As we reported yesterday, a liquidity crunch brought cryptocurrency exchange FTX to its knees on Tuesday. Hours later, FTX announced it had entered a non-binding agreement to be acquired by its rival, Binance. The acquiring exchange would’ve been able to provide market liquidity and bridge the gap if the deal closed. This helped cool surging fears and kept a lid on volatility across cryptocurrencies at the time.

In another turn of events yesterday, Binance left FTX hanging less than a day after entering the agreement. Rumors had begun surfacing of a hole in the FTX balance sheet that could be as large as $5-10B. We suspect something along these lines to be the case after Binance announced:

“Our hope was to be able to support FTX’s customers to provide liquidity, but the issues are beyond our control or ability to help.

Every time a major player in an industry fails, retail consumers will suffer. We have seen over the last several years that the crypto ecosystem is becoming more resilient and we believe in time that outliers that misuse user funds will be weeded out by the free market.”

This turn of events sent crippling fear right back into crypto markets—putting significant pressure on both Bitcoin and Ethereum for the second day in a row. Both the SEC and CFTC are said to be investigating FTX as we speak.

What To Watch Today

Economy

- 8:30 a.m. ET: Consumer Price Index, month-over-month, October (0.6% expected, 0.4% prior)

- 8:30 a.m. ET: CPI excluding Food and Energy, MoM, October (0.5% expected, 0.6% prior)

- 8:30 a.m. ET: Consumer Price Index, year-over-year, October (7.9% expected, 8.2% prior)

- 8:30 a.m. ET: CPI excluding Food and Energy, YoY, October (6.5% expected, 6.6% prior)

- 8:30 a.m. ET: CPI Index NSA, October (298.488 expected, 296.808 prior)

- 8:30 a.m. ET: CPI Core Index SA, October (300.094 expected, 298.660 prior)

- 8:30 a.m. ET: Real Average Hourly Earnings, year-over-year, October (-3.0% prior)

- 8:30 a.m. ET: Real Average Weekly Earnings, year-over-year, October (-3.8% prior)

- 8:30 a.m. ET: Initial Jobless Claims, week ended Nov. 5 (220,000 expected, 217,000 prior)

- 8:30 a.m. ET: Continuing Claims, week ended Oct. 29 (1.487 million expected, 1.485 prior)

- 2:00 p.m. ET: Monthly Budget Statement, October (-$90.0 billion expected, -$429.7 billion prior)

Earnings

Market Trading Update

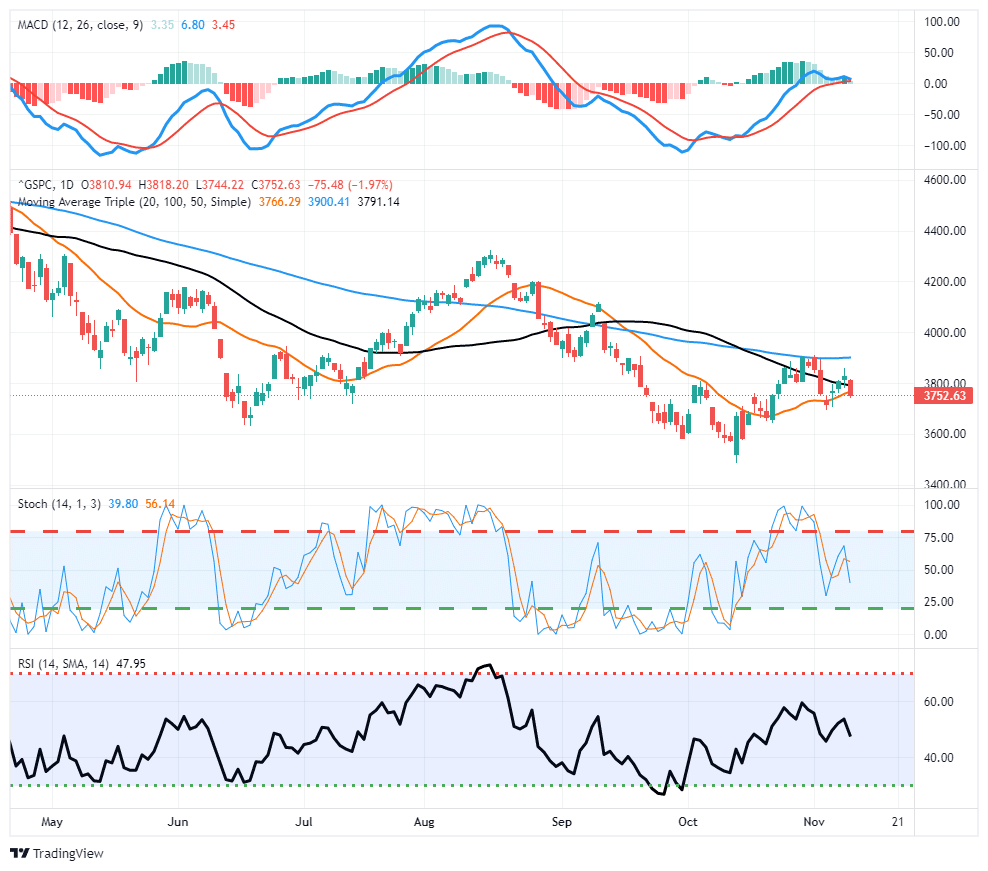

The last couple of days of the “midterm election” rally got wiped out as disappointment over Republican performance in key Senate races. At the moment, it appears there will still be gridlock, with the Senate split and control of the House falling to Republicans. The Georgia Senate seat is still up for grabs with a runoff deciding the majority control of the Senate. As we’ve written previously, investors hoping for the post-election rally could be left hanging this time.

Other pressures also weighed on the stock market yesterday as Cryptocurrencies were decimated over fallout from the FTX failure. Also, there was a terrible auction for 10-year Treasuries, highlighting the lack of liquidity in that market. Lastly, investors are also pairing back exposure ahead of the CPI report tomorrow, which could see stocks either surge higher or retest recent lows.

The CPI report this morning will set the tone for equities today. The market is flirting with important support at the 20-dma. The action yesterday was not good, and the MACD “sell signal” is dangerously close to flipping. Caution remains advised.

Market Matters

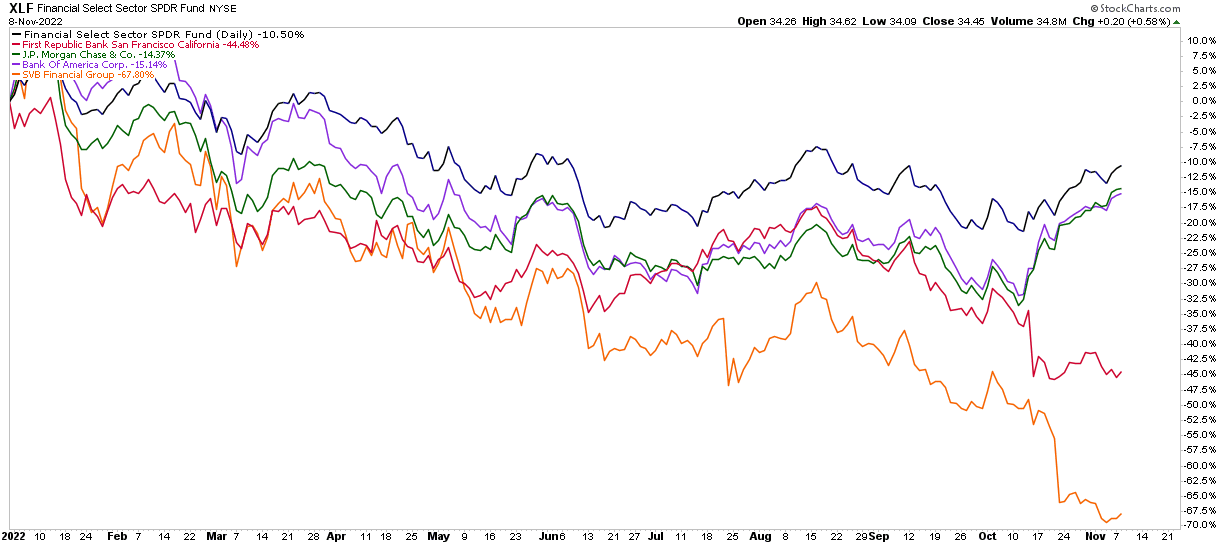

The main source of banking profits is Net Interest Income (NII). Banks generate NII by borrowing on the short end (deposits are liabilities) and lending at higher rates on the long end (loans are assets). Massive consumer banks like JPM and BAC have benefited from the Fed’s rate hikes by charging more on loans while still paying low rates on liabilities. Despite the inverted yield curve, they can generate higher NII margins since deposits aren’t chasing rates to a great degree.

Be careful of falling into the trap of thinking all banks will benefit, given the inverted yield curve, however. First Republic Bank (FRC) serves wealthy clients who are more deliberate with their cash. The bank has been forced to pay higher rates on liabilities to keep deposits from leaving. According to the WSJ, FRC is seeing NII margins decline, and its stock price has followed suit after shareholders were left hanging. SIVB is running into a different problem. Deposits fell 6% in the 3rd quarter as its start-up clients burn cash while new funding rounds have drastically slowed. Market matters- and these banks have unfortunate exposures in this environment.

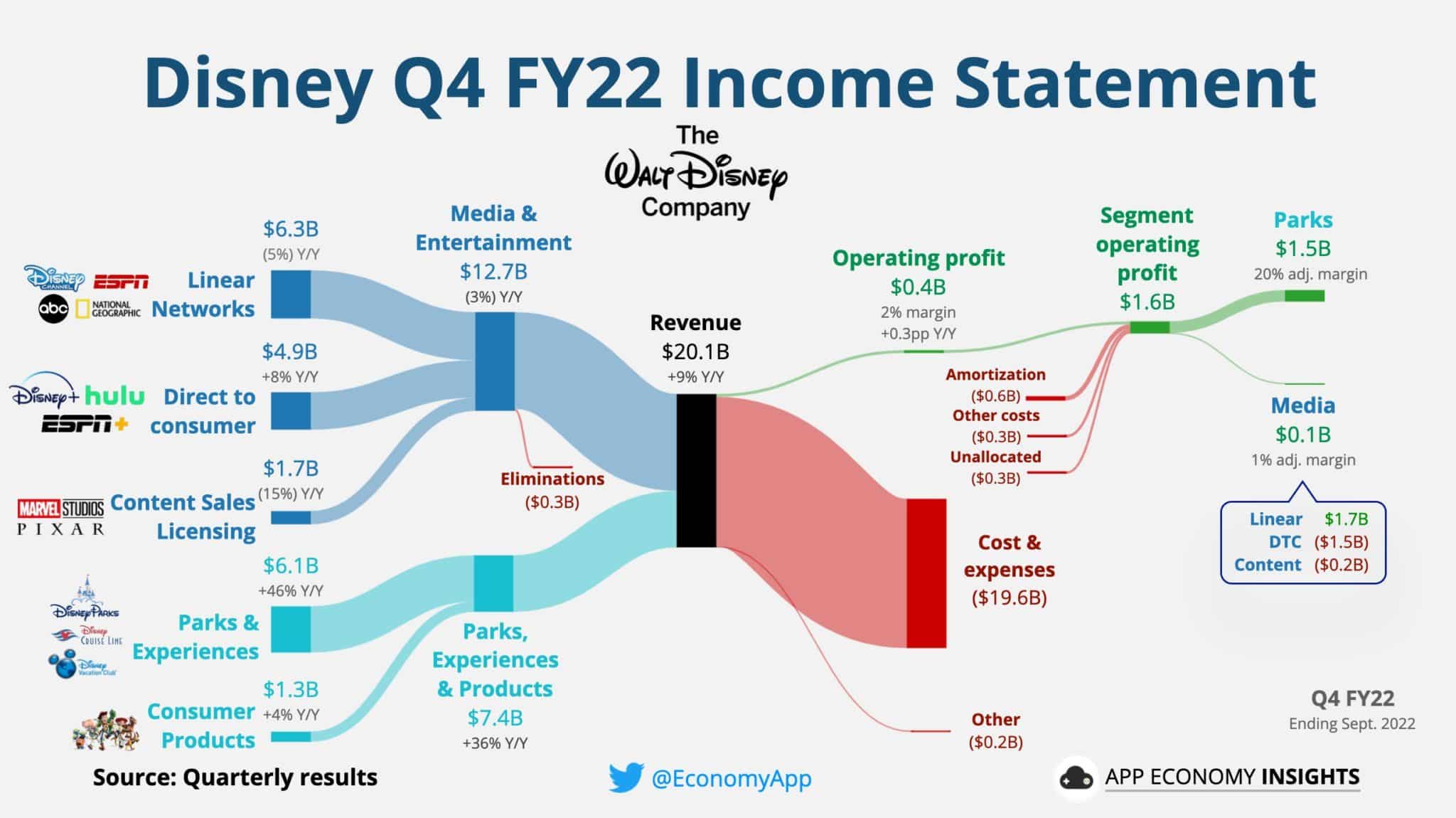

Disney Missed on Top and Bottom Line – Guess What Happened Next?

In a quarter where punishments have been especially harsh for those missing expectations on both their top and bottom lines, DIS did just that. Revenue of $20.2B came up short of expectations of $21.4B, while adjusted EPS of $0.30 missed the consensus of $0.56. Their Parks segment failed to continue showing strong results as margins missed expectations, and guidance raised concerns about profitability going forward. There was a bright spot in the dismal results- Disney+ subscriber growth of 12.1M users. Unfortunately, this wasn’t enough to keep the stock from getting clobbered. DIS stock fell over 13% in yesterday’s trading. The handy chart below from App Economy Insights illustrates how Disney’s quarter went.

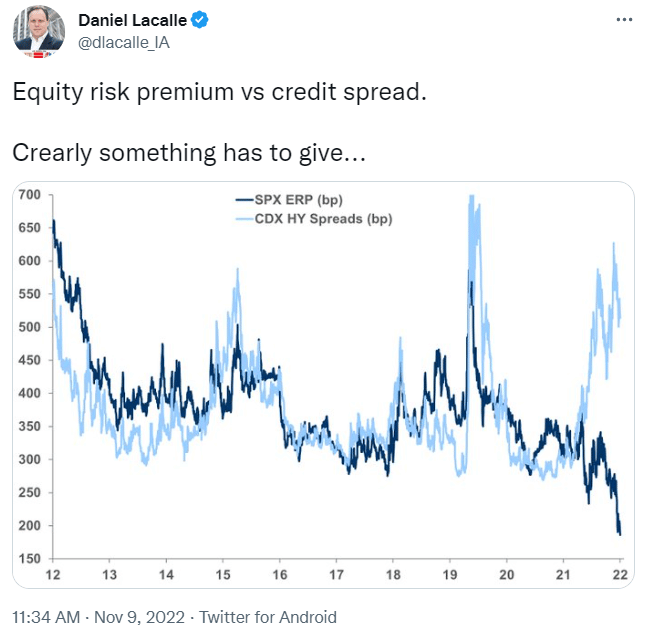

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read