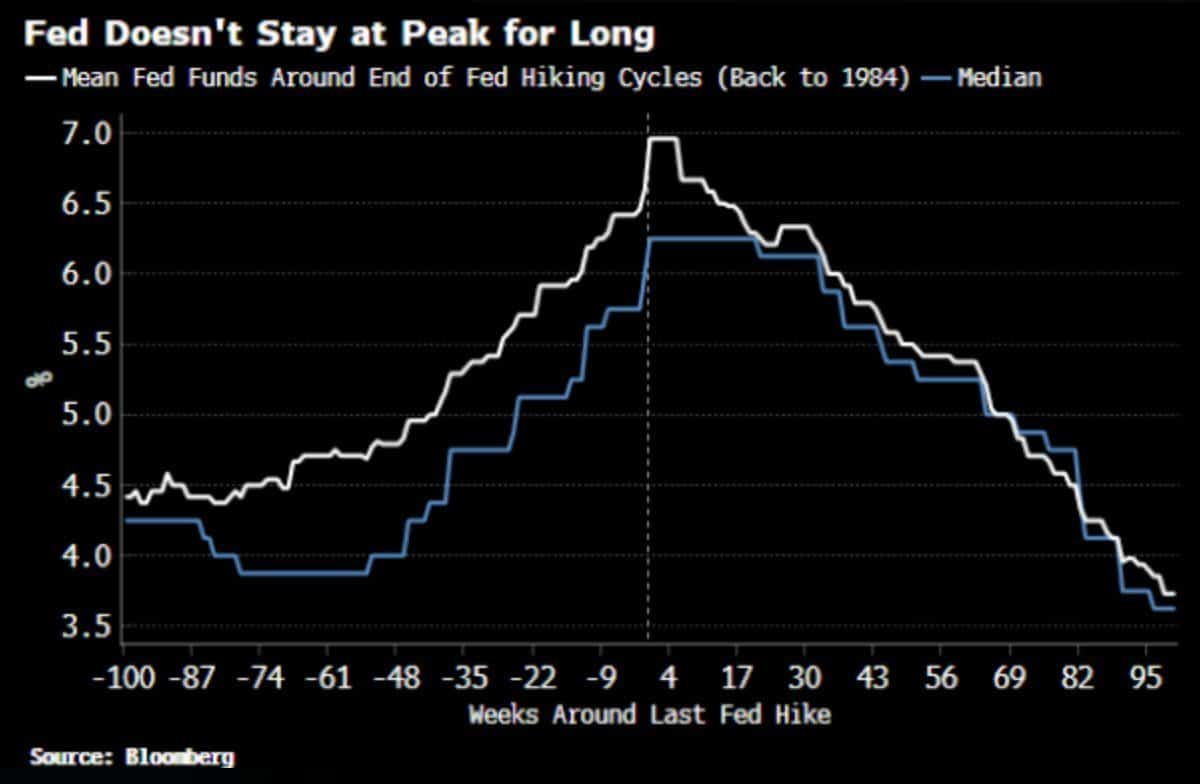

Yesterday’s Commentary, Is the Fed Done, contemplates whether or not Wednesday’s rate hike was the last for the cycle. If it was, as many seem to think, the next question for investors should be how long until the Fed cuts rates. Yesterday’s Commentary shared a table with market-implied Fed rate cut probabilities. A day after the meeting, with the banking crisis accelerating, investors expect a 50% chance for the first 25 basis point rate cut in July. The market expects the Fed to cut rates by almost 2% by this time next year.

While Powell and Fed keep chanting “higher for longer,” history argues Fed rate cuts could be coming by this summer. As we share below from Bloomberg, Fed pauses do not last very long. However, this time is different. Inflation is well above the Fed’s 2% target, forcing them to keep rates high unless “something breaks.” What may break? Regional banks are breaking, and the situation is starting to become worrisome. The Fed will be forced to react. Will they add liquidity backstops for troubled banks or will it resort to cutting rates? Assuming the banking situation calms down, the Fed will likely pause until the economy slows materially and the unemployment rate increases substantially. Until those occur, inflation will likely remain sticky.

What To Watch Today

Economics

Earnings

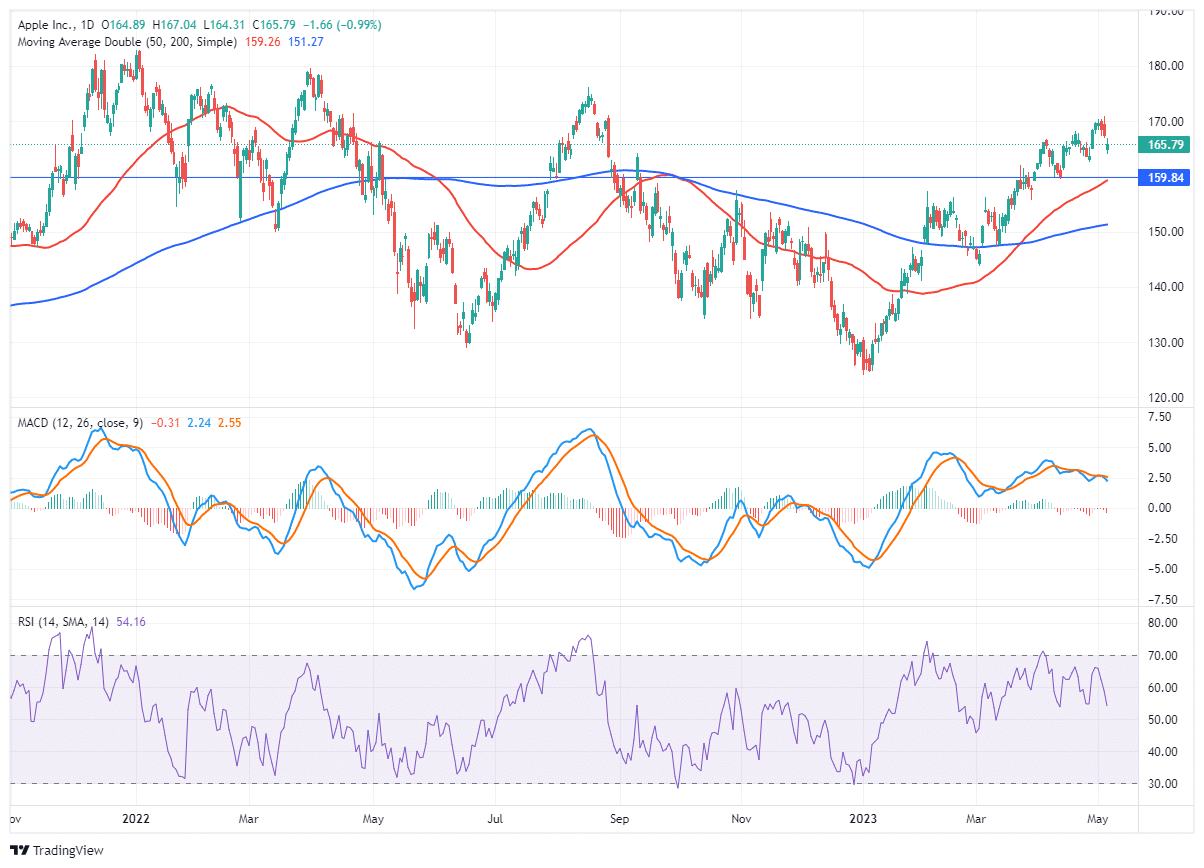

Market Trading Update

Despite concerns about bank failures plaguing the financial sector, the market currently remains extremely resistant to a sell-off. Yesterday, the market fell slightly as markets digested the Fed’s latest rate hike, and several regional banks plunged sharply on liquidity concerns. PacWest (PACW) declined nearly 50% on the day, while Western Alliance (WAL) fell more than 38%.

However, after the bell Apple (AAPL) reported earnings that beat estimates on stronger-than-expected iPhone sales. Given its size in the major indices, it will likely support any further weakness in the market today. Apple has been a long-term holding in our portfolio, and we have been looking for opportunities to add more to the position. While earnings were good, Apple remains on a short-term MACD sell signal, suggesting prices could struggle near-term to consolidate some of the recent gains from the October lows. Ideally would like a pullback that reduces the short-term overbought condition and provides a better entry point to increase exposure.

Jobless Claims Tick Higher, and Labor Costs Soar

Initial jobless claims, a good leading indicator for employment, ticked up to 242k from 229k. While not a concerning number, there is clearly a weakening in the labor market. Continuing claims fell slightly to 1.805 million. The labor market is generally considered healthy if jobless claims are below 275-300k and continuing claims are below 2 million.

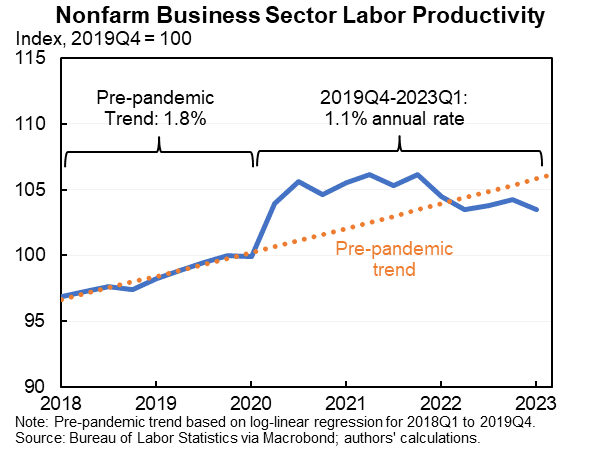

Unit labor costs grew much more than expected at +6.3%, up from 3.2% in the fourth quarter. As a result, first-quarter productivity fell by 2.7%. This data does not speak to economic activity per se but does portend that corporate profit margins are likely under pressure. Basically, the numbers say corporations are paying more in wages but getting less for the money.

The graph below shows that productivity rose during the pandemic as companies could pass along higher prices without boosting wages. Workers were in short supply as the economy recovered and wages rose. As a result, productivity is now below the pre-pandemic trend.

Stocks, Oil, and Bonds

The graph below from Fusion Point Capital shows that stocks, oil, and bonds are simultaneously resting on key support and resistance trend lines. It’s likely a break above resistance or below support for one of these markets may set the tone for the rest.

Repossessing Harleys Are Not Easy

Bloomberg published an interesting article describing how Harley Davidson struggles to repossess motorcycles from delinquent borrowers. We presume repossessing a Harley may be more dangerous than a Prius and, therefore, Harley may find it harder to employ repossession employees. However, the article talks about a bigger issue. Many financial lenders are in similar shoes as Harley. Consequently, they may not be able to recover as much value on delinquent loans as they could have before the labor shortage.

The repossession industry is seeing an uptick in demand as more Americans struggle to afford their car payments. And companies that specialize in seizing vehicles are having trouble hiring enough agents, after many decamped for other jobs during the pandemic when business largely dried up due to stimulus measures.

For Milwaukee-based Harley, the repo shortage combined with a decline in retail bike values. That contributed to realized credit losses of about $52.6 million in the first quarter for the company’s financial arm, vice president and treasurer David Viney said on a conference call Thursday.

“A lot of people left the repossession industry during Covid,” Viney said.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.