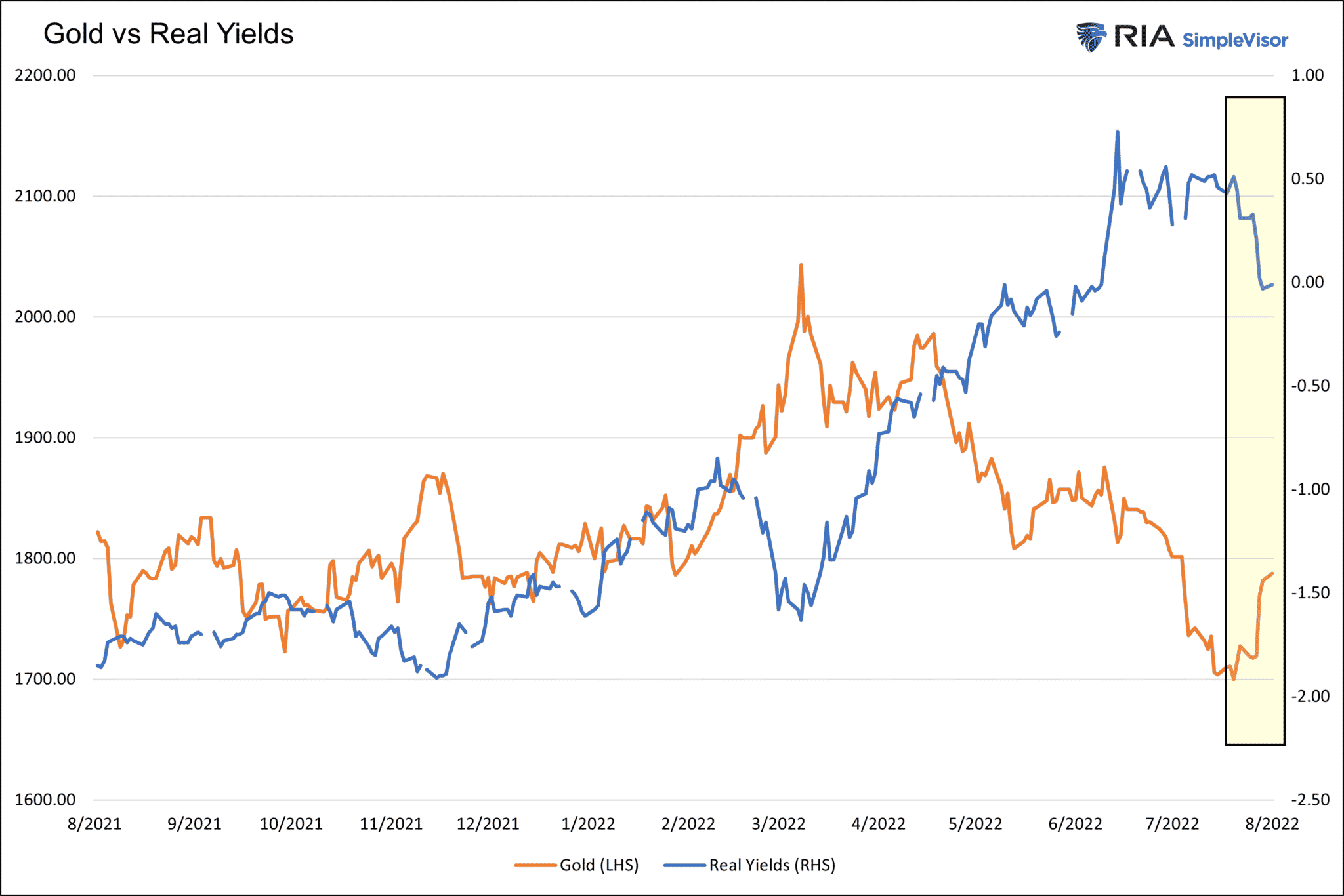

In just the last two weeks, gold prices have spiked by $85/ounce. Why? Some claim a recent increase in inflation expectations is driving gold higher. That is partially true. However, it doesn’t tell the whole story. The reality is that real yields are falling, which is driving gold higher. Real yields, which are inversely correlated with gold prices, are the difference between nominal yields and inflation expectations. Over the last two weeks, real yields have fallen by 53bps as inflation expectations rose by 18bps and nominal yields fell by 35bps. Real yields inversely correlate with gold prices because they best describe the Fed’s influence on markets. When the Fed is dovish or believed to be in the future, real yields fall and often go negative.

The market is starting to price in a Fed stall and pivot. Accordingly, investors believe the Fed is shifting from a hawkish to a dovish stance. As a result, real yields are falling, and gold is rising, as shown in the yellow box below. The outlook for gold may not be bullish if bond investors start fretting that a dovish Fed will fuel more inflation and push nominal yields higher to catch up with the recent increase in inflation expectations.

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended July 29 (-1.8% prior)

- 9:45 a.m. ET: S&P Global U.S. Services PMI, July final (47 expected, 47 prior)

- 9:45 a.m. ET: S&P Global U.S. Composite PMI, July final (47.5 prior)

- 10:00 a.m. ET: Factory Orders, June (1.2% expected, 1.7% prior)

- 10:00 a.m. ET: Factory Orders Excluding Transportation, June (1.7% prior)

- 10:00 a.m. ET: Durable Goods Orders, June final (1.9% expected, 1.9% prior)

- 10:00 a.m. ET: Durables Excluding Transportation, June final (0.3% prior)

- 10:00 a.m. ET: Nondefense Capital Goods Orders Excluding Aircrafts, June final (0.5% prior)

- 10:00 a.m. ET: Nondefense Capital Goods Shipments Excluding Aircrafts, June final (0.7% prior)

- 10:00 a.m. ET: ISM Services Index (53.5 expected, 55.3 prior)

Earnings

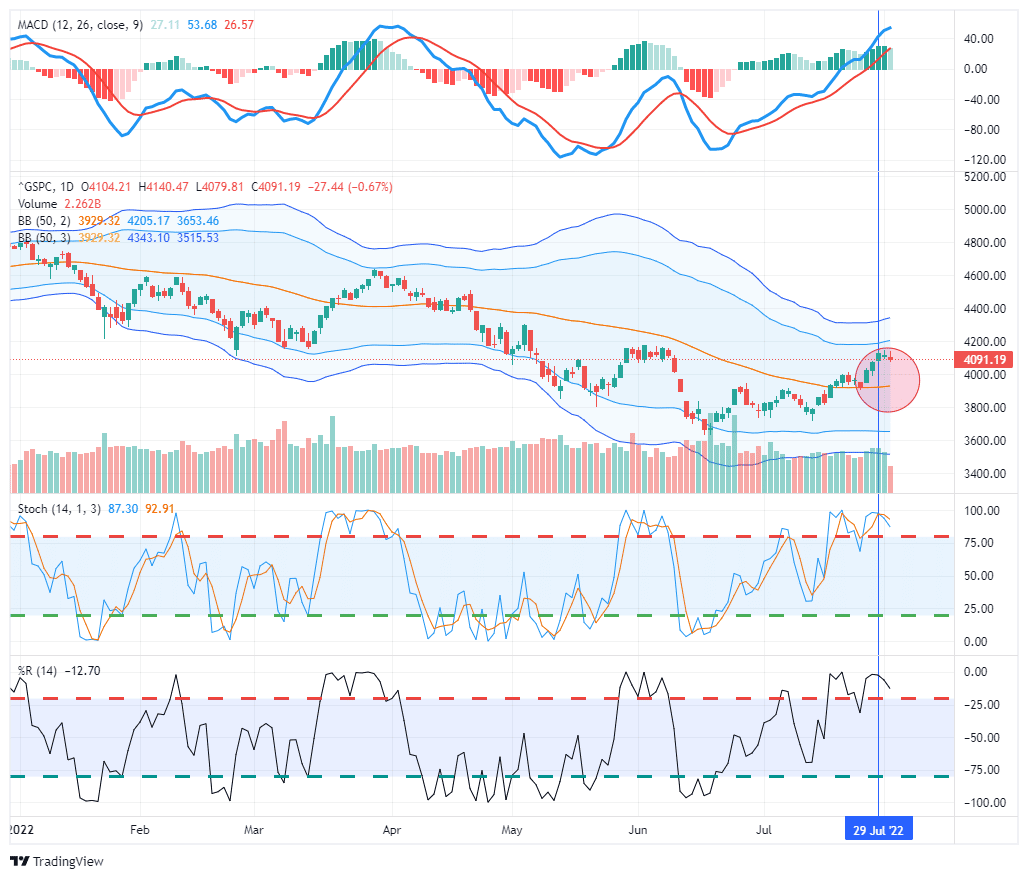

Market Trading Update – Profit Taking Hits Markets

As we noted in this past weekend’s Bull Bear Report (subscribe for free weekly email delivery):

“As of Friday’s close, the market is now on track for the best month since 2020. However, short-term markets are now extremely overbought and pushing up into very tough resistance. A pullback and some profit-taking next week will not be surprising.”

Such is precisely what we witnessed this week so far. With markets very overbought, a pullback is not surprising. However, as discussed recently, the key to this current rally will be the 50-dma. While a correction is healthy, support must hold in order for the market to continue is bullish rally. A failure of that resistance will likely see stocks either retest, or set, new lows. On both Monday and Tuesday we took profits in our recent technology additions and are looking to use weakness to add those weightings back.

Trade cautiously for now, we are still in a dangerous market.

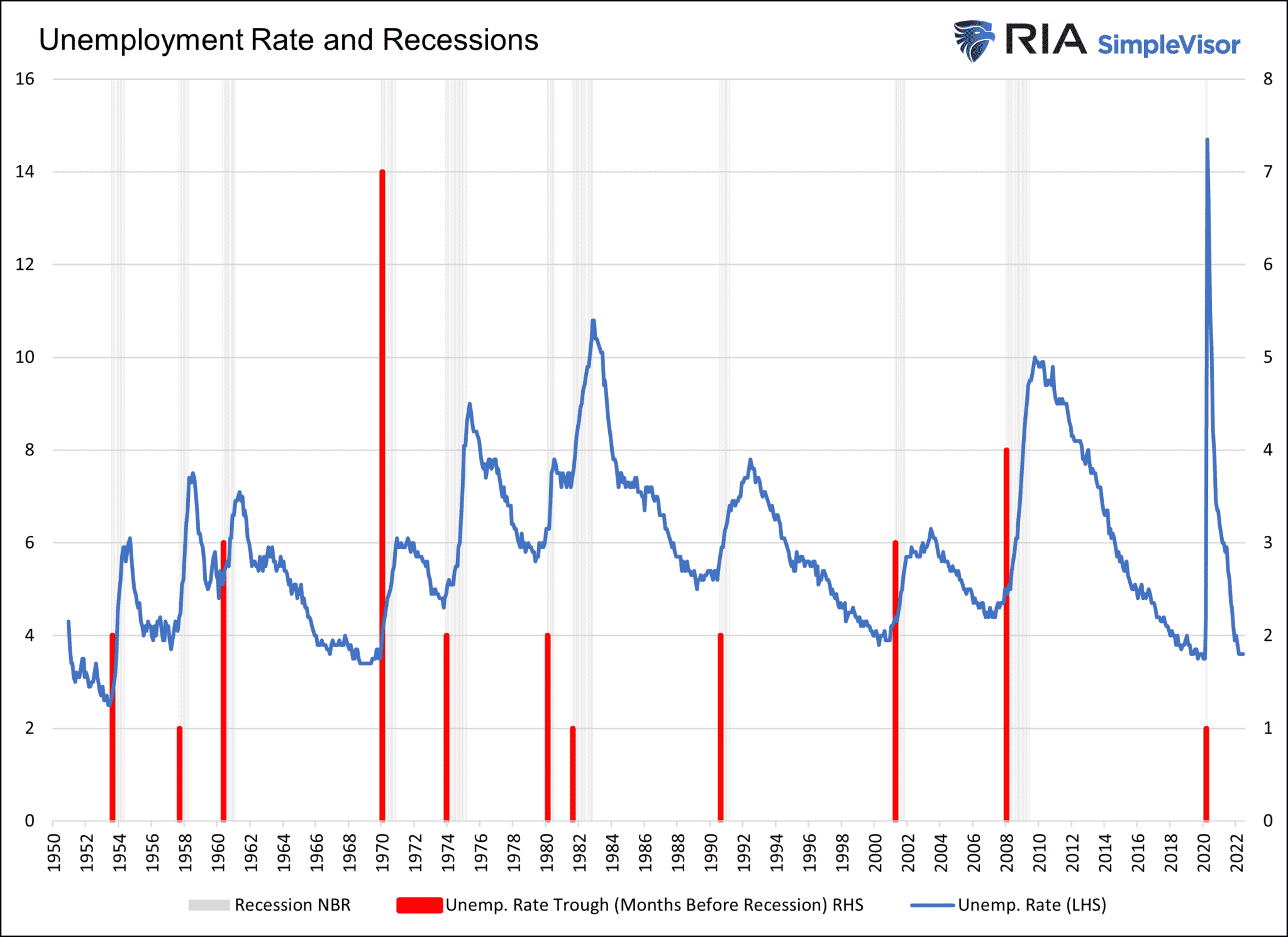

Unemployment and Recessions

A debate rages among economists about whether or not we just entered a recession. Some argue yes because real GDP has been negative for two quarters in a row. Others believe that it’s not just GDP that determines a recession but also a rising unemployment rate. That debate may end this Friday. The graph below shows the unemployment rate (blue), recessions (gray), and the number of months the unemployment rate troughed (red) before each recession. Since 1950 there have been eleven recessions. On average, the unemployment rate bottoms 2.5 months before an official recession declaration by the NBER. In seven of the eleven instances, the unemployment rate started rising one or two months before a recession. If the unemployment rate ticks higher this Friday, from a very low historical level, the odds of the NBER declaring July or August as the recession start will increase significantly.

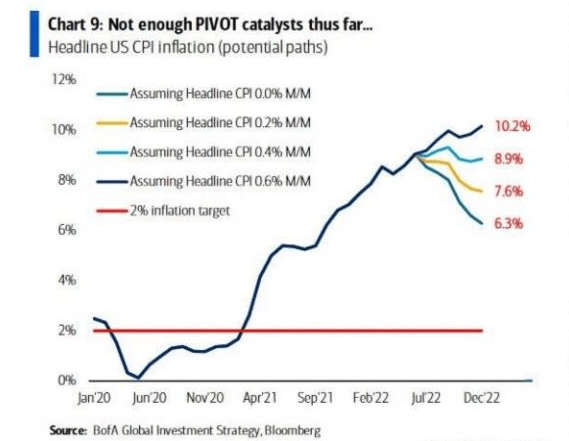

The Path of Inflation

The graph below uses various monthly inflation rates to map out where year-over-year CPI may end the year. The market is assuming the Fed will stall later this year and pivot early next year. Unless monthly inflation starts declining, we must ask ourselves, will the Fed feel they have tamed inflation if it’s still greater than 6%? While we think annual inflation rates will start to decline, we do not believe it will be enough to get the Fed to stall and pivot as soon as the market thinks it will.

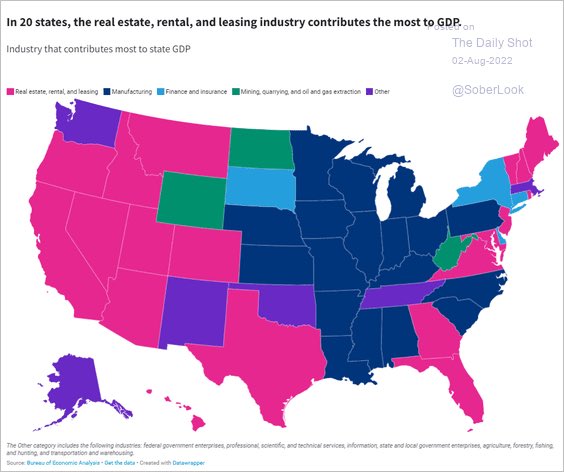

Real Estate Really Matters

Real Estate accounts for about 15-20% of GDP and almost a third of CPI. As we assess inflation, debate economic growth, and try to gauge what the Fed may or may not do, we must keep a close eye on real estate activity. The graph below shows that in 20 states, real estate, rental, and leasing industries are the most significant contributors to GDP. California and Texas are the two largest states measured by GDP, and they are both states with real estate as the predominant driver of GDP. California has almost twice the GDP as Texas at nearly $3.2 trillion.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read