Market fears subsided a bit over the past couple of days as Powell testified before Congress. While Powell believes a recession is not a major risk, other indicators and even the NY Fed disagree. However, Powell said the central bank is open to raising rates again as it works to slow inflation, but he added that the pace of hikes would depend on how quickly inflation starts to decline, based on “the incoming data and the evolving outlook for the economy.”

In recent months, the Fed has accelerated the pace of its interest rate increases, starting with a quarter-point hike in March and a half-point increase in May. That was followed by last week’s bump of three-quarters of a percentage point—the biggest hike in nearly three decades. Such also sparked market fears that a recession would impact growth.

However, those fears somewhat abated when Powell reassured senators the economy was on strong footing and offered optimism about the future.

We are not so sure that is the case.

What To Watch Today

Economy

- University of Michigan Sentiment, June final (50.2 expected, 50.2 prior)

- University of Michigan 1-Year Inflation, June final (5.4% expected, 5.4% prior)

- University of Michigan 5-10-Year Inflation, June final (3.3% expected, 3.3% prior)

- New Home Sales, May (590,000 expected, 591,000 prior)

- New Home Sales, month-over-month, May (-0.2% expected, -16.6% prior)

Earnings

Pre-market

CarMax (KMX) to report adjusted earnings of $1.53 on revenue of $9.05 billion

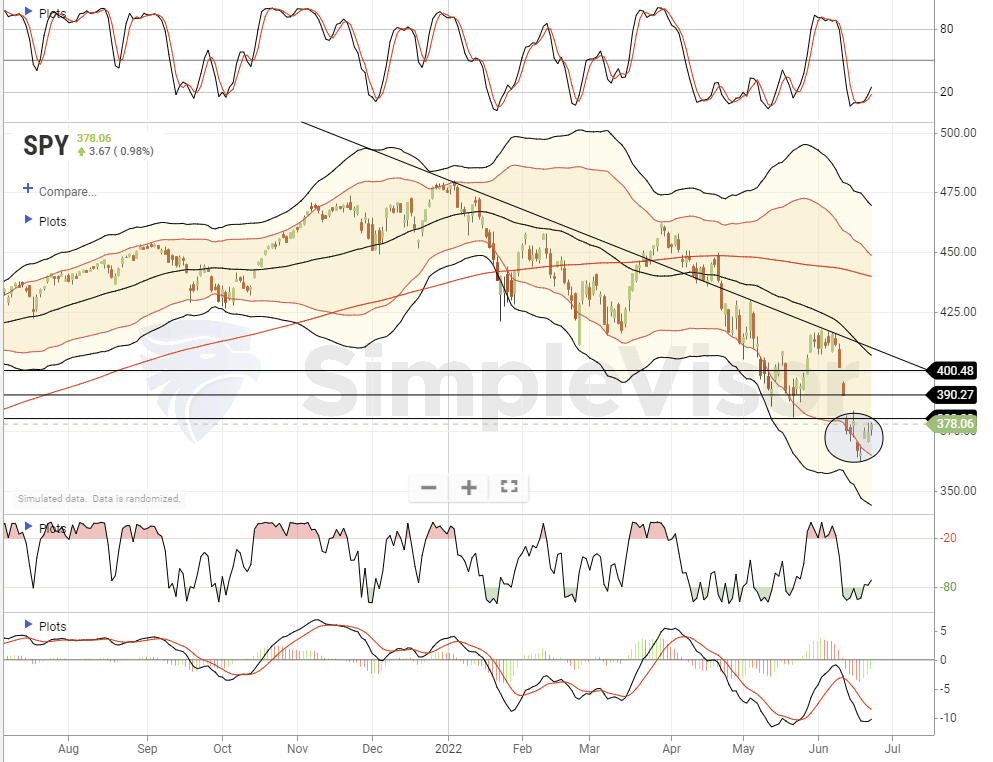

Market Trading Update – Rally On Garth

While market action has been very sloppy as of late, it is rallying off of the recent lows from last week.

That’s the good news.

The not-so-good news is that there are several levels of heavy resistance just ahead with the first level getting tested tomorrow. That level is the top where stock prices opened after they gapped down following the Fed rate hike. The second and third levels are the bottoms of each of the waterfall declines that intersect with the tops and bottoms of the previous minor consolidation.

These levels should be used to raise cash and rebalance risk accordingly for now. If we begin to see stronger action in the market that suggests a bottom is forming, we will start an accumulation strategy. However, that is not now.

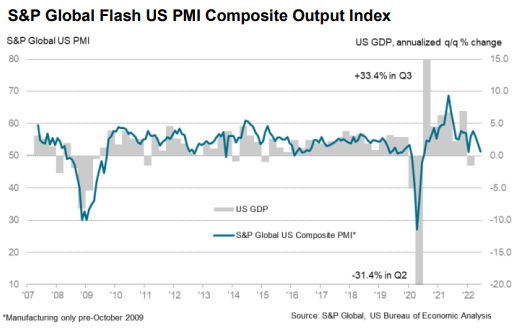

US Flash PMI Sends Warning Signal

The S&P Global Flash US Composite PMI sank to a level of 51.2 in June from 53.6 in May. The preliminary estimate was the weakest in five months and signals a significant slowdown in the expansion rate of US business activity. The Flash Services PMI fell to 51.6 in June from 53.4 in May (5-month low), and the Flash Manufacturing PMI fell to 52.4 in June from 57.0 in May (23-month low). While services output continued growing, both new orders and manufacturing output decreased for the first time in two years.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence commented:

“The pace of US economic growth has slowed sharply in June, with deteriorating forward-looking indicators setting the scene for an economic contraction in the third quarter. The survey data are consistent with the economy expanding at an annualized rate of less than 1% in June, with the goods-producing sector already in decline and the vast service sector slowing sharply.”

The report stoked growth fears in the bond market, causing yields to fall for the second straight trading session. Equity markets stumbled but ultimately finished higher.

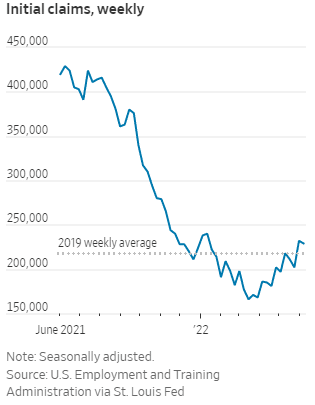

Jobless Claims Remain Subdued

Jobless claims for the week ended June 18th were 229k versus a consensus of 227k and a prior reading of 231k. Results were essentially in line with expectations, and although hovering at a five-month high, initial claims remain at unalarming levels. Tightness in the labor market persists despite increasing chatter about layoff plans.

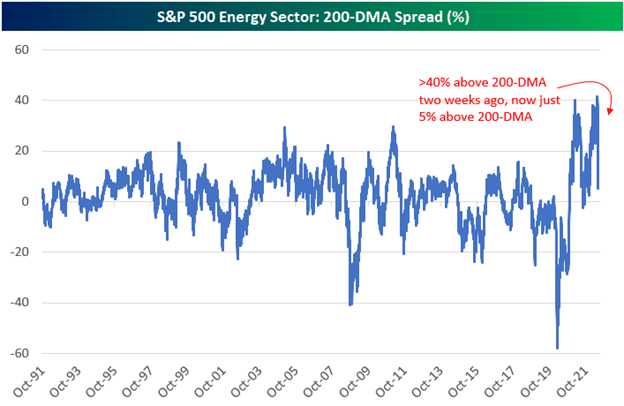

Energy Stocks are Correcting Hard and Fast

Energy stocks are taking a break from their insane rally this year as the price of crude oil pulls back. The charts below from Bespoke help put the gravity of the correction into perspective. This is the third worst two-week change for the S&P 500 energy sector in the last 40+ years. Even after the correction, the price of XLE is still up 30% YTD.

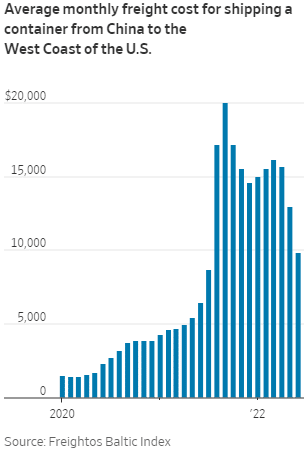

China to US Shipping Rates Find Some Relief

Stockpiles of excess inventory at US retailers such as Target (TGT) have led to order cuts in recent months. The cooling of demand is now flowing through to shipping rates, which should offer marginal relief to US wholesalers and retailers. Freight rates from China to the US are down 34% YTD and 50% YoY according to Freightos Baltic Index.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.