The graph below shows that 5yr yields have risen over 2% in 2022. Many in the media ascribe the yield surge to rising inflation expectations. However, as we offer below, two well-followed measures of 5-year inflation expectations have been relatively flat for the last few months. The question then is, what gives?

First, with many risk assets falling in price, liquidity is required to meet margin calls. Treasury securities are the world’s most liquid assets, and its likely investors may be selling them to meet such demands. Second, the Bank of Japan (BOJ) has capped the yield on its 10-year note at .25%. To defend the cap, the bank must buy its bonds whenever the yield approaches .25%. Such actions typically pressure the yen lower. Might the BOJ be selling Treasury bonds to provide the means to buy their notes and to keep the yen from falling further? The yen is down 15% year to date.

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended June 10 (-6.5% prior)

- 8:30 a.m. ET: Empire Manufacturing, June (2.5 expected, -11.6 prior)

- 8:30 a.m. ET: Retail Sales Advance, month-over-month, May (0.1% expected, 0.9% prior)

- 8:30 a.m. ET: Retail Sales excluding autos and gas, MoM, May (0.4% expected, 1.0% prior)

- 8:30 a.m. ET: Import Price Index, MoM, May (1.1% expected, 0.0% prior)

- 8:30 a.m. ET: Import Price Index excluding petroleum, MoM, May (0.6% expected, 0.4% prior)

- 8:30 a.m. ET: Import Price Index, year-over-year, May (11.9% expected, 12% prior)

- 8:30 a.m. ET: Export Price Index, month-over-month, May (1.3% expected, 0.6% prior)

- 8:30 a.m. ET: Export Price Index, year-over-year, May (18.0% prior)

- 10:00 a.m. ET: Business Inventories, April (1.2% expected, 2.0% prior)

- 10:00 a.m. ET: NAHB Housing Market Index, June (67 expected, 69 prior)

- 2:00 p.m. ET: FOMC Rate Decision, lower bound, June 15 (1.25% expected, 0.75% prior)

- 2:00 p.m. ET: FOMC Rate Decision, higher bound, June 15 (1.50% expected, 1.00% prior)

- 2:00 p.m. ET: Interest on Reserve Balances Rate, June 16 (1.40% expected, 0.90% prior)

Earnings

Pre-market

- No notable companies are expected to report.

Post-market

- No notable companies are expected to report.

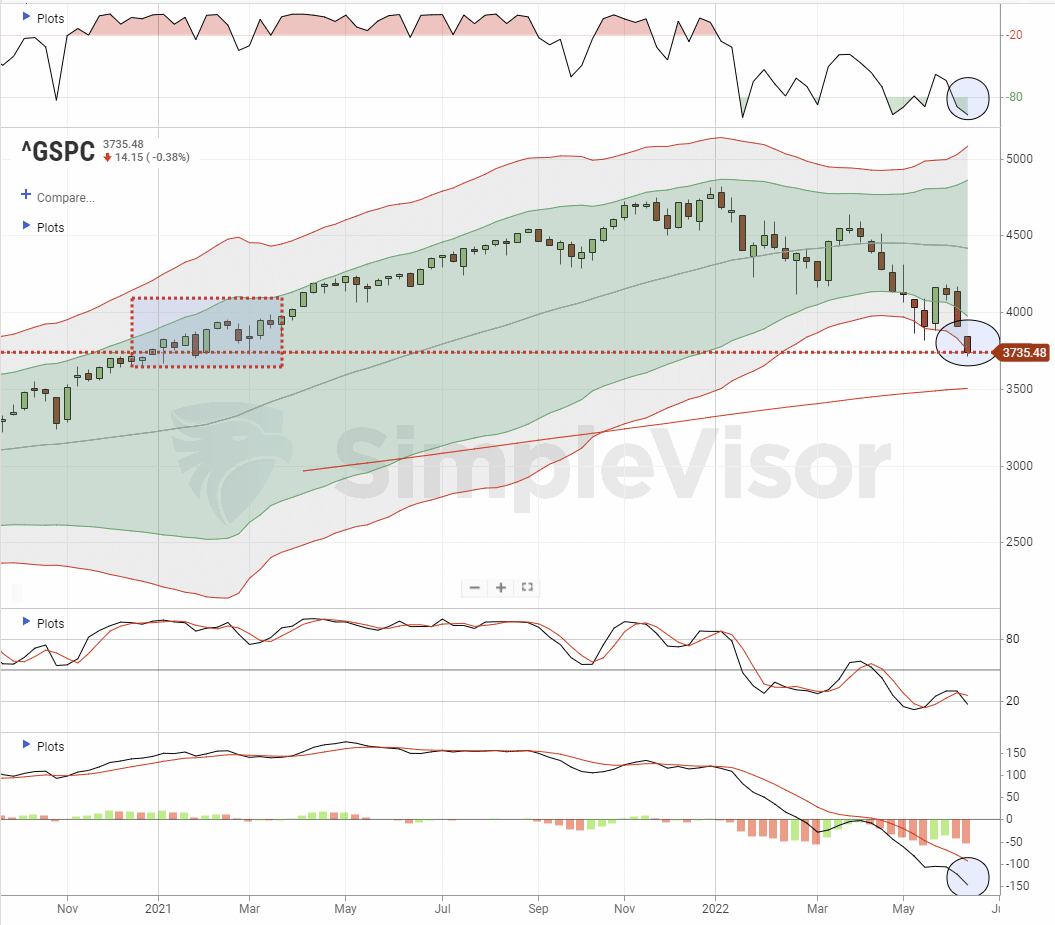

Market Struggles To Find Footing

Yesterday, the market struggled to find some footing ahead of the FOMC meeting announcement this afternoon. Notably, the waterfall decline since last Thursday put the markets back into a deep, weekly oversold condition. While inflation expectations remain muted, the markets are pricing in more aggressive Fed rate hikes.

Yesterday, we covered half of our short-S&P 500 ETF position for this reason as a short-term bounce is likely. While the forward outlook for the market remains weak as the Fed tightens policy, fairly strong rallies should be expected to previous levels of resistance. Currently, our target for a short-term rally is roughly 4000 but a retracement to 4400 on the S&P 500 index is possible.

Fed Preview

What we thought would be a “boring” Fed meeting today may be anything but that. While implied inflation expectations are reasonably stable, Fed concerns about inflation seem to be rising. Recent articles from Nick Timiraos (WSJ), often a source of intentional Fed leaks, wrote on Monday about the potential for a 75bps rate hike. Wall Street seems to be getting behind that idea as well, with many banks forecasting a 75bps increase. So what happens to stocks and bonds if they only go 50 or raise by 75?

Our question is tough to answer. If the Fed only goes 50, stock investors may breathe a sigh of relief, but bond investors may worry as the Fed is not vigilant enough on inflation. Higher yields may likely, in that case, translate to lower stock prices in time. If they go 75, bonds may rally, but stock investors may fret that such aggressive action will ensure a recession. That said, stock investors may applaud 75 as the Fed wants to tackle inflation sooner rather than later. As you can tell by the array of outcomes, it is anyone’s guess. Further complicating the matter is a massive options expiration on Friday. It is quite likely the Fed meeting will usher in volatility through the remainder of the week.

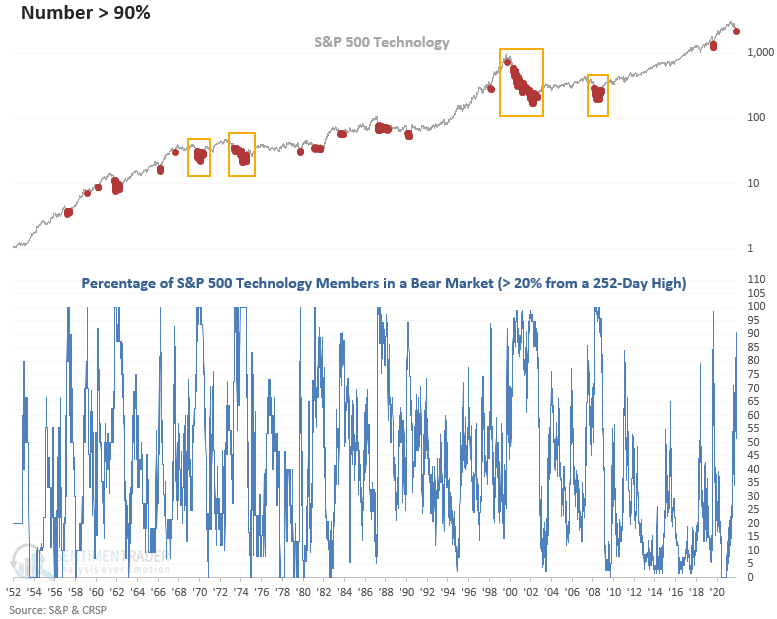

90% Of Tech Stocks Are In A Bear Market

“For only the second time in more than a decade, the number of Technology stocks in a bear market exceeded 90%. Several cases like 2007-08, 2000-02, 1973-74, and 1968-70 maintained a high level of stocks in a bear market for a significant amount of time, especially 2000-02.” – Sentiment Trader

Dollar is Surging

The graph below shows the dollar index has been on a tear over the last year. Since May 2021, the index is up over 15%. The appreciation is primarily a function of the Fed’s hawkish monetary policy and the relative dovishness of other large central banks. The ECB, for instance, is just starting to raise rates and will not embark on QT. The BOJ is still one of the rare dovish central banks left. While the difference in monetary policy may remain, the dollar may not strengthen further. An appreciating dollar is bad for exports and encourages imports, weighing U.S. corporate profits. A stronger dollar will help keep import prices down, which may help temper inflation. Conversely, Europe and Japan can ill afford more inflation and may likely step in to arrest the decline in their currencies.

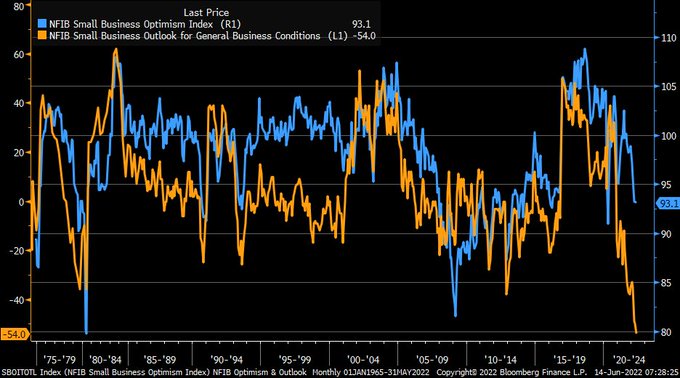

Small Businesses Outlook Worst in 48 Years

As we discussed last week, the University of Michigan Consumer Sentiment Expectations Index sits just shy of 80-year lows. The most recent NFIB Survey paints a similar picture about the expectations of small business owners. The NFIB Index is falling and now sits at 5-year lows, but the NFIB expectations index is plummeting. Per the Report:

The NFIB Optimism Index fell 0.1 points in May to 93.1, marking the fifth consecutive month below the 48-year average of 98. Owners expecting better business conditions over the next six months decreased four points to a net negative 54%, the lowest level recorded in the 48-year-old survey. Expectations for better business conditions have deteriorated every month since January.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read