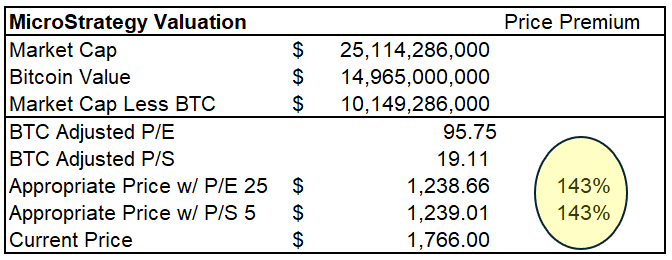

Microstrategy (MSTR) provides its customers with business intelligence, mobile software, and cloud-based services. Despite losing money and zero growth in revenues over the last ten years, investors can’t seem to buy enough of MicroStrategy. The rationale is not based on prospects for their core technology businesses but on their massive accumulation of Bitcoin since 2020. For many investors, MicroStrategy is a Bitcoin surrogate. Instead of dealing with crypto exchanges and the potential of losing your key, Bitcoin investors flocked to the ease of owning MicroStrategy stock. On the surface, the trade makes sense. However, with the advent of Bitcoin ETFs, it’s worth appreciating what MicroStrategy investors are truly buying.

We constructed the table below to show how MicroStrategy investors are paying a 43% premium to own Bitcoin. To quantify that, we stripped the value of its Bitcoin holdings from its market cap, leaving us with a market cap for the true technology company. With that adjustment, MicroStrategy trades with a P/E of 95 and a P/S of 19. If we assume it should trade with a P/E of 25 and P/S of 5, the stock, including the value of its Bitcoin, should be 1238, well below the current price of 1766. More concerning, the valuation ratios we assume below are high, considering the company has exhibited zero growth in ten years. Further, we use their highest level of earnings and sales for the calculation, not the lower current figures. Accordingly, the real Bitcoin premium is likely well north of our estimate.

What To Watch Today

Earnings

Economy

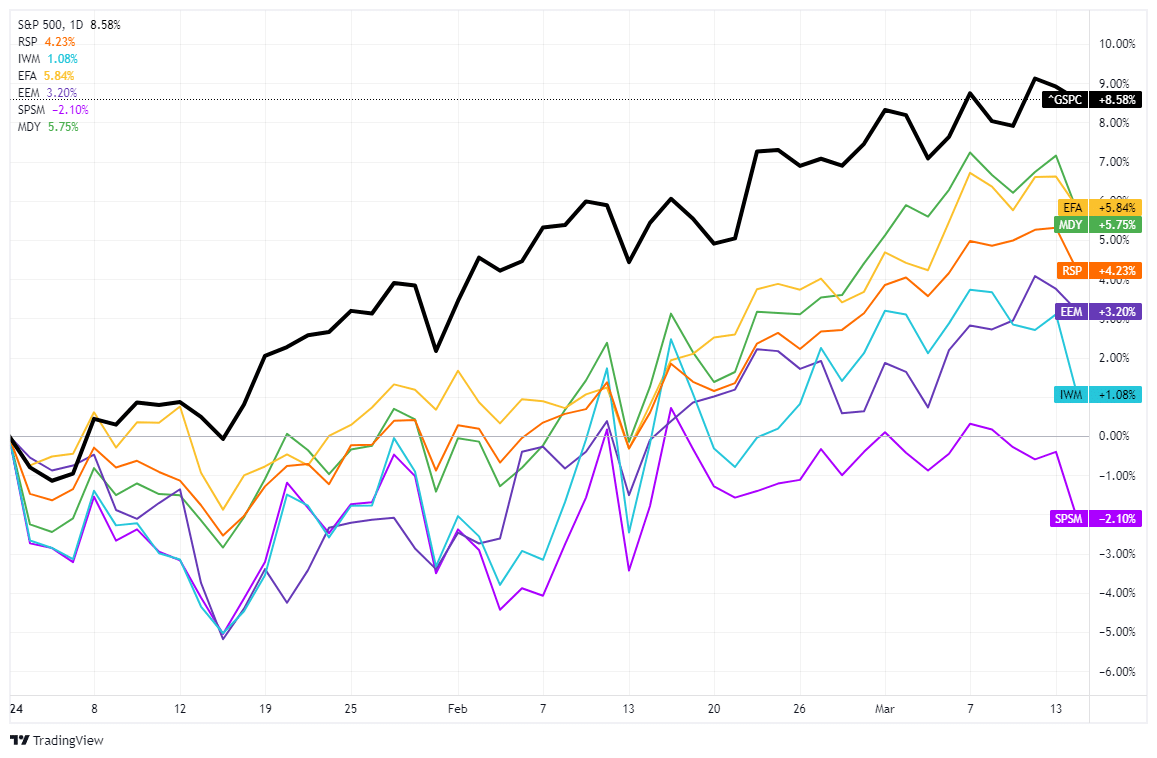

Market Trading Update

As discussed yesterday, the market’s momentum continues to wane, particularly in small capitalization companies. While the S&P 500 is up 8.58% YTD, small caps are negative for the year. While mid-capitalization and international stocks caught a bid this year, they still lag the S&P by a wide margin. Such is particularly the case with both emerging markets and the Russell 2000.

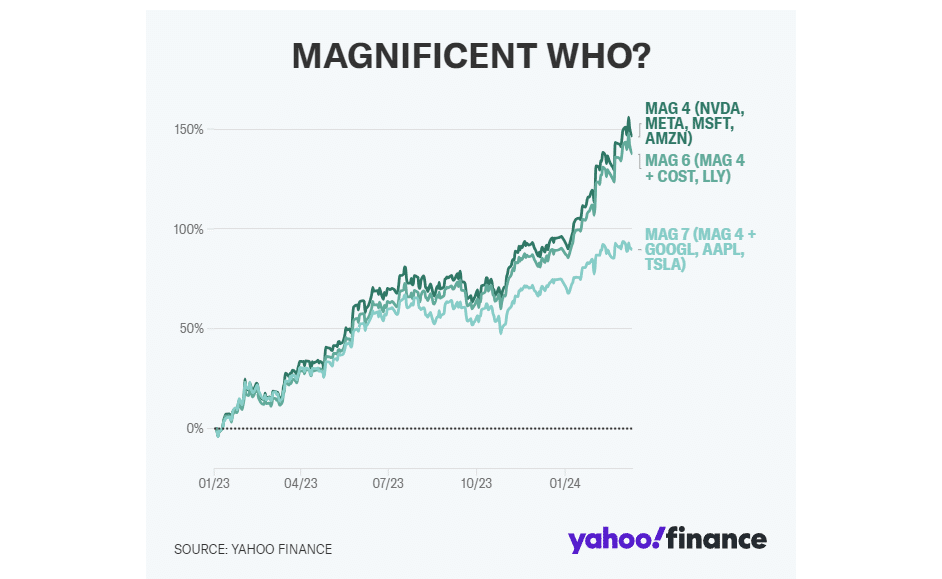

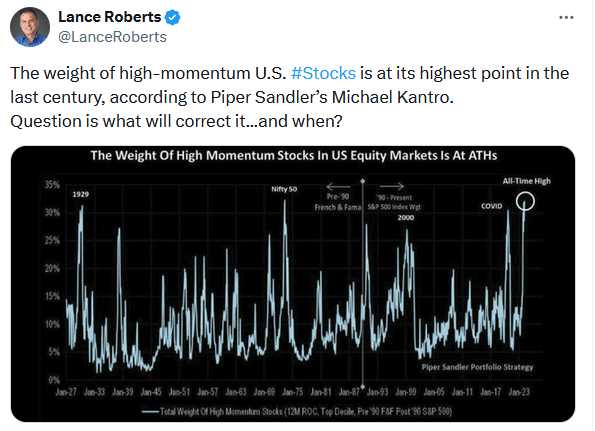

For investors, it remains a chase for a handful of momentum stocks that have surged this year. As noted by YahooFinance yesterday, it has been a rotation in the “Magnificent 7” from the original to the new breed. To wit:

“Taking out the three clear laggards — Tesla, Apple, and Alphabet — improves the returns of the Magnificent Seven over the longer term. And as a purely intellectual exercise, Yahoo Finance’s Head of News, Myles Udland, reshuffled the Magnificent deck. He’s keeping the Mag Four outperformers, losing the three laggards, and adding a couple “diversified” stocks — Costco (COST) and Eli Lilly (LLY) — to the list.”

The point here is that the market is still being primarily driven by a handful of large-capitalization names while the rest of the market lags. While such doesn’t mean that you can’t make money in other areas of the market, the narrowness of the breadth continues to remain a concern, along with the more extreme concentration of market-capitalization-weighted stocks in the index.

While none of this means that the market will crash any time soon, historically, it does suggest lower future returns as markets eventually correct its imbalances.

Retail Sales and PPI

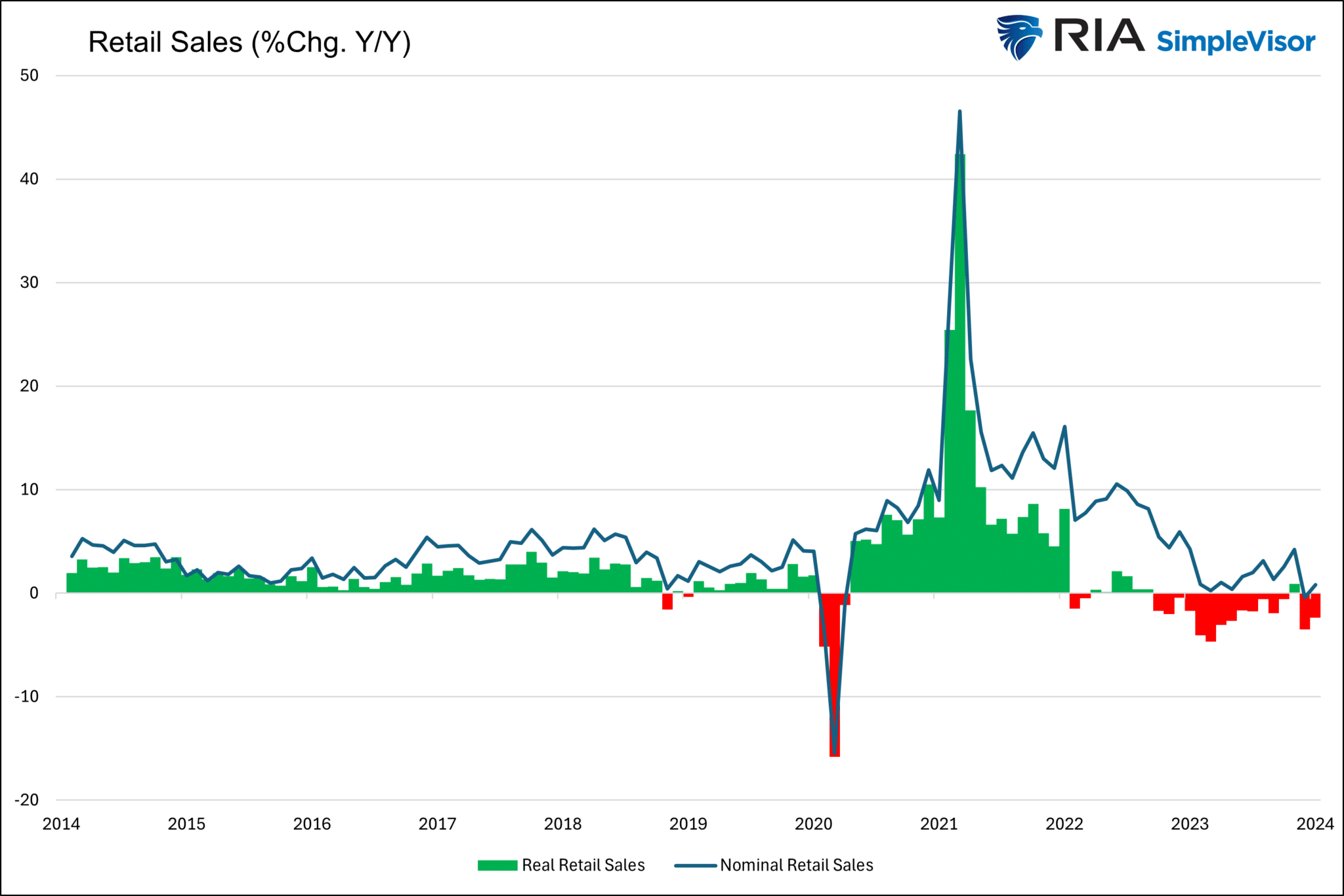

Retail Sales were a little weaker than expected. Monthly sales in February grew by +0.6%, worse than the +0.8% consensus and much better than last month’s -1.1 %. The control group, which feeds GDP, was zero, compared to -0.3 % last month. The graph below, courtesy of Charlie Bilello, shows that both retail sales and real retail sales are moderately below their historical averages.

PPI, like CPI, was a little hotter than expected. Headline PPI rose 0.6% last month, well above estimates of +0.3%. However, the core PPI was only 0.1% above expectations at +0.3%. On a year-over-year basis, the headline PPI is running at 1.6%, and the core PPI is at 2%.

Approximately a third of the increase in the PPI was driven by a 6.8% increase in gasoline prices. Such is not likely to be repeated next month, so the calls for a re-acceleration of PPI based on yesterday’s data will likely prove misleading.

More On Coming Liquidity Shortages

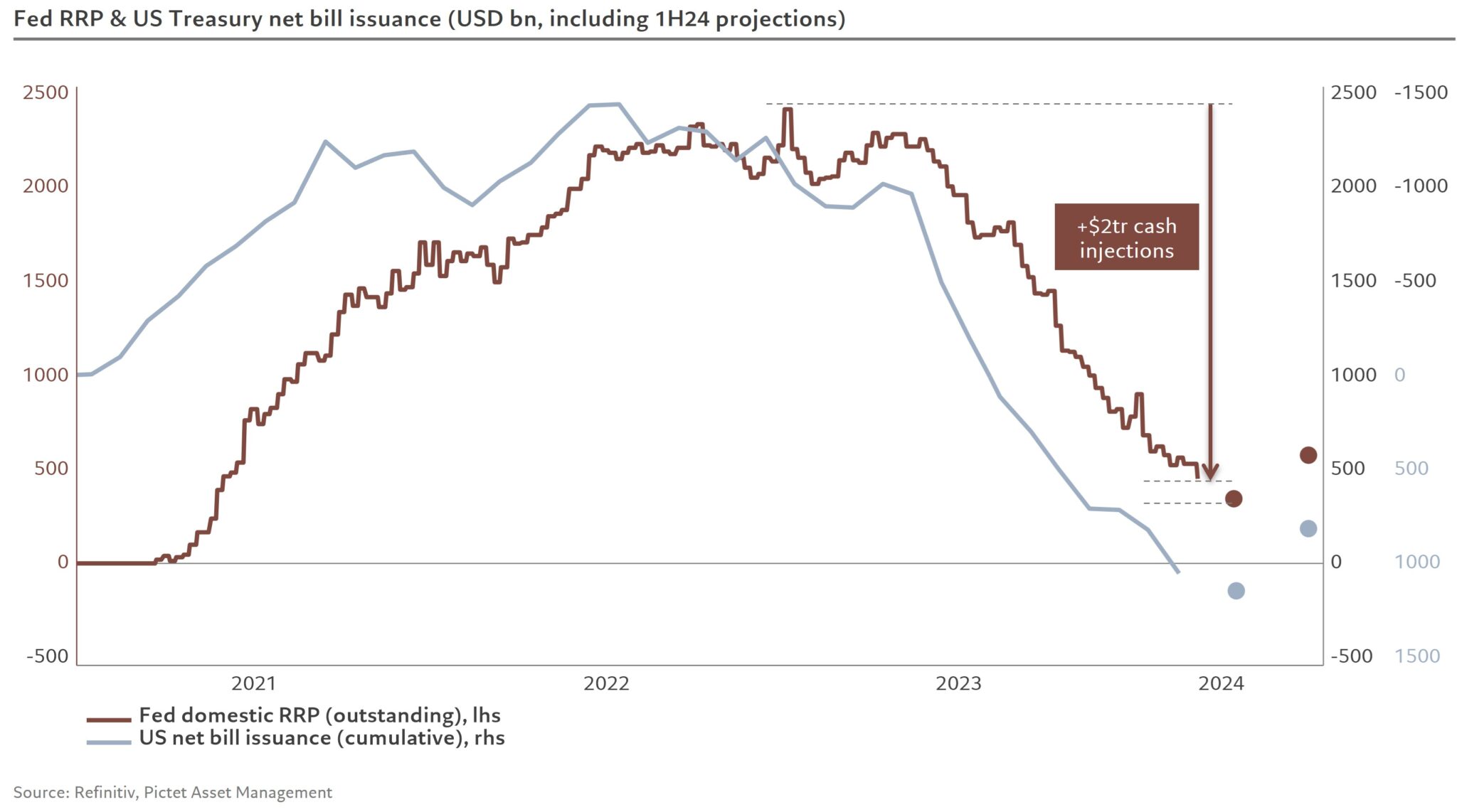

Last week, we wrote Liquidity Problems Are Closer Than You Think, which warns that the excess liquidity in the financial system is quickly waning. We highlighted the Fed’s reverse repurchase program (RRP) as it serves as a good gauge for the amount of excess liquidity. The graph below, courtesy of Pictet Asset Management, adds to our analysis. The blue line represents net T-bill issuance. Its y-axis to the far right is inverted to make it easily comparable to RRP balances (red). Net T-bill issuance in late 2020 and throughout 2021 turned negative. At that time, the massive T-bill issuance in early 2020 was maturing and not being fully replaced as deficits declined. As the amount of T-bills outstanding declined, money market investors needed an investment replacement. Accordingly, they invested in RRP. Please read our article for more about RRP and why the Fed offers it.

Since late 2022, net T-bill issuance has been increasing. Consequently, money market investors are, in the aggregate, buying T-bills and exiting RRP trades. Once RRP balances are negligible, the Treasury will draw liquidity from the financial system. The dots show that net Treasury funding needs may decline in the coming months. That is solely a function of incoming tax revenue. However, looking past April, net issuance will increase and likely bring RRP balances to near zero. Barring changes in Fed policy, that is when liquidity problems are most likely to surface.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.