Senator Manchin and Omicron and bears are weighing on investor sentiment heading into the holiday-shortened week. Sen. Manchin told Fox News Sunday evening that he cannot get behind the democrats’ Build Back Better legislation. Soon thereafter, Goldman Sachs downgraded its GDP forecast for the first quarter of 2022. Meanwhile, the accelerating spread of Omicron and response measures adopted across Europe have sparked further concerns surrounding demand.

Stocks closed lower on Monday with the best sector performances from Staples and Utilities, respectively. Bonds finished slightly higher, while crude fell on demand concerns as Omicron continues spreading. It appears as if Senator Manchin and Omicron might possibly take the wind out of Santa’s rally.

What To Watch Today

Economy

- 8:30 a.m. ET: Current Account Balance, Q3 (-$205 billion expected, -$190.3 billion in Q2)

Earnings

Pre-market

- 6:30 a.m. ET: Apogee Enterprises (APOG) to report adjusted earnings of $0.54 on revenue of $317.7 million

- 7:00 a.m. ET: General Mills Inc (GIS) to report adjusted earnings of $1.05 on revenue of $4.8 billion

- 7:00 a.m. ET: Rite Aid Corp (RAD) to report adjusted losses of $0.10 on revenue of $6.4 billion

Post-market

- 5:05 p.m. ET: BlackBerry Limited (BB) to report adjusted losses of -$0.07 on revenue of $176.8 million

Quote of the Day

“Inflation is just like alcoholism. The good effects come first.” – Milton Friedman

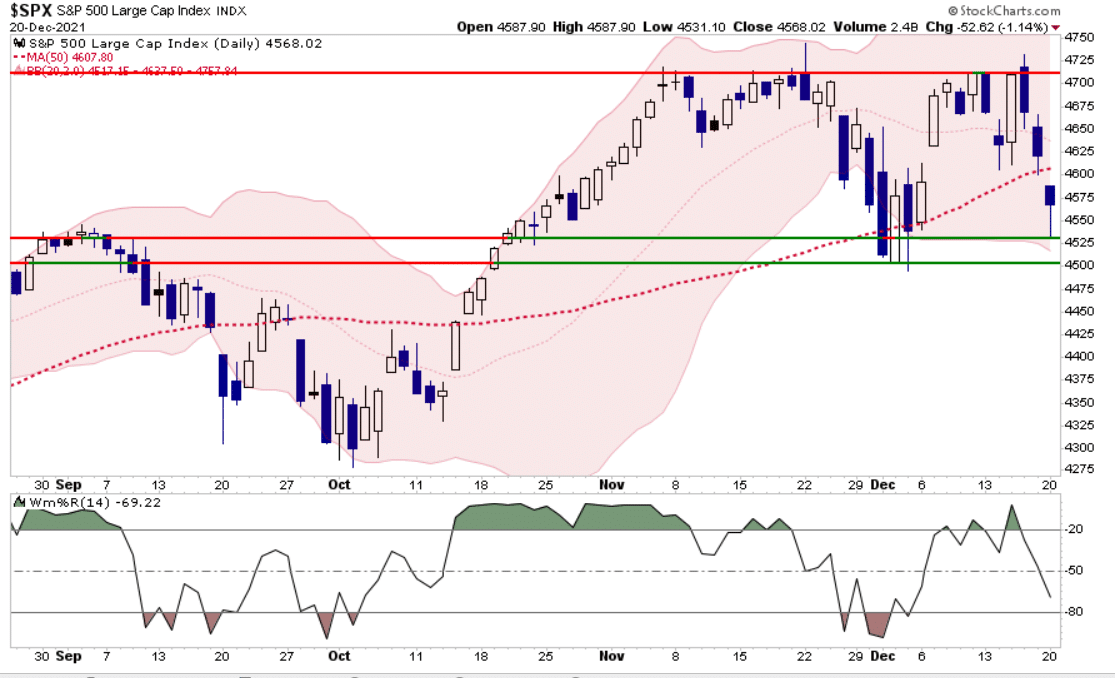

Market Bounces Off Of Support – Can The Santa Rally Finally Start

It’s been a rough 3-trading days since the market hit all-time highs, however, futures are pointing higher this morning. Yes, despite all of the teeth-gnashing and screams for the “selling to stop,” the market remains well confined to a consolidation pattern currently. Yesterday, the market held support at the September highs.

While we could see some additional selling this week as concerns over Manchin, the BBB, and Omicron continue to flood the media. Furthermore, the market is not entirely oversold just yet. However, we will see a counter-trend rally that can be used to rebalance equity risk at better prices.

As I noted in early November, I still think we have probably seen the highs for 2021. A rally between now and year-end would likely push stock prices back towards those highs. However, a failure of support at 4500-4525, and it is likely we will markets a good bit lower in short-order.

Maintain your risk controls. Most importantly, don’t let emotions during light trading, low liquidity, markets drive you to make investment mistakes. Those are the ones we always tend to regret the most.

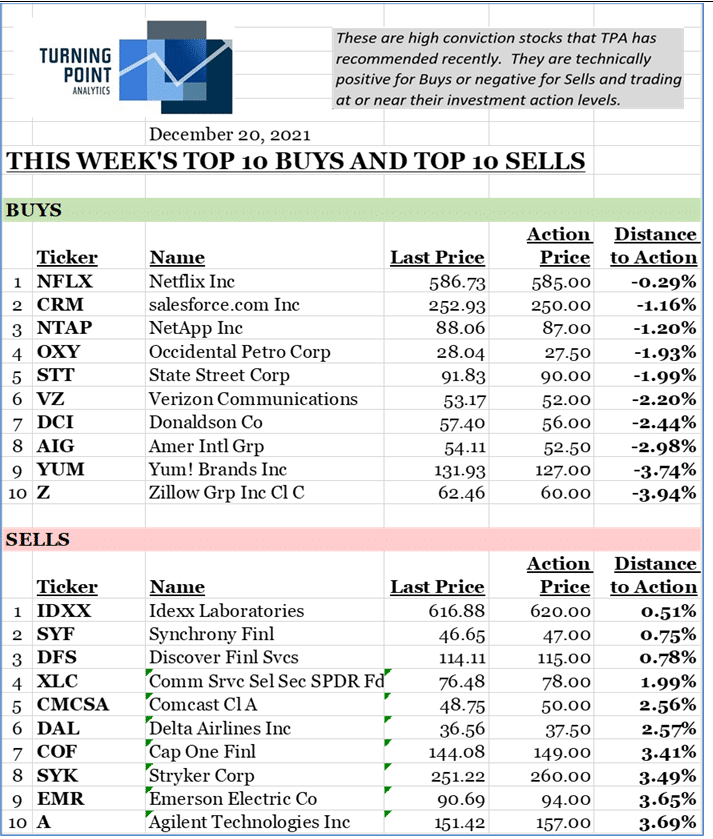

This Week’s TPA Top-10 Buys And Sells

Click on RIAPro+ today to add TPA Research to your subscription for just $20/month.

What’s up With Turkey?

A few readers have asked us for a summary of Turkey’s financial debacle, so here it goes: In case you are unaware, inflation in Turkey is running over 100% a year, in part because its currency, the Lira, is plummeting. In September, it took approximately 8 Lira to exchange for a dollar. Today it takes over 17. Money is fleeing the country as savers/investors protect from Lira depreciation, making a bad problem worse. Adding insult to injury, President Erdogan is fighting conventional wisdom and cutting interest rates. His actions are inflaming inflation and crushing its currency.

A few key points:

- In late November Erdogan cut interest rates from 19% to 15% despite surging inflation. They are now 14%. As a result of lower rates and higher inflation, real interest rates in Turkey are collapsing. There is no financial incentive to hold onto Lira. Turkish stocks are at 16-year lows and down 80% from their 2013 highs.

- The Fed has begun tapering and a few emerging market central bankers are hiking rates. Brazil for instance has hiked 6 times for a total of 2%. Higher interest rates incentivize emerging market investors to shift funds from Turkey to countries like Brazil. This leads to further outflow of money from Turkey.

- Typically a country in Turkey’s shoes would use currency reserves, like U.S. dollars or euro, to support their currency. They do not have a lot of reserves. It’s also not obvious they will get help from other countries. In fact, they have been threatening Greece, Syria, and Iraq. Its also unlikely Erdogan would accept an IMF bailout.

Turkey is likely to collapse financially and possibly politically. Making this situation more complex is their geopolitical role as intermediary between the east and west and between Islamism and Christianity. A further decline in Turkey’s position could weigh on global markets in the days, weeks, and months ahead.

Stuffing Your Stockings With MLPs

In our latest SimpleVisor blog- Five MLP Stocks to Stuff the Stockings – we scanned through the MLP sector to provide subscribers with five MLP stocks that offer value. Per the article:

“Recently, MLP stocks have traded poorly, offering patient investors more dividend yield and value than is typical. Since peaking in January 2020, AMLP, an ETF holding MLPs, is down 10%. Over the same period, the popular energy ETF XLE is up 3%.”

For a little more context on how MLPs are trading versus energy stocks and the price of crude oil, consider the graph below. The blue line shows the price ratio of AMLP to XLE is at the bottom end of its five-year trading range. AMLP only holds MLPs, while XLE broadly holds all types of energy stocks. The orange line is the price ratio of AMLP to crude oil. It is also near the bottom of its five-year trading range. The MLPs we highlight in the report have relatively low valuations and tend to pay high dividend yields. That said, recent returns have generally been poor.

MLP’s follow different investor tax guidelines, therefore do your own research before investing.

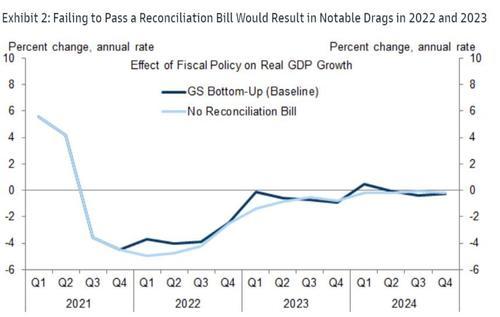

GDP Estimates Cut as BBB Falters

Senator Joe Manchin single handily squashed the Democrat’s $2 trillion Build Back Better social infrastructure plan. In response, Goldman Sachs quickly reduced its GDP forecast for Q1 2022 from 3% to 2%. They also lowered the remaining quarters’ expectations throughout the year ahead. Expected fiscal spending for 2022, while robust relative to pre-Covid levels, will be sharply reduced from 2020 and 2021 spending levels and thus create a drag on the economy.

The rising threat of the Omicron variant and varying degrees of lockdowns and more conservative consumer behavior may further harm economic activity in the first quarter. We remind you this comes as the Fed is reducing QE and talking about raising interest rates as early as March. If markets continue to trade poorly, will Senator Manchin and Omicron cause the Fed to back off on their recent hawkish pivot?

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

Also Read