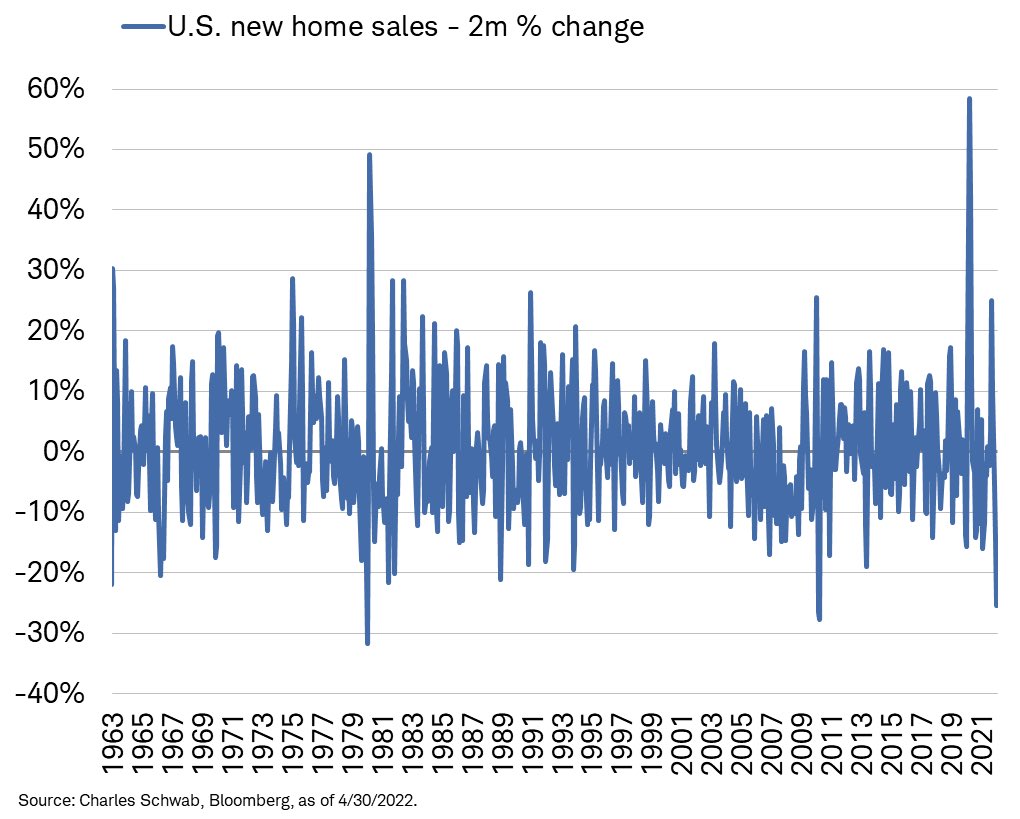

New home sales plummeted to an annualized rate of 591k, well below expectations of 750k. As the graph below shows, the two-month decline in new home sales was only worse during the financial crisis and in 1980. Between inflation’s damaging effect on consumer psyches and their wallets, as well as sharply rising mortgage rates, weakness should be expected. Based on new home sales and completed but unsold inventories, there is a 9-month inventory of new homes. Despite the high inventory, new home prices are not plummeting. Not yet, at least! The median price of a new home is up 19.6% versus last year.

New home construction is an integral part of the economy, and housing accounts for about two-thirds of CPI. This data provides more mounting evidence that the economy may slip into a recession in the coming months. For more recession evidence, consider our latest article- Snap Goes The Economy.

What To Watch Today

Economy

- 8:30 a.m. ET: GDP Annualized, quarter-over-quarter, 1Q second (-1.3% expected, -1.4% prior)

- 8:30 a.m. ET: Personal Consumption, quarter-over-quarter, 1Q second (2.8% expected, 2.7% prior)

- 8:30 a.m. ET: GDP Price Index, quarter-over-quarter, 1Q second (8.0% expected, 8.0% prior)

- 8:30 a.m. ET: Core PCE, quarter-over-quarter, 1Q second (5.2% expected, 5.2% prior)

- 8:30 a.m. ET: Initial Jobless Claims, week ended May 21 (215,000 expected, 218,000 prior)

- 8:30 a.m. ET: Continuing Claims, week ended May 14 (1.310 million expected vs. 1.317 million)

- 10:00 a.m. ET: Pending Home Sales, month-over-month, April (-2.0% expected, -1.2% prior)

- 10:00 a.m. ET: Pending Home Sales NSA, year-over-year, April (-8.0 expected, -8.9% prior)

- 11:00 a.m. ET: Kansas City Fed Manufacturing Index, May (18 expected, 25 prior)

Earnings

Pre-market

- Macy’s (M) to report adjusted earnings of $0.83 on revenue of $5.36 billion

- Dollar Tree (DLTR) to report adjusted earnings of $2.02 on revenue of $6.77 billion

- Dollar General (DG) to report adjusted earnings of $2.31 on revenue of $8.71 billion

- Ulta Beauty (ULTA) to report adjusted earnings of $4.45 on revenue of $2.12 billion

- Lions Gate (LGF) to report adjusted earnings of $0.09 on revenue of $964.64 million

- VMware (VMW) to report adjusted earnings of $1.56 on revenue of $3.19 billion

- Alibaba (BABA) to report adjusted earnings of 7.10 (CNY) on revenue of 200.59 (CNY) billion

- Burlington Stores (BURL) to report adjusted earnings of $0.66 on revenue of $2.04 billion

- Jack in the Box (JACK) to report adjusted earnings of $1.34 on revenue of $262.93 million

- Buckle (BKE) to report adjusted earnings of $1.00 on revenue of $308 million

Post-market

- Costco (COST) to report adjusted earnings of $3.02 on revenue of $51.50 billion

- Dell Technologies (DELL) to report adjusted earnings of $1.40 on revenue of $25 billion

- Gap (GPS) to report an adjusted loss of $0.14 on revenue of $3.46 billion

- Autodesk (ADSK) to report adjusted earnings of $1.34 on revenue of $1.15 billion

- Workday (WDAY) to report an adjusted loss of $0.02 on revenue of $291 million

- Sumo Logic (SUMO) to report an adjusted loss of $0.17 on revenue of $66.09 million

- American Eagle Outfitters (AEO) to report adjusted earnings of $0.25 on revenue of $1.14 billion

Market Triggers A Buy Signal…Finally

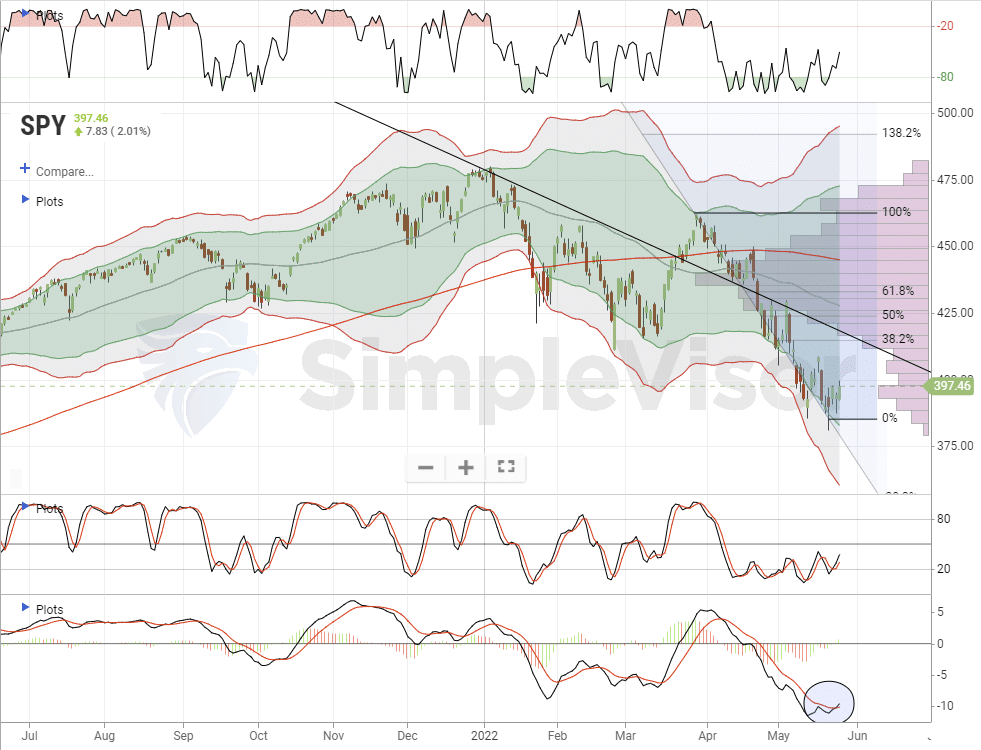

After 8-weeks of tough sledding, the market finally triggered a MACD buy signal with yesterday’s rally. Such suggest could potentially see the market attempt a reflexive rally back to previous resistance levels over the next couple of weeks. As noted, the most likely initial target for a rally is the downtrend line which intersects the 38.2% retracement level from the March highs. If we can break above that trend line there is resistance at the 50% retracement, and potentially the 200-dma. Each one of those levels should be sold into to raise cash and rebalance risk for now.

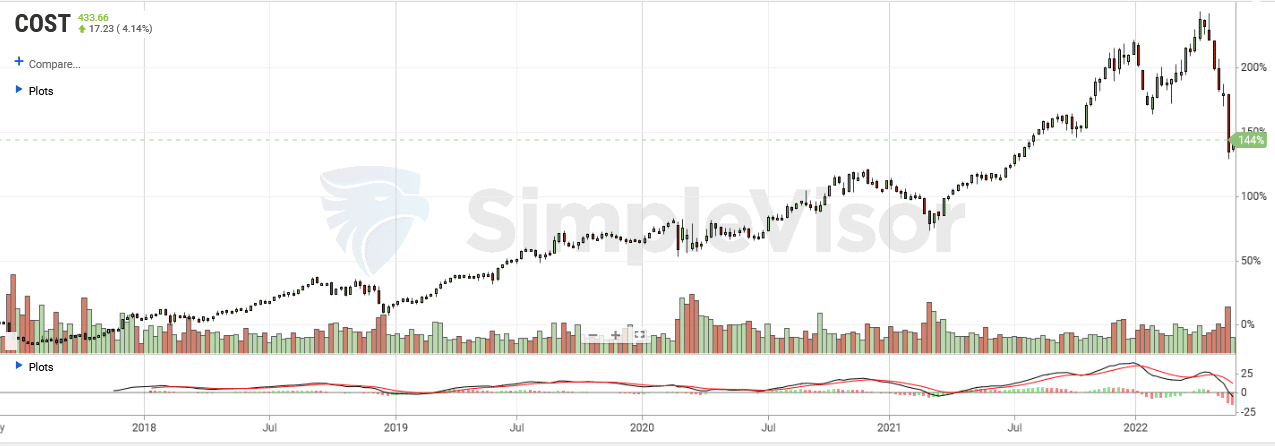

Costco On Deck

Costco’s (COST) stock is down almost 25% in the last month as other retailers, such as Walmart and Target, fell sharply on bad earnings and outlooks. COST announces earnings after the close today. Its earnings and sales are likely to be decent, given what Walmart reported on Sam’s Club. Expectations are for EPS of $3.04 and revenues of $51.56 billion.

Keep in mind that Costco’s membership fee revenue helps pad earnings, unlike many of its competitors. In our mind, the risk of COST stock taking a hit lies in pessimistic forward-looking estimates on sales and profits from its executives. That said, one can argue the stock is trading with the bad news priced in.

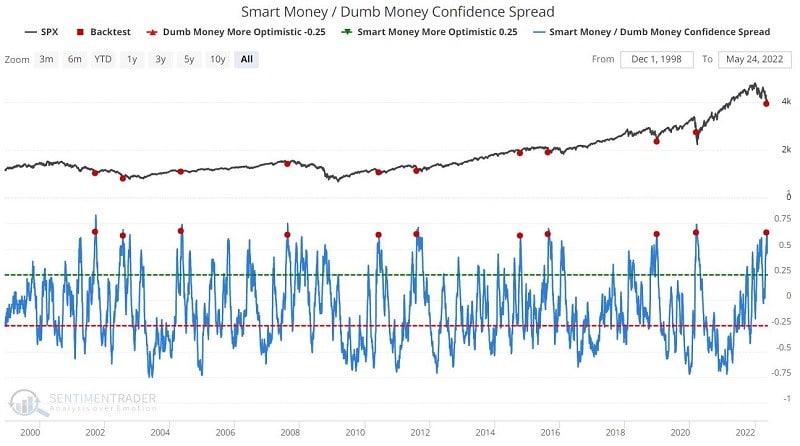

Dumb Money Doing Dumb Things

“Our Smart Money / Dumb Money Confidence Spread (SMDM) recently reached the upper decile of historical readings by crossing above 0.63. The chart below displays when SMDM crossed above 0.63 for the first time in three months. A reading of this level can only occur when Smart Money is quite confident and Dumb Money is extremely pessimistic.

A longer-term investor should view this SMDM signal as an “alert” that we may be entering a favorable period to put available cash to work in the stock market. Higher stock prices have consistently followed the signals described above over many years. There are, however, never any guarantees that the “next one” will follow suit. It is up to you and you alone to decide if you will use the signals and how.” – Sentiment Trader

The Fed Minutes Do not Pivot

The FOMC minutes provide the Fed an opportunity between FOMC meetings to update the markets on their latest views. Yesterday’s release of the minutes from May 4th shared very little new insight. Most members still expect half-point rate increases at the June and July meetings. Despite recent economic data and corporate commentary, “all participants concurred the U.S. economy was still very strong, the labor market was extremely tight, and inflation was very high.” That statement alone leads us to believe that recent market volatility and higher interest rates are not enough to get the Fed to back off on rate hikes or QT. Anyone looking for signs of a Fed pivot will be disappointed with the minutes. That said, they made a few comments that allude that recent rate hikes and the Fed’s hawkish bias appear to be affecting the economy and financial markets. To wit:

“Financial conditions tightened notably over the period. Treasury yields increased across the curve, with the rise primarily reflecting higher real interest rates.“

“The staff noted that increased uncertainty and ongoing volatility had reduced risk appetite in financial markets and eased price pressures, although valuations of many assets remained elevated.“

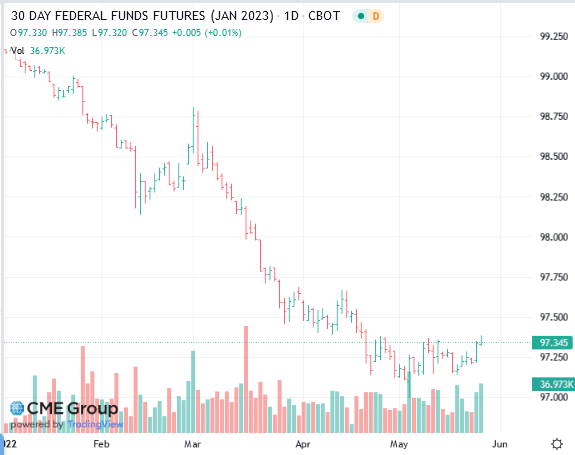

Re-Pricing Fed Funds Expectations

Recently, there is growing evidence that a recession could start as early as the Q2 GDP release in July. This is not being lost on the bond markets and implied expectations for how much the Fed will raise rates. Since early May, the 2yr U.S. Treasury yield has fallen by about .25% to 2.51%. Over the same period, the January Fed Funds futures contract, shown below, has increased in price by a similar amount. Essentially, both indicators imply the Fed will hike rates 25 basis points less than was expected a few weeks ago. While the market thinks the Fed will be a little less hawkish, it has yet to hear any substantial change in Fed rhetoric to warrant a change in expectations. We presume rhetoric will not change materially until inflation shows more signs of abating.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read