This week’s screen looks for opportunities in the U.S. refining industry.

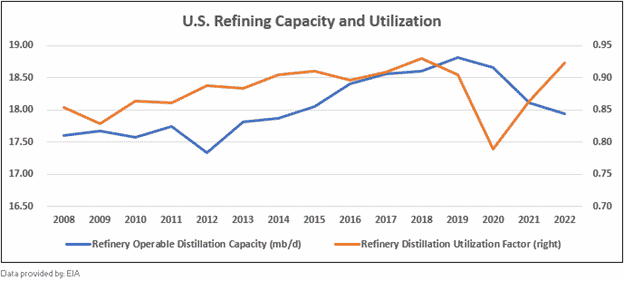

The first chart below shows that U.S. refining capacity has declined since 2019. At the same time, demand for refined products such as gasoline and jet fuel are returning to pre-pandemic levels.

The combination of record low distillate inventories, crimped refining capacity, and normalizing demand have sent crack spreads soaring this year. Crack spreads represent the difference between the purchase price of crude oil and the selling price of refined products. Thus, they serve as an indicator of the profit margins realized by refineries.

The two charts below show how the 3:2:1 crack spread for WTI oil on the U.S. Gulf Coast has evolved. They are now near double historical norms, and although well off the highs, they remain very elevated. Unfortunately for Americans, additional refining capacity is not something that comes online quickly. Projects can take up to ten years from start to finish, so refiners’ margins have the potential to stay elevated for many years to come, especially if demand continues its upward trend.

Screening Criteria

- Market Cap >$5B

- Country = USA

- Oil & Gas Refining/Integrated

- PEG Ratio <2

- Debt/Equity < 1.5

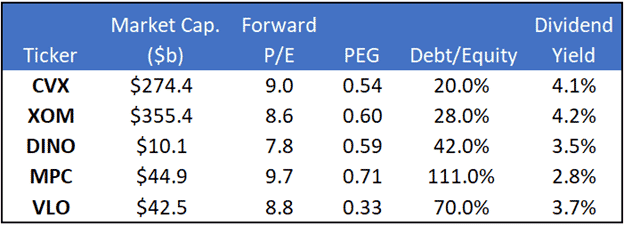

Our screen returned five companies, two of which are integrated oil & gas companies, while the remaining three operate purely downstream. The integrated players have a slight margin advantage since they essentially receive crude at the cost of production while the other players purchase at the market price. All five companies are priced for value and pay a respectable dividend yield.

A recession could temper demand and depress crack spreads back to normal levels. However, as mentioned above, additional refining capacity cannot come online quickly.

Company Summaries (all descriptions courtesy Zacks)

Chevron CVX

Chevron is one of the largest publicly traded oil and gas companies in the world with operations that span almost every corner of the globe. The only energy component of the Dow Jones Industrial Average, Chevron is fully integrated, meaning it participates in every aspect related to energy from oil production, to refining and marketing. Chevron remains well positioned to navigate the volatility in oil and gas prices. Being an integrated firm engaged in all aspects of the oil and gas business. Chevron divides its operations into two main segments: Upstream and Downstream. Chevron s other activities include transportation and chemicals. Chevron s current oil and gas development project pipeline is among the best in the industry.

Exxon XOM

ExxonMobil s bellwether status in the energy space, optimal integrated capital structure that has historically produced industry-leading returns and management s track record of capex discipline across the commodity price cycle make it a relatively lower-risk energy sector play. The company owns some of the most prolific upstream assets globally. Other aspects of the company s story include the largest global refining operations, substantial chemicals assets and a dividend history and credit profile that are second to none in the space. ExxonMobil s capital spending discipline is quite aggressive. The company has a plan in place to allocate significant proportion of its budget to key oil and gas projects. The company s business perspective looks different from most peers since big oil rivals have pledged to lower carbon emissions to tackle climate change. ExxonMobil divides its operations into three main segments: Upstream, Downstream and Chemical.

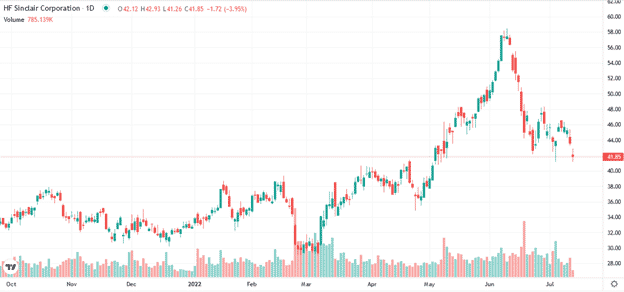

HF Sinclair DINO

HF Sinclair Corporation is an energy company which produces and markets light products such as gasoline, diesel fuel, jet fuel, renewable diesel and other specialty products. It owns and operates refineries located principally in Kansas, Oklahoma, New Mexico, Wyoming, Washington and Utah. HF Sinclair Corporation, formerly known as HollyFrontier Corporation, is based in DALLAS.

Marathon Petroleum MPC

Marathon Petroleum Corporation is a leading independent refiner, transporter and marketer of petroleum products. The company came into existence following the spin-off of Marathon Oil Corporation s refining sales business into a separate, independent and publicly-traded entity. Marathon Oil completed the acquisition of its rival Andeavor. Marathon Petroleum operates in two segments: Refining and Marketing and Pipeline Transportation. Refining and Marketing: The unit s operations refineries, located in the various regions of the United States. Marathon Petroleum through its marketing organization sells transportation fuels, asphalt and specialty products throughout the country to support commercial, industrial and retail operations. Midstream: This unit mainly reflects Marathon Petroleum s general partner and majority limited partner interests in MPLX LP and Andeavor Logistics LP that own and operate gathering and processing assets along with crude transportation and logistics infrastructure.

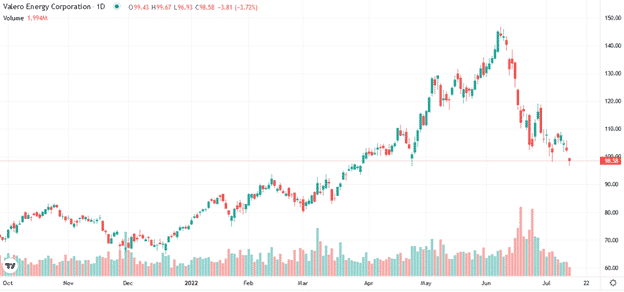

Valero Energy VLO

Valero Energy Corporation is the largest independent refiner and marketer of petroleum products in the United States. It has refineries located throughout the United States, Canada and the United Kingdom. Moreover, Valero is a leading ethanol producer with ethanol plants in the Midwest. The products of the company are sold in the markets of the United States, Canada, the United Kingdom, Ireland and Latin America. The company s brand names are carried by outlets. The company organizes its business through three reportable segments, namely, Refining, Ethanol and Renewable Diesel.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)

Also Read