In this 01-14-22 issue of “Inflation Surge Pushes Fed To Hike Rates Faster.”

- Market Struggles With Inflation Surge

- The Fed Is Getting Aggressive

- Portfolio Positioning

- Sector & Market Analysis

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Is It Time To Get Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Schedule your “FREE” portfolio review today.

Market Struggles With Inflation Surge

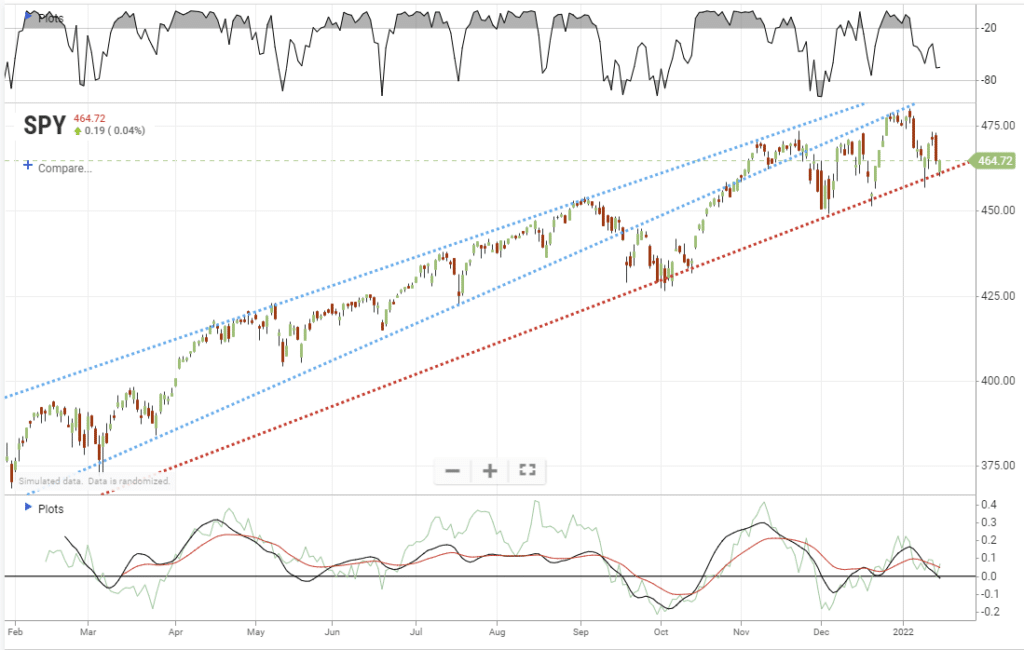

Last week, we started our discussion by reviewing the market’s failure at previous resistance.

“However, as shown, the market is overbought, pushing into heavy bull-trend resistance, and is nearly 10% above its 200-dma. Notably, the upper trend line repeatedly provided resistance against the advance, while the lower trend line provided that support. In September, that changed with the lower support giving way, and is now providing another resistance level to the advance.”

Chart updated through Friday.

Notably, despite the market’s failure to hold previous gains, it successfully retested and held the lower trend line. However, sell signals remain in place and have not yet reached more oversold levels. The concern remains the Fed’s more aggressive stance to battling the inflation surge, which hit 7% annualized this past month.

We will discuss the latter point more in a moment.

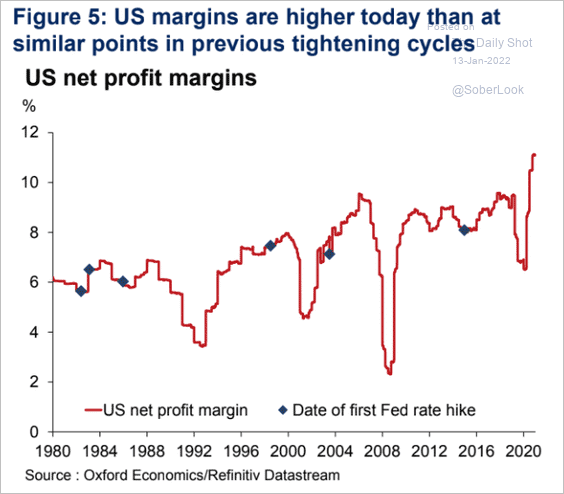

However, starting next week, we will enter into “earnings season,” which should remain supportive of stocks in the near term. The big question will be whether companies have successfully passed on higher input prices, wages, and benefit costs to consumers. Therefore, profit margins will be the thing to watch and corporate outlooks for the rest of the year.

With corporate net profit margins at records, fueled by $5 Trillion in stimulus, there is likely a substantial risk of disappointment in the quarters ahead.

Earnings Have Likely Peaked

Wall Street estimates for 2022 remain exceedingly high. Interestingly, most Wall Street analysts view 2022 as an ongoing economic recovery. Such is interesting considering the recovery from the 2020 pandemic was anything but a normal post-recessionary recovery.

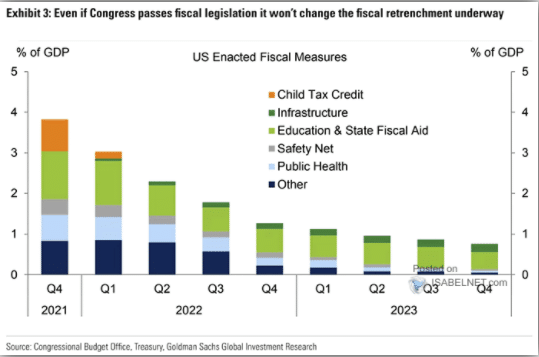

There are several reasons why we believe we could see corporate earnings could contract more than expected. The first, as shown below, is the retraction of liquidity. While more than $5 trillion of fiscal liquidity pulled forward a massive level of demand, creating supply shortages, that liquidity will continue to reverse.

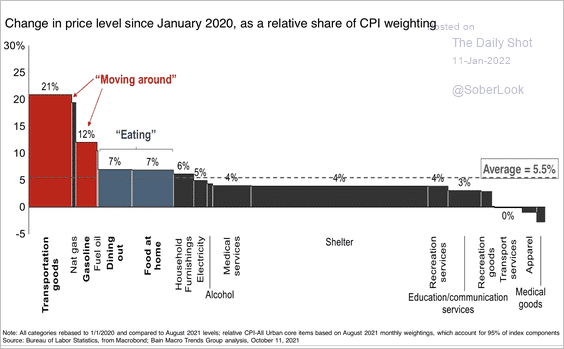

Secondly, the inflation surge will have a two-pronged effect on earnings as input costs continue to erode profits along with slowing demand as consumers retrench due to higher living costs. Such is particularly the case with surging energy and transportation costs which increase production costs for companies and costs of living for consumers.

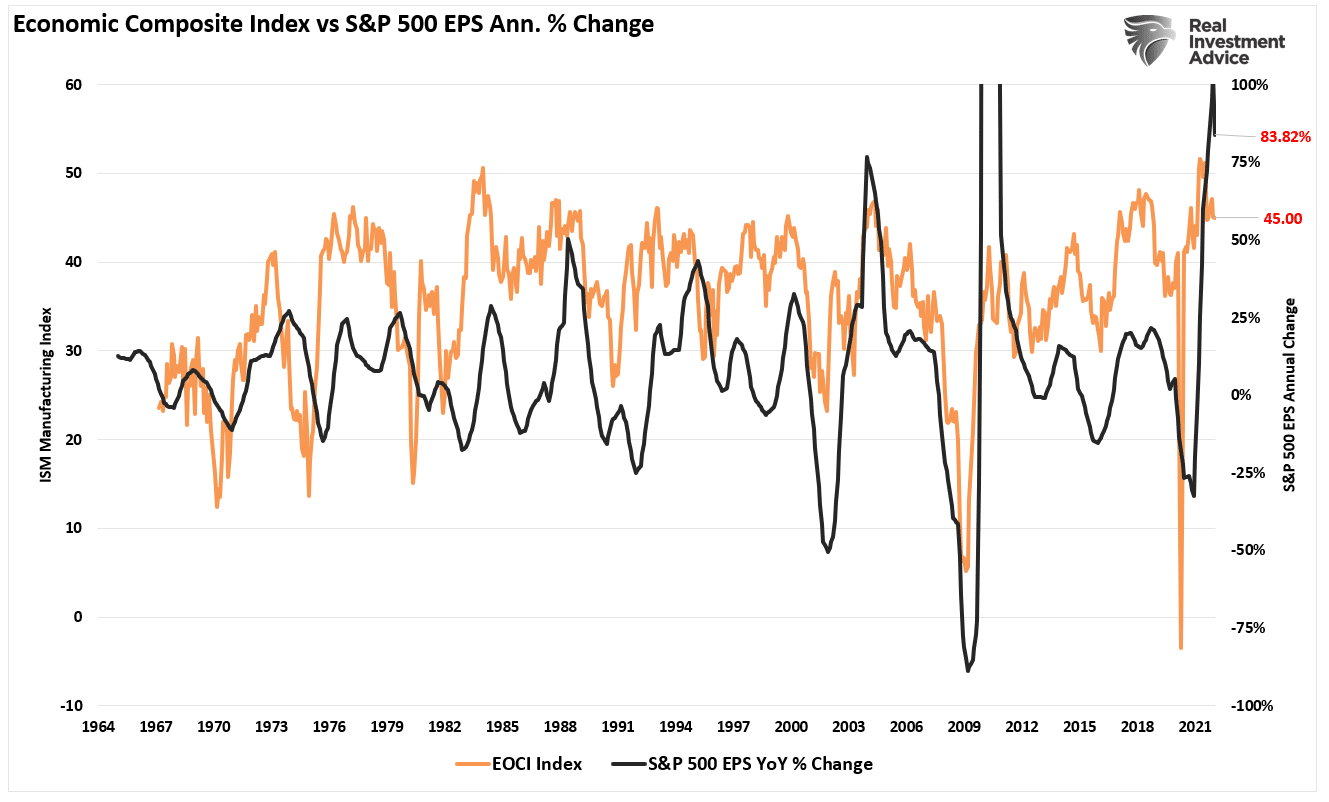

Lastly, earnings growth has likely peaked following the economic shutdown that crashed revenues. Fueled by the massive liquidity surge, recovery in earnings will revert to norms as economic growth slows. A good proxy for the reversion in earnings is the high correlation to our broad economic composite index.

Not surprisingly, and as suggested previously, estimates have already started to soften.

Given that the flood of liquidity created an artificial increase in economic activity, reversing to more historical norms should not be a surprise.

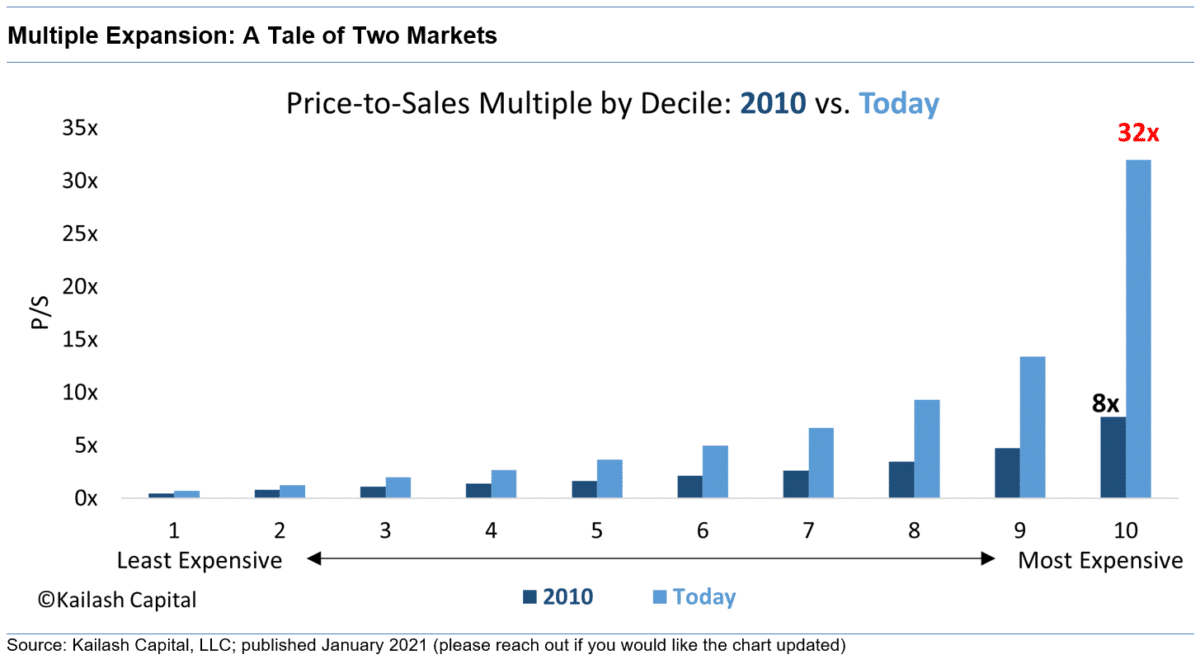

Such will be problematic for investors trying to justify overpaying for valuations when inflation and interest rates rise.

“The most expensive 10% of companies in the market had seen their multiples explode from 8x price to sales to 32x.” – Kailash Concepts

This Week’s MacroView

The Fed Is Getting Aggressive

As noted, the Fed is becoming considerably more aggressive now that CPI is running at 7% annually. Last Tuesday, the following headlines hit the tape.

- BOSTIC SAYS FED COULD EASILY PULL $1.5 TRILLION OF “EXCESS LIQUIDITY” FROM FINANCIAL SYSTEM, THEN WATCH MARKET REACTION FOR FURTHER BALANCE SHEET REDUCTIONS.

- MESTER: ABLE TO LET BAL SHEET TO RUN DOWN FASTER THAN LAST TIME.

- POWELL: WE EXPECT TO ALLOW BALANCE-SHEET RUNOFF LATER IN 2022.

- POWELL: BALANCE SHEET IS FAR ABOVE WHERE IT NEEDS TO BE.

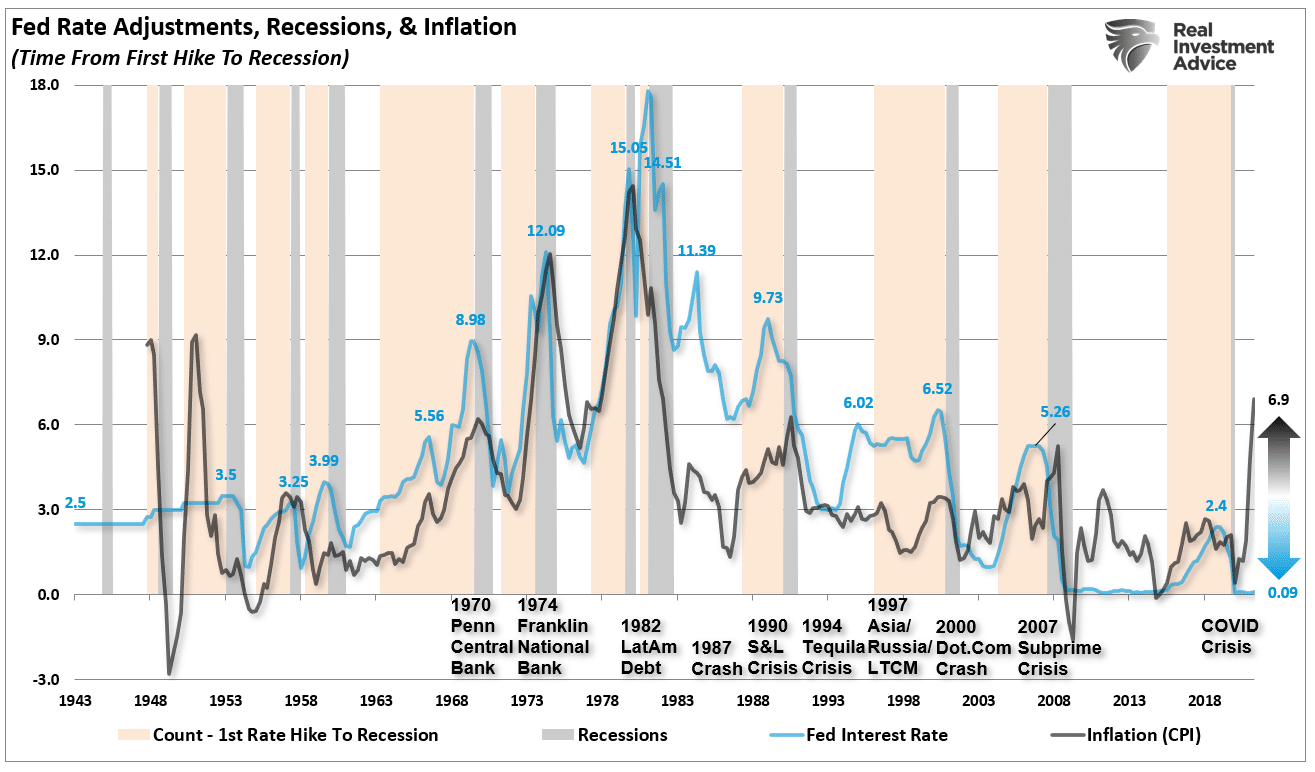

With Jerome Powell and two other Fed members heavily hinting that not only is balance sheet reduction (QT) likely, but the Fed may do so at a much faster pace than market participants are expecting. Of course, with Fed Funds at zero and the inflation surge at 7%, the Fed is considerably “behind the curve” in terms of monetary policy.

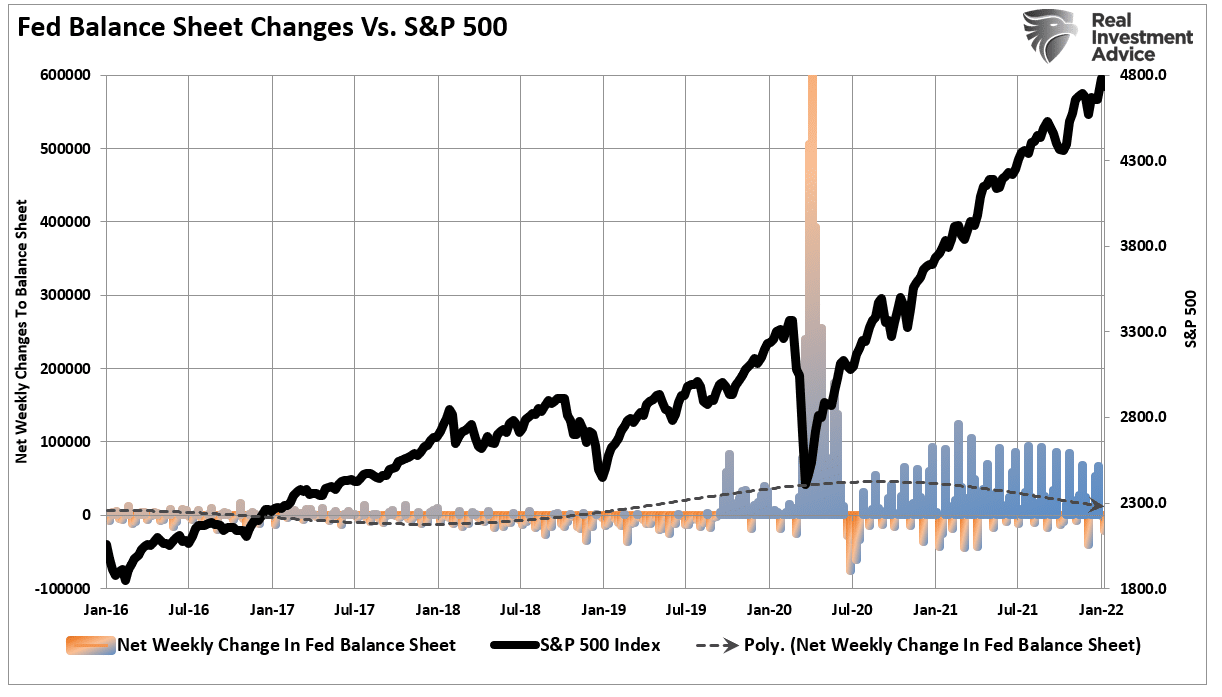

However, while the Fed should be aggressively tapering their balance and hiking rates, in reality, they are not. As shown below, the weekly changes to the balance sheet continue to remain positive.

Such suggests that the Fed is talking a “mean game” to the markets. Likely they are hoping the inflation surge will slow without taking substantial action that would create financial instability. Moreover, with the mid-term elections rapidly approaching and the President polling very poor even among Democrats, the risk of losing both Congressional houses is high. A cratering stock market would ensure a change of control.

If the Fed aggressively moves to combat inflation, the risk of a market correction increases. On the other hand, if they support the financial markets, inflation robs the poor of their incomes.

Such is the perfect receipt for a policy mistake.

A Policy Mistake In The Making

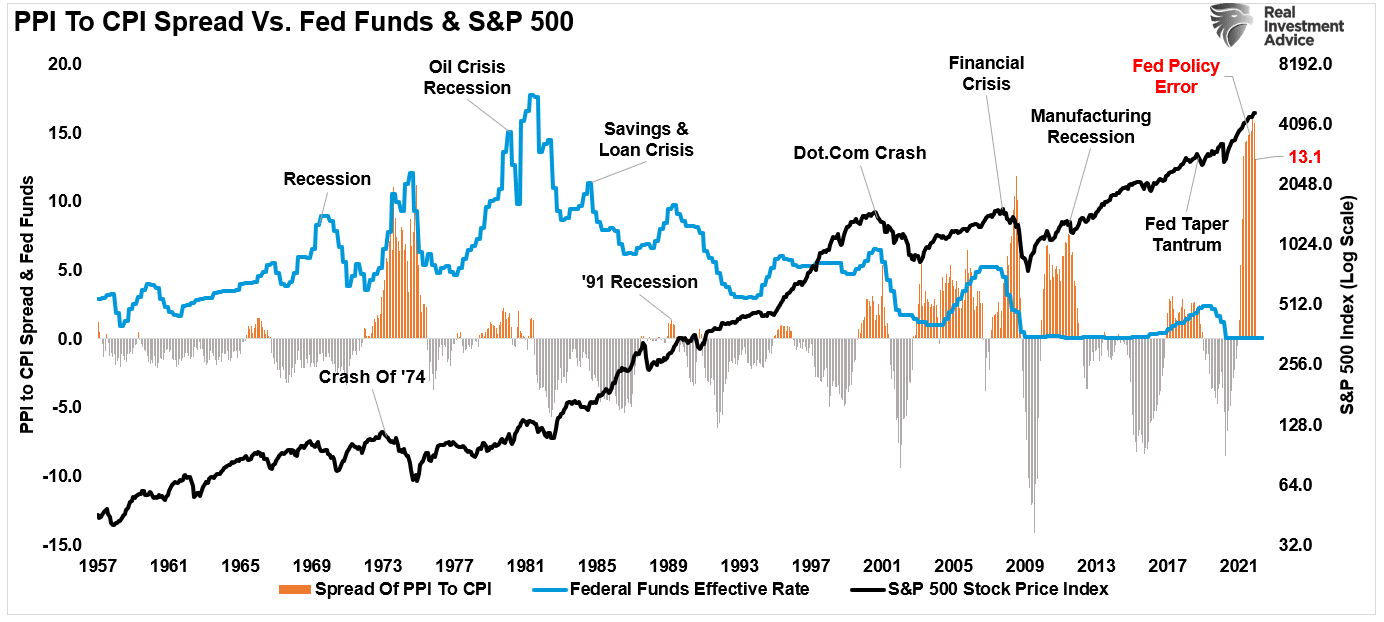

As noted, the Fed is in a tough spot. While they should be aggressively tightening policy, they are also aware of the ramifications of losing market stability. As shown, the massive spread between input and consumer prices suggests corporations cannot pass along inflation entirely. Such means we could see a contraction in profit margins in the quarters ahead.

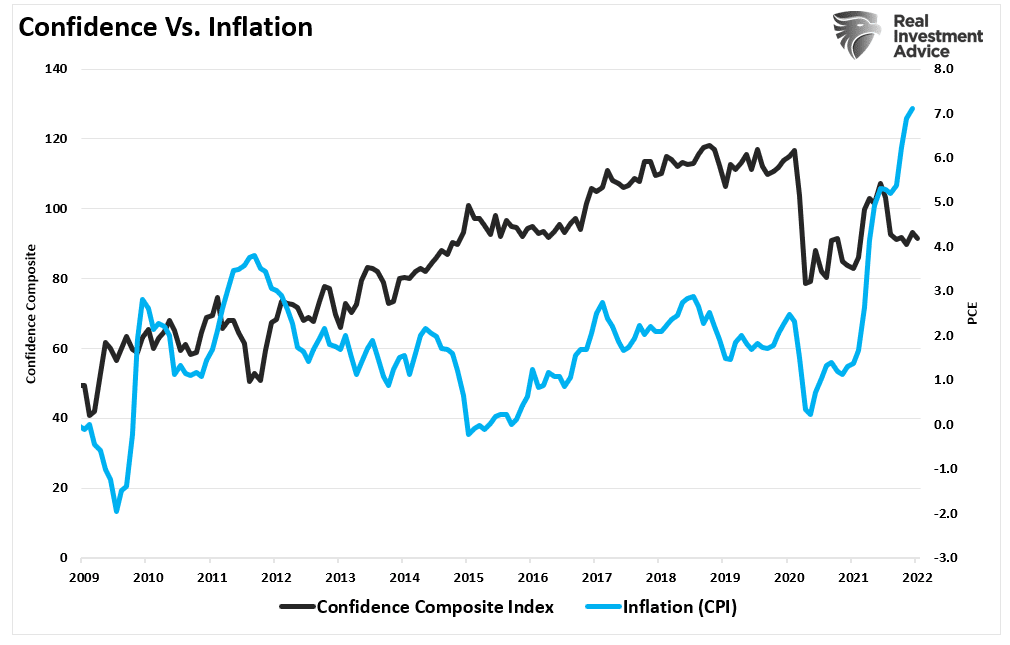

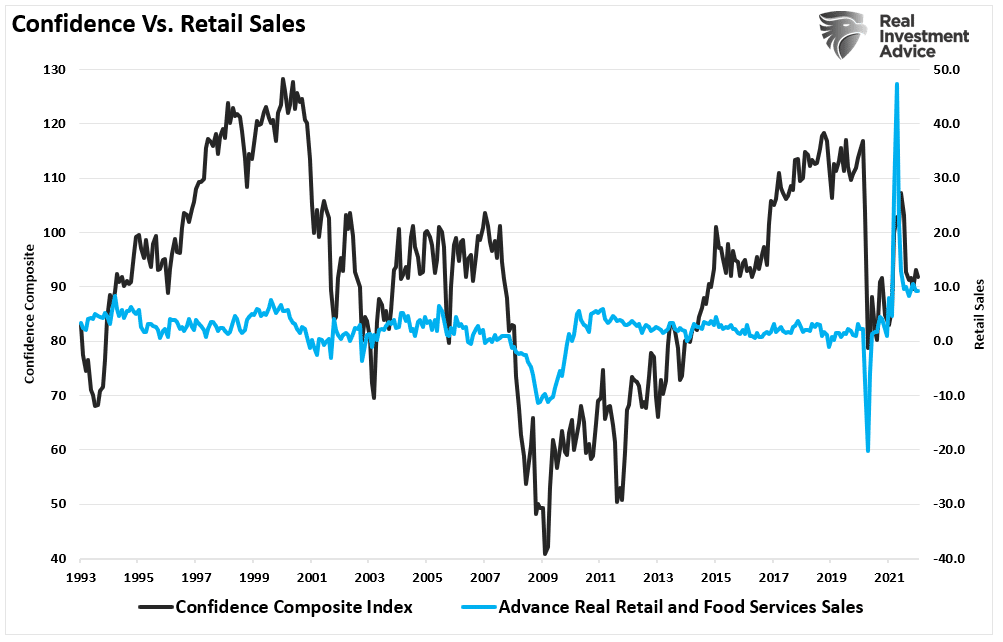

Furthermore, the surge in inflation erodes consumer confidence. As prices rise, so does the cost of living for the average American struggling to make ends meet.

That loss of confidence quickly translates into lost sales (demand reduction). Consider that retail sales comprise roughly 40% of PCE, which is approximately 70% of GDP. The decline in retail sales suggests weaker economic growth ahead.

If the Fed raises rates to break the inflation surge, such also retards economic growth. Higher rates historically equate to more negative market outcomes. Such is particularly true when valuations become elevated and low rates support the bullish thesis.

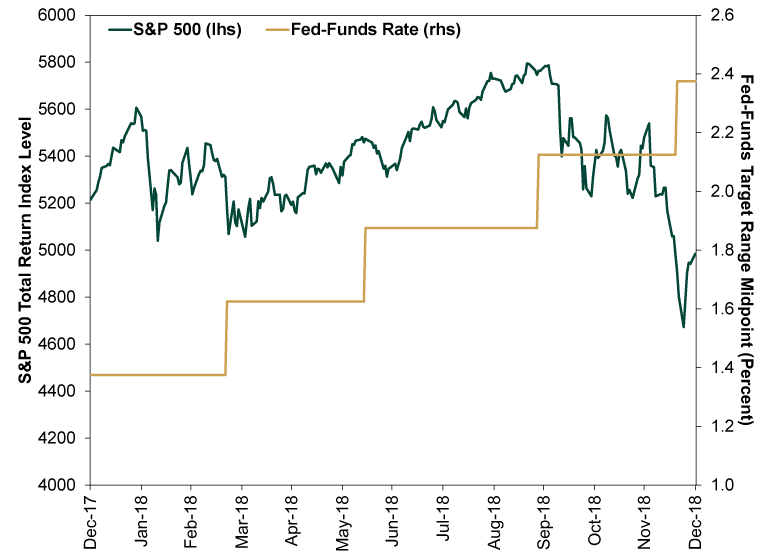

The most significant risk to investors is the Fed’s ability to “jawbone” the markets to maintain financial stability when reversing monetary accommodation. Such is the same environment we saw in 2018 where the Fed uttered the words “we are nowhere close to the neutral rate.”

Two months later, and 20% lower in the markets, Jerome Powell discovered he had magically reached the “neutral rate” and needed to ease off on monetary tightening.

Of course, in 2018, Powell didn’t have 7% inflation to deal with.

This time could indeed be different.

Portfolio Update

Last week, we touched on the “instability of stability” and why we should be mindful of the risk in our portfolios. Over the previous two weeks, the rise in market volatility has undoubtedly raised concerns. Unfortunately, high-beta, over-valued, fundamentally weak companies continue to suffer the brunt of the selling, and really few companies are immune to bouts of selling pressure.

Last week, we sold our S&P index trading position. Such raised cash in portfolios. We also made minor changes to our bond portfolio to extend our duration as yields rise and are now extremely overbought. This week, we again added to our bond holdings to increase our duration, further moving us toward our target allocations. (Target Model Weights: 60% stocks / 40% bonds and cash.)

Over the next couple of weeks, we will continue to utilize rallies to reduce high beta stocks in our portfolio and increase exposure to our value-based holdings. These changes will be gradual until volatility declines and the market establishes a new base.

As Michael Lebowitz concluded in his recent 2022 Market Outlook:

“If we learned anything from 2020, the future is far from certain. Not only should we expect the unexpected, but the market reactions to the unexpected may be vastly different than what many assume.

Navigating 2021 in hindsight was easy. However, a year ago, the outlook was daunting. No doubt 2022 will offer us both risk and rewards. Limiting risks and reaping the rewards will help traverse what offers to be another tricky year.

Maybe, more importantly, relying on trusted economic and market models and not letting psychological biases hinder investment decisions may prove to be the best advice we can offer.”

With that, I agree.

Market & Sector Analysis

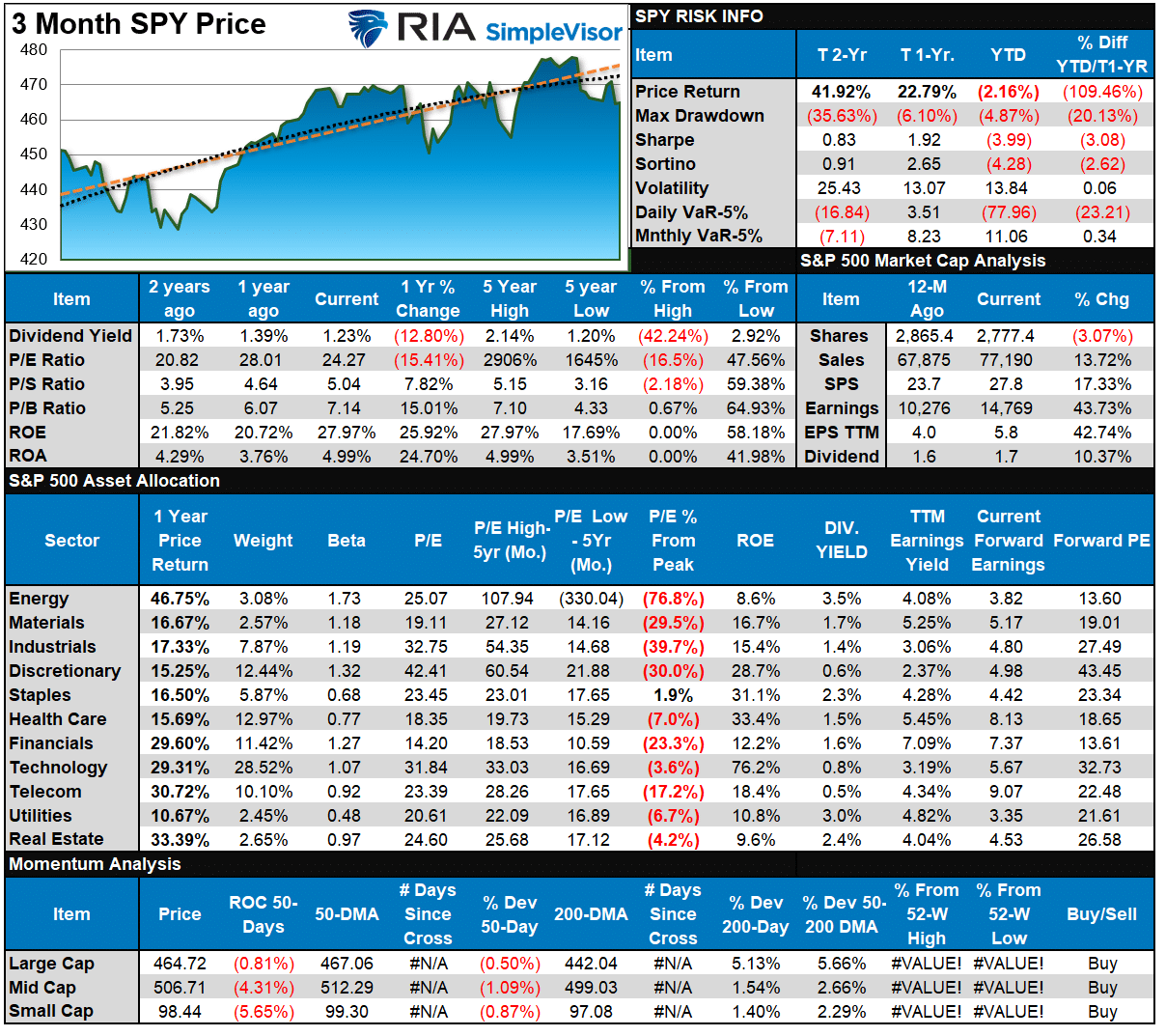

S&P 500 Tear Sheet

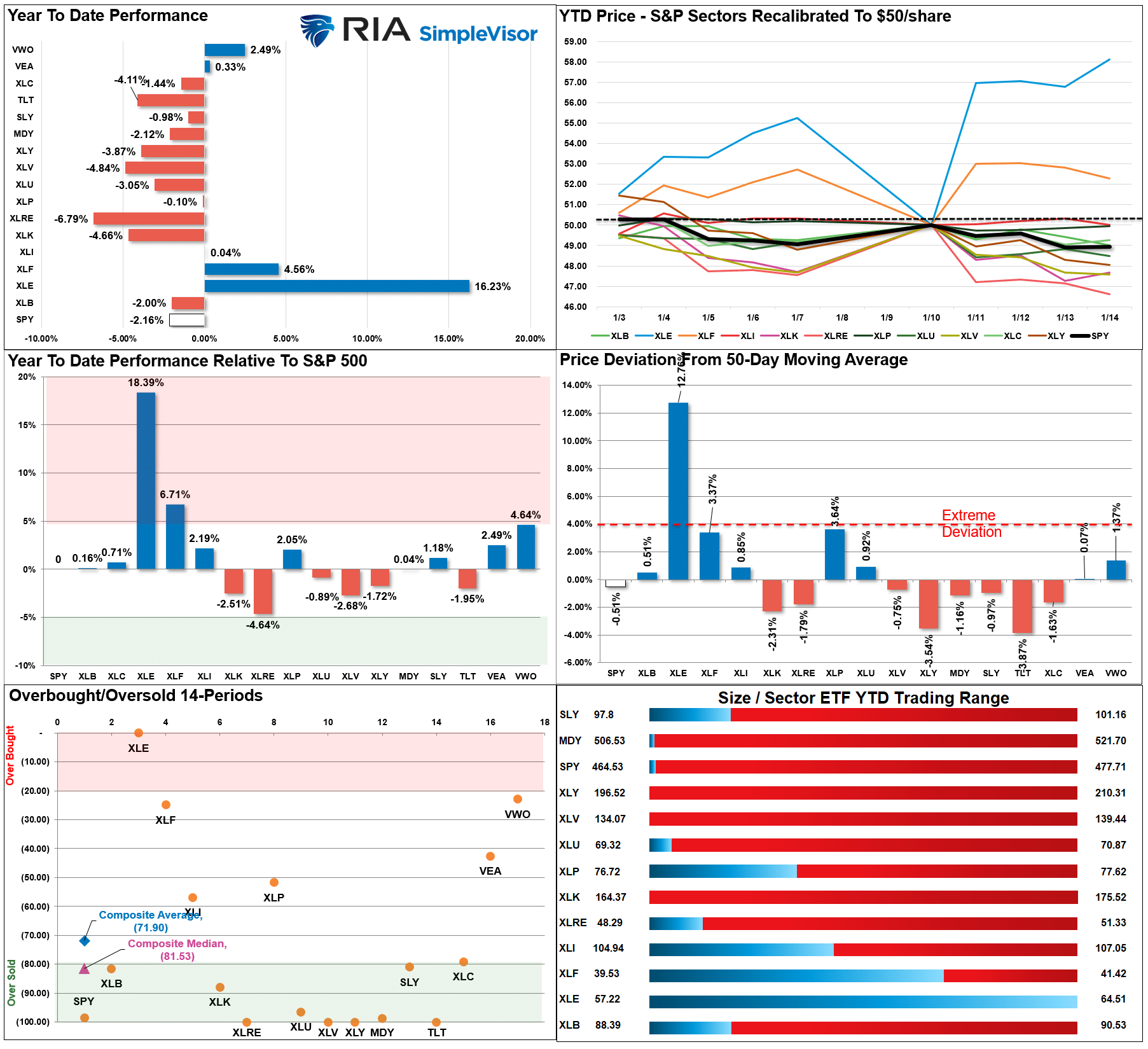

Relative Performance Analysis

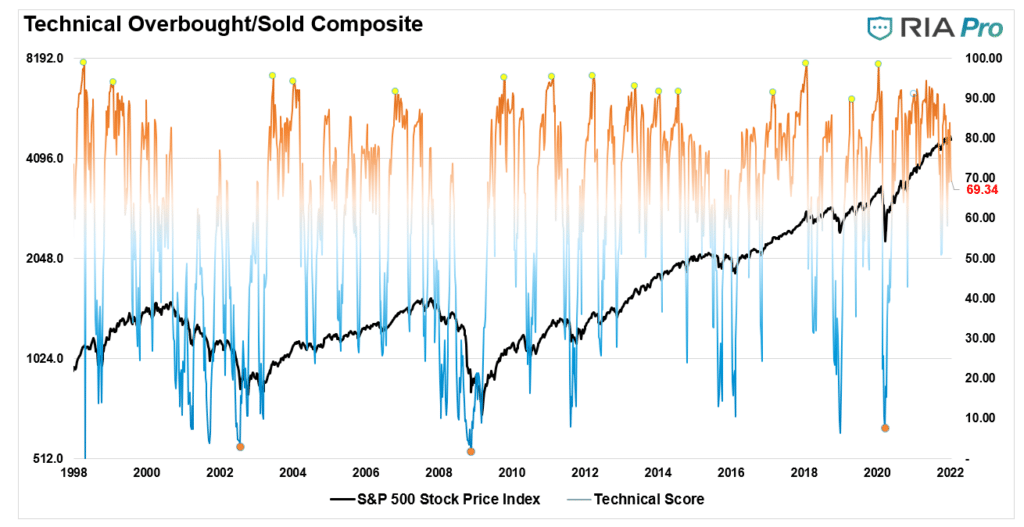

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The current reading is 69.34 out of a possible 100.

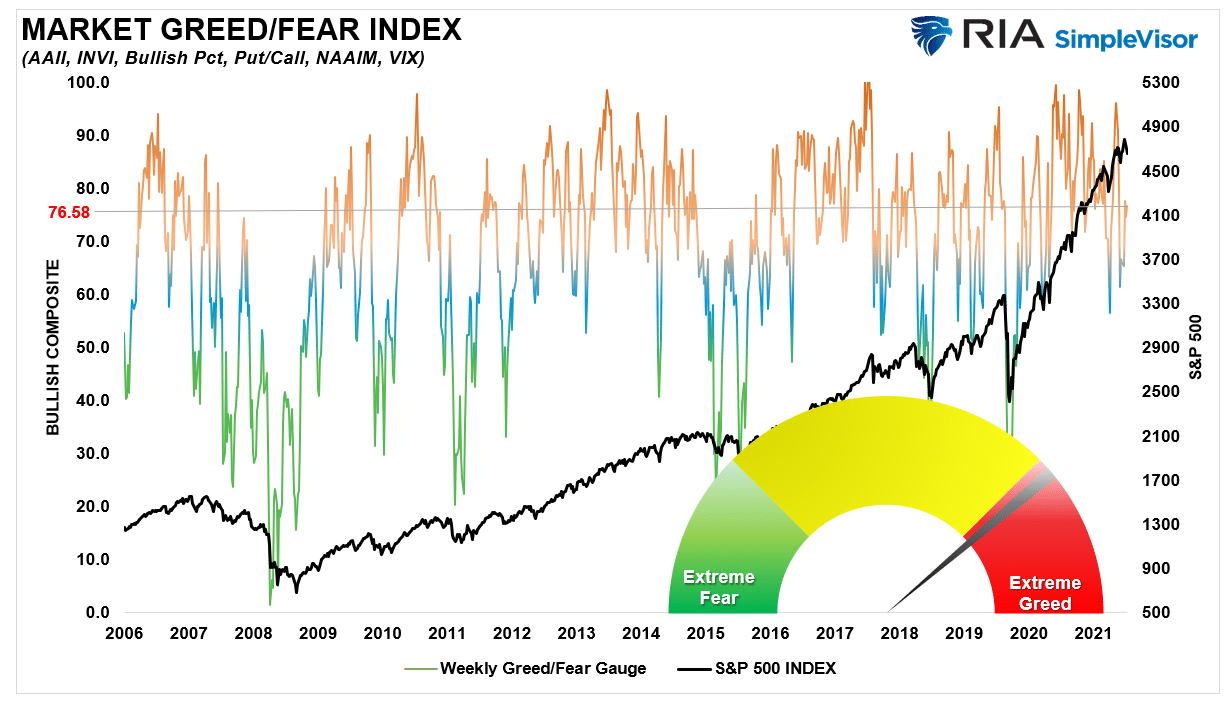

Portfolio Positioning “Fear / Greed” Gauge

Our “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0-100. It is a rarity that it reaches levels above 90. The current reading is 76.58 out of a possible 100.

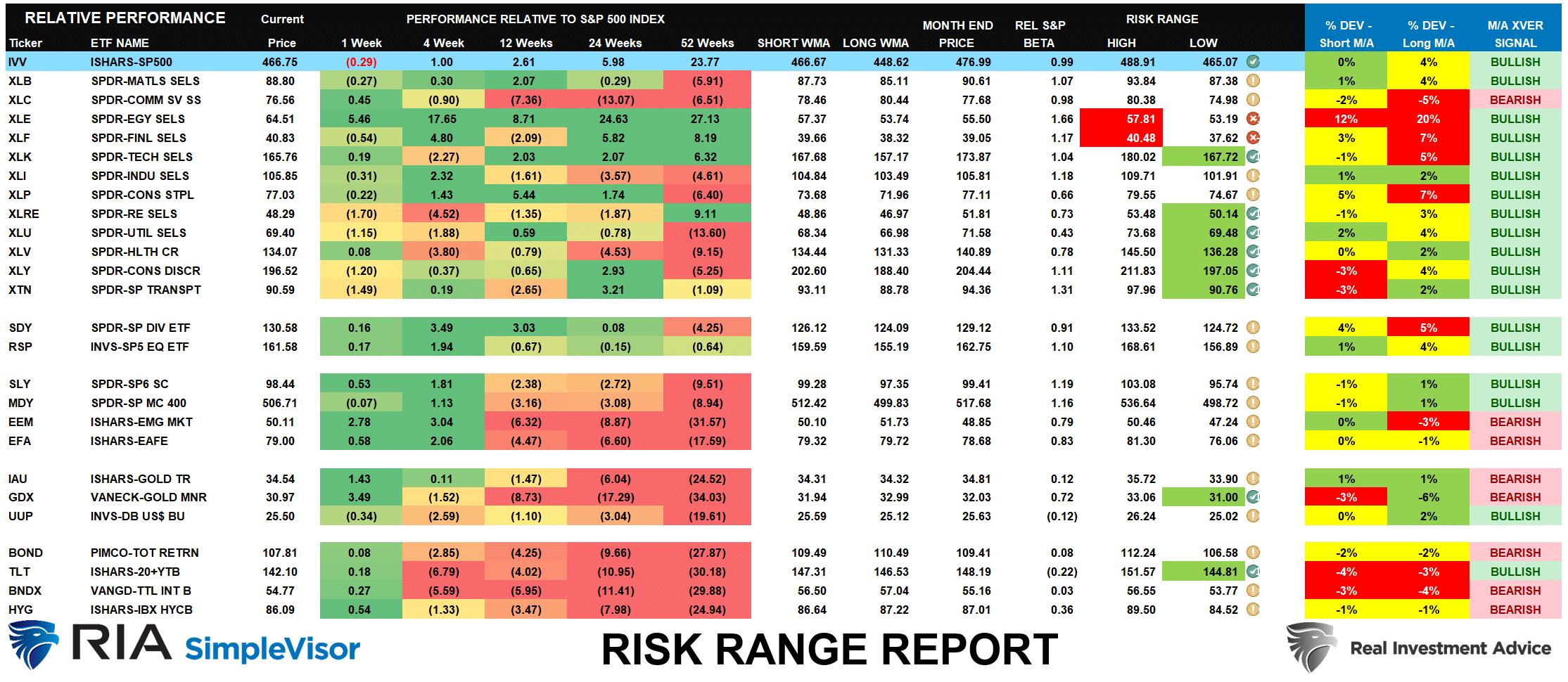

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares each sector and market to the S&P 500 index on relative performance.

- “MA XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- Table shows the price deviation above and below the weekly moving averages.

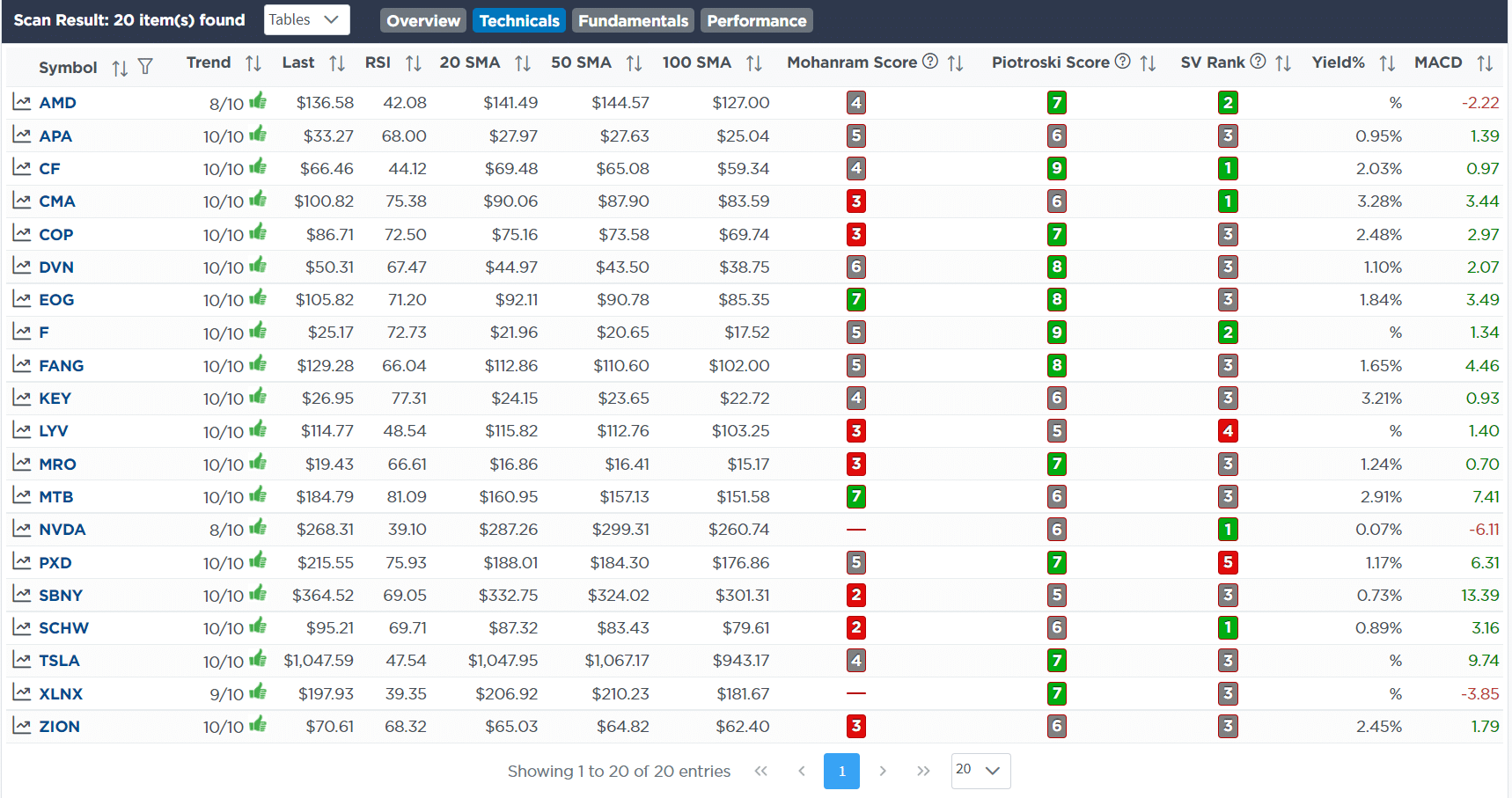

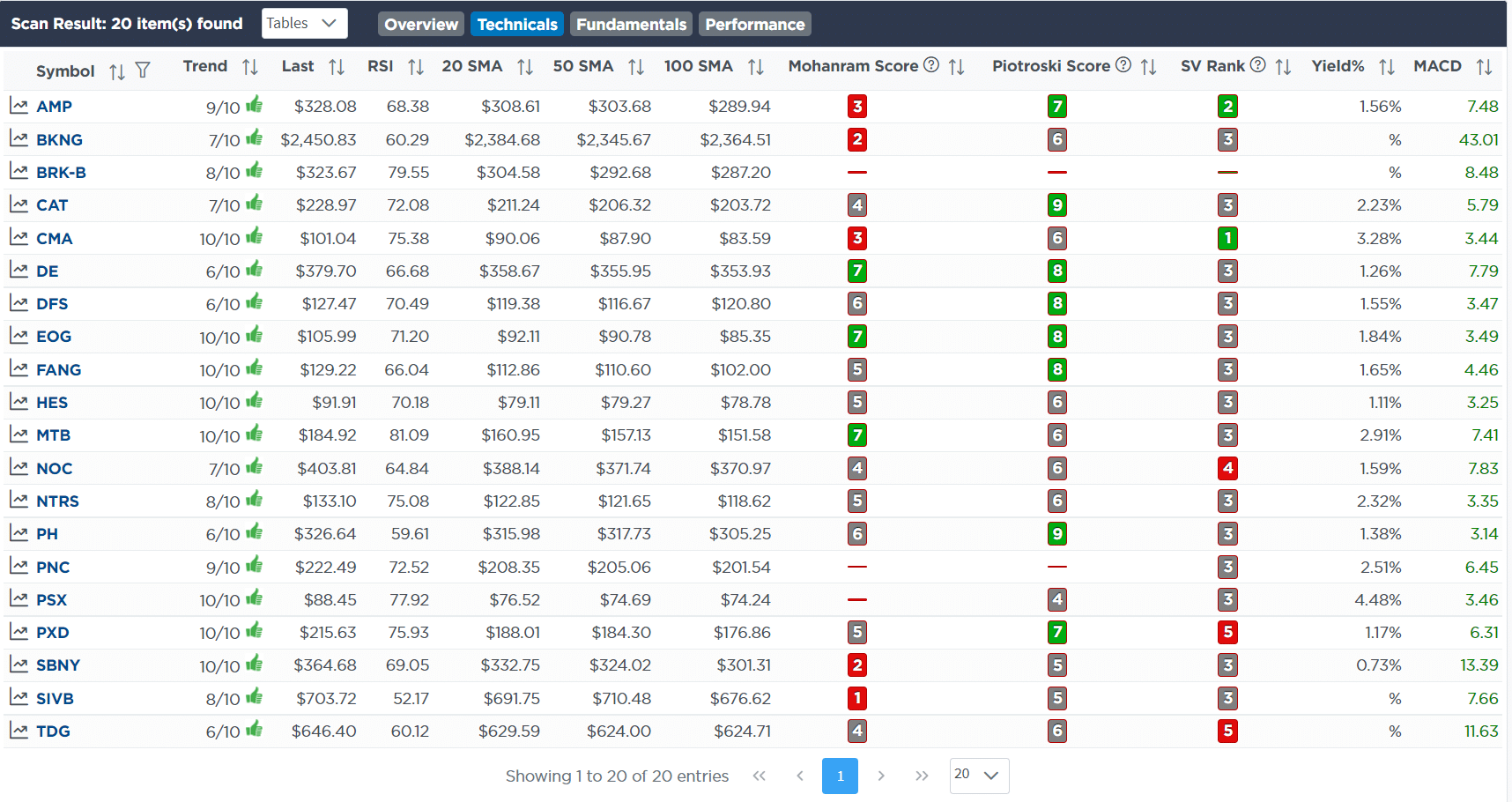

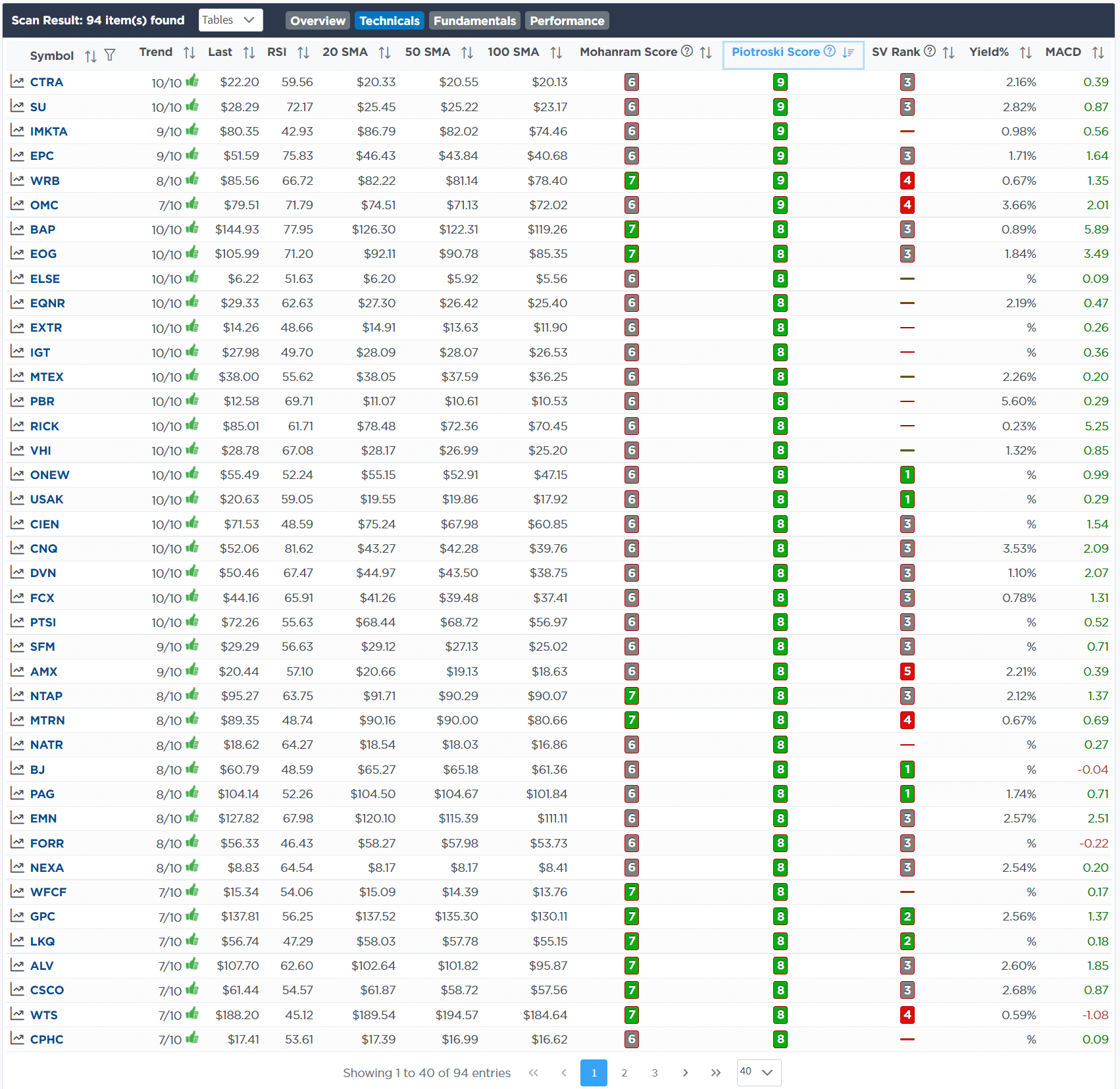

Weekly Stock Screens

Each week we will provide three different stock screens generated from SimpleVisor: (RIAPro.net subscribers use your current credentials to log in.)

This week we are scanning for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Technically Strong With Strong Fundamentals

These screens generate portfolio ideas and serve as the starting point for further research.

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Technical & Fundamental Strength Screen

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

“After having previously reduced our holdings in TLT, the recent decline in bond prices has now pushed TLT to more extreme oversold levels. Importantly, when the Fed begins its rate hikes and tapering program, historically rates fall as the markets enter into a “risk-off” mode. To capitalize on that trade we are using the recent decline in bond prices to increase our duration in the portfolio as a hedge against our long-equity positions.” – 01-13-22

- Add 1% of the portfolio to TLT increasing total weighting to 8%.

Lance Roberts, CIO

Have a great week!