“Increased borrowing must be matched by increased ability to repay. Otherwise, we aren’t expanding the economy – we’re merely puffing it up.” – Henry Alexander of Morgan Guaranty Trust

The original Potemkin Village dates to the late 1700s. At that time, Russian Governor Grigory Aleksandrovich Potemkin constructed facades to hide the poor condition of his town from Empress Catherine II.

Since then, Potemkin Village represents a false construct, physical or narrative, created to hide the actual situation.

As the pandemic ravaged the economy, the Federal Reserve, White House, and Congress went to work and built a Potemkin economy around the ailing economy.

As a result, the curb appeal of today’s economic recovery is beautiful. However, when our clients’ wealth is at stake, we understand looks can be deceiving. As such, we prefer to open the front door and explore the real economy. In the long run, it is sustainable economic growth that supports asset prices. In the short run, however, investors may continue to be mesmerized by the Potemkin economy. At some point, any differences between the Potemkin economy and the actual economy will become problematic for investors.

Selling A Narrative

Narratives of a booming economic recovery can only mislead the public and investors for so long. Toss in robust economic data, and the façade seems awfully real.

Consider the following:

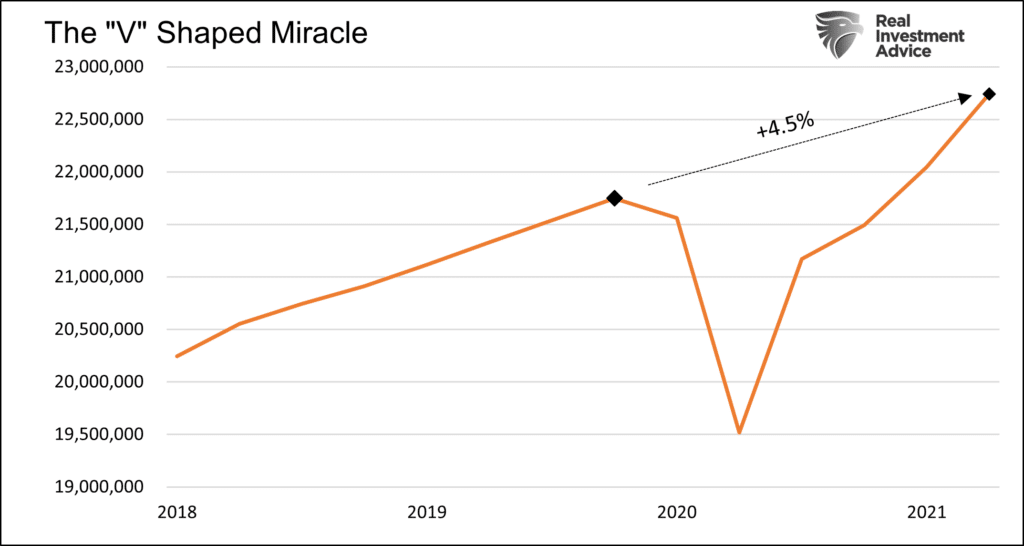

Nominal GDP is now 4.5% above the high-water mark set pre-pandemic. Historically, economic recoveries do not get more “V-shaped!”

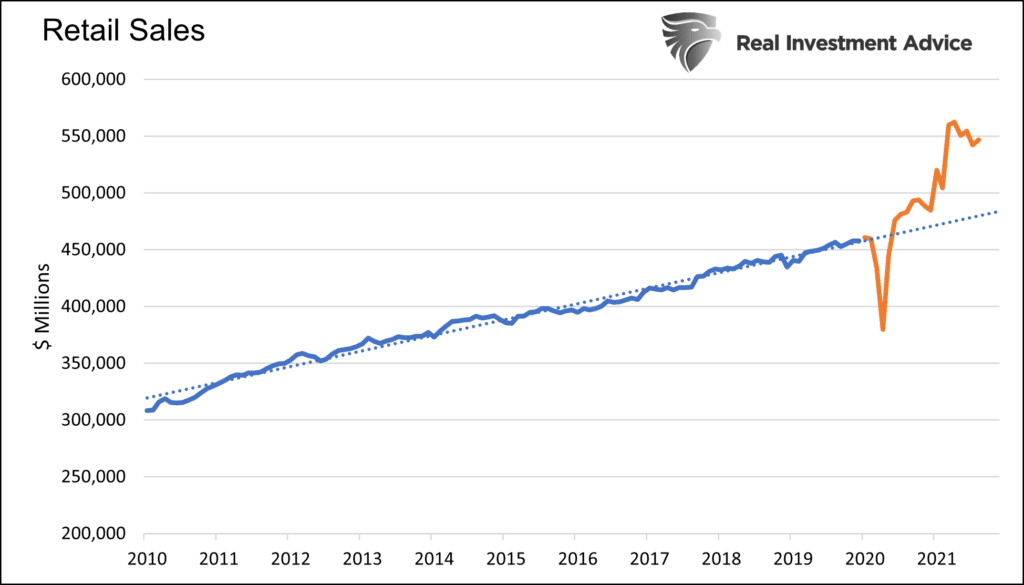

Retail Sales are running about 12% above its trend of the last ten years. The premium represents nearly five years of growth at the prior trend.

CPI and Core CPI (excluding food and energy) are nearly triple their respective growth rates of the last five years.

The ISM Purchasers Managers Index, measuring manufacturers sentiment, was recently at its highest level in over 30 years. The ISM Services Index is at the highest level in over 25 years.

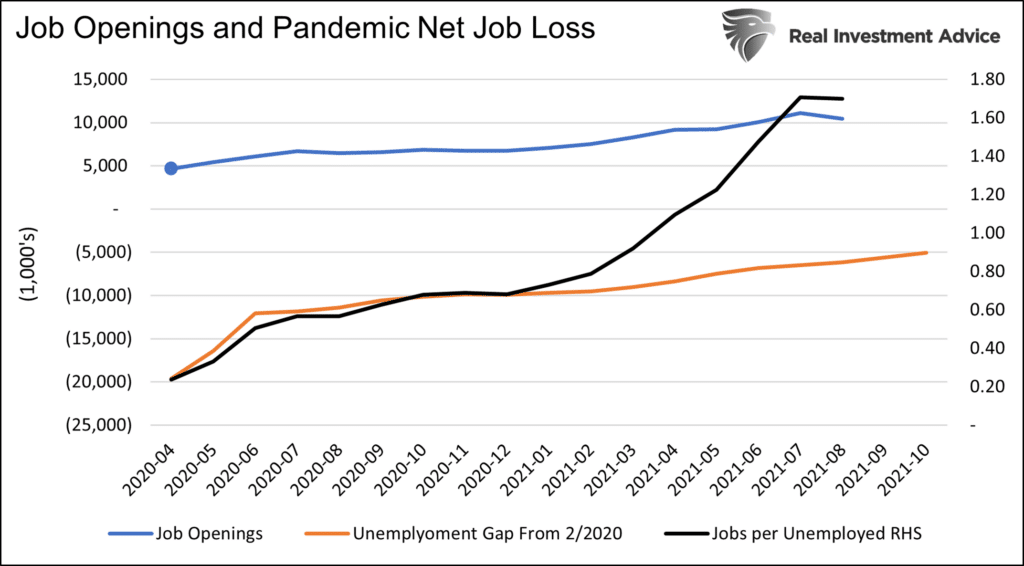

Many other measures of economic activity are fully recovered or will be shortly. The only major economic data point under some pressure is employment. Even that, however, is improving sharply from the Pandemic lows. In What A Rate Hike Might Mean For “Stonks,” we quantify that it too is fully recovered. Supporting our belief is the fact there are more job openings than unemployed people.

The Real Economy

There is no doubting economic data is incredibly strong. However, what’s essential to understand is whether the economic activity is durable and sustainable or just a flimsy façade propped up by weak timbers that will erode in short order. To examine the recovery properly and its staying power, we must examine the impetus behind it.

The pandemic recession was atypical. The global economy shut down in an unprecedented manner. To offset lost activity, the fiscal response from the government was massive.

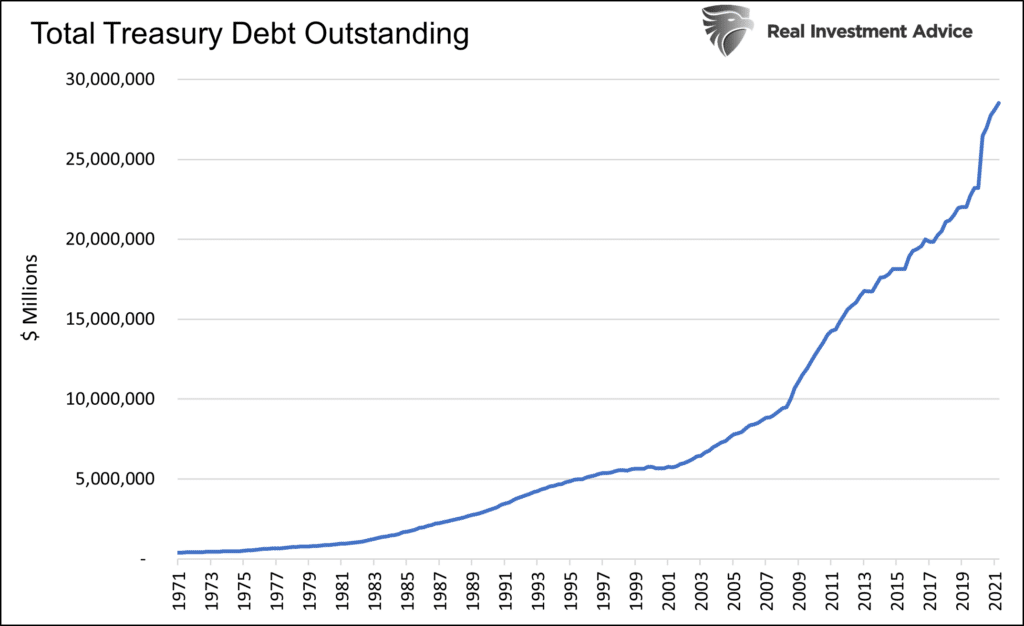

As shown below, Federal Debt outstanding rose by over $5 trillion in a little more than a year. As a comparison, debt increased by a little over $2 trillion during the 2008/09 financial crisis. Debt has grown at about six times the rate of the economy since the pandemic began.

As a percentage of GDP, the current deficit is more significant than during the Civil War, WWI, Great Depression, and the Financial Crisis. Only the deficit funding WWII surpassed current levels.

Backstopping the Treasury

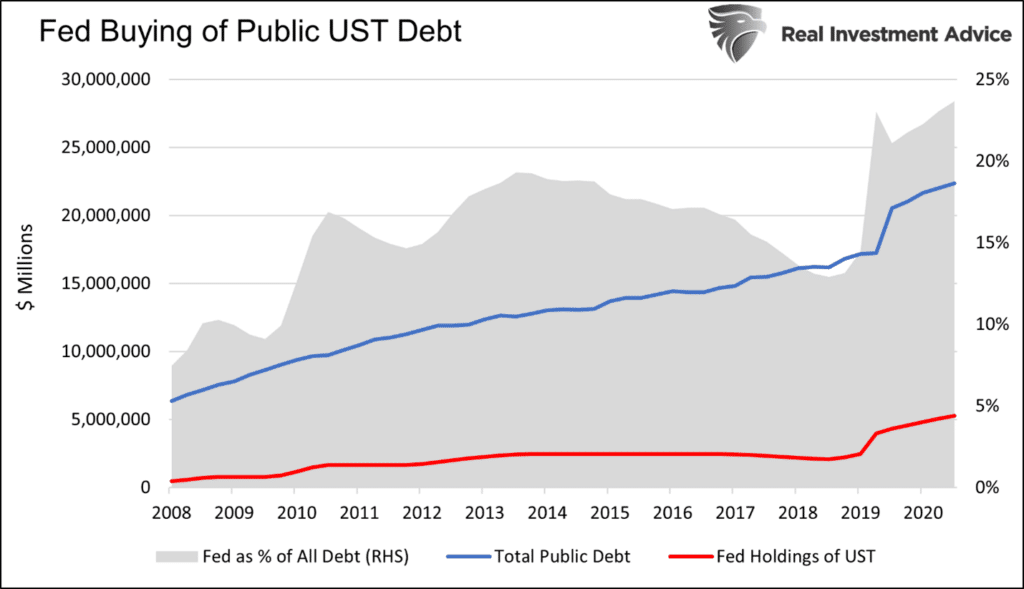

Before the pandemic, the level of government debt was already at record highs and climbing faster than economic growth. The only way to keep such a scheme going is to continually lower interest rates to manage the federal interest expense. Since interest rates are already at record lows, the Fed also buys a considerable amount of bonds, effectively reducing the amount of debt outstanding.

Over the last year, the Fed bought more than half of the Federal debt issued. The graph below shows the Fed now holds 25% of all public Treasury debt outstanding. After the financial crisis, the percentage was less than 10%.

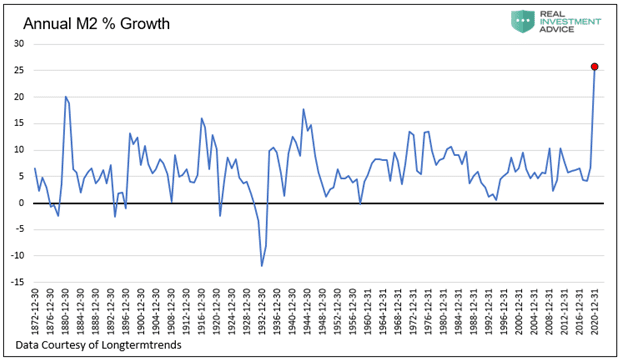

The following graph puts the growth of the Fed’s balance sheet into context. The resulting rise in annual M2 money supply growth is the largest since at least the Civil War.

Illustrating The Facade

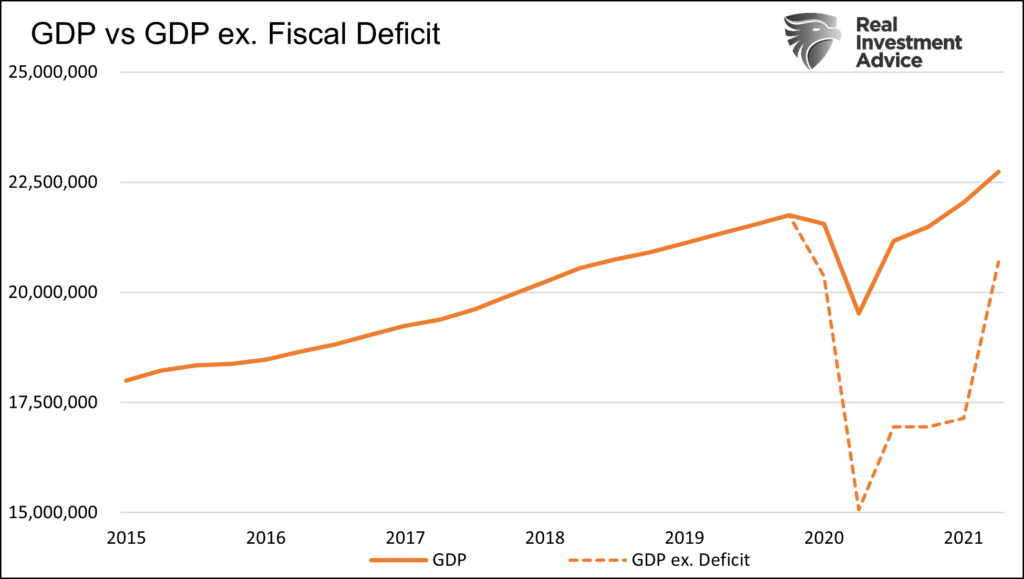

The graph below shows how government spending greatly boosted GDP The orange line shows GDP has fully recovered from the pandemic. The dotted-orange line, subtracting government spending from GDP, shows the organic economy is still 5% below pre-pandemic levels. That is in stark contrast to GDP, which is running almost 5% above pre-pandemic levels.

Will the Façade blow over?

If something can’t go on forever, it will eventually stop.

This article is not about whether the government should have supported the economy, and if so, to what degree. We leave politics at the door.

What we care about is understanding how long the economic recovery façade can last. To do so, we need to study the foundation of the façade.

The timbers and beams forming the façade are massive federal spending. The foundation supporting government spending is the Federal Reserve. Specifically, purchasing Treasury securities and keeping interest rates at zero allows the Treasury to borrow at will with minimal impact on the bond markets or the government’s interest expense.

Despite recent reductions, the Fed is still buying bonds at a $105 billion monthly pace and pledging to keep interest rates at zero. The internal and external pressure on the Fed to fight inflation is increasing. However, the Fed seems intent not even to discuss raising interest rates.

Headwinds to QE and Ultimately our Facade

Politicians, economists, and even some Fed Presidents are increasingly concerned inflation may be persistent. “Transitory,” a term to describe a short bit of higher inflation, seems to be overstaying its welcome. To wit, Senator Rick Scott recently penned a letter to Powell. In it he says he will not support his renomination unless the Fed focuses on inflation and starts winding down excessive monetary policy.

“I cannot stand idly by as the Federal Reserve continues its current path of foolishly ignoring rising inflation that is hurting American families. Further, I am gravely concerned by the Federal Reserve’s inaction in winding down its unprecedented market intervention and increased purchase of federal government debt as well as the increased politicization of the Federal Reserve itself that has occurred under your watch.”

Persistent, not transitory, inflation poses significant problems for the Fed. To combat inflation, the Fed needs to raise rates and stop QE. If that doesn’t work, they would likely sell assets on their balance sheet. If the Fed tightens policy via the steps above, the Treasury’s job becomes much more complex and costly.

Sustained inflation will weaken the foundation of the facade and blow our Potemkin economic recovery over.

Summary

As long as the foundation for the Potemkin economy can withstand economic and market pressures, our façade can last. However, there are limits to what the Fed can do. Inflation is one such limiter. If the Fed can thread the needle and taper QE but still adequately support post-crisis Treasury deficits, the façade may last longer than we think.

If, however, inflation, political pressures, or other factors cause the Fed to slam on the brakes, our foundation will crack, and the Potemkin economy will fall, revealing a much worse state of the economy than most investors understand.

The economy is not robust. As Alexander says, “we are puffing it up” with fiscal and monetary gimmickry.