I want to discuss a recent WallStreet Journal article by Ruchir Sharma entitled “The Rescues Ruining Capitalism.”

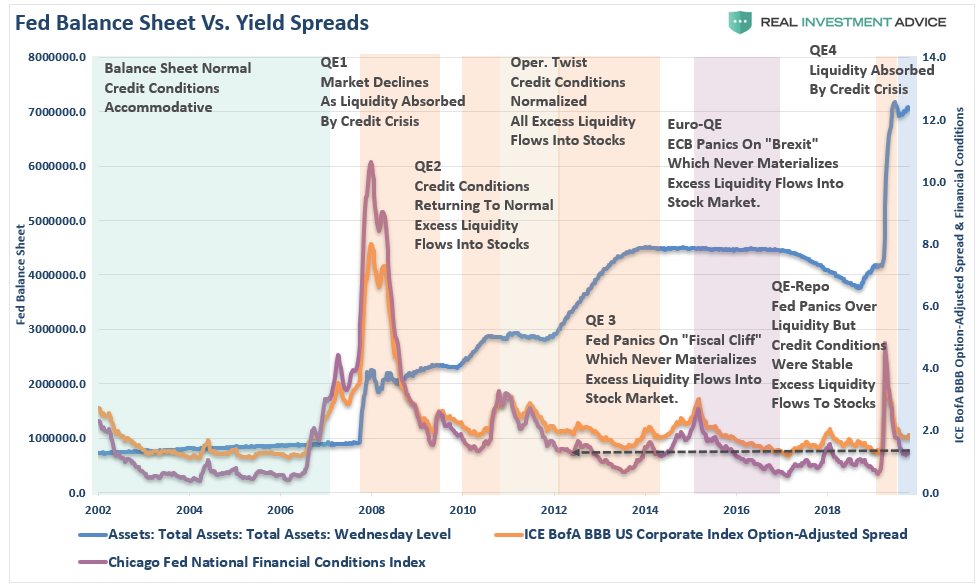

We talk much about the bailouts and stimulus programs related to the economic shutdown and pandemic. However, the bailouts began back in 2008 when the Federal Reserve intervened with the insolvency of Bear Stearns.

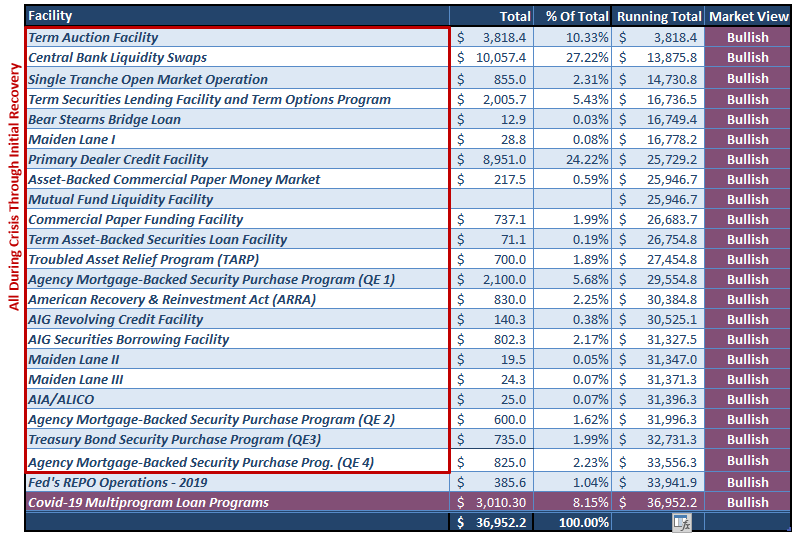

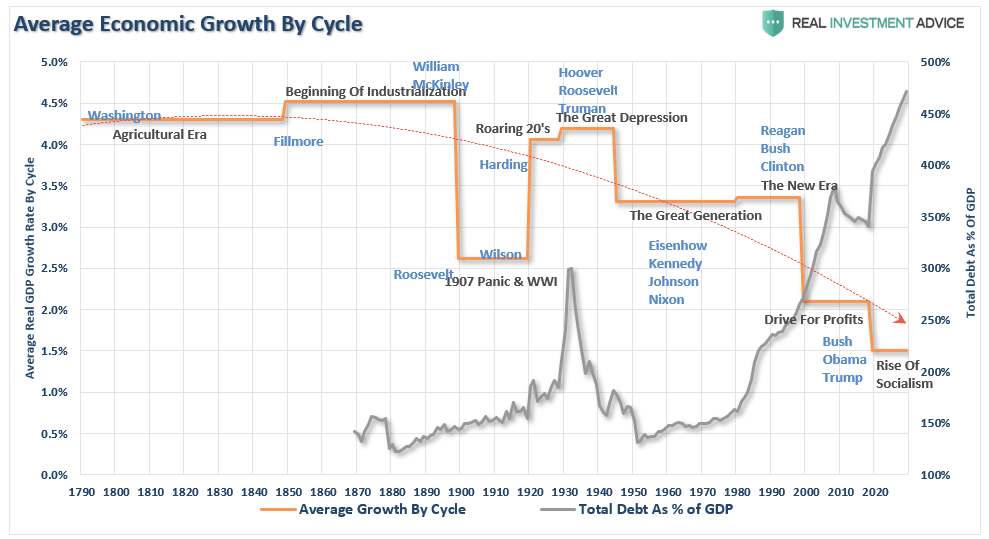

To date, the Federal Reserve, and the Government, have pumped more than $36 Trillion into the economy to keep it “afloat.”

I say “afloat” rather than “growing” because, during the last decade, economic “growth” was a function of population growth. Monetary interventions were successful in creating inflation in financial assets. However, during the same period, the economy grew by only $2.92 Trillion.

In other words, for each dollar of economic growth since 2008, it required $12.67 of monetary stimulus. Such sounds okay until you realize it came solely from debt issuance.

Bailouts Ruining Capitalism

We need that bit of history to understand why “bailouts are ruining capitalism.”

“Modern society looks increasingly to government for protection from major crises. Whether recessions, public-health disasters or, as today, a painful combination of both. Such rescues have their place. Few would deny that the Covid-19 pandemic called for dramatic intervention. But there is a downside to this reflex to intervene, which has become more automatic over the past four decades. Our growing intolerance for economic risk and loss is undermining the natural resilience of capitalism and now threatens its very survival.” – Sharma

Sharma is correct.

Such was a point I recently discussed in “Recessions Are A Good Thing.” To wit:

“Just as poor forest management leads to more wildfires, not allowing ‘creative destruction’ to occur in the economy leads to a financial system that is more prone to crises.

Given the structural fragility of the global economic and financial system, policymakers remain trapped in the process of trying to prevent recessions from occurring due to the extreme debt levels. Unfortunately, such one-sided thinking ultimately leads to skewed preferences and policymaking.

As such, the “boom and bust” cycles will continue to occur more frequently at the cost of increasing debt, more money printing, and increasing financial market instability.”

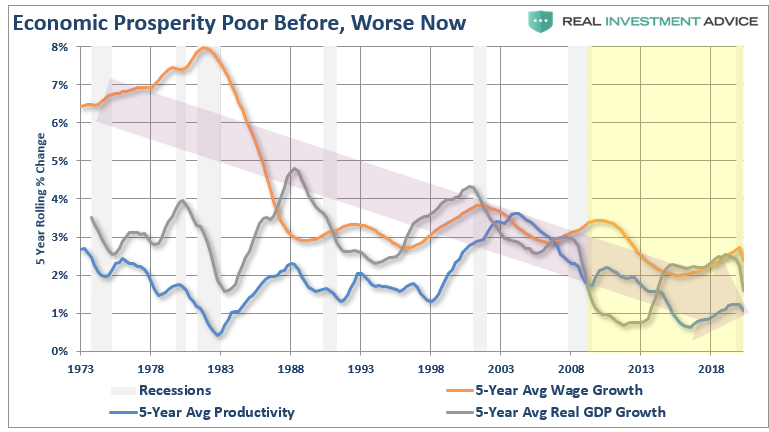

The Fed’s foray into “policy flexibility” did extend the business cycle longer than normal. However, those extensions led to higher structural budget deficits. The byproduct was increased private and public debt, artificially low interest rates, negative real yields, and inflated financial asset valuations.

Specifically to Sharma’s point:

“However, these policies have all but failed to this point. From ‘cash for clunkers’ to ‘Quantitative Easing,’ economic prosperity worsened. Pulling forward future consumption, or inflating asset markets, exacerbated an artificial wealth effect. Such led to decreased savings rather than productive investments.”

The Fed’s “Moral Hazard”

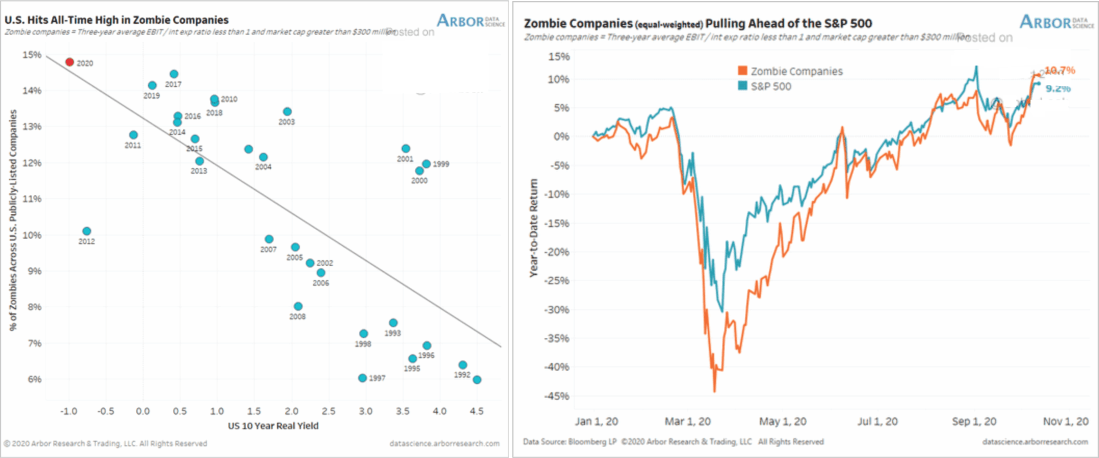

“This is a dangerous form of denial. A growing body of research shows that constant government stimulus has been a major contributor to many of modern capitalism’s most glaring ills. Easy money fuels the rise of giant firms and, along with crisis bailouts, keeps alive heavily indebted “zombie” firms at the expense of startups, which typically drive innovation. All of this leads to low productivity—the prime contributor to the slowdown in economic growth and a shrinking of the pie for everyone.” – Sharma

By not allowing “recessions” to perform their natural “Darwinian” function of “weeding out the weak,” to Sharma’s point:

“Zombies’ are firms whose debt servicing costs are higher than their profits but are kept alive by relentless borrowing.

Such is a macroeconomic problem. Zombie firms are less productive, and their existence lowers investment in, and employment at, more productive firms. In short, a side effect of central banks keeping rates low for a long time is it keeps unproductive firms alive. Ultimately, that lowers the long-run growth rate of the economy.” – Axios

If capitalism were allowed to function, the weak players would fail. Stronger market players would acquire failed company assets. Bond-holders would receive some compensation for their debt holdings. Shareholders, the ones who accepted the most risk, would get wiped out.

Furthermore, assuming capitalism was allowed to function, investors would require appropriate compensation for the risk when loaning money to companies. Such would provide higher returns to credit-related investors rather than the current state of abnormally low yields for junk-rated debt.

Why is this currently the case? It is the direct result of the Fed’s creation of “moral hazard.” The definition of which is:

“A lack of incentive to guard against risk as investors believe the Fed is protecting them from the consequences of it.”

The Stock Market Is Not The Economy

“At the same time, easy money has juiced up the value of stocks, bonds and other financial assets, which benefits mainly the rich, inflaming social resentment over growing inequalities in income and wealth. It should not be surprising that millennials and Gen Z are growing disillusioned with this distorted form of capitalism and say that they prefer socialism. The irony is that the rising culture of government dependence is, in fact, a form of socialism—for the rich and powerful.” – Sharma

Sharma’s statement is incredibly important. If you are a Millenial or Gen Z’er and are voting for more socialistic policies, you are doing economic harm to yourself. A commonality of all socialistic countries is a very significant division between the top 10% and the bottom 90%. Under socialism, wealth and opportunity get concentrated at the top, with little remaining for everyone else.

In America, if you make $30,000/year, you are in the lower-income levels of the economy and barely above poverty levels. However, compared to the rest of the world, you are in the top 1% of income earners.

Capitalism creates opportunities. Socialism destroys it by removing the incentives to innovate and produce. Throughout history, the correlation between the economy, earnings, and asset prices over time are high.

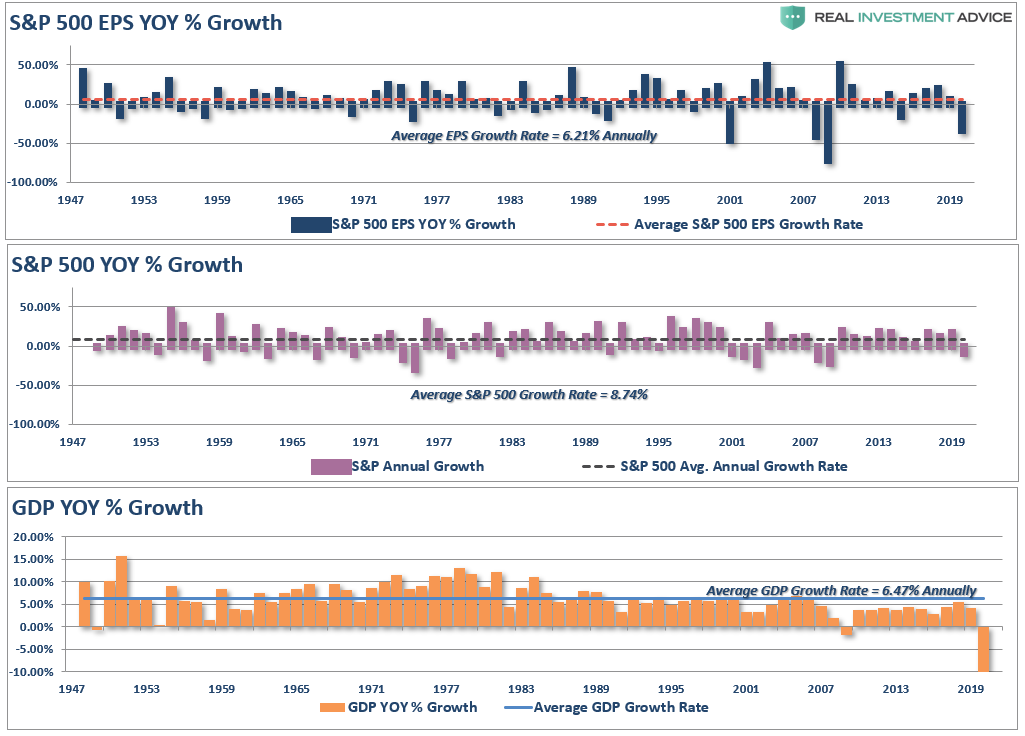

Since 1947, earnings per share have grown at 6.21% annually, while the economy expanded by 6.47% annually. That close relationship in growth rates should be logical, particularly given the significant role consumer spending has in the GDP equation.

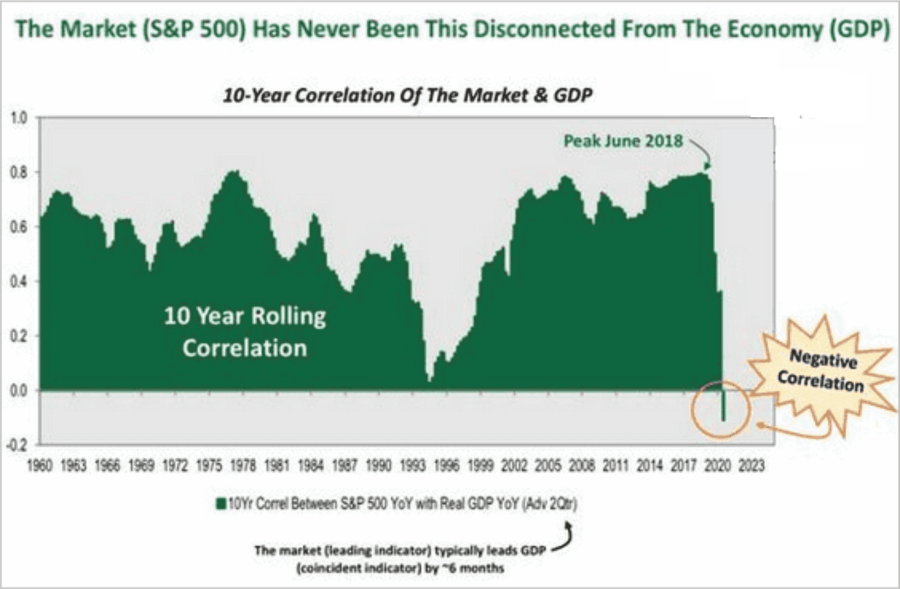

The current “negative correlation” is quite an anomaly given that corporate earnings are the result of economic activity. However, that relationship broke due to the massive amount of Federal Reserve interventions in the financial markets. That distortion masks the economy’s underlying weakness and the “moral hazard” created by the Fed.

Bigger Debts Aren’t The Solution.

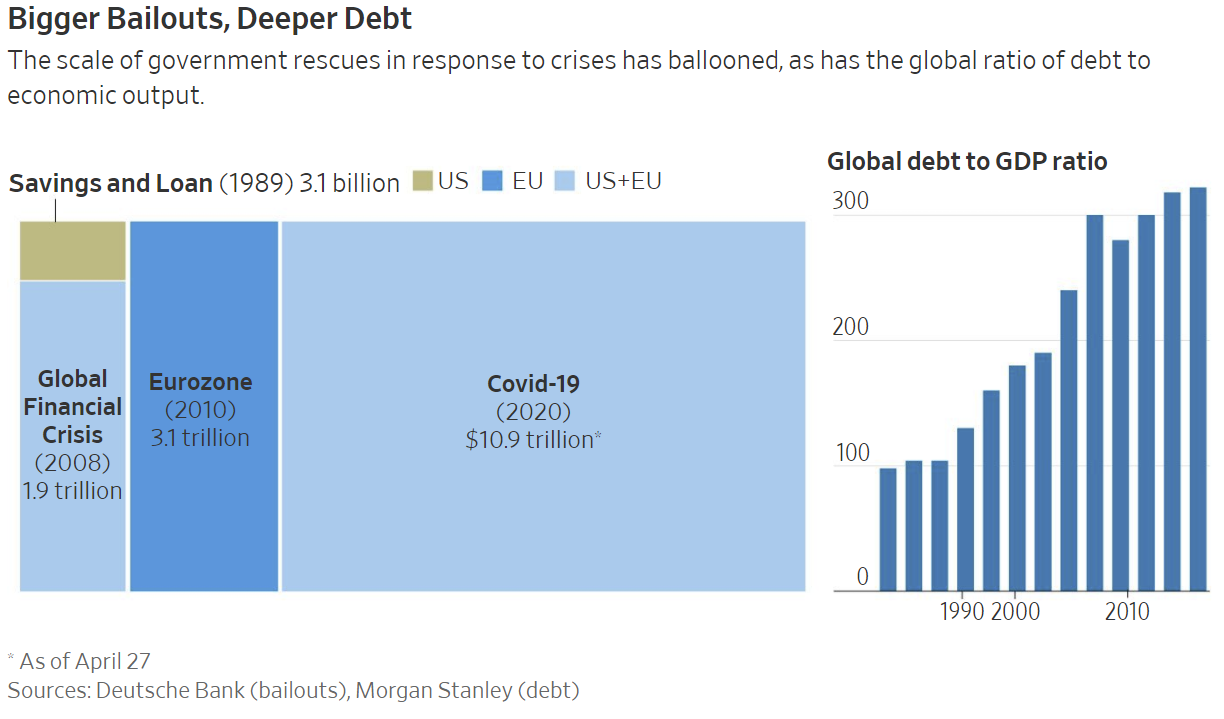

“The rest of the world followed the Fed. As interest rates fell toward zero, the world’s debts—including households, governments and nonfinancial companies—more than tripled between 1980 and 2007 to more than three times the size of the global economy.

It was taking more debt to fuel the same amount of growth, because more debt was going to unproductive borrowers. Capitalism was bogging down.” – Sharma

The statement of unproductive debt is critical to understanding why policies fail to achieve their economic growth goals and inflation.

Unproductive debt retards economic growth over time as it diverts revenue into debt service rather than productive investments. While the Federal Reserve fails to recognize the impact of their policies, we have a decade of experience showing that surging debt and deficits inhibit organic growth.

Keeping the economy on perpetual life support shows too clearly that the economy will fail unless fiscal and monetary stimulus continues.

However, by bailing out failed enterprises to avoid short-term economic pain, the consequence of not allowing the system to “clear itself” creates further distortions in the economy.

As President Kennedy once said:

“The time to repair the roof is when the sun is shining.”

Instead, we seem to have just removed the roof altogether.

The fact that debt and deficits rose under full employment conditions suggests a more profound underlying fiscal problem previously existed and has now worsened.

We Need A Better Solution

“What capitalism urgently needs is a new, more focused approach to government intervention—one that will ease the pain of disasters but leave economies free to grow on their own after the crises pass.” – Sharma

He is correct. The CBO’s budget projections are a harsh reminder of the consequences of debt and deficits.

“The longer policymakers wait to fix the debt, the harder and costlier it will get. Delaying action means the necessary changes will be spread among fewer people. Policymakers will have less ability to carefully target adjustments. And ultimately, it will be harder to phase in new policies or give families and businesses time to prepare and adjust for them.” – CFRB

There is no “pain-free” escape from the “debt hole” into which we have dug ourselves. Sharma is correct in his statement:

“When the pandemic passes, authorities need to shift out of rescue mode and start weaning capitalism off easy money and bailouts.”

However, even the “weaning process” will be painful. Stock markets will decline, the economy will weaken, and bankruptcies will rise. But such are the choices policymakers will have to make.

The continuous bailouts continue to distort the market’s price signals, which makes the markets less efficient in allocating capital. Such has led to the rising number of “zombies” and monopolies, the widening of wealth inequality, and lower productivity and growth.

The deformation of capitalism will be an economic plague that continues to lead to further dysfunction alienating younger generations. Social unrest and revolt will be the eventual result.

We can make choices today, which will be unpopular. Individuals will have to endure the short-term “pain.” However, it will be well worth the more robust economy tomorrow.

Or, you can wait until our creditors make those choices for us all at once.