According to the most recent AAII sentiment poll, bears have outnumbered bulls for 35 consecutive weeks. Such is the longest streak going back to at least 1987. While the sentiment is historically poor, which many construe as bullish, investor positioning is not following suit. The graph in the upper left shows the AAII’s extreme bearishness. The three other graphs point to bullish investor positioning. Investor logic is at a crossroads as sentiment and positioning are worlds apart. Before we would be comfortable claiming that the bear market is over, we would like to see poor sentiment and, similarly, negative positioning reflecting investors are indeed scared.

The bottom two graphs show that SPY’s short positioning and the VIX are near the year’s lows. The top right graph highlights that flow into equity funds remain near all-time highs. Further, they are well above any point in the last 12 years.

What To Watch Today

Economy

- 7:30 a.m. ET: Challenger Job Cuts, year-over-year, November (48.3% prior)

- 8:30 a.m. ET: Personal Income, October (0.4% expected, 0.4% prior)

- 8:30 a.m. ET: Personal Spending, October (0.8% expected, 0.8% prior)

- 8:30 a.m. ET: PCE Deflator, month-over-month, October (0.5% expected, 0.3% prior)

- 8:30 a.m. ET: PCE Deflator, year-over-year, October (6.0% expected, 6.2% prior)

- 8:30 a.m. ET: PCE Core Deflator, month-over-month, October (0.3% expected, 0.5% prior)

- 8:30 a.m. ET: PCE Core Deflator, year-over-year, October (5.0% expected, 5.1% prior)

- 8:30 a.m. ET: Initial Jobless Claims, week ended Nov. 26 (235,000 prior)

- 8:30 a.m. ET: Continuing Claims, week ended Nov. 19 (1.5701 million prior)

- 9:45 a.m. ET: S&P Global U.S. Manufacturing PMI, November final (47.6 expected, 50.2 prior)

- 10:00 a.m. ET: Construction Spending, month-over-month, October (-0.2% expected, -0.2% prior)

- 10:00 a.m. ET: ISM Manufacturing, November (49.7 expected, 50.2 prior)

- WARDS Total Vehicle Sales, November (14.60 million expected, 14.90 prior)

Earnings

Market Trading Update

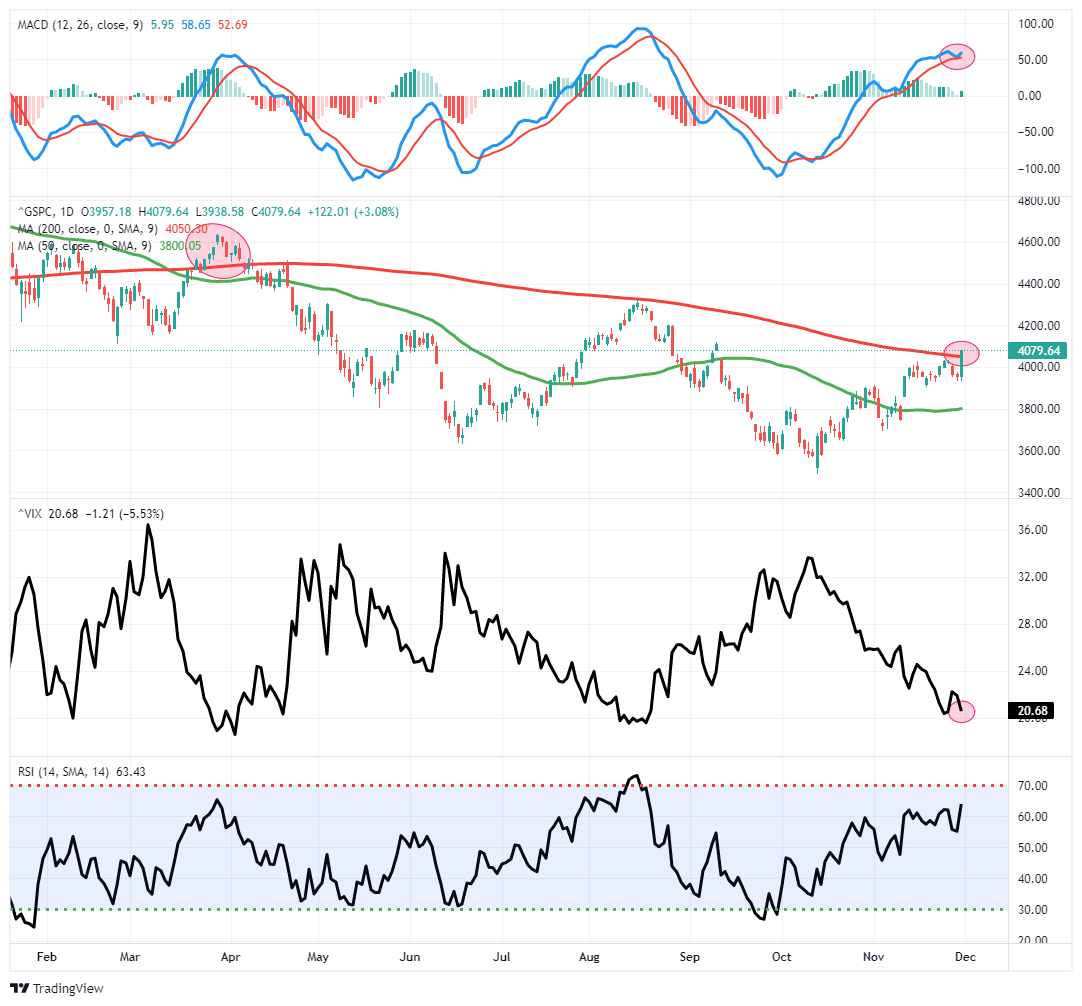

With Powell signaling that the Fed would slow the pace of interest-rate increases, starting as soon as at its Dec. 13-14 meeting (read: 75bps hike are dead), stocks soared on Wednesday, keeping the MACD “buy signal” from crossing.

“While Powell did have his hawkish moments, like when he repeated that it’s likely that interest rates will need to go “somewhat higher” than what policymakers had forecast in September, he was more dovish than hawkish and omitted language from Nov 2 when he said that “we have a ways to go with interest rates before we get to the level that is sufficiently restrictive.”

And despite Powell’s saying that history has taught him “loosening policy prematurely would be a mistake” and that the Fed is going to stay the course until its job is done, stocks exploded when he echoed Brainard saying that “If you are waiting for inflation to go down, it’s very difficult not to overtighten.”

In response to Powell’s dovishness, the S&P 500 soared 2.9% higher, crossing above the 200-dma and sending the VIX plummeting back toward its lows. Despite tighter monetary policy coming, the rally will certainly excite the bulls near term and could send the markets higher. However, just because the market is currently above the 200-dma, we need a successful retest and confirmation of that break before increasing equity exposure. The last time we broke above the 200-dma, it was short-lived.

Job Growth is Finally Slowing

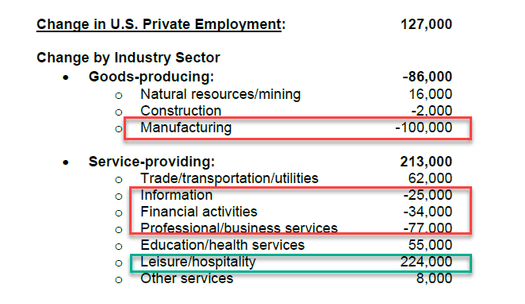

The ADP report shows a gain of 127k jobs in November, well below the +200k estimate and +239k in October. As shown below, +127k is the lowest increase in almost two years. The second table, courtesy of Zerohedge, shows that the leisure and hospitality industry grew the most, while significant job losses occurred in manufacturing and professional and business services. Further, small and large businesses lost jobs, but companies with 50-249 employees saw significant job growth. From the Fed’s perspective, this may be the first labor report that shows their actions are finally weighing on the labor markets. Per ADP’s Chief Economist:

Turning points can be hard to capture in the labor market, but our data suggest that Federal Reserve tightening is having an impact on job creation and pay gains. In addition, companies are no longer in hyper-replacement mode. Fewer people are quitting and the post-pandemic recovery is stabilizing.

Yesterday’s JOLTS data seems to confirm ADP. The number of job openings fell to 11.3 million. While still extremely high, it has been trending lower over the last six months. Chicago’s PMI fell sharply to levels that occur at the peak of recessions. However, the employment gauge within the report rose by 1.5 points to 47.1. The number still points to a contraction in the labor force but not to a meaningful degree.

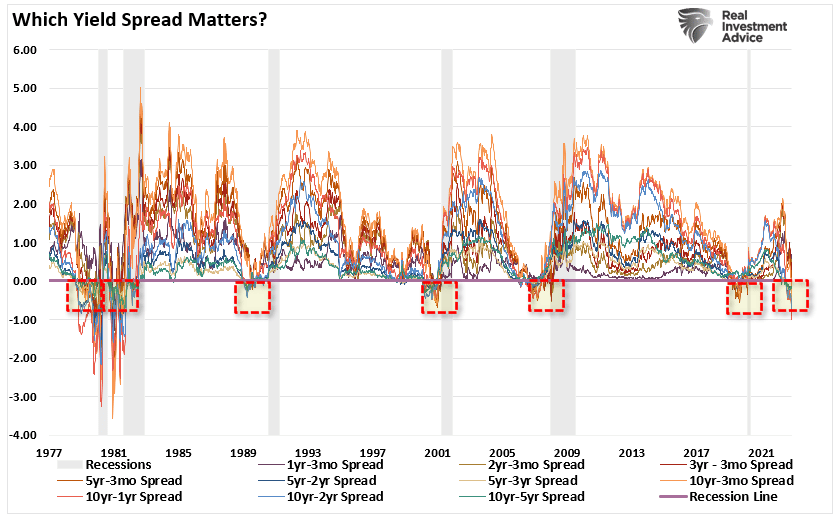

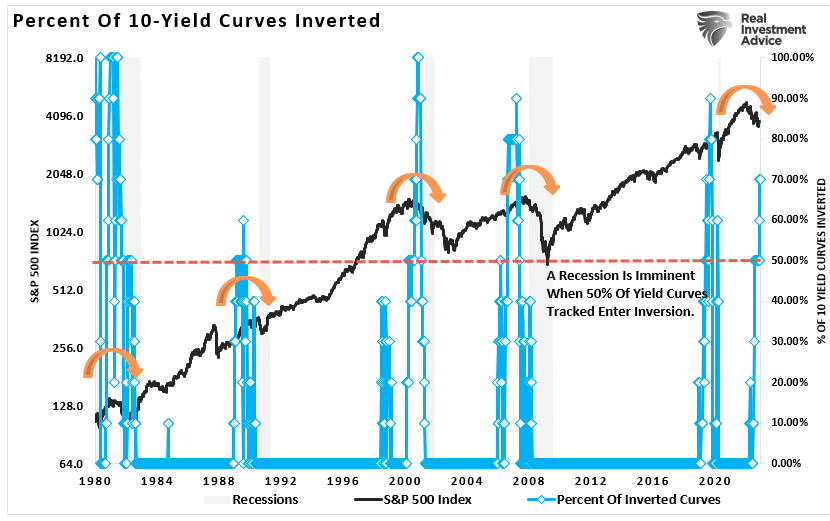

Yield Curve Update

Yesterday we focused on the 10yr/3m yield curve and the potential implication of inversion for stock prices. Today we take a broader look at many yield curves to better appreciate the recession warning being signaled. The graphs show an inversion in 70% of yield curves and in some cases at levels not seen in 40 years. Each time this many yield curves were inverted, a recession soon followed. Note, however, the recession typically occurs after the yield curve un-inverts. In the same vein, it is common for the stock market to roll over once the yield curves start to un-invert.

One Monetary Policy Fits All

Why are U.K. pension funds requiring bailouts? Any wonder Japan is capping interest rates despite rising inflation? Does the Fed have anything to do with the FTX failure? These questions and many others are best assessed with understanding the dollar’s role in the global economy. As such, our latest two-part article (Our Currency, The World’s Problem, and One Monetary Policy Fits All – Part II) helps readers appreciate the dollar, higher interest rates, QT, and the role the Fed plays globally. To summarize the two articles- in economic terms, demand for the dollar increases while supply falls. The result is the asset classes most dependent on liquidity, often the more speculative of assets, are starting to show stress.

The world is dependent on dollars for trade. Further and more importantly, it is estimated there is at least $13 trillion in foreign dollar-denominated debt outstanding. For these borrowers, dollar strength results in higher coupon payments and payments at maturity. As a result of the strong dollar, demand for the dollar increases, creating a vicious spiral. As QT continues, the supply of dollars will likely decline. Further stress in speculative markets and on foreign borrowers will occur. More concerning, stress will slowly but surely move toward more traditional markets highly dependent on leverage.

The key takeaway we hope to impart is that Fed policy is the de facto monetary policy for the world.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read