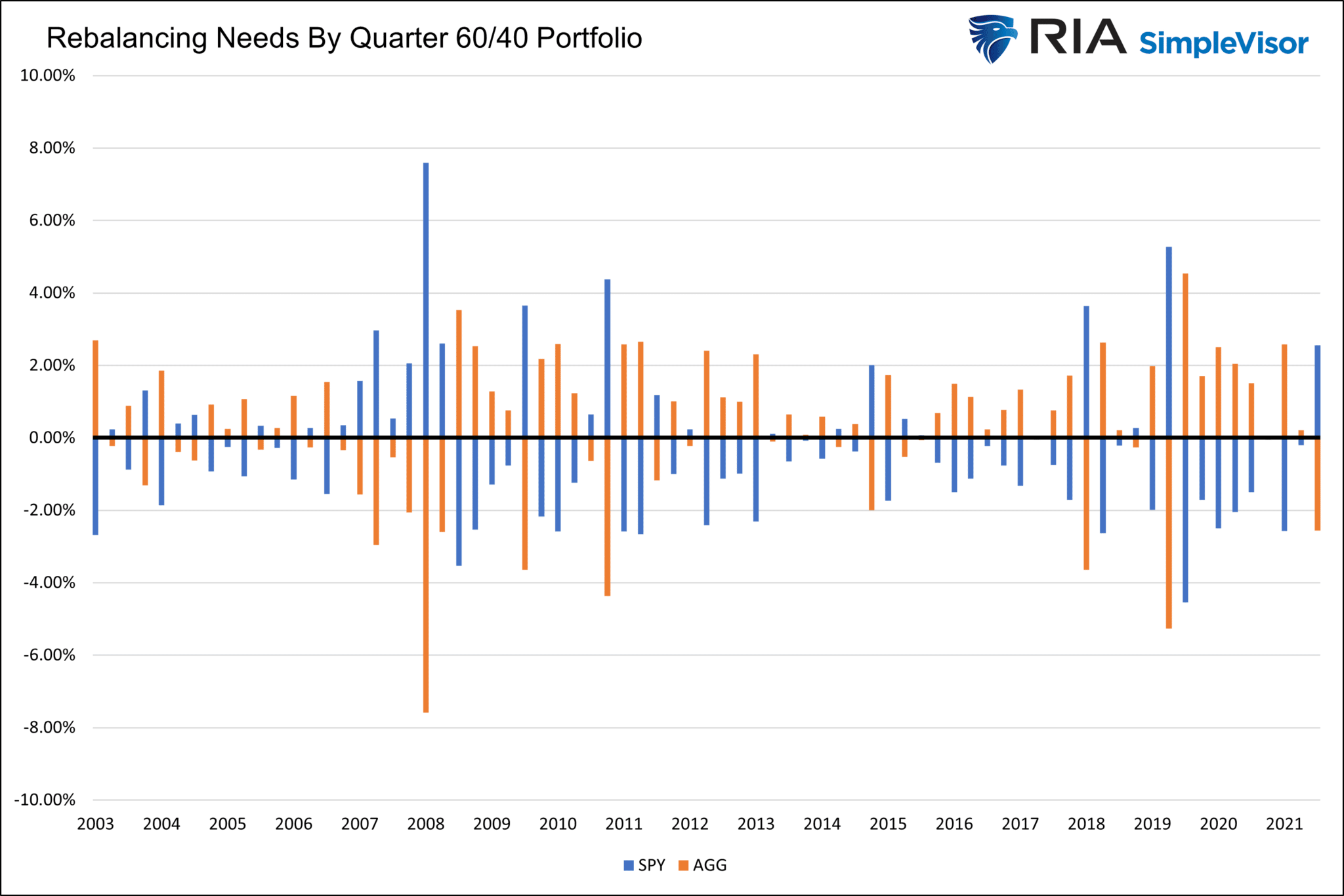

At the end of each quarter, markets often experience heightened volatility as institutional money managers adjust their holdings. For example, window dressing occurs when portfolio managers buy and sell certain securities based on what has been trading well and not so well. When their clients see their quarterly holdings, window dressing makes them think they are/were positioned properly with recent market trends.

Rebalancing trades can be another market mover at quarter ends. Rebalancing entails buying positions that became underweighted due to price declines and selling those which became overweighted due to gains. In another section below, we quantify what this means for markets this quarter-end and at previous quarter ends. The bottom line is that window dressing, rebalancing, and risk management can create volatility at quarter ends.

What To Watch Today

Economy

- 8:30 a.m. ET: Personal Income, month-over-month, May (0.5% expected, 0.4% prior)

- 8:30 a.m. ET: Personal Spending, month-over-month, May (0.4% expected, 0.9% prior)

- 8:30 a.m. ET: Real Personal Spending, month-over-month, May (-0.3% expected, 0.7% prior)

- 8:30 a.m. ET: Initial Jobless Claims, week ended June 25 (229,000 expected, 229,000 prior)

- 8:30 a.m. ET: Continuing Claims, week ended June 18 (1.318 million expected, 1.315 million prior)

- 8:30 a.m. ET: PCE Deflator, month-over-month, May (0.7% expected, 0.2% prior)

- 8:30 a.m. ET: PCE Deflator, year-over-year, May (6.4% expected, 6.3% prior)

- 8:30 a.m. ET: PCE Core Deflator, month-over-month, May (0.4% expected, 0.3% prior)

- 8:30 a.m. ET: PCE Core Deflator, year-over-year, May (4.8% expected, 4.9% prior)

- 9:45 a.m. ET: MNI Chicago PMI, June (58 expected, 60.3 prior)

Earnings

Pre-market

- Constellation Brands (STZ) to report adjusted earnings of $2.50 on revenue of $2.17 billion

Post-market

- Micron Technology (MU) to report adjusted earnings of $2.44 on revenue of $8.64 billion

- Walgreens Boots (WBA) to report adjusted earnings of 94 cents on revenue of $32 billion

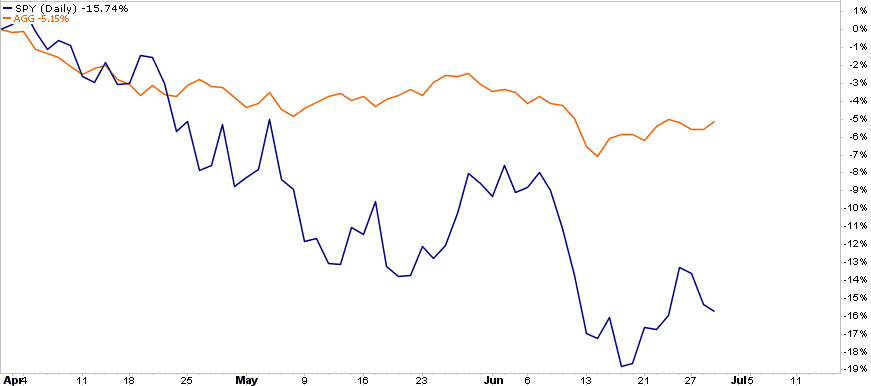

Market Trading Update – Holding Support

As we enter the last day of the quarter-end, the market has struggled this past week despite the need for managers to increase equity exposure. The market failed at the second resistance level yesterday but did hold support at 3800. We added a little exposure to portfolios given the recent MACD buy signal, but our stop remains very tight. If the market fails to rally today, we are likely going to retest recent lows next week. Overall, the market remains confined to a bearish downtrend channel that has contained any significant rallies since the beginning of the year.

Quarter-End Rebalancing Needs

To help appreciate this quarter end’s rebalancing needs first consider the performance of stocks and bonds over the last three months. What matters is not necessarily how much stocks and bonds moved, but how much they changed versus each other. For instance, if stocks and bonds rose by the same amount, the rebalancing need would be zero. Conversely, if stocks rose and bonds fell, rebalancers will sell stocks and buy bonds to return to their preferred stock-bond allocation.

Last quarter, the S&P fell by 15%, while the Bloomberg Aggregate Bond Index (AGG) fell by only 5.5%. As a result, investors wanting to rebalance their portfolios will likely have to buy stocks and sell bonds. The graph below shows by what percent of a portfolio a balance 60/40 stock/bond portfolio would have to adjust their holdings. As shown, the March quarter-end had minimal rebalancing needs as stocks and bonds had similar performance. This quarter, a hypothetical balanced manager must buy 2.56% of its portfolio value in stocks and sell 2.56% of bonds. That amount is almost twice the average since 2004. Keep in mind rebalancing activity often occurs over a week or more before the month-end. As such it may have happened already or we could catch a bid in stocks today if they all waited until the last day.

TikTok – Zero To $12 Billion

“TikTok is on track to reel in $12bn in advertising revenue this year, according to new reports from people familiar with the company’s financials.

When compared to the established big players in digital ads, namely Google and Facebook, that’s small potatoes — Google Search alone brought in almost $150bn last year, and Facebook did more than $110bn.

But when you compare where TikTok is on its journey, having been founded in just 2016, the company’s progress is remarkable. If those reports prove accurate, Tiktok will have broken the $10bn a year mark in just its sixth full year — a milestone that took Facebook more than a decade. YouTube took 14 years. Snapchat and Twitter? They’re both barely halfway to that milestone.

What’s more remarkable is that TikTok’s parent company, Bytedance, which owns a number of other social media and tech assets in China, is on an even steeper trajectory. Bytedance reportedly made $34bn last year, less than a decade since it was founded” – Chartr

Zombie Apocalypse

Per Bloomberg: “A near-record 128 members of Russell 3000, worth $281B have failed to turn a profit in any quarter for six straight years & almost tripled since 2017.”

Very low-interest rates allowed these companies to borrow and offset losses. That era may be coming to an end. And, with higher rates, the luck of some of these companies may be coming to an end.

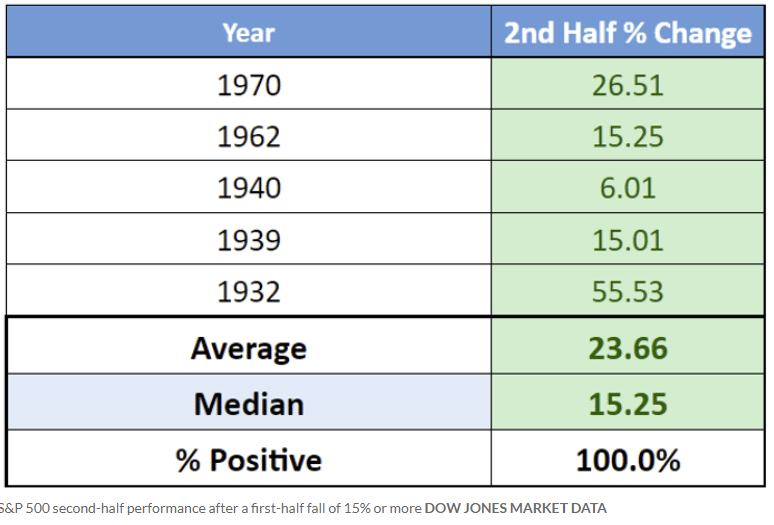

What Do Markets Historically Do Following The A Terrible 1st Half?

“The S&P 500 was down 19.8% year-to-date through Tuesday’s close, which would be its worst first half since 1970, according to Dow Jones Market Data. The large-cap benchmark is down 20.3% from its record finish on Jan. 3. The index earlier this month ended more than 20% below that early January record. Such confirms the pandemic bull market ended on Jan. 3, marking the start of a bear.

Data compiled by Dow Jones shows the S&P 500 bounced back after past first-half falls of 15% or more. The sample size, however, is small, with only five instances going back to 1932 (see table below).” – MarketWatch

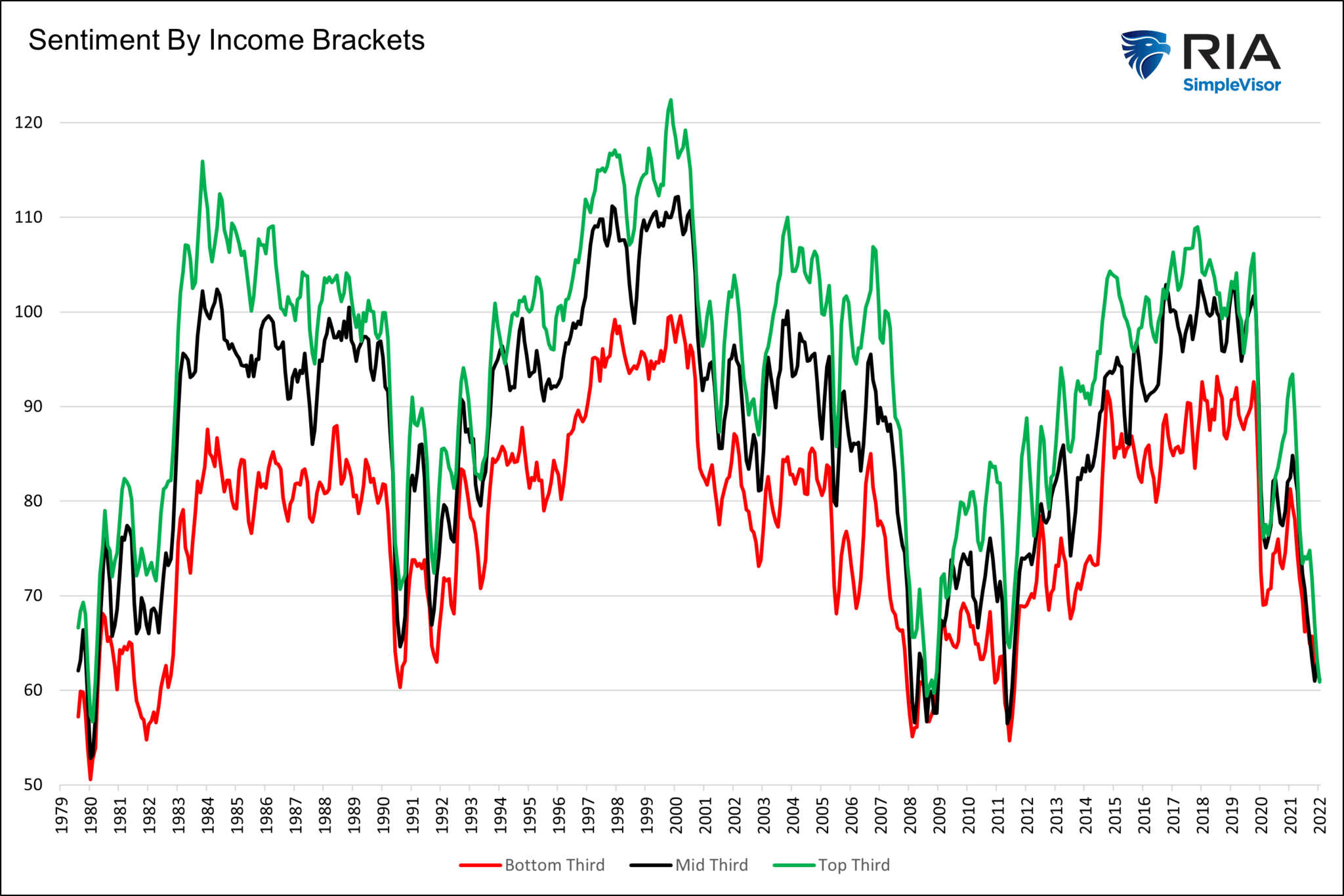

Inflation is Weighing on the Wealthy

High inflation rates often take a larger toll on the poor versus the wealthy. This is because they often spend a larger portion of their income than the wealthy. According to the University of Michigan, this round of inflation is causing more concern for the wealthy than the poor. The top 33% of wage earners, constituting over 50% of personal consumption, are registering a lower University of Michigan sentiment reading than the bottom 33%. The graph below shows that this is the first time such a concurrence has happened. On average, sentiment is 16% better for the top 33% of wage earners versus the bottom 33%.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read