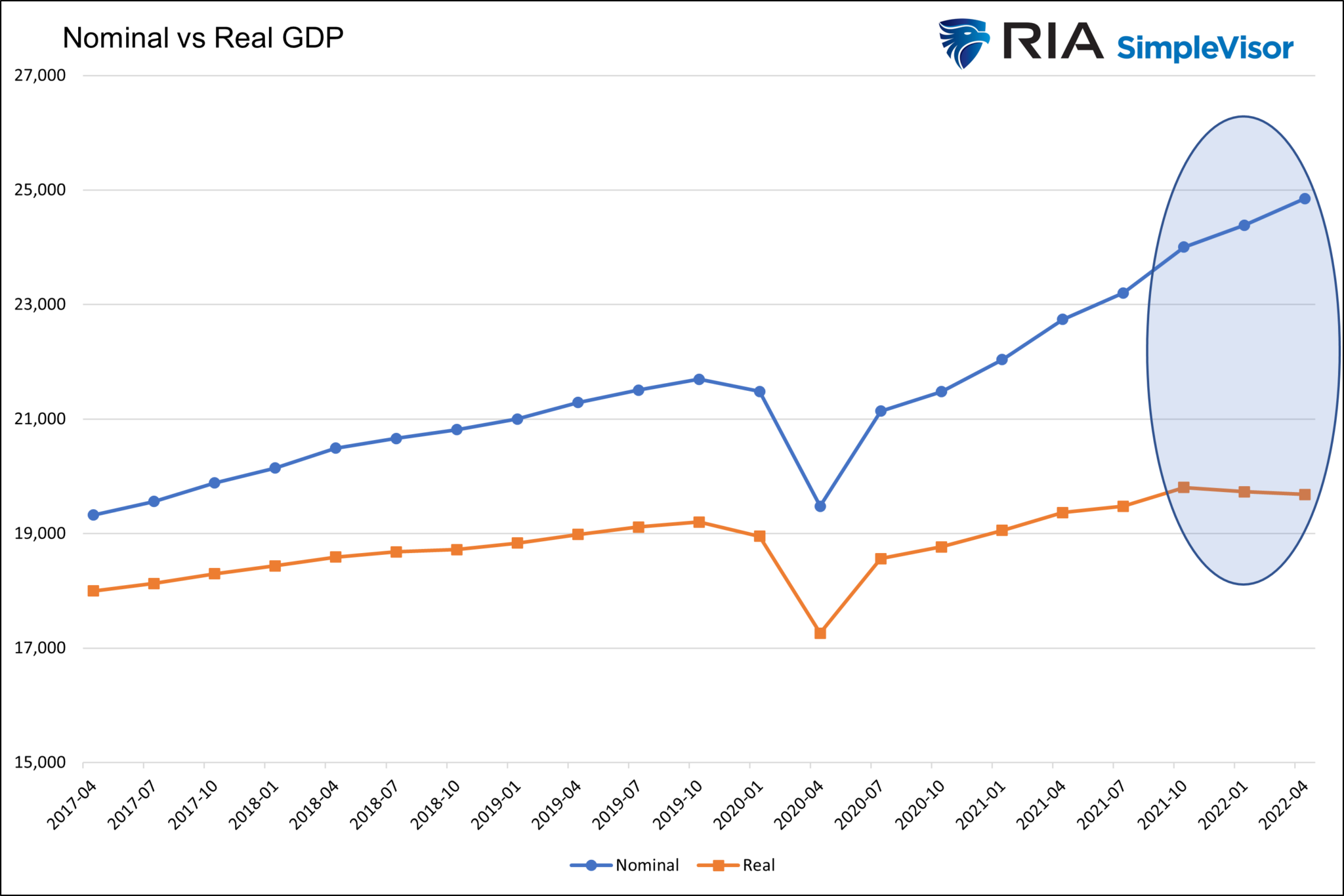

For the second quarter in a row, GDP was negative. Second quarter GDP fell 0.9% after the first quarter’s negative 1.6% print. Are we in a recession? Technically some claim two straight quarters of negative GDP signify a recession. While we tend to agree, we must be aware that the economy is growing rapidly on a nominal basis. Nominal GDP rose 7.8% from +6.6% in the first quarter.

Possibly more important within the report is the Personal Consumption Expenditure Price Index (PCE). This is the inflation factor that adjusts the positive 7.8% growth rate to the negative .09% real growth rate. It is also the Fed’s preferred inflation gauge. PCE remains very high at +8.7% year-over-year, the highest in this cycle and since the +11% in 1981!

What To Watch Today

Economy

- 8:30 a.m. ET: Employment Cost Index, 2Q (1.2% expected, 1.4% prior)

- 8:30 a.m. ET: Personal Income, month-over-month, June (0.5% expected, 0.3% prior)

- 8:30 a.m. ET: Personal Spending, month-over-month, June (0.9% expected, 0.2% prior)

- 8:30 a.m. ET: Real Personal Consumption, month-over-month, June (-0.4% prior)

- 8:30 a.m. ET: PCE Deflator, month-over-month, June (0.9% expected, 0.6% prior)

- 8:30 a.m. ET: PCE Deflator, year-over-year, June (6.8% expected, 6.3% prior)

- 8:30 a.m. ET: PCE Core Deflator, month-over-month, June (0.5% expected, 0.3% prior)

- 8:30 a.m. ET: PCE Core Deflator, year-over-year, June (4.7% expected, 4.7% prior)

- 9:45 a.m. ET: MNI Chicago PMI, July (55 expected, 56.0 prior)

- 10:00 a.m. ET: University of Michigan Sentiment, July preliminary (51.1 expected, 51.1 prior)

- 10:00 a.m. ET: University of Michigan Current Conditions, July final (57.1 expected, 57.1 prior)

- 10:00 a.m. ET: University of Michigan Expectations, July final (47.5 expected, 47.3 prior)

- 10:00 a.m. ET: University of Michigan 1-Year Inflation, July final (5.2 expected, 5.2% prior)

- 10:00 a.m. ET: University of Michigan 5-10-Year Inflation, July final (2.8% expected, 2.8% prior)

Earnings

- AstraZeneca (AZN), Sony (SON), Aon (AON), BNP Paribas (BNPQY)

Market Trading Update – Market Rallies As Earnings Continue To Be “Less Bad Than Expected”

As we have discussed over the last several days, the bulls continue to remain in charge as earnings from companies like MSFT, GOOG, AMZN, and AAPL, have been “less bad than expected.” Such has finally lifted the hopes from beaten down investors and the negative sentiment is starting to reverse. As I have stated previously, what is needed for a strong “counter-trend” rally in a bear market is for Jim Cramer to pronounce its “time to buy.” That occurred yesterday. To wit:

“When the Fed gets out of the way, you have a real window and you’ve got to jump through it. … When a recession comes, the Fed has the good sense to stop raising rates,” the “Mad Money” host said. “And that pause means you’ve got to buy stocks.”

Actually, that is incorrect. As we discuss in our upcoming Bull Bear Report Newsletter (Subscribe for free weekend email), when the Fed pauses, historically, that is when the recession is beginning, not ending.

Nonetheless, the bull market rally is “on,” and the market is in the midst of its best month since 2020. As shown below, the market has solidly confirmed its retest of the 50-dma and is now rapidly approaching more extreme overbought conditions. Our target for the rally remains 4150-4200, where it will likely be a good idea to take some profits and rebalance risk accordingly.

A White Collar Recession

The Milken Institute put a paper claiming this recession, unlike previous ones, will affect the employment of higher paid white collar employees more so than lower paid blue collar employees. Per the article:

“The Joe Six Pack, who used to be the first guy to be laid off, can be less concerned if he has one of these jobs that are in high demand, like the Amazon warehouse worker, delivery guy, the guy who’s working in the ghost kitchen,”

The article claims that many people employed in industries that were essentially shut down during the pandemic upgraded their skills. As a result, there is a labor shortage for specific low-paying jobs. Even as demand for goods and services slows, employers will be reluctant to cut said jobs. The fear is they will not be able to hire them back when the economy picks up again. As a result, cost-cutting actions may fall disproportionately upon higher-paid white-collar employees this time.

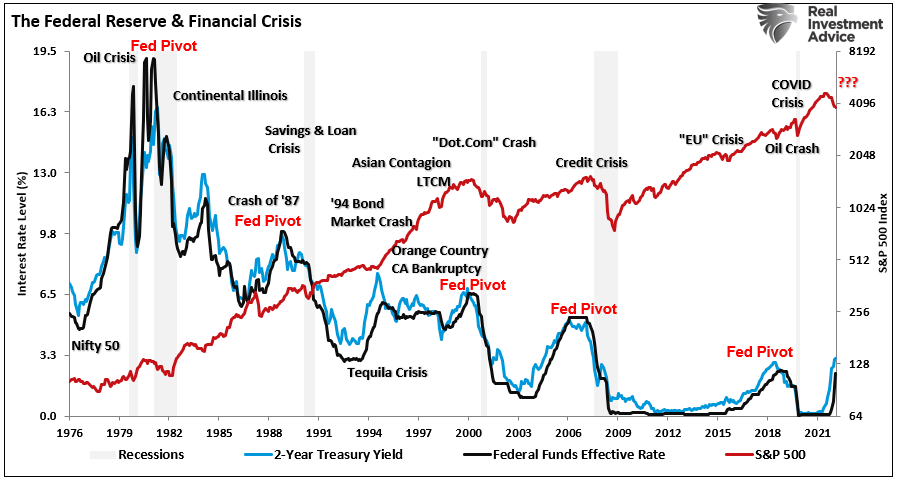

Meeting-By-Meeting Decisions- No More Forward Guidance

It’s time for “meeting-by-meeting” decisions, with little forward guidance. The stock market took off when Jerome Powell uttered “meeting-by-meeting” on Wednesday. Is meeting-by-meeting with no guidance bullish? Bulls argue that Powell is connotating that weakening economic data will begin to factor into its policy decisions. Without providing forward direction, the Fed can stall or pivot quicker and better react to slowing economic activity.

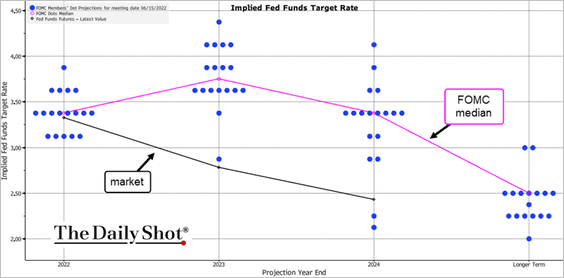

Bears argue that the message allows the Fed to raise interest rates higher than expected if inflation doesn’t slow quickly enough. Further, the Fed will not have to scare the markets by telegraphing bearish actions in advance. From an eagle’s perspective, soaring above the bulls and bears, we will continue to closely follow inflation data and try to ascertain how it will affect Fed policy. Powell is clear that fighting inflation is the Fed’s number one goal. Policy and liquidity will shift with inflation data. Ultimately, it is liquidity that drives the markets. The graph below shows market expectations for Fed Funds are below those of Fed members.

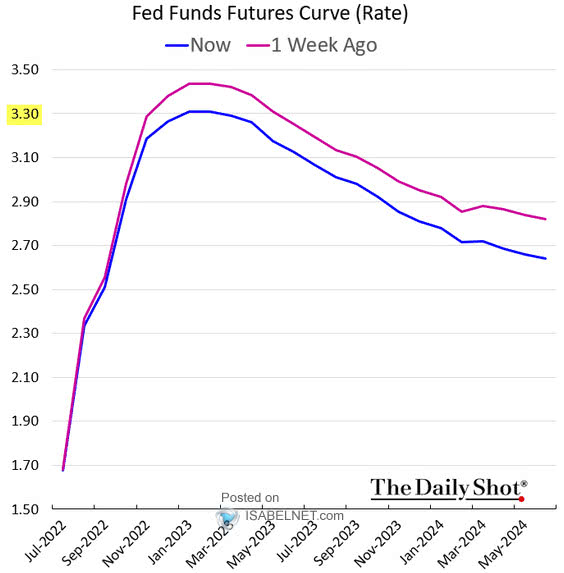

2023 Pivot

The graph below shows the market expects Fed Funds to rise another 1% through this year and then to start falling. After getting rates up 3.30%, Fed Funds futures imply the Fed will lower rates by 25 basis points by May 2023. We think a peak in the 3.00-3.50% range is very reasonable. However, the big question is, what’s next? The market is pricing in a very short “stall.” It thinks the Fed goes from tightening to easing, albeit at a slow pace. Barring a sharp increase in unemployment, deepening recession, or financial instability, a longer stall period should be expected. The Fed is making it clear they want inflation back to 2%. Late this year and early next year, inflation will likely still be well above 5%. The Fed does not want to rekindle inflation too soon with easy monetary policy.

The second graph helps provide historical context to what we might expect. Of the last three recessions, the Fed stalled for at least six months. Inflation, however, was not an issue in those three instances.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read