Unretirement: The reversal of retirement due to extenuating circumstances because, as humans, we go through change, and sometimes life gets in the way. So, if you’re looking to unretire, there are four important steps to consider.

Keep in mind that a storm of changing employment and retirement trends emerged during the pandemic. A subset of the population 65+ had decided their assets appreciated enough to leave the job market. The dip is showcased in the Labor Force Participation rate growth since 2000 (chart courtesy of Advisor Perspectives). RIA readers are familiar with the ‘Great Resignation,’, especially among the Millennial cohort. But, older workers left too—perhaps too soon in the face of a turbulent start to markets in 2022.

The St. Louis Fed recently shared research titled The Great Retirement: Who Are the Retirees? The Institute for Economic Equity dug into the continued exit from the labor force of workers 65 and older. Notably, those 65-74 were the largest cohort to retire during the pandemic. The reasons cited for the departure include avoiding mental health distress, challenges the pandemic created, and notable wealth gains for investment portfolios and residential real estate.

The Fed’s research outlines that many retirees eventually return to the labor market in some form.

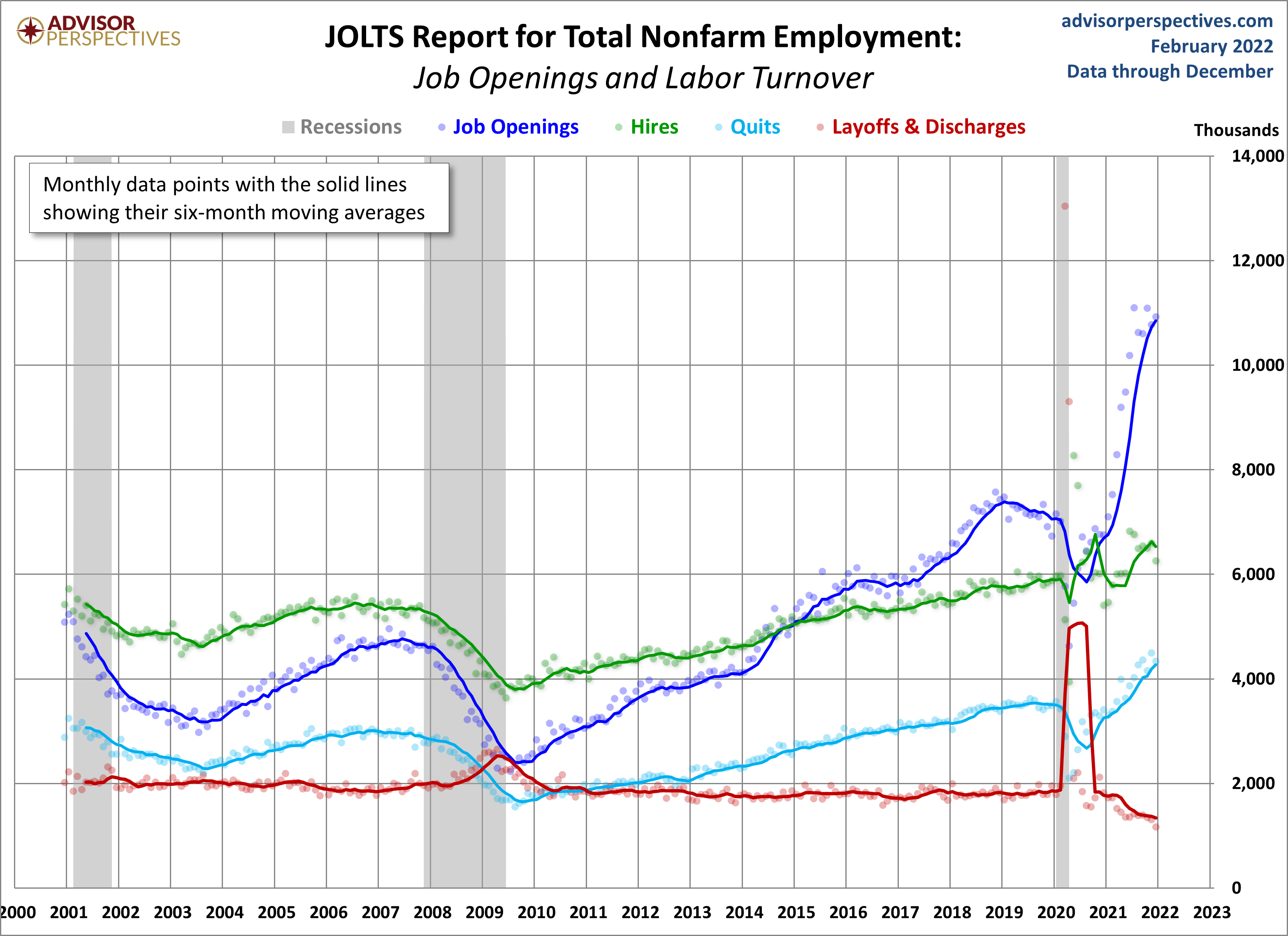

Businesses badly need older workers. As seen in JOLTS, all workers are in demand! Yet, I foresee an emerging trend of unretirement employment because work is a purpose; retirement requires mental preparation, and perhaps a segment of newer retirees will realize they jumped into a significant life change prematurely.

Frankly, I already hear the swan song from several recent retirees – I left work too soon and need something to do. I’m considering…

So, if you’re looking to unretire, here are four important steps to consider:

One: Don’t beat yourself up because things change.

With markets in turmoil, retirees may decide to return to work to reduce distributions from their investment accounts. Frankly, if you’ve done comprehensive planning with RIA, you’re going to be ok as we help retirees prepare for lackluster or adverse market cycles. However, psychologically and emotionally, returning to work I’ve observed is a fantastic boost to a person’s well-being.

A part-time job that utilizes long-term skills keeps one social and bolsters household cash flow are all positives for returning to work. Keep in mind people who transition slowly to retirement: work full time, then part-time, are most likely to experience fewer diseases and function better day-to-day compared to those who stop working altogether.

That’s at least the results of the Journal of Occupational Health Psychology study. Bridge employment is healthier than leaving the workforce cold turkey, which is what occurred during the pandemic. Now, with the environment slowly returning to normal, many retirees may assess the overall value of returning to the labor force.

Two: Did you take Social Security at 62? Possibly there’s time to reverse this decision.

Suppose you signed up for Social Security at age 62 or before full retirement age. In that case, there could be time to reverse the decision and make unretirement even more worthwhile especially if you’re married to a lower wage-earning spouse who would depend on survivor benefits.

For example, if you claim at age 62, spousal retirement benefits, usually ½ of a working spouse’s primary insurance amount, will be reduced by 25%. A spouse can be negatively impacted as a survivor since benefits would be reduced accordingly.

An example:

Keep in mind a widow(ers) benefit is based on 100% of the decedent’s Social Security PIA if benefits have started. For example, Richard is 59 with a PIA at full retirement age of $2,797. Claiming Social Security at age 62 drops his monthly benefit drops to $2,098. Richard’s wife Kim would see her benefit reduced to $2,098 if he passes. If he doesn’t claim at age 62 and passes away, Kim can receive his full benefit of $2,797. Kim should wait until her full retirement age to claim Richard’s full retirement benefit. The Social Security claiming decision is a family decision. How you claim affects spouses and survivors.

Pay it back?

Also, if you started Social Security before full retirement age, pay it back. Yep, all of it. If it’s been twelve months or less, that’s a viable option. The move will get you back on track for the maximum benefit at full retirement age. Or delayed credits at age 70. Social Security is one of the most affordable lifetime income options out there. There’s no private annuity available that provides the same, robust lifetime income available to Americans through Social Security. Postponing benefits from age 62 to 70 results in a 76% increase in monthly lifetime benefits. If your full retirement age is 67, wait until 70. At that time, your benefit increases by 8 percent a year or 24 percent.

Recently, I helped someone examine the four steps to ‘unretire.’ Unfortunately, it was too late to pay back Social Security. However, he did secure part-time employment and stay below the Social Security earnings test threshold. For this year, one dollar of Social Security benefits is withheld for every two dollars earned above $19,560. The benefits aren’t lost; they’re just postponed and added to your monthly benefit at full retirement age. Also, the definition of earnings only includes salary and wages. In the earnings test definition scope, retirement account distributions are not considered.

For example, Jim is 63. He finds a position that pays him $35,000 a year. Social Security subtracts $19,560, then divides by two. The amount withheld is $15,440/2 or $7,720.

I wouldn’t use the earnings test as a sole reason not to work. The benefits of work overall can outweigh dollars withheld. However, if you’re looking to unretire, the Social Security impact is one of the four important steps to consider.

Three: Revise your financial plan as a step to unretire.

Another move to make as you walk the four steps to unretire is to update your comprehensive financial plan. A financial plan is a written, holistic financial diagnostic; consider an adequately designed plan as a financial integrity awareness tool. An unretirement strategy increases household cash flow and may postpone or reduce portfolio withdrawals through times of market stress. Consequently, plan success rises, and so does investment portfolio survivability.

A properly designed financial plan will cover essential elements like retirement savings, insurance analysis, and estate review; a qualified planner will target and outline specific areas of strength and weakness along with flexible, realistic routes to each financial goal.

If you’re stressing over the process or how long it takes to get a plan together: Don’t. Of course, there’s a financial self-discovery period, but the effort will raise holistic financial awareness. After all, there are none of the daily highs and lows of the stock market. No sizzle. Financial planning doesn’t make headlines or capture the attention of media-talking heads. A plan only cares about you.

Consider financial planning the mundane sentinel which forms the foundation of money awareness. When plans are attached to goals or life benchmarks, as I call them, they take on a life of their own as progress markers along the path to a successful financial life.

A plan is a complete diagnostic of money chemistry. And the numbers don’t lie. When we take the step to ‘unretire’ there’s a comfort found in the numbers.

At times, it’s is validation; other times, an awakening.

So, let me ask:

“Would you rather have a comprehensive plan completed by a professional who adheres to a fiduciary standard where your financial health and plan are paramount, or a broker tied to an incentive to sell product?”

Brokerage firms are willing to offer financial plans at no cost. However, the price ultimately paid for products and lack of objectivity is not worth a ‘free’ plan. I’ve labored over numerous retirement plans prepared by brokerage firms: They were not crafted for people seeking to prepare adequately for retirement.

Nothing about longevity assessments (which we do through analysis to help people plan realistically based on health habits and family history), zero about maximized Social Security claim strategies, erroneous inflation rates (too low), and aggressive forward returns (too high) for risk assets like stocks. What about taxes in retirement? Not one plan included a tax-smart retirement income distribution analysis. However, what stood out was a trend to recommend sizable investments in variable annuities.

If you’re looking to unretire one of the four important steps to consider is a financial plan.

Four: Reset your ‘FULL’ retirement clock.

If you’re looking to unretire, one of the four important steps is to reset and pay attention to your FULL retirement clock.

There is a clock, an inner voice, a gut feeling that notifies retirees to put a full stop on work and quickly move on to other interests. It’s a sign of a complete, satisfying transition to a retirement lifestyle where hobbies and other interests outweigh the mental attributes of work. As a retiree, or unretiree, the time will come; you will know when the FULL retirement clock alarm rings.

From my experience partnering with others through this process, it takes on average five to seven years into part-time or consulting work for the clock to go off. At that time, the transition to hobbies, travel, and social events is complete, and a paying job loses its place in importance. I’ve witnessed retirees decide to stop work and never look back. Many say – “I don’t know when I ever had time to work, I’m so busy!” It’s then I know that the internal clock has struck the proper hour, and the high-speed retirement fun tailwind has hit full throttle!

Last, according to the Center for Retirement Research at Boston College, one of my favorite think-tanks on all things retirement, released a March paper titled Will Unretirement Help Solve The Labor Shortage? The short answer is no. Per the study, the rate of unretirement has been relatively low over the last four decades, averaging a bit over 6 percent. We shall see if the lingering effects of the pandemic will increase the average.

Regardless, the re-entry of retired workers age 55-70 into the labor force would be a welcome change by many small business owners who understand older American employees are diligent, hard-working, and dependable.

If you’re looking to unretire, I hope these four steps are important to consider.

Richard Rosso, MS, CFP, CIMA is the Head of Financial Planning for RIA Advisors. He is also a contributing editor to the “Real Investment Advice” website and published author of “Random Thoughts Of A Money Muse.” Follow Richard on Twitter

Customer Relationship Summary (Form CRS)

Also Read