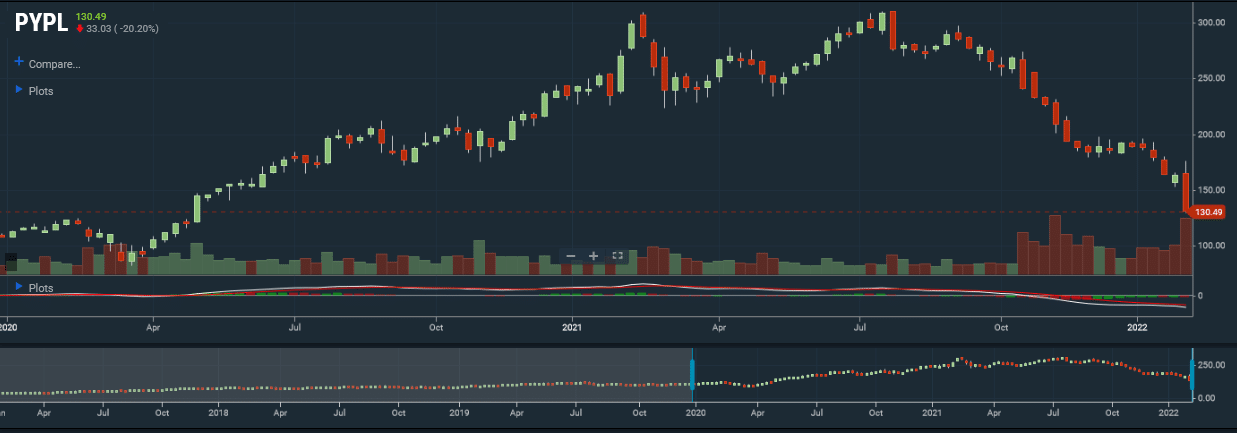

This earnings season seems to be generating more volatility than is typical. Yesterday’s earnings releases were no exception. Paypal fell over 20% despite only missing earnings by a penny and beating revenue expectations by $30 million. Investors are not thrilled with sharp reductions in Paypal’s forward earnings guidance. Paypal shares are now down well over 50% from last July’s record highs. Meta (Facebook) is trading down 20% in pre-market trading on disappointing earnings, forward guidance, and user statistics. On the flip side, Google rose 8% Wednesday, as they handily beat earnings and announced a stock split.

With valuations at extremes and the Fed changing stance, stocks like Paypal and Meta are get crushed when they disappoint. With many companies having reported fourth-quarter earnings, the new source of volatility will shift to Wall Street upgrades and downgrades. Buckle up!

{dmc}

What To Watch Today

Economy

- 7:30 a.m. ET: Challenger Job Cuts, year over year, January (-75.3% prior)

- 8:30 a.m. ET: Nonfarm Productivity, fourth quarter preliminary (3.9% expected, -5.2% expected)

- 8:30 a.m. ET: Unit Labor Costs, fourth quarter preliminary (1.0% expected, 9.6% during prior quarter)

- 8:30 a.m. ET: Initial Jobless Claims, week ended Jan. 29 (245,000 expected, 260,000 during prior week)

- 8:30 a.m. ET: Continuing Claims, week ended Jan. 22 (1.620 million expected, 1.675 million

- during prior week)

- 9:45 a.m. ET: Markit US Services PMI, January final (50.9 expected, 50.9 prior month)

- 9:45 a.m. ET: Markit US Composite PMI, January final (50.8 expected, 50.8 prior month);

- 10:00 a.m. ET: ISM Services Index, January (59.5 expected, 62.0 prior)

- 10:00 a.m. ET: Factory Orders, December (-0.4% expected, 1.6% final)

- 10:00 a.m. ET: Factory Orders Excluding Transportation, December (0.4% expected, 0.8% final)

- 10:00 a.m. ET: Durable Goods Orders, December final (-0.9% expected, -0.9% prior)

- 10:00 a.m. ET: Durable Goods Excluding Transportation, December final (0.4% prior)

- 10:00 a.m. ET: Capital Goods Orders Nondefense Excluding Aircrafts, December final (0.0%)

- 10:00 a.m. ET: Capital Goods Shipments Nondefense Excluding Aircrafts, December final (1.3%)

Earnings

Pre-market

- 6:30 a.m. ET: Cigna (CI) to report adjusted earnings of $4.71 on revenue of $43.97 billion

- Merck (MRK) to report adjusted earnings of $1.54 on revenue of $13.19 billion

- Eli Lilly & Co. (LLY) to report adjusted earnings of $2.48 on revenue of $7.75 billion

- Honeywell (HON) to report adjusted earnings of $2.07 on revenue of $8.71 billion

- Estee Lauder (EL) to report adjusted earnings of $2.62 on revenue of $5.49 billion

- Cardinal Health (CAH) to report adjusted earnings of $1.25 on revenue of $45.34 billion

Post-market

- 4:05 p.m. ET: Ford (F) to report adjusted earnings of $0.45 on revenue of $34.79 billion

- Amazon (AMZN) to report adjusted earnings of $7.80 on revenue of $137.83 billion

- Snap (SNAP) to report adjusted earnings of $0.11 on revenue of $1.20 billion

- Pinterest (PINS) to report adjusted earnings of $0.43 on revenue of $832.92 million

- Activation Blizzard (ATVI)to report adjusted earnings of $1.31 on revenue of $2.66 billion

- Skechers (SKX) to report adjusted earnings of $0.34 on revenue of $1.55 billion

- GoPro (GPRO) to report adjusted earnings of $0.35 on revenue of $382.75 million

- Fortinet (FTNT) to report adjusted earnings of $1.15 on revenue of $961.96 million

- News Corp. (NWSA) to report adjusted earnings of $0.33 on revenue of $2.64 billion

- Unity Software (U) to report an adjusted loss of $0.08 on revenue of $293.39 million

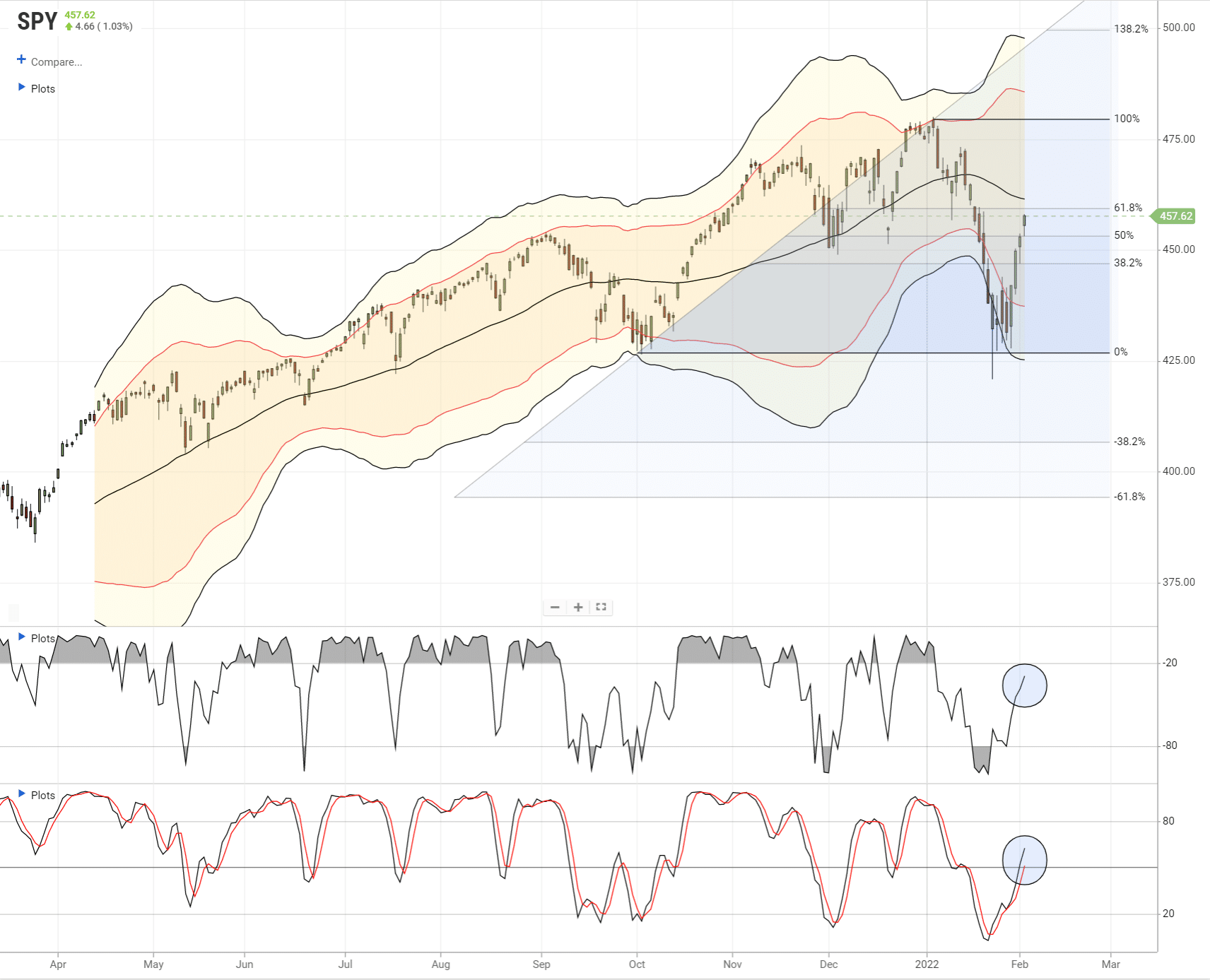

Rally Update

In last week’s newsletter, we outlined a rally sequence taking the S&P 500 back towards the 50-dma. While we expected that 50% to 61.8% retracement to take a week or two, it occurred over just the last few days. The rally is not overbought on either indicator as of yet. Stock selection is now becoming very important to avoid companies like Paypal, and own companies like Google.

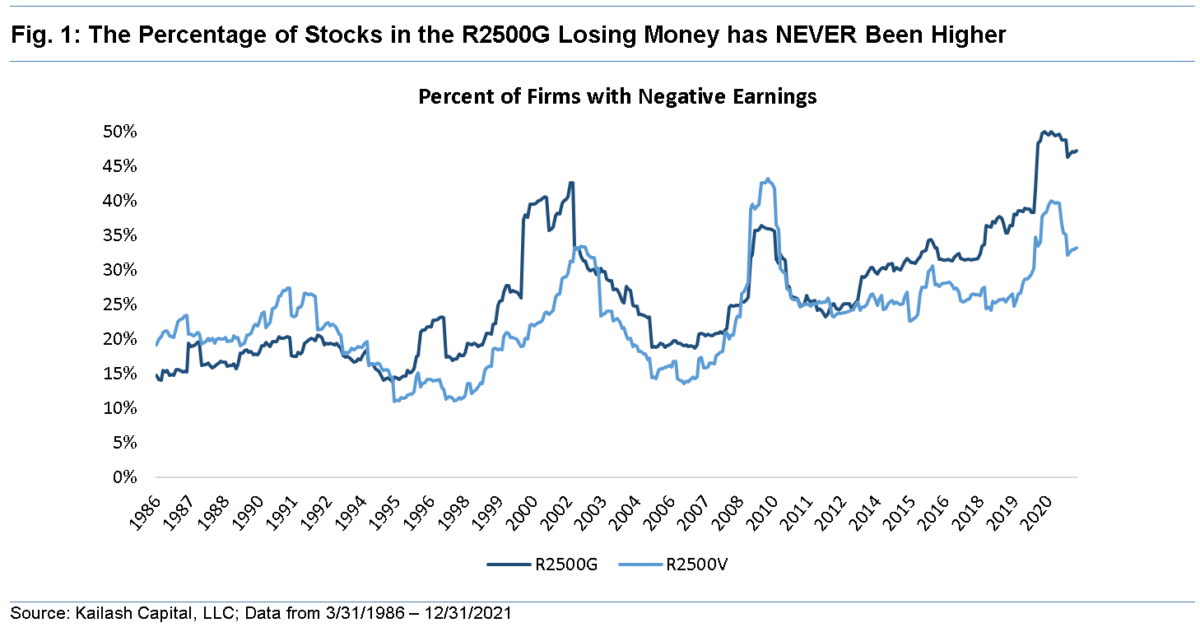

Be Careful What You Own

A great report from Kailash Concepts discusses the FTSE Russell 2500 index which, as they note, is considered THE benchmark for small and mid-capitalization companies.

The chart below shows that the percentage of firms in the Russell 2500 indexes that lose money is falling from dot.com highs of ~50% in Growth and ~35% in Value. History suggests the loss-making firms in the R2500G will inflict severe damage on their owners compared to their profitable neighbors in that same index.

Eurozone Inflation Heating Up and So Is The Euro

Consumer prices in the Eurozone rose by 5.1% versus expectations of 4.4%. The surprisingly high inflation rate is leading markets to price in an ECB rate hike by July. Prior to the data, the first hike was not expected until September. The increase in inflation was primarily a function of rapidly increasing food and energy prices. The core (ex-food and energy) rate of inflation was 2.3%, down slightly from last month’s reading.

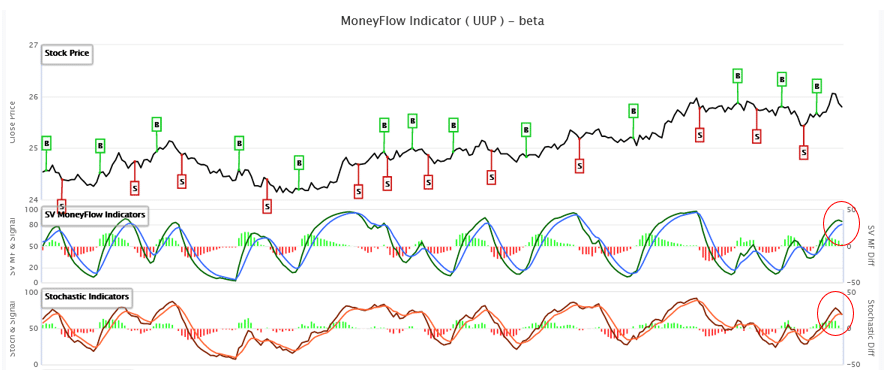

The euro is rising versus the dollar as the market assumes the ECB will need to take a more hawkish stance and thus reduce the expected interest rate differential between the Eurozone and the United States. Such should detract from recent dollar strength. From an equity perspective, we must consider the ECB is more likely to remove liquidity in concert with the Fed and other central banks. Global liquidity, was a big driver of outsized equity returns last year. The graph below shows the dollar ETF (UUP) has recently given up some gains. Further, it’s heading toward a sell signal (red circles) using our SimpleVisor proprietary model (middle graph) and stochastics (bottom graph).

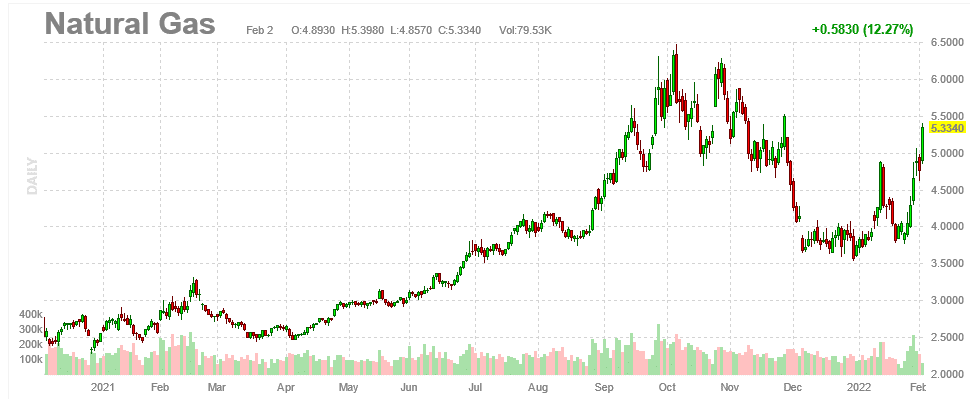

Natural Gas Is On Fire

Natural gas prices are up sharply over the past two weeks. Since the beginning of the year, natural gas is up nearly 60%, including yesterday’s 10+% increase. As the graph below shows, the price has been very volatile over the last six months. For instance, the recent price gains mirror the sharp decline in the last week of November. Both moves occurred over periods of less than two weeks. Driving recent gains are weather forecasts for a return of the deep freeze in mid-February and concerns about tighter than average supplies.

Google’s Just Keeps Growing

As discussed in yesterday’s morning commentary, while Paypal’s earnings were dreadful, Google, by every measure, continued to perform. As noted by Chartr:

Alphabet reported quarterly revenue of about $75bn, which is up about 32% on this time last year, with just about every single segment firing on all cylinders.

YouTube ad revenue was up a healthy 25%, but it was nothing on Alphabet’s main property, Google Search, which clocked in a record $43bn of quarterly revenue, growing 36% on last year. Even better than that was Google’s Cloud biz, which competes with Microsoft’s Azure and Amazon’s AWS, it notched revenue that was up 45% on last year.

As noted yesterday, we have a near 5% weighting in the Equity portfolio. We have no exposure to companies like Paypal and Meta.

ADP

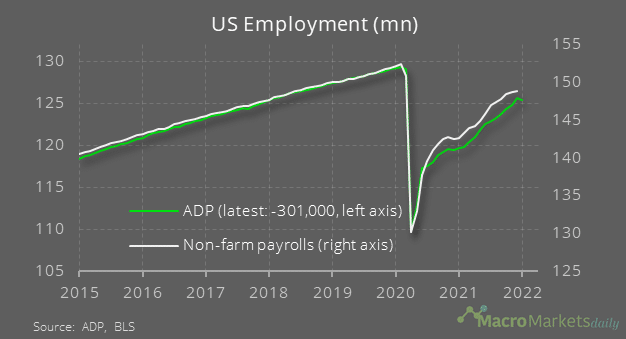

The ADP report, a precursor to Friday’s BLS report, was well below expectations showing a loss of 301k jobs in January. Expectations were for a gain of 200k jobs. This was the first time ADP reported a negative print since December 2020. Per ADP chief economist Nela Richardson – “The labor market recovery took a step back at the start of 2022 due to the effect of the omicron variant and its significant, though likely temporary, impact to job growth,”

We tend to agree the decline is likely due to one-off factors such as Omicron and traditional holiday-related employment changes. We suspect this is not enough to change the Fed’s perceived path, but if labor weakness continues, the Fed has an excuse to shift to a more dovish stance. The graph below from Macro Markets Daily shows the strong correlation between ADP and the BLS data.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

Also Read