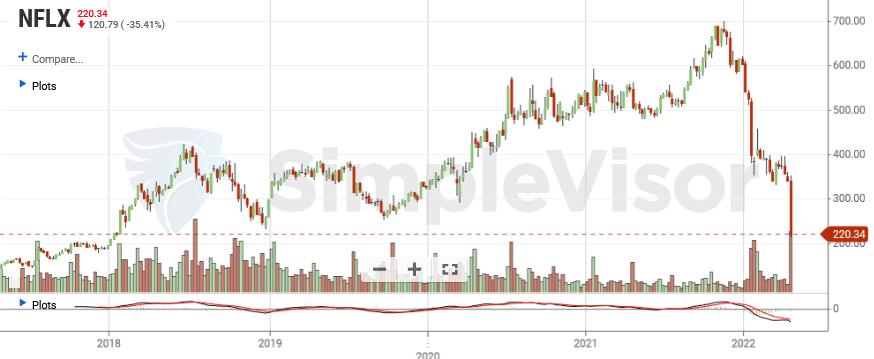

Shares of Netflix (NFLX) lost over a third of their value on Wednesday after announcing they lost 200k subscribers in the first quarter. If you recall, Netflix fell 22% on January 21st after its prior quarterly earnings report. Year to date, the stock is down over 60% and back to early 2018 levels. Not only does Netflix face stiff streaming competition, but it lost 70,000 Russian customers in the last three months.

We think the more significant takeaway from Netflix’s report is not specific to Netflix or streaming but a broader macroeconomic problem. Some Netflix customers and customers of many discretionary products are forced to make hard consumption choices due to inflation. Investors seem to understand how inflation affects consumption. To that end, the consumer staples sector (XLP) is up 4% this year, while consumer discretionary stocks (XLY) are down 13% year to date.

What To Watch Today

Economy

- 8:30 a.m. ET: Philadelphia Fed Business Outlook index, April (20.5 expected, 27.4 in March)

- 8:30 a.m. ET: Initial jobless claims, week ended April 16 (185,000 during prior week)

- 8:30 a.m. ET: Continuing claims, week ended April 9 (1.475 million during prior week)

- 10:00 a.m. ET: Leading Index, March (0.3% expected, 0.3% in February)

Earnings

Pre-market

- Dow Inc. (DOW) to report adjusted earnings of $2.07 on revenue of $14.50 billion

- Danaher (DHR) to report adjusted earnings of $2.67 on revenue of $7.56 billion

- Xerox (XRX) to report adjusted earnings of 13 cents on revenue of $1.66 billion

- AT&T (T) to report adjusted earnings of 75 cents on revenue of $37.07 billion

- American Airlines (AAL) to report adjusted losses of $2.41 on revenue of $8.82 billion

- Pool Corp. (POOL) to report adjusted earnings of $3.13 on revenue of $1.27 billion

- AutoNation (AN) to report adjusted earnings of $5.25 on revenue of $6.51 billion

- Alaska Air Group (ALK) to report adjusted losses of $1.59 on revenue of $1.66 billion

- Tractor Supply Co. (TSCO) to report adjusted earnings of $1.42 on revenue of $2.92 billion

- Philip Morris International (PM) to report adjusted earnings of $1.49 on revenue of $7.42 billion

- Union Pacific (UNP) to report adjusted earnings of $2.52 on revenue of $5.75 billion

- Blackstone (BX) to report adjusted earnings of $1.05 on revenue of $2.48 billion

Post-market

- Las Vegas Sands (LVS) to report adjusted losses of 22 cents on revenue of $1.08 billion

- Snap (SNAP) to report adjusted earnings of 1 cent on revenue of $1.07 billion

- Boston Beer Co. (SAM) to report adjusted earnings of $2.07 on revenue of $446.27 million

Market Trading Update

Despite the dismal report from Netflix, the market held its ground today for the most part. While there was a pullback in some of the technology names in the communication space, the rest of the market faired okay most of the day. The market remains oversold, and the short-term buy signal is more evident. We continue to think the short-term bias is to the upside given the overall psychological negativity, and the earnings season now underway.

Netflix Economics

“Like many startups, for years Netflix burned cash in order to grow faster. Now, ironically, it is in the opposite position — with a mature business that has stopped growing. In Netflix’s most recent financial year the company reported a healthy operating income of more than $6bn. That gives Netflix a decent amount of margin to work with as the company begins its efforts to get growth back on the right side of zero — if it can keep its huge content costs from spiraling higher.” – Chartr

Value vs Growth

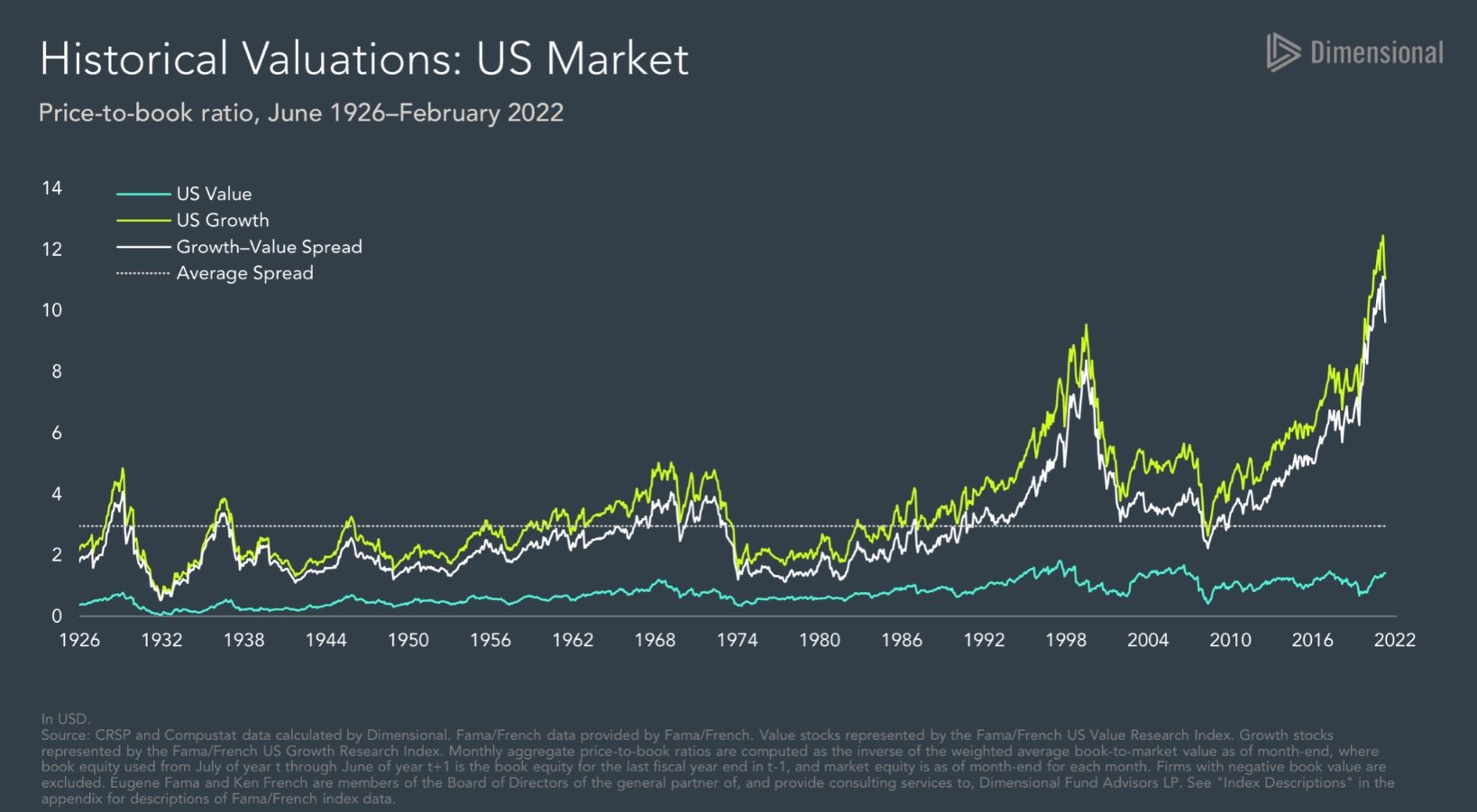

In the last few months value stocks have decently outperformed growth stocks. Most market commentators explain it as investors seeking safety in conservative, lower beta, and higher dividend stocks. While true, the graph below provides further context. The price to book ratio of growth stocks is at unprecedented levels, even with the recent decline. At the same time the ratio for value stocks is plodding along near its longer-term average. Prior peaks in the growth-value spread ultimately return to and sometimes through the longer-term average spread. This leaves us an important question, has the growth-value spread peaked?

Japanese Yen and Treasury Bonds- Two Peas in a Pod

The graph below shows the recent strong correlation between the Japanese yen and ten-year Treasury yields. As shown in blue, the yen has collapsed this year. At the start of the year, it took 114 yen to buy a dollar. Today it takes 129. The yen’s weakness is primarily a function of the Bank of Japan’s (BOJ) easy monetary policy. To wit, last night, they offered to buy an “unlimited amount” of ten-year Japanese Treasury bonds (JGBs) at .25%. That wasn’t its first time. The bank’s goal is to cap interest rates. At the same time the BOJ is aggressive with QE, the U.S. and other countries are quickly raising rates and reversing QE.

A weaker yen will eventually result in more inflation for Japan, which in turn might force the BOJ to take a more hawkish stance. Given the ferocity of the currency move, it would not be surprising to see the BOJ and/or the Fed/Treasury intervene in currency markets to halt the yen’s depreciation. Treasury yields should fall if the yen stabilizes or appreciates. The MACD reading in the lower graph shows the yen is grossly oversold on a technical basis. A reflexive bounce in the yen and Treasurys is likely.

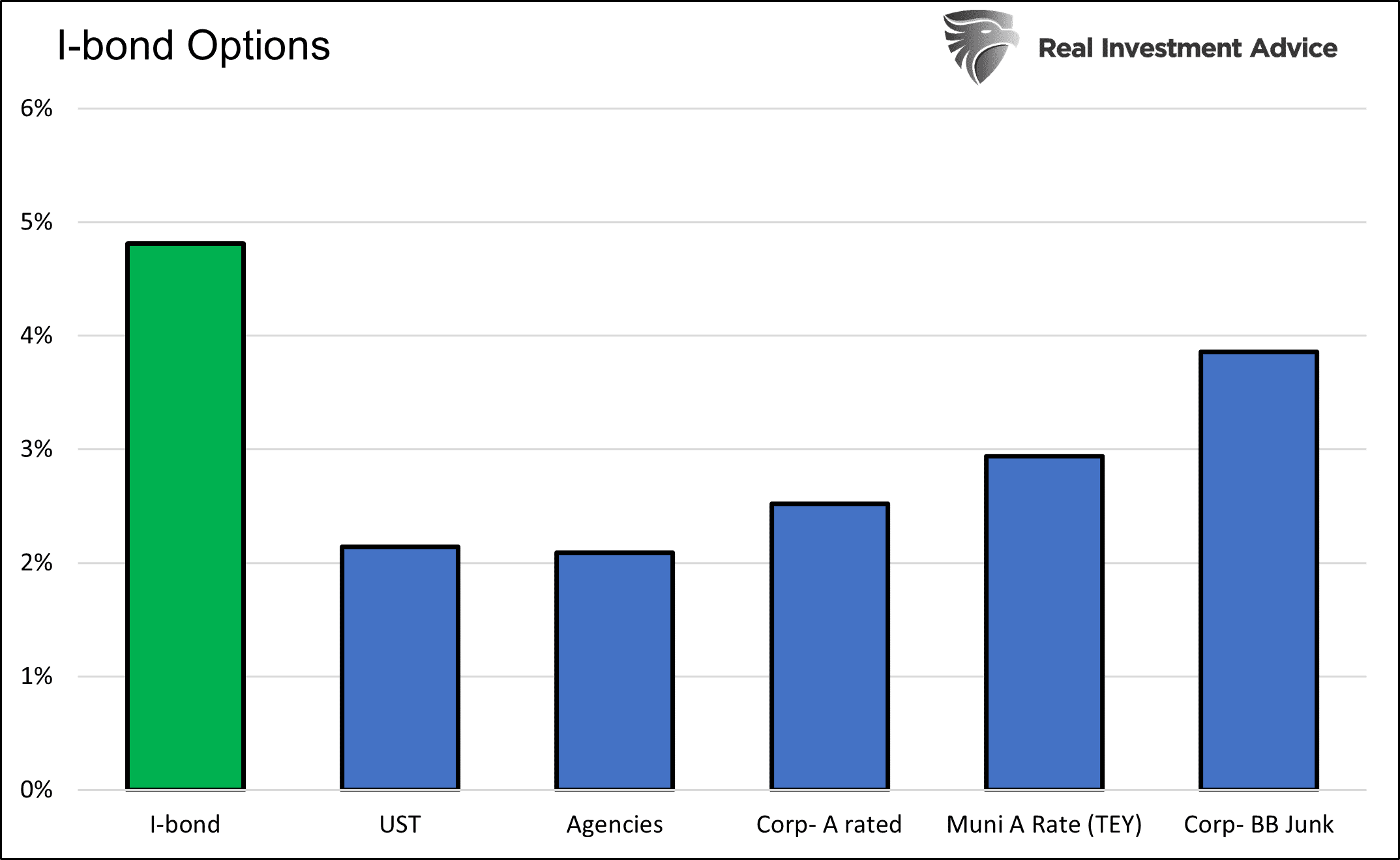

Series I-Bonds – Are They Right For You?

On Wednesday, we published I-Bonds: At 7%, It’s Hard to Go Wrong. The article provides details of a type of bond that many investors are unfamiliar with. Series I-bonds are offered directly to investors by the U.S. Treasury, and they currently yield at least 7.12%. Our report not only discusses the pros and cons of I-bonds but compares them to TIPS and other fixed-income alternatives.

The article concludes that the fiscal and monetary policy landscape of the past decades and those looking forward virtually ensures I-bonds, even with a zero percent real yield, make a lot of sense for many investors. As we write: “Regardless of inflation in the future, I-bonds should be a much better alternative to money markets or short maturity bonds. The state of indebtedness in the U.S. requires the Fed’s efforts to support it with negative real yields (inflation-adjusted). We do not see that changing.”

The graph below from the article compares I-bonds to other bonds with one-year maturities. While we make inflation assumptions to calculate the one-year I-bond yield, it will, in most inflation scenarios, be the best alternative.

CPI has to fall below 3% in the following six months to make an investor indifferent between a 1-year junk bond and the I-bond. Keep in mind the I-bond is risk-free while the junk bond is far from it. Even at 0 percent inflation in the second six-month period, a buyer is indifferent between buying a one-year Treasury bill and an I-bond today.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

Also Read