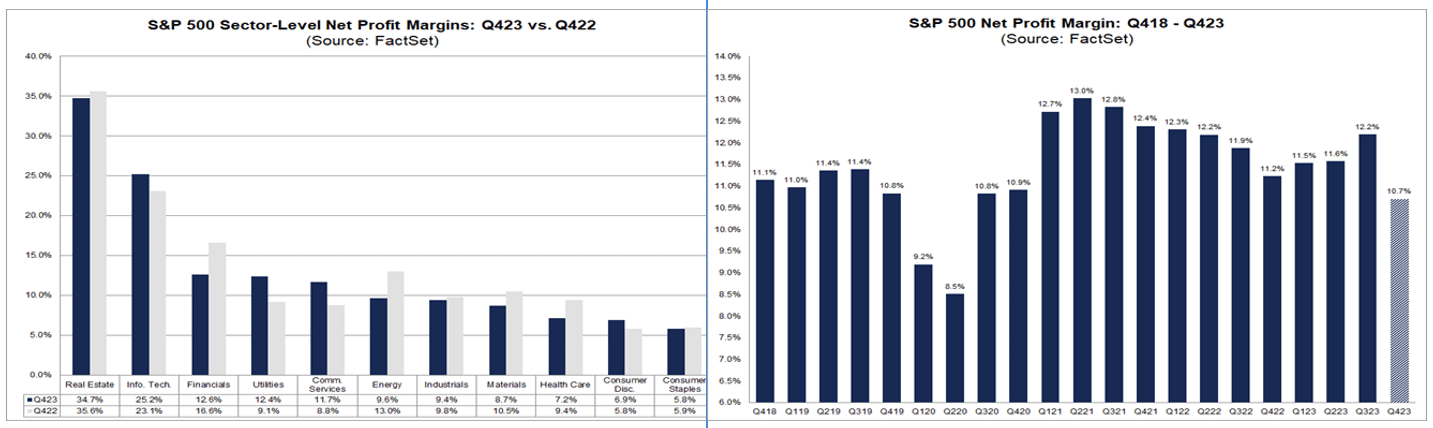

Since peaking in the first quarter of 2022, the net profit margin on the S&P 500 has generally trended lower. During the pandemic, many companies could increase prices more than their rising input costs and improve their profit margins. Strong demand due to pent-up savings and fiscal stimulus also helped. However, with inflation normalizing and stimulus checks largely spent, profit margins are subsiding. The graph on the right, courtesy of FactSet, shows that net profit margins for the fourth quarter are down to 10.7%, slightly below pre-pandemic levels.

The graph on the left shows the annual change in profit margins by sector. Four sectors (Technology, Utilities, Communications, and Consumer Discretionary) posted margin gains over the past year. Utilities posted the biggest gain, increasing from 9.1% to 12.4%. The other seven sectors saw declining margins, led by Financials (12.6% vs. 16.6%) and Energy (9.6% vs. 13.0%). If margins continue to decline, investors may want to reconsider the higher-than-normal valuations placed on the S&P 500. However, FactSet justifies higher valuations- “As of today, the estimated net profit margins for Q1 2024 and Q2 2024 are 11.7% and 12.1%, respectively.” If correct, margins would rise back to or above pre-pandemic levels. But, all bets are off if a recession occurs.

What To Watch Today

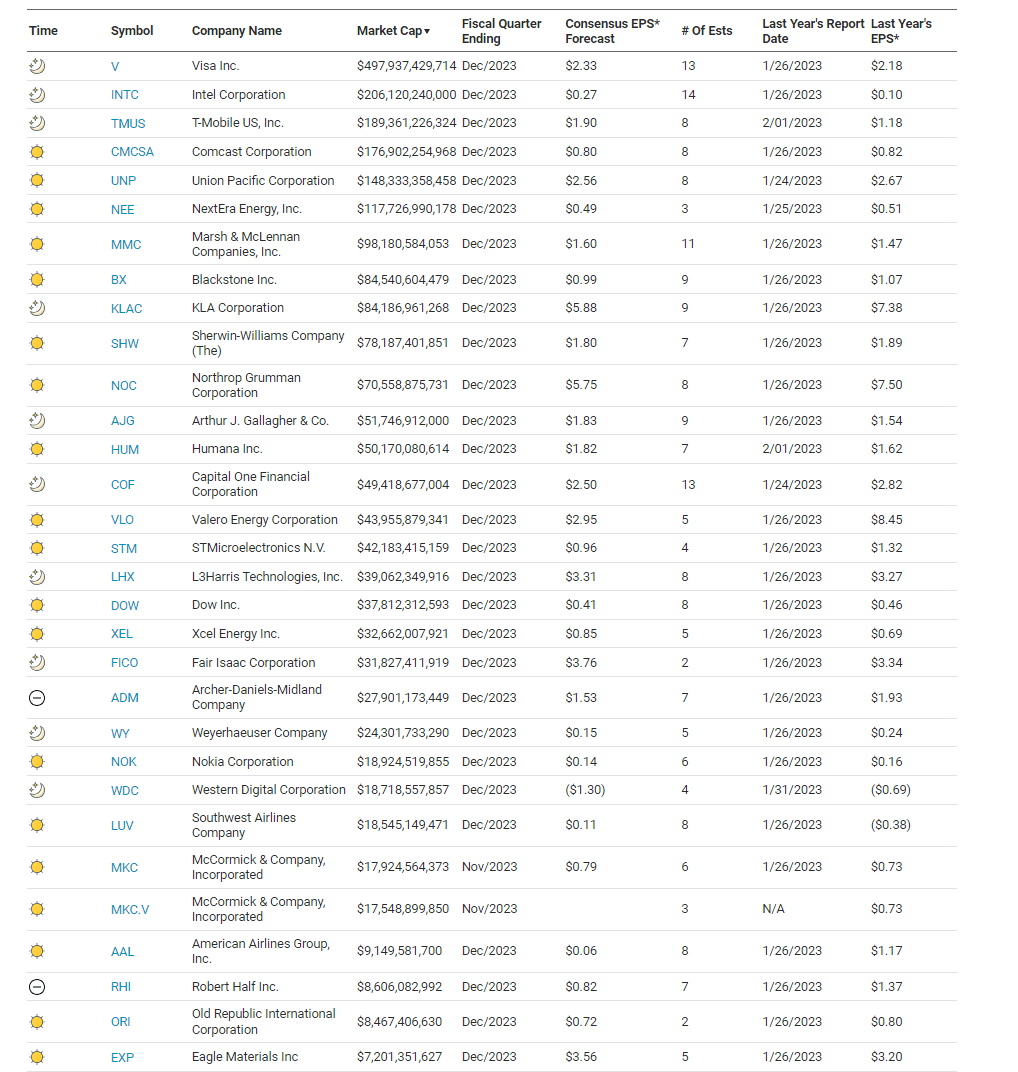

Earnings

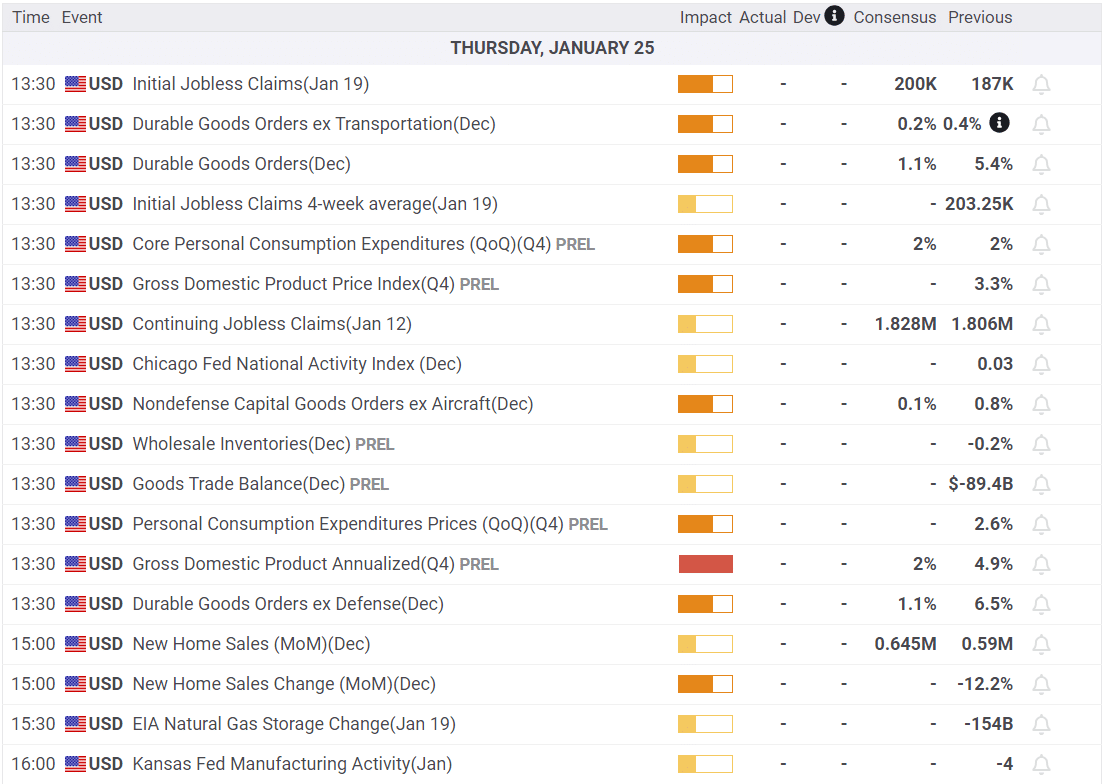

Economy

Investing Summit: LAST CHANCE – EVENT THIS SATURDAY

January 27th, we are hosting a live event featuring Greg Valliere to discuss investing in the 2024 presidential election. What will a new president mean for the markets, the risks, and where to invest through it all? Greg will be joined by Lance Roberts, Michael Lebowitz, and Adam Taggart for morning presentations covering everything you need to know for the New Year.

Register now, as there are only 150 seats. The session is a LIVE EVENT, and no recordings will be provided.

Market Trading Update

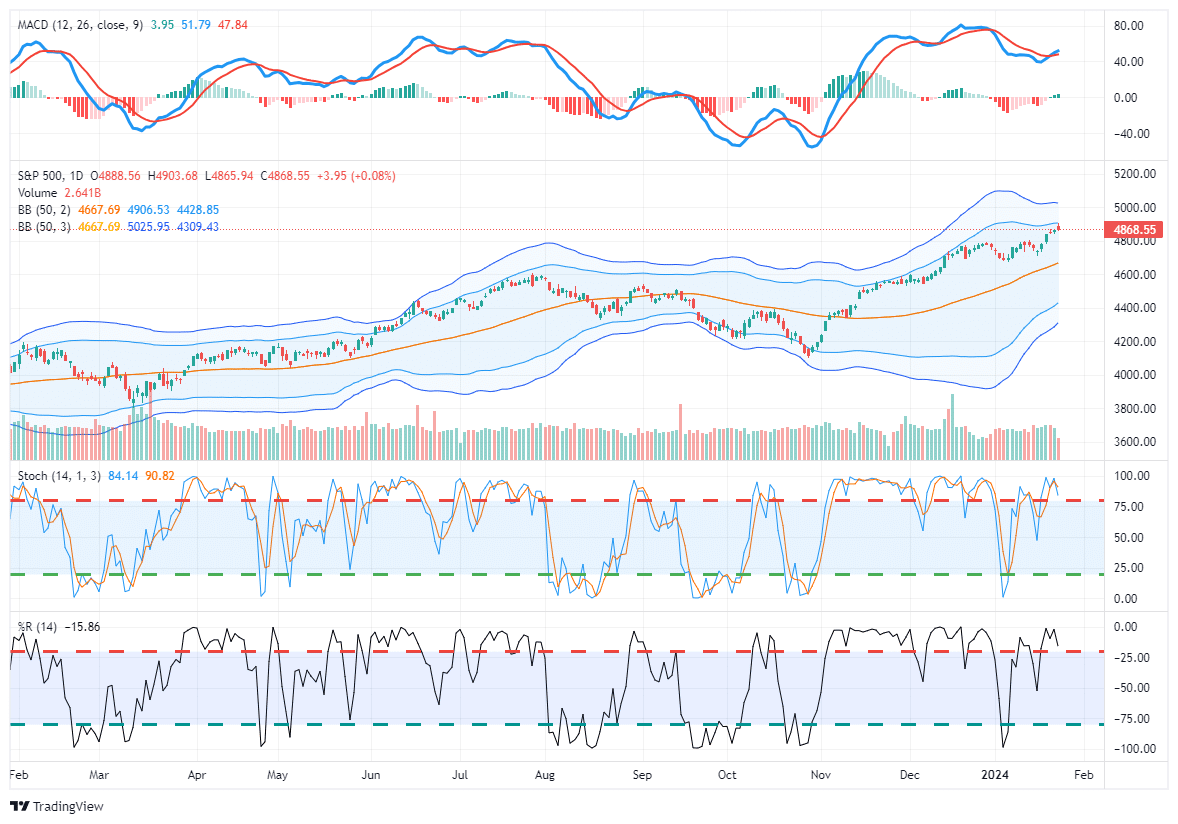

The market triggered a MACD “buy signal” from a fairly high level, which we suggested would limit upside action. Despite strong earnings reports so far, the market is 2 standard deviations above its 50-DMA and overbought on multiple indicators. Unsurprisingly, the market gave up its early gains yesterday and closed near flatline. It would not be surprising to see the market struggle to advance from current levels, and even with the buy signal in place, a pullback to previous support would not only be healthy but should be expected. Such pullbacks should be used to add equity exposure to portfolios as needed.

Today is another big day for earnings, but we also have a LOT of economic data for the market to process. Manufacturing reports have come in much weaker than expected, and today, we get a first look at Q4 GDP and consumption estimates. Understand that these numbers are based on the estimates of economists, so the numbers should be close to expectations. However, we will likely see these numbers revised down somewhat over the next two months as actual data is factored in.

Nonetheless, there is likely little in the data to deter the market’s current expectations for 5-6 rate cuts this year. However, next week’s FOMC meeting could potentially put a damper on things if the Fed decides to walk back some of its recent dovishness to cool markets down a

Is California The Economic Canary In The Coal Mine?

In a recent Commentary, we noted that according to the Philadelphia Fed, 21 of the 50 states are in economic contraction. While that may be worrying, the amount of economic activity in each state varies widely. Therefore, as we wrote:

“What matters from a national perspective is the economic activity in the most significant states ranked by GDP. In order, California, Texas, New York, Florida, and Illinois have the biggest GDPs. Three of them, California, Texas, and Florida, have positive economic growth, per the Philadelphia Fed.”

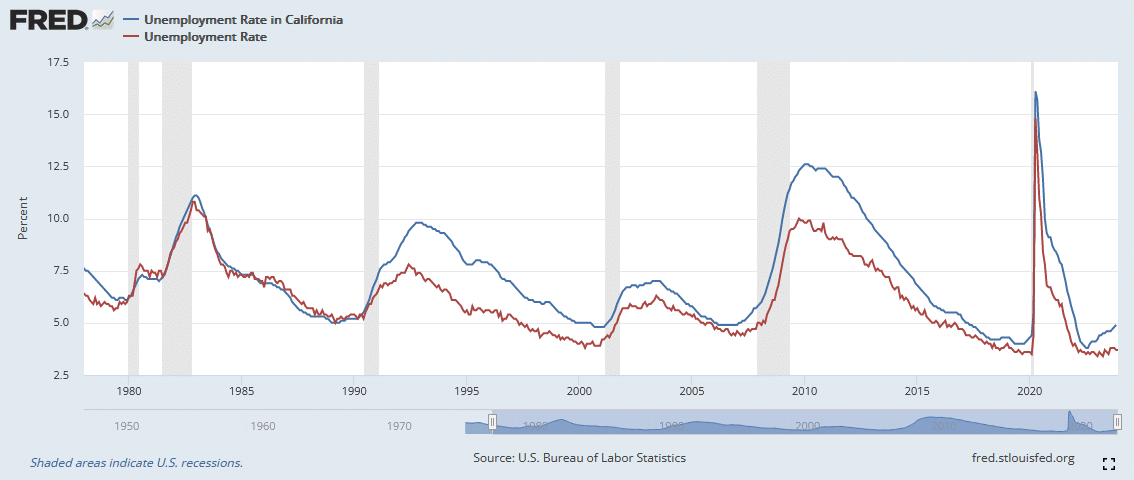

The Philadelphia Fed claims the economy in California, accounting for over 10% of national GDP, is growing, albeit slowly. But the second graph below warns otherwise. Its unemployment rate has ticked up from 3.8% in July 2022 to 4.9% today. Further, California and national employment trends correlate closely. Accordingly, we are concerned the recent divergence will fade, with the national rate catching up to California’s rate. If so, California might be the canary in the economic coal mine!

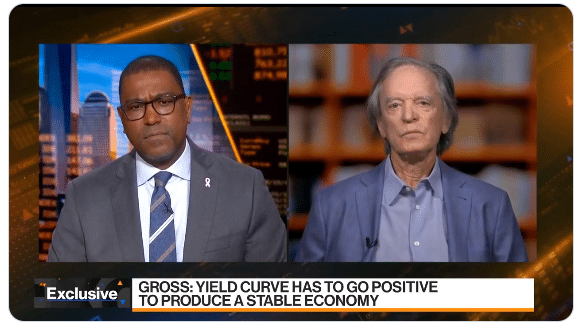

Bond King Bill Gross Remains Bearish

Bill Gross, retired portfolio manager at PIMCO, has been on the wires recently, warning of a recession. In his latest interview (LINK HERE), he thinks the Fed should halt QT immediately and cut rates to avoid a “significant recession.” Per the interview-

“I would stop quantitative tightening. I think that’s just not a correct philosophy and policy at this point to continue to tighten quantitatively. They should leave the reserve balance around $7 trillion and just see what happens going forward. I also think that, yes, the Fed should lower interest rates over the next 6 to 12 months. Real interest rates are simply too high. The 10-year real interest rate is 1.8%, which historically is very restrictive. And I think not only the Fed but I would like to see the real interest rate on the 10-year come down to 1.5%. The way to do that is to lower interest rates from where we have it now at 5.25% for fed funds and to basically balance out real interest rates and lower them so that the economy won’t go into a significant recession.”

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read