All Quiet on the Western Front is a 1929 novel which describes German soldiers’ extreme physical and mental stress during World War I, and subsequent detachment from civilian life felt by many soldiers upon returning home. This novel was eventually made into a major motion picture.

The phrase “all quiet on the Western Front” has become a colloquial expression meaning stagnation, or lack of meaningful change, in any context.

Many financial markets ended 2018 with considerable volatility. The stock market, as measured by the S&P 500 index, fell from its peak in early October to a December 26th low by over 21%. The WTI crude oil market fell from an October peak over $77/bbl to a December 24th low near $42/bbl, a 45% decline. The natural gas market spiked considerably in November, only to fade significantly in December. At least one hedge fund, optionsellers.com, was forced to shutter from these extreme moves in price.

Since the beginning of 2019, stock market volatility has been subdued (at least in comparison to the fourth quarter). The average trading ranges for the S&P 500 index has diminished considerably, at least for now. In hindsight, we might view some of the large market moves in late 2018 to have been end-of-year positioning and/or profit taking, with January as a mean-reversion month.

January has largely been “quiet on the Midwestern front.” “Midwestern” is used here because the most influential options markets are conducted on Chicago exchanges –CME Group and the CBOE. Many readers may be surprised to learn that some options markets actually have more value at risk than the futures and cash markets themselves. In some cases and on certain days, the options market can become the tail that wags the dog of the underlying markets.

Op-ex Price Magnets

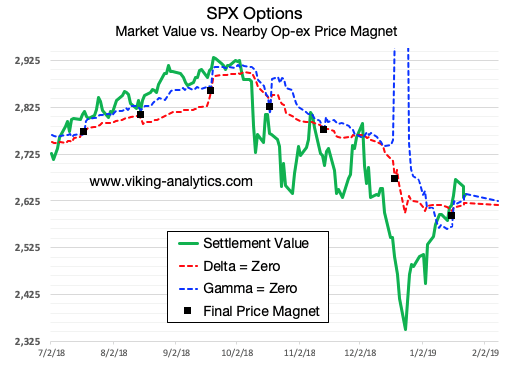

Over the last several years, we have developed a trading indicator that relies on mean-reverting behavior in about a dozen markets. The Op-ex Price Magnet is our proprietary tool which shows where options markets have priced in an “ideal” option expiration price, the value at which total market delta is neutral. We can demonstrate mean-reversion behavior towards market delta neutral in many different markets and exemplified by the graph below.

This tool can be considered to be an “options sentiment index,” and therefore it is not necessary to trade futures or even options to use the tool. As a sentiment indicator, the Price Magnet tool shows where the market makers are expected to maximize profits for about a dozen different markets. Here is a sample graph for the S&P 500 options traded on CBOE.

There are two important dynamics to consider in the graph above. First, the price (the green line) will often mean-revert back to the point of delta neutral (the red line). This dynamic can be attributed to order flow and market maker positioning into options expiration.

The other dynamic – seen in late December – shows where gamma can spike, resulting in a “gamma covering” event. We believe that the sharp declines in and around Christmas can be attributed in part to forced selling by the market makers to bring their gamma back in line by covering their options losses. A similar dynamic happened in the natural gas market in and around the time that optionsellers.com was forced to liquidate.

This is a relatively complicated topic, so we encourage readers to visit our website or send us an e-mail if you have specific questions on this methodology. As a practical consideration, our published articles on trading the S&P 500 index during 2018 resulted in successful trades more than 80% of the time (verifiable through Seeking Alpha).

Friday, January 18th was the first monthly expiration for S&P 500 (SPX) options, stocks and ETFs. This week there is a monthly expiration for grains and US Treasury futures. Next week, there is a monthly expiration for both gold and natural gas. We don’t currently see high probability mean-reversion trades in any of these key markets, but that could change quickly.

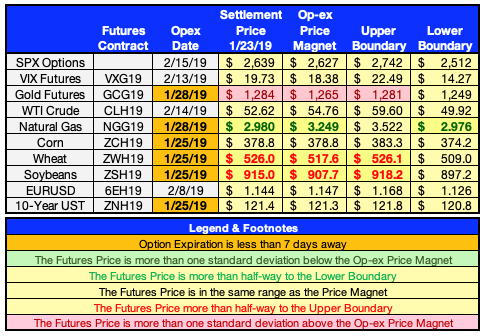

The following table is an example of the summary data that is included in our daily reports.

Thank you for reading our work and we look forward to providing more guidance on markets that have strong Price Magnets into option expiration.

Erik Lytikainen, the founder of Viking Analytics, has over twenty five years of experience as a financial analyst, entrepreneur business developer and commodity trader. Erik holds an MBA from the University of Maryland and a BS in Mechanical Engineering from Virginia Tech. You can learn more about his work on his website: www.viking-analytics.com.

Also Read