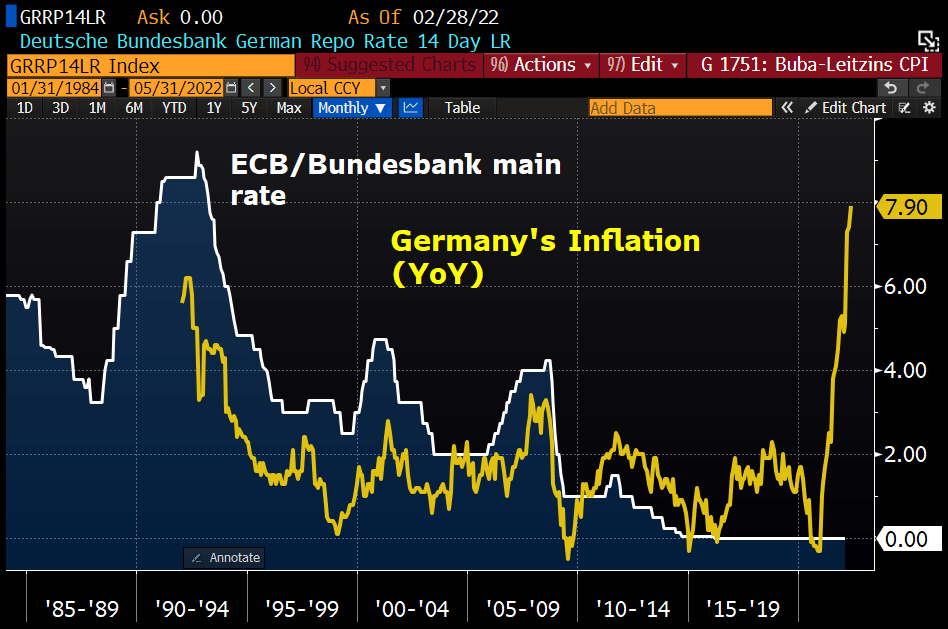

Recent inflation data for Germany and Europe shocked economists on Monday, rising much more than expected. Eurozone inflation rose to 8.1% from 7.4%, led higher by Germany reporting 8.7% inflation. That was the highest inflation rate for Germany since 1973! U.S. Treasury bond yields rose in sympathy as the German inflation data raises concerns U.S. inflation may not be peaking. Driving German and European inflation higher is a weaker euro and high oil prices. With the EU rejecting Russian oil and gas, energy inflation will likely stay elevated. As we share below, the ECB has yet to raise rates or stop QE despite surging inflation. Such dovish activity in light of high inflation will further foster inflation concerns.

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, the week ended May 27 (-1.2% prior)

- 9:45 a.m. ET: S&P Global U.S. Manufacturing PMI, May final (57.5 expected, 57.5 prior)

- 10:00 a.m. ET: Construction Spending, month-over-month, April (0.5% expected, 0.1% prior)

- 10:00 a.m. ET: ISM Manufacturing, May (54.5 expected, 55.4 prior)

- 10:00 a.m. ET: ISM Prices Paid, March (80 expected, 84.6 prior)

- 10:00 a.m. ET: ISM New Orders, May (53.5 prior)

- 10:00 a.m. ET: ISM Employment, May (50.9 prior)

- 10:00 a.m. ET: JOLTS Job Openings, April (11.300 million expected, 11.549 million prior)

- 2:00 p.m. ET: Federal Reserve Releases Beige Book

- WARDS Total Vehicle Sales, May (13.70 million expected, 14.29 million prior)

Earnings

Pre-market

- No notable reports are scheduled for release.

Post-market

- GameStop (GME) to report an adjusted loss of $1.16 on revenue of $1.33 billion

- Chewy (CHWY) to report adjusted earnings of $0.02 on revenue of $2.41 billion

- PVH (PVH) to report adjusted earnings of $1.60 on revenue of $2.09 billion

- Hewlett Packard (HPE) is expected adjusted earnings of $0.45 on revenue of $6.81 billion

- Pure Storage (PSTG) to report adjusted earnings of $0.04 on revenue of $522 million

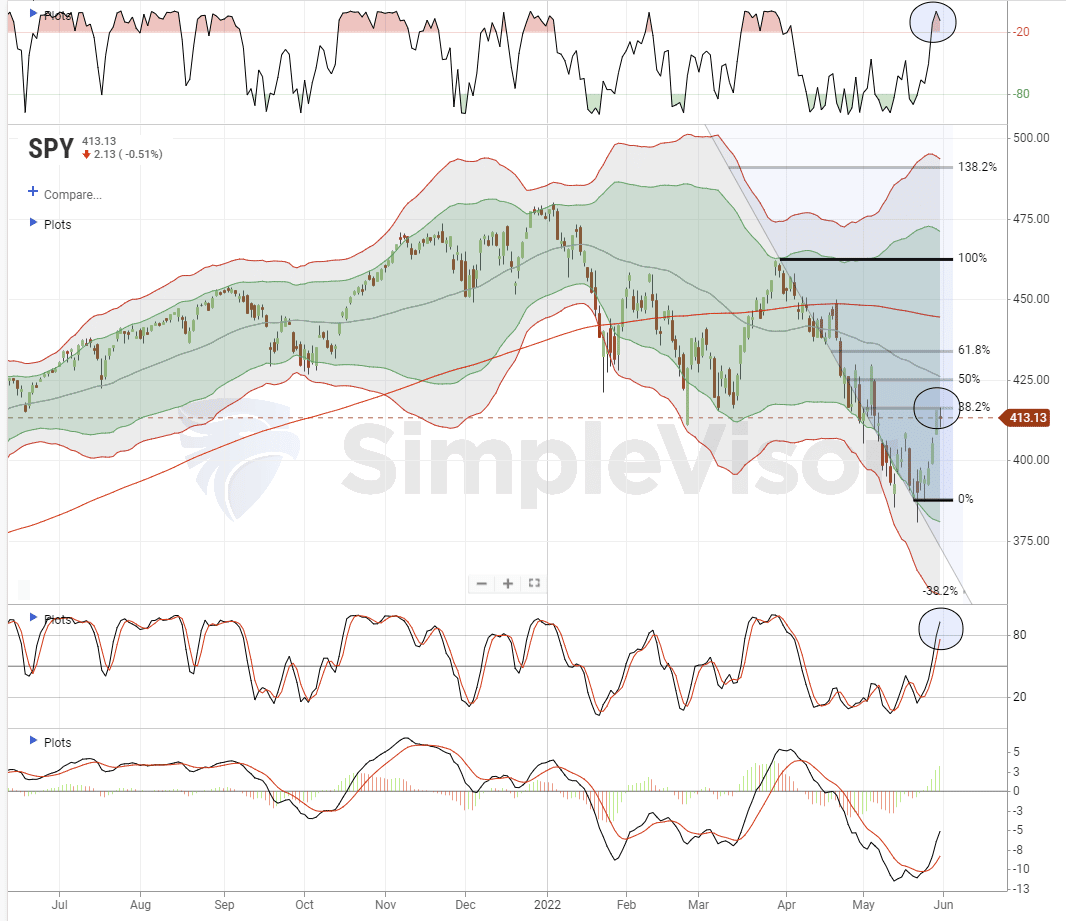

Market Update – Rally To First Resistance Level

While German inflation pushed yields higher yesterday, the market also ran into resistance at the first Fibonacci retracement level from the recent low. As discussed last week, the 38.2% retracement level was our initial target to reduce some equity exposure which we did yesterday. Our next target will be the 50% retracement level which also coincides with the 50-dma. With the market already moving back into overbought territory short term, reducing risk and rebalancing allocations still makes sense.

See the full major market technical review and update at Simplevisor.com.

Mixed Economic Data

Economic data for Tuesday was mixed. The FHFA House Price Index rose less than expected at 1.5% and 19% annually. On the other hand, the Case-Shiller Home Price Index rose 2.4% for the month and now sits at a 21.2% annual growth rate. The data for both indexes are from March, so the adverse price effects from higher mortgage rates are not yet in the data. The 30-year mortgage rate for March ranged from 3.3% to 4.7%. It currently stands at around 5.5%.

Regional manufacturing surveys were also mixed. The Chicago PMI report came in above expectations at 60.3, up from 56.4 last month. The Dallas Fed Manufacturing Survey fell into contractionary levels at -7.3 versus +1.1 last month. Price data in both surveys are largely unchanged.

The Dallas report signals weak growth ahead. Per the report- “The new orders index fell nine points to 3.2, and the growth rate of orders index plummeted 18 points and turned negative at -5.3. Both readings mark their lowest levels in about two years.“

The Chicago PMI asked a special question: Are you seeing any easing up in the supply chain blockages? Only 2.13% said yes, while 61.7% said no. The large majority of the remainder answered somewhat.

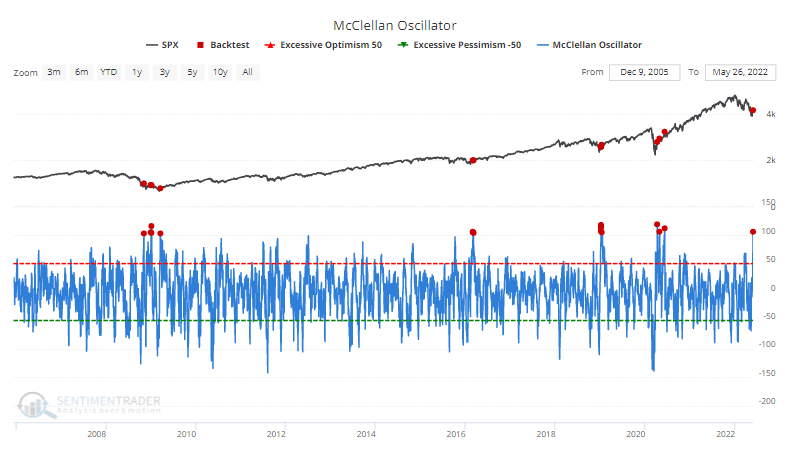

Buying Surge Argues Against Bear Market Rally

Is this still a “bear market rally?” Sentiment Trader recently suggested it might be more than that.

“Here we go again.

In late March 2020, thrusts in buying interest were wildly impressive. But almost all technicians mocked them as ‘unofficial’ because they didn’t meet some arbitrary, cherry-picked, overly optimized rules.

It’s happening again, and there is even more skepticism that this rally is real. The number of articles dismissing the gains as just another “bear market rally” is nearly double the prior record from early April 2020.

In the three days leading up to the exchange holiday, more than 80% of the volume on the NYSE flowed into advancing stocks. We typically do not see this kind of behavior during bear markets, usually at the end of them.

All the buying pressure pushed the McClellan Oscillator above +100. Every time this happened in the past 20 years, it marked the end of the selling pressure (or very close to it).”

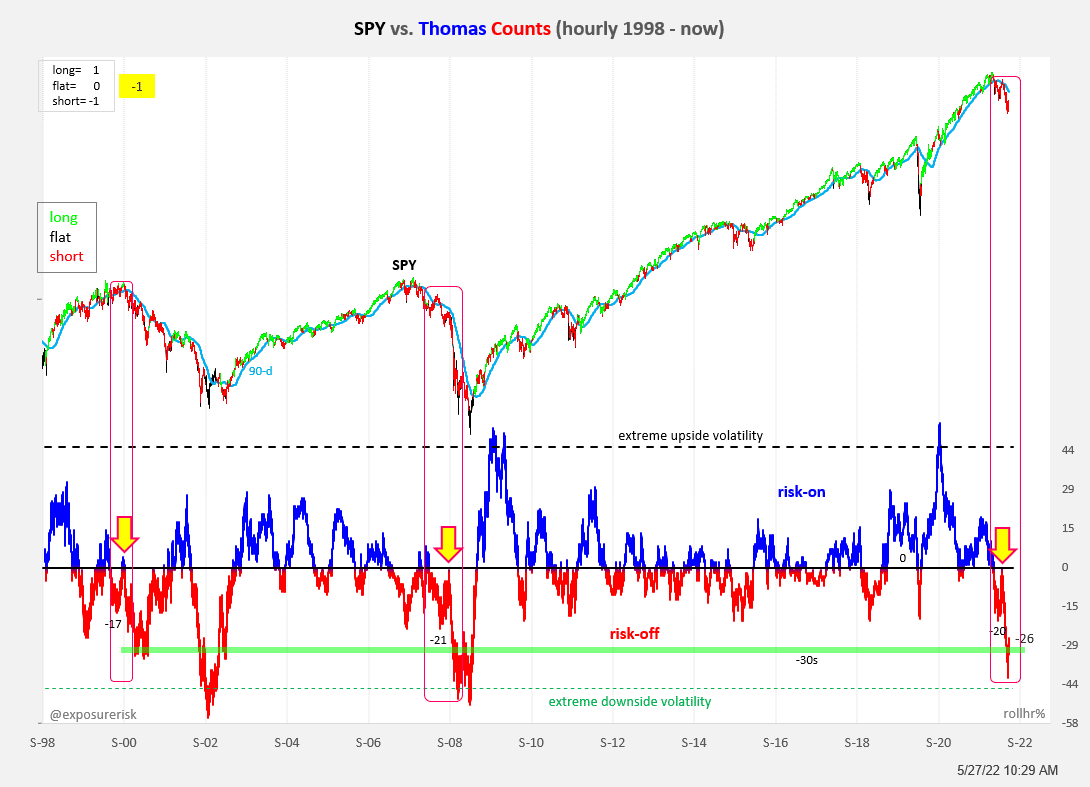

Extreme Upside-Downside Signal More Pain Ahead

The graph and commentary below are from @exposurerisk. The hourly chart below counts extreme volatility events. Unlike 2020, the market is behaving much more like a bear market than a short-lived drawdown. In the last 20 years, the only two times this occurred were in 2000 and 2008. This graph gives credence to those that think the bear market is just getting started.

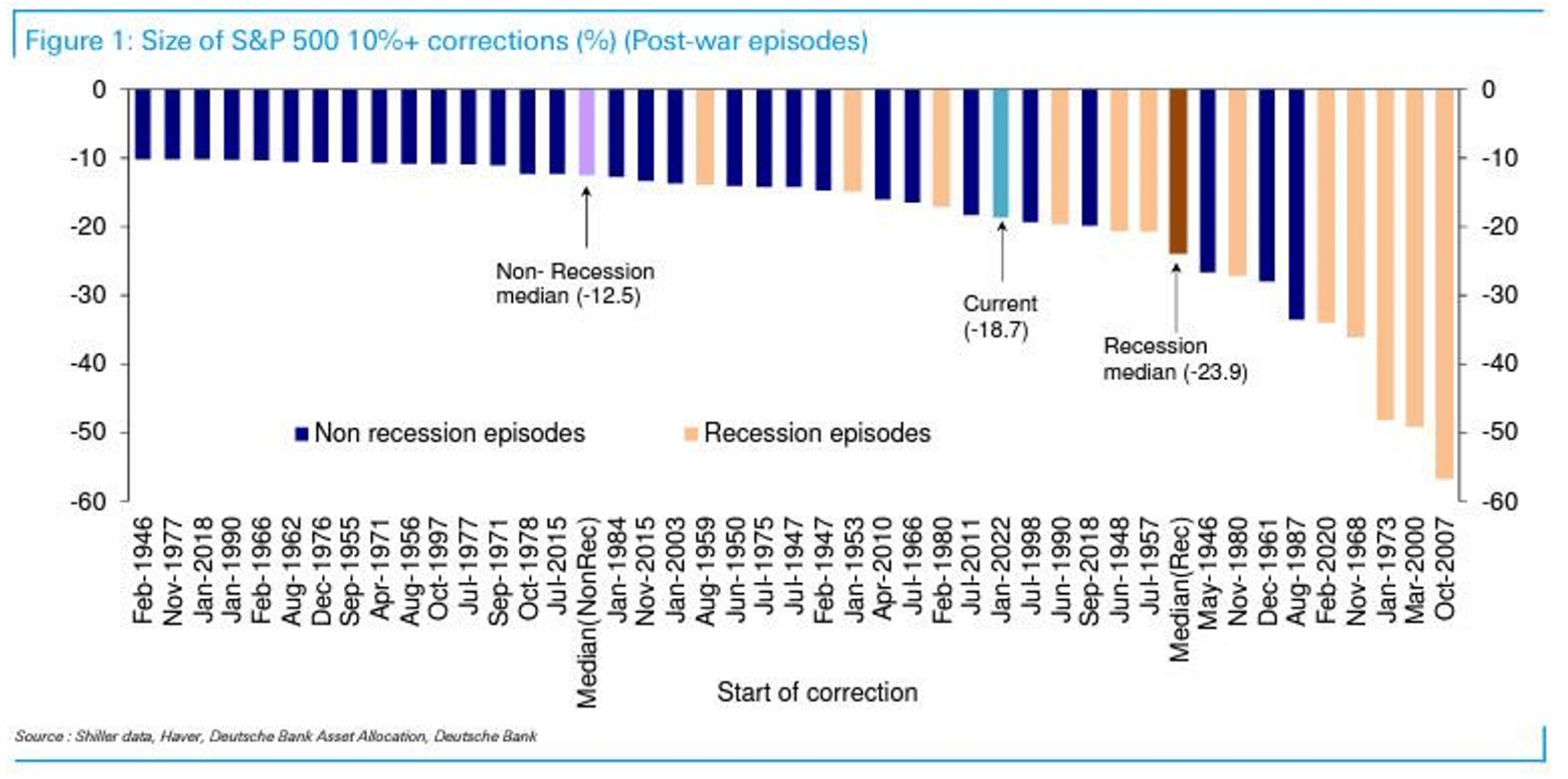

Recession Bear Market

The graph below from Callum Thomas compares ten percent or larger drawdowns and whether or not they occurred during a recession. As the graph shows, the current episode is starting to resemble drawdowns occurring during recessions versus those in non-recessionary periods. Callum says the “key point is that the answer as to whether this is going to be a more drawn out and deeper bear market will depend on recession: yes or no.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read