Stocks and bonds had an especially bullish reaction to new data out Thursday showing that inflation continues to moderate after reaching a 40-year high over the summer. But is it enough for Powell to back off from more aggressive rate hikes?

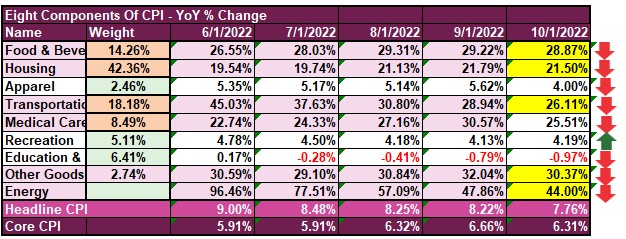

MoM inflation was unchanged at 0.4% versus estimates of 0.6%. Core inflation MoM fell to 0.3% in October from 0.6% in September and beat the consensus estimate of 0.5%. Here is the breakdown, with every inflation sector down except recreation (Halloween tweet).

The favorable print crushed the dollar and sent bonds and equities flying as investors reassessed their expectations for the path of rate hikes. The data was enough to spark a rally, but is it enough for Jay Powell and the FOMC? We share two quotes below from last Wednesday’s FOMC press conference Q&A. Keep in mind that at the time of the meeting, Powell likely had a good idea of the data released yesterday.

“And trying to make good decisions from a risk management standpoint, remembering of course that if we were to over-tighten, we could then use our tools strongly to support the economy, whereas if we don’t get inflation under control because we don’t tighten enough, now we’re in a situation where inflation will become entrenched and the costs, the employment costs in particular, will be much higher potentially. So, from a risk management standpoint, we want to be sure that we don’t make the mistake of either failing to tighten enough, or loosening policy too soon.”

“And the last thing I’ll say is that I would want people to understand our commitment to getting this done. And to not making the mistake of not doing enough or the mistake of withdrawing our strong policy and doing that too soon. So those, I control those messages and that’s my job.”

What To Watch Today

Economy

- 10:00 a.m. ET: University of Michigan Consumer Sentiment, November Preliminary (59.5 expected, 59.9 prior)

- 10:00 a.m. ET: U. of Mich. Current Conditions, November Preliminary (62.8 expected, 65.6 prior)

- 10:00 a.m. ET: U. of Mich. Expectations, November Preliminary (55.5 expected, 56.2 prior)

- 10:00 a.m. ET: U. of Mich. 1 Year Inflation, November Preliminary (5.1% expected, 5.0% prior)

- 10:00 a.m. ET: U. of Mich. 5-10 year Inflation, November Preliminary (2.9% expected, 2.9% prior)

Earnings

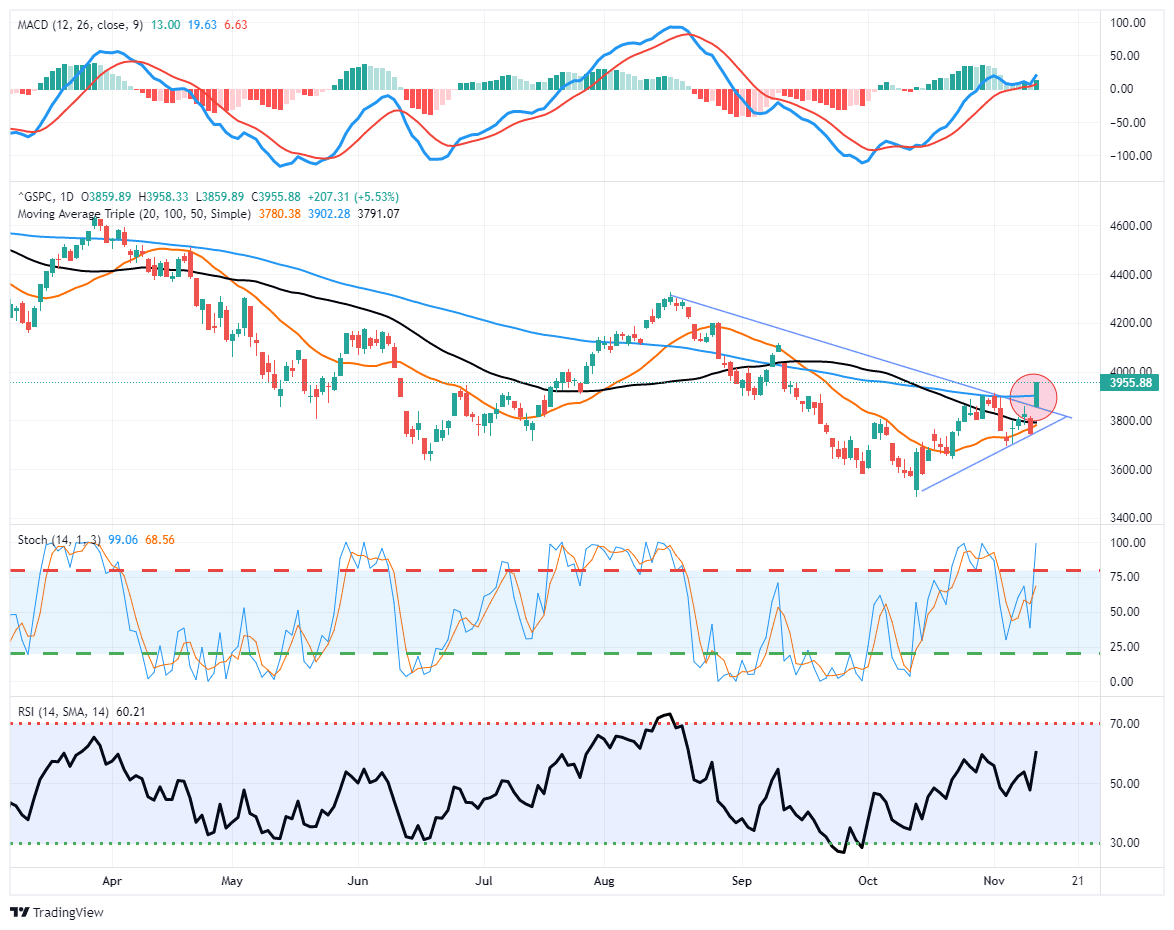

Market Trading Update

Stocks surged yesterday as weaker inflation data gave the bulls a reason to celebrate, hoping that a Fed “pivot” is closer at hand. While we believe that is overly optimistic, the market tested and held key support again at the 20-dma after the FTX (cryptocurrency) blow-up on Wednesday. The subsequent rally off support turned our MACD “buy signal” higher, keeping it intact, and the market cleared critical resistance at the 100-dma. Such now sets the stage for a rally to the 200-dma between 4000 and 4100.

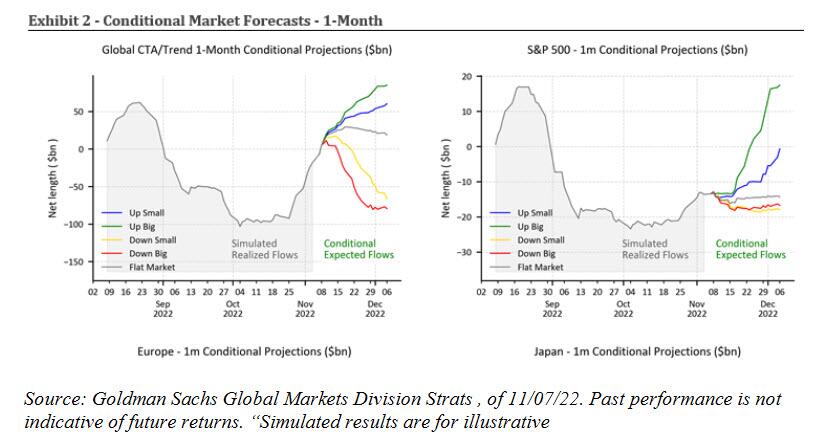

The surge in asset prices also cleared levels that are now forcing short-sellers to cover positions which will add “fuel to the rally” over the next few days. As noted by Goldman Sachs, CTAs bought $43BN last week and bought $79BN last month; now that we are back over the short-term trigger, Goldman calculates that there is a whopping $38BN to buy over the next week and substantially more (green line) in an up big market: as shown in the chart below, the bank expects more than +$79B of Buying over a month.

While the rally certainly has some legs, be sure and use it to take profits, rebalance risks, and adjust portfolio exposures accordingly. We aren’t through with the bear market just yet.

The Myth of the Strong Consumer

There’s quite a difference between consumption remaining strong and consumers remaining strong. Even so, many Wall Street pundits continue to advise that consumers remain strong. We’d argue that while consumption has held up in the face of inflation, the consumer is showing clear signs of struggle.

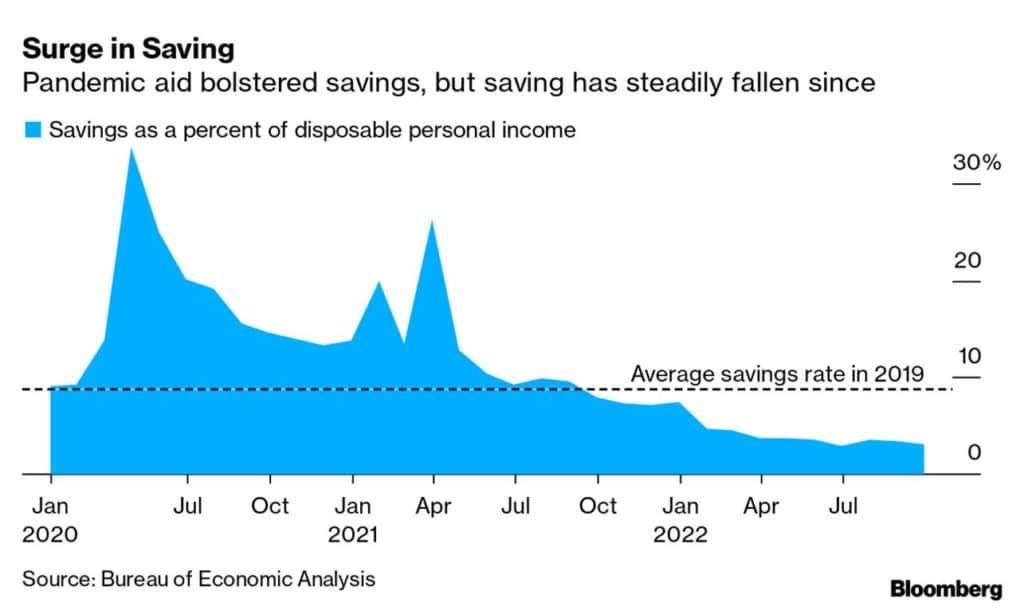

TransUnion reports that credit card balances surged 19% YoY in the 3rd quarter to an all-time high of $866B. This followed a 12% increase in credit cards issued to subprime consumers in Q2, the surge was driven by card use across all risk tiers. Furthermore, the chart below shows that savings as a portion of disposable income have significantly deteriorated as inflation has picked up. Consumers aren’t strong. Consumption is. They are just using credit to bridge the gap, which works against their future prosperity as more income goes to service debt.

Is Elon Driving Twitter into the Ground?

Elon Musk is truly on a rampage at Twitter after taking the company private two weeks ago today. He fired most top executives when the acquisition closed, and two resigned yesterday. He laid off 50% of the staff disorganizedly and is now asking some to return after they were let go “by mistake.” His controversial status lost the company’s advertising revenue after he saddled it with debt in the takeover. On top of that, his first email to Twitter staff ended remote work for everyone and said bankruptcy was possible. For those who are left, employee morale is most likely in the dirt.

The Twitter fiasco may start bleeding over to Tesla as well. But is it enough to remove the “Musk hype” premium from TSLA’s stock price? Wedbush analyst, Dan Ives, removed the stock from their Best Ideas list yesterday. He wrote:

“In what has been a dark comedy show with Twitter, Musk has essentially tarnished the Tesla story/stock and is starting to potentially impact the Tesla brand with this ongoing Twitter train wreck disaster… Musk’s attention focus from Tesla to Twitter, and ultimately the fear that this Twitter lightening rod of controversy on a daily (almost hourly) basis starts to negatively change the Tesla brand globally.”

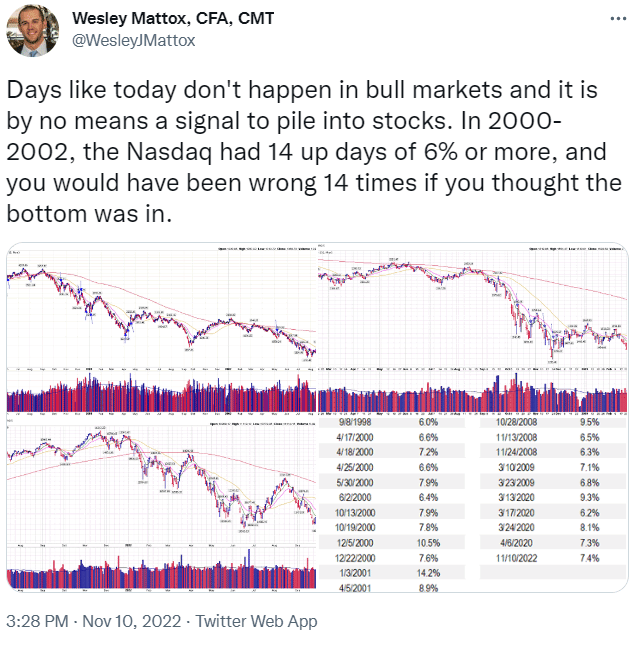

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read