Moody’s, the last of the three major credit rating agencies to have an AAA rating on the United States government, put Uncle Sam on credit watch negative. The AAA rating is still intact. But, Moody’s warns investors and the Treasury Department that a rating downgrade to AA is probable unless serious budgetary steps are taken to limit debt issuance. However, and this is important, they add “in the context of higher interest rates” in their rationale. Will Moody’s remove their negative outlook if rates decline toward pre-pandemic levels? Might lower rates persuade S&P and Fitch to consider rating upgrades or put them on positive watch?

“In the context of higher interest rates, without effective fiscal policy measures to reduce government spending or increase revenues, Moody’s expects that the US’ fiscal deficits will remain very large, significantly weakening debt affordability.” – Moody’s

Our thoughts: We believe Moody’s warning and downgrades from other rating agencies have a near-zero impact. A credit rating on an entity that can print its own money and presides over the world’s reserve currency is meaningless. In a way, the rating agencies acknowledge this. To explain, consider what the rating would be if the government were a private entity. As we wrote in Risk-Free Government Debt: “When Fitch calculates the credit rating for a company, it uses the debt service coverage ratio (DSCR), among other fundamental measures of debt, assets, and liquidity…. As shown, the government’s DSCR would land it firmly in junk bond territory between a B and CCC rating.“ The agencies currently rate USA debt on par with the most fiscally sound companies and sovereign nations.

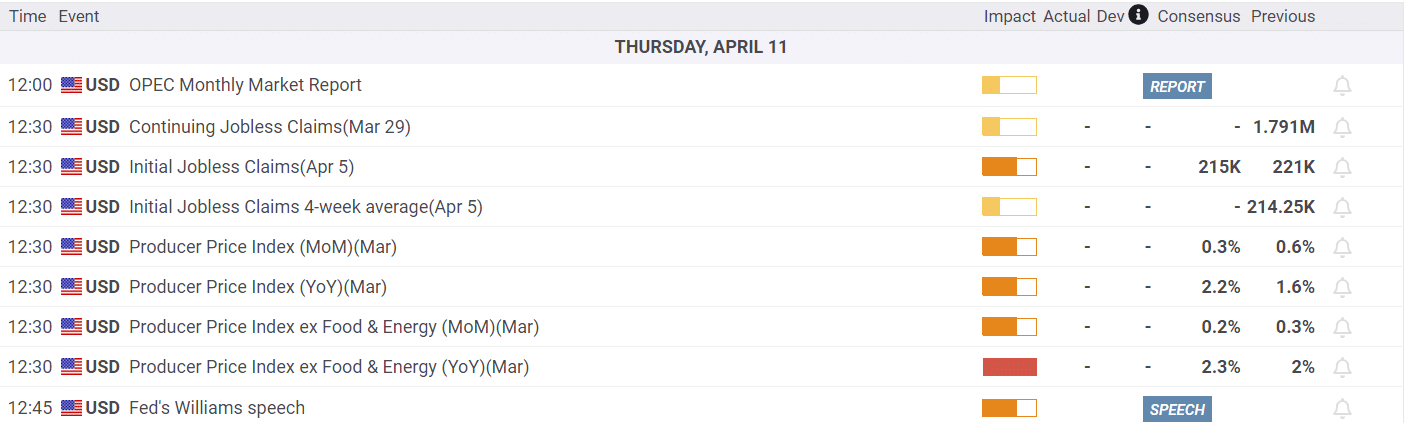

What To Watch Today

Earnings

Economy

Market Trading Update

Yesterday, the market retested the breakout of the previous downtrend line resistance from the July highs. With the market turning that previous resistance into support, it further solidifies the bullish tone the market has taken since the beginning of July. Much like October of 2022, the bottom of that selloff was marked by the technical thrust higher beginning in November. While the current selloff was more protracted than that of 2022, the difference this time is the market is trading above the 200-DMA with only minor resistance at 4500. However, looking back at last year, the advance higher was not a straight line. We should expect some pockets of weakness along the way, particularly in mid-December. Continue to use weakness to add exposure to portfolios for now.

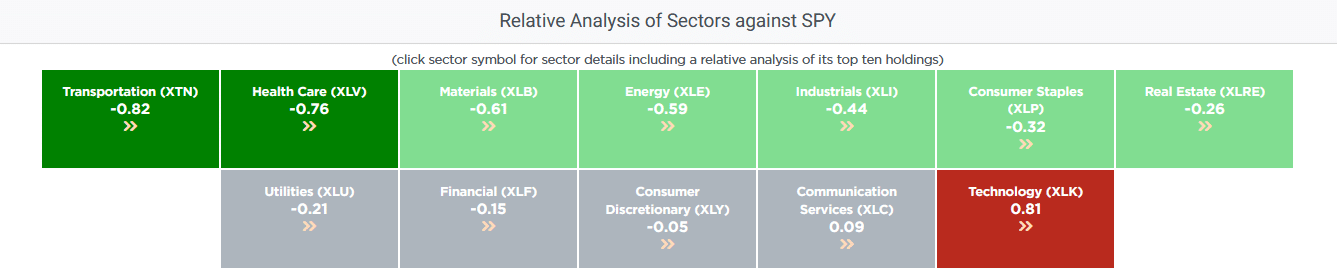

Technology Leads The Market Once Again

The first table below comes courtesy of SimpleVisor. The sector scores quantify how each sector measures against the S&P 500 on a technical basis. Red, as technology currently is, is extremely overbought, while green denotes oversold conditions. As shown, technology is grossly overbought, while all sectors are flat or negative versus the S&P 500. Such a stark difference between technology and just about everything else reminds us of the outperformance of the energy sector in 2022.

Next, the heat map below shows the performance of each of the S&P 500 stocks and their year-to-date gain. The size of each square is a function of each company’s market cap. Except for technology, Google, Meta, Amazon, and Tesla, you notice a majority of the market is having a bad year.

CPI This Morning

With markets eagerly following every last word from the Fed and the Fed nearly solely focused on inflation, today’s CPI could be a significant number for the markets. The table below shows what Wall Street forecasters expect the headline and core indexes to be. If the number exceeds estimates, stocks and bonds will likely sell off in unison. Conversely, a weaker-than-expected number, along with the recent slowing of the labor market, could easily cause the stock and bond markets to rally significantly.

Future Inflation Expectations & Bonds

The following table is worth considering. Inflation expectations of two major Wall Street firms are close to the Fed’s 2% objective. Given expectations are at or near 2%, it is surprising to see bonds yielding 4.75%-5.25%, based on the fact that interest rates hovered around inflation rates before the pandemic. The market is either betting that inflation will stay stubbornly high or that Treasury debt issuance will weigh heavily on the market. Regarding the second point, its worth noting the government’s debt-to-GDP ratio has actually declined since peaking in 2021.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.