Wednesday’s Home Purchase Index fell sharply to the lowest level since 1995. The index compiled by the Mortgage Bankers Association (MBA) computes the number of home purchases based on a sample of approximately 75% activity. The combination of elevated home prices and mortgage rates approaching 7% keeps individuals from buying houses or even seeking out mortgage applications. The MBA mortgage application index is also near 28-year lows.

The most recent Case-Shiller Home Price Index has fallen but still stands almost 20% above trend. In addition to high prices, mortgage rates keep the affordability of homes out of range for many potential buyers. While the demand side of the housing market is troubling, owners aren’t selling. The supply of existing homes is under three months. Compare that to the relatively hot housing market in the five years pre-pandemic when the supply was never below three months! The chart below of the MBA home purchase index is courtesy of Mish Shedlock.

What To Watch Today

Economics

- 8:30 a.m. ET: Q4 Nonfarm Productivity (est. 2.5%)

- 8:30 a.m. ET: Q4 Unit Labor Costs (est. 1.6%)

- 8:30 a.m. ET: Weekly Initial Jobless Claims (est. 195,000)

- 8:30 a.m. ET: Weekly Continuing Jobless Claims (est. 1,669,000)

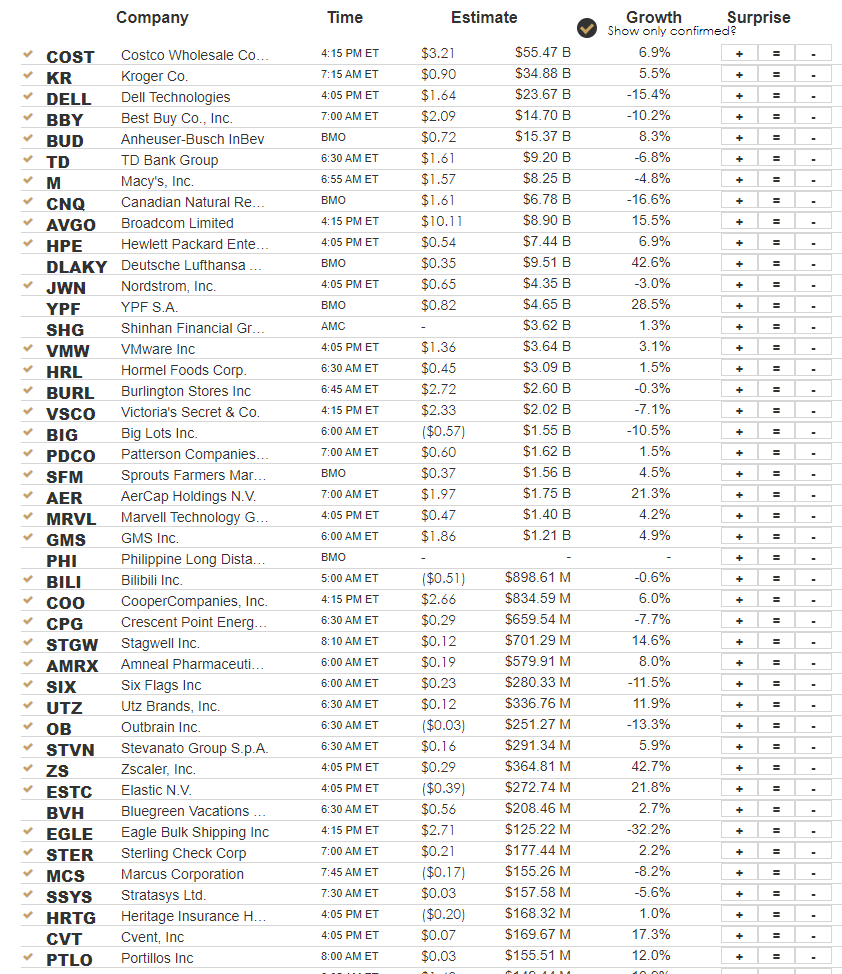

Earnings

Market Trading Update

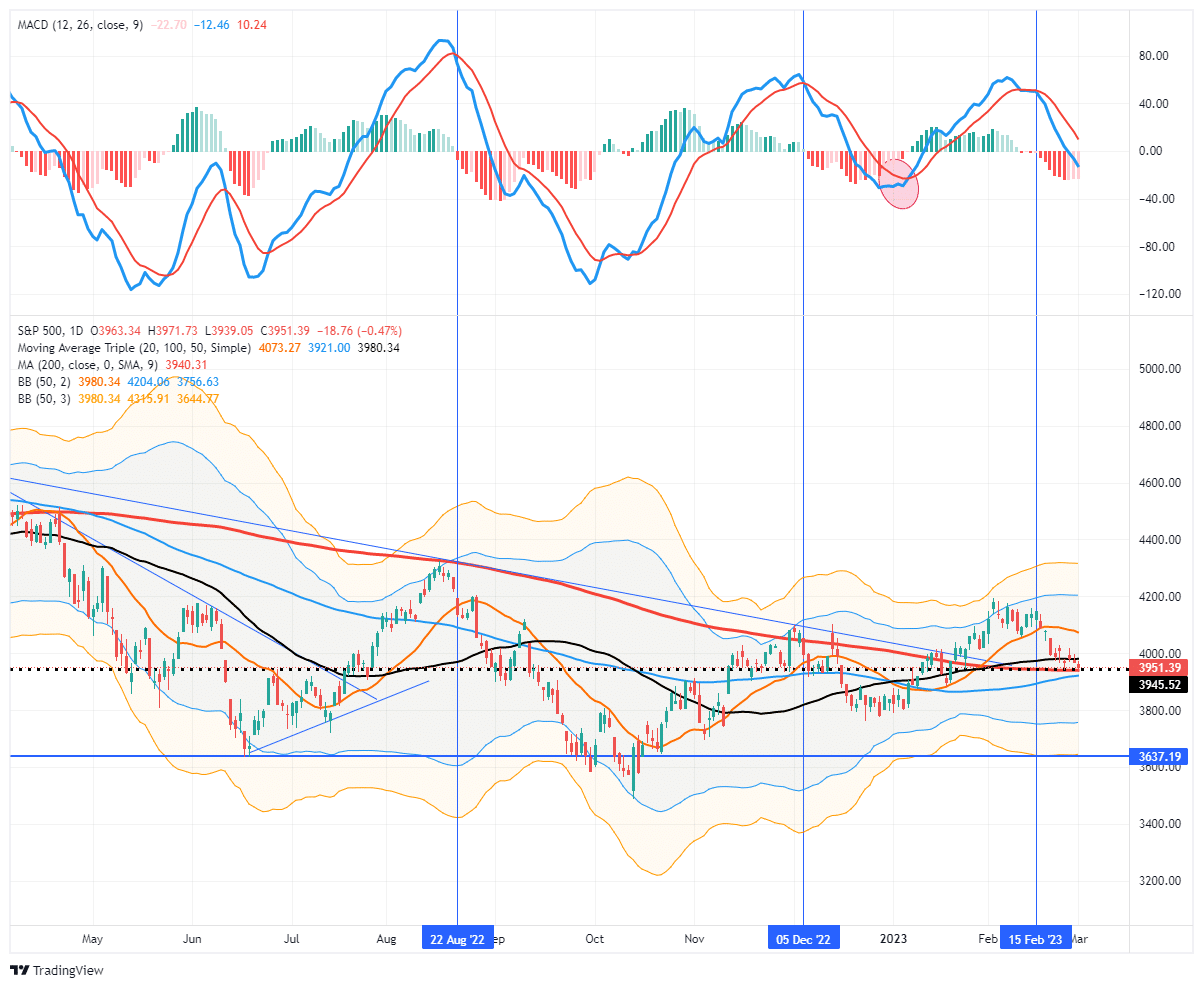

It’s make-or-break time for the S&P 500 as the market closed on the 200-DMA yesterday, coinciding with the top of the downtrend line from the January 2022 peak. With the market now oversold on a short-term basis, following two weeks of steady selling pressure, a rally today or tomorrow will not be surprising.

Here is the important point. If the market breaks support at the 200-DMA, it is advisable NOT to sell down exposure immediately. The reason is that there has been a lot of selling pressure by the time the market breaks a support level. With sellers likely exhausted short-term, we often see initial breaks of support retraced in the next couple of days. Be patient, and wait for a bounce to see if the broken support is retaken or a failed test. If the market rallies to previous support and fails, it will be a confirmed break, and equity risk can be reduced. This lag will help reduce potential “head fakes” that sometimes occur with technical analysis.

Volatility in Bull and Bear Markets

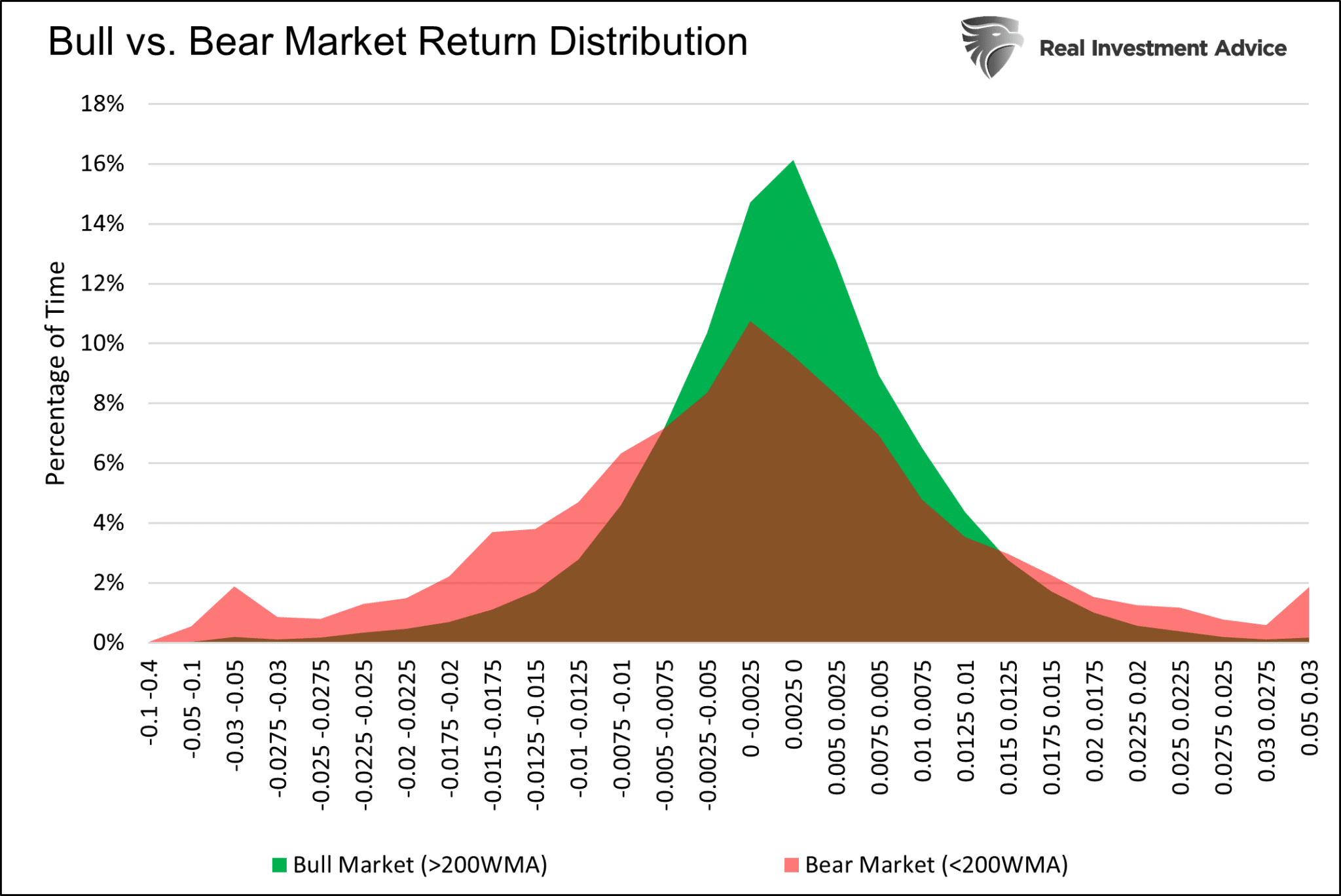

The graph below from Willie Delwiche compares the S&P 500 (blue) to the number of consecutive days (orange) in which the S&P 500 moved less than 1%. The graph is an excellent way of showing that volatility in bull markets tends to run much lower than in bear markets. Since 2022, the longest streak of days in which the market did not move more than 1% daily was seven. Most often since 2022, two to three days of low volatility was a long streak. The second graph below is from an upcoming article on risk and return. It shows significantly more instances of larger daily price moves in bear markets than in bull markets.

China is Reopening To Powell’s Chagrin

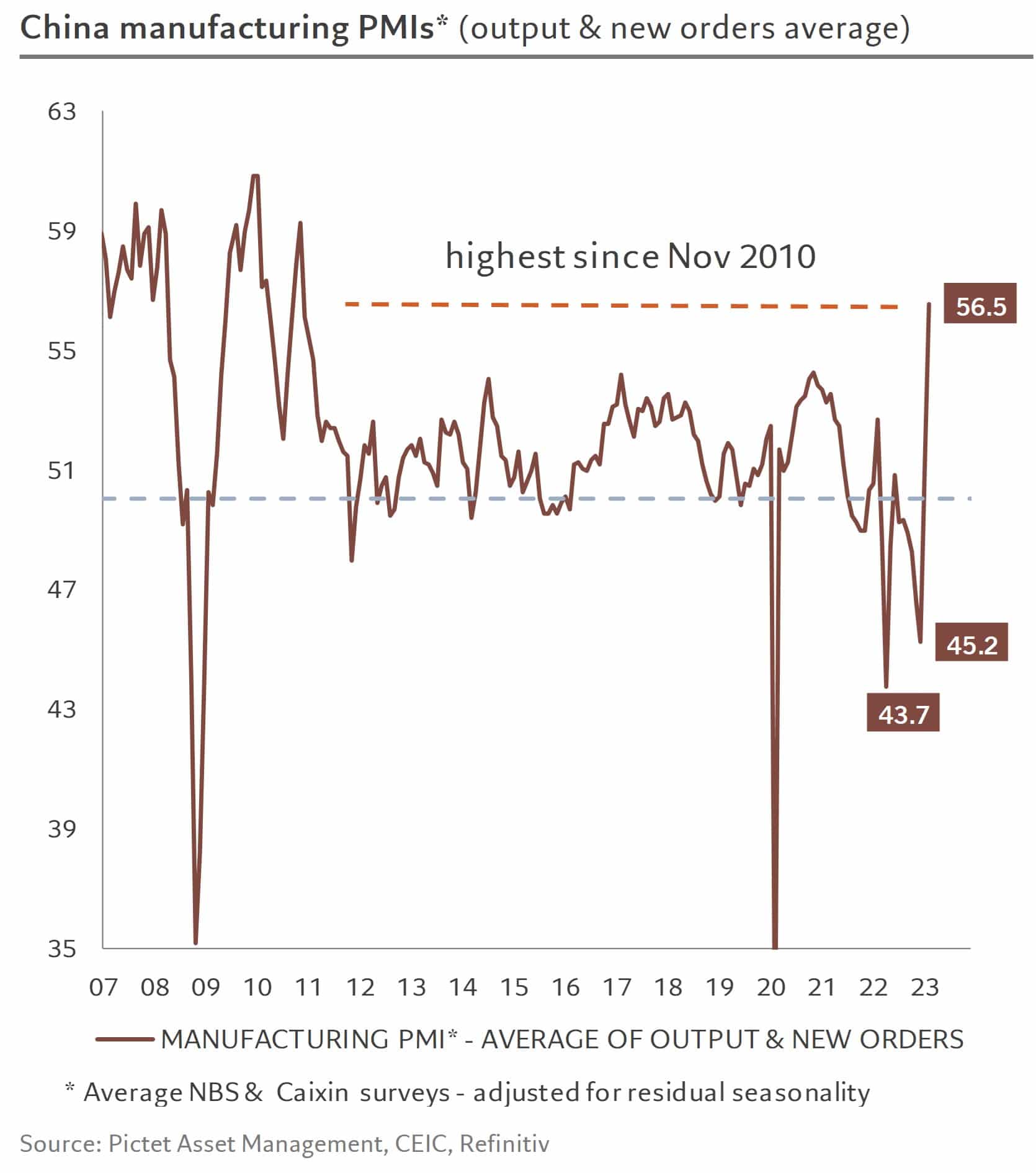

China dropped its strict covid protocols this year, and the economy seems to be waking up. The PMI index, which tends to lead economic growth, rose to 52.6, the highest reading since 2012. The graph below shows that the output and new orders part of the PMI index jumped to a 13-year high. Non-manufacturing showed equally strong gains. While we should cheer such strong growth from the world’s second-largest economy, we must also consider China’s reopening will put upward pressure on inflation. Commodities are trading higher on the news while inflation expectations are ticking up. This bit of information will reinforce the Fed’s hawkish stance.

How Valid is the No Landing Scenario?

During most of 2022, economists on Wall Street and the Fed debated how the economy would slow. Some, like Powell, believed a soft landing with no recession was possible. Others felt a hard landing, aka recession, would likely result from higher interest rates. Recently, the no-landing scenario has been growing in popularity. For more on this theory, check out our latest article, The No Landing Scenario and UFOs.

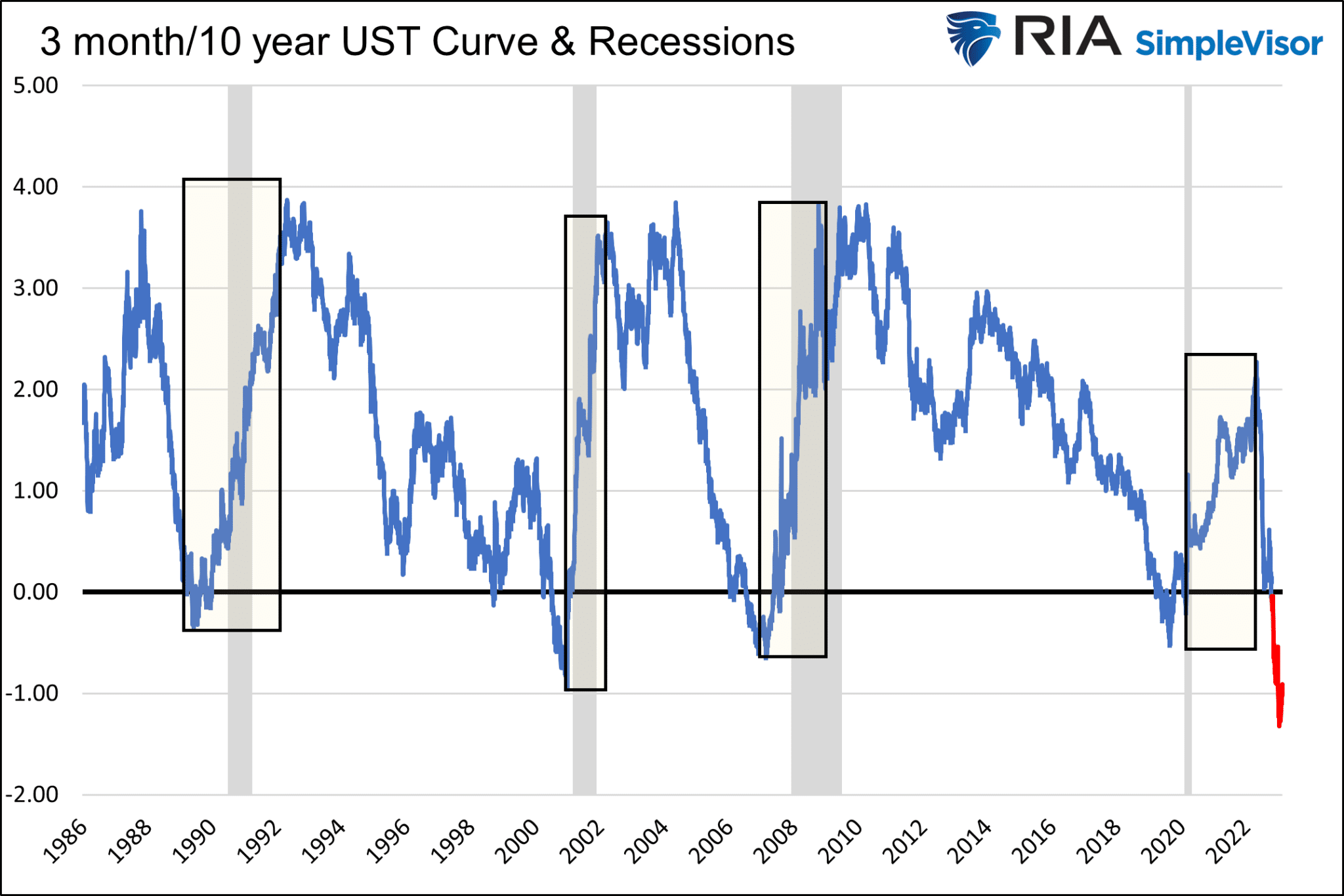

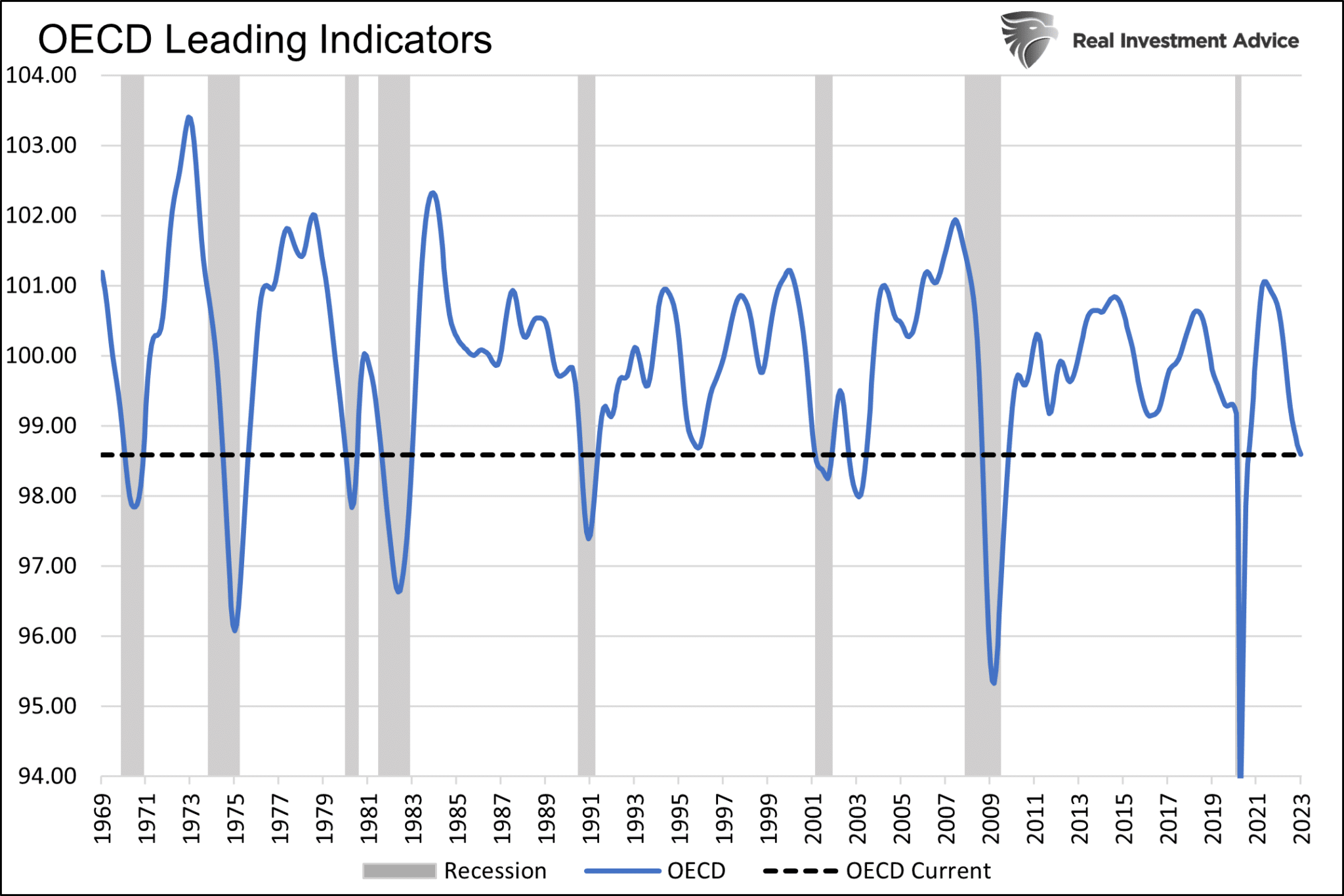

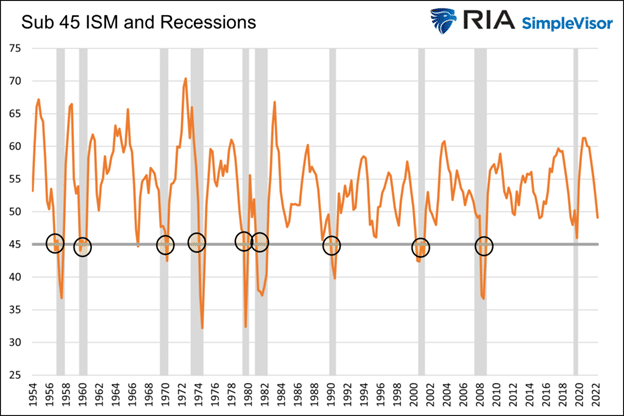

To forecast such a scenario, you must believe this time is different. The article describes how the economy is MORE vulnerable to higher interest rates, not LESS vulnerable. Further, we provide multiple charts showing various leading indicators often preceding recessions. We share a few below. Is this time different?

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.