With the price of oil, fertilizer, grains, and other agricultural products soaring, we thought it would be helpful to find food companies with thin profit margins that may struggle to pass on higher costs to consumers. In contrast to our other screens that have focused on stocks with the potential for outperformance in a given scenario, this screen highlights stocks that investors may wish to avoid.

Despite the inflation headwinds listed above and other negative factors, many food staples companies have outperformed the market this year and are trading near 52-week highs. To wit, XLP (a Consumer Staples ETF) is down only 6% this year while the S&P 500 is down 11%.

Staples, in general, are outperforming because they tend to have lower betas and higher dividends. Investors are flocking to perceived safety, as is typical in down markets. However, are investors overlooking the underlying fundamentals for some of these companies and just buying them because they have been a port in the storm in prior bear markets?

Screening Criteria

Sector = Consumer Defensive (staples) from the following subsectors: beverages, farm products, grocery stores, packaged goods, and food distribution.

Net Profit Margin <20%

Price Performance >0% YTD

Price >50 and 200-day moving averages

Price = 0-5% from 52 week high

Our initial scan yielded ten companies. We decided to use market cap to trim the list to five. As you will notice below, three of the five companies are well known name-brands that are likely widely held by investors.

Company Summaries (all descriptions courtesy Zacks)

Keurig Dr Pepper (KDP)

Keurig Dr Pepper Inc. manufactures and distributes non-alcoholic beverages. The Company offers soft drinks, juices, teas, mixers, water and other beverages. Its brands include Keurig(R), Dr Pepper(R), Green Mountain Coffee Roasters(R), Canada Dry(R), Snapple(R), Bai(R), Mott s(R) and The Original Donut Shop(R). Keurig Dr Pepper Inc., formerly known as Dr Pepper Snapple Group., is based in Texas, United States.

KDP is up 0.5% YTD and is outperforming XLP over the same period. It trades at a forward P/E of 22.3 with modest expectations for earnings growth, which yield a PEG ratio of 4.3. While the rotation into less cyclical sectors has helped performance YTD, a weakening consumer and cost pressures may shrink margins over the next few quarters and negatively impact the stock.

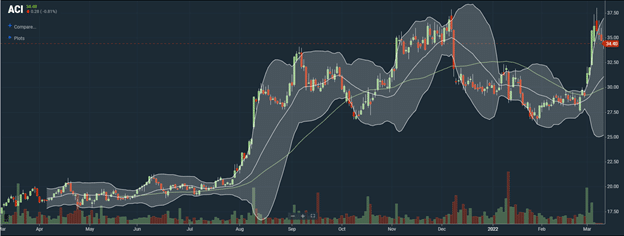

Albertsons Companies (ACI)

Albertsons Companies, Inc. provides retail food products. The Company distributes fruits, vegetables, canned items and other related goods. Albertsons Companies Inc. is based in the United States.

ACI is up 15.2% YTD and is handily outperforming XLP with the majority of outperformance coming earlier this month. On top of cost pressures and a lack of pricing power from a fundamental perspective, the sharp price increase earlier this month has left ACI retreating from significantly overbought conditions. Fundamental and technical factors may work against the stock simultaneously.

Hostess Brands (TWNK)

Hostess Brands, Inc. is involved in developing, manufacturing, marketing, selling, and distributing sweet goods primarily in the United States. The company produces new and classic treats which includes: Ding Dongs, Ho Hos, Donettes, Fruit Pies as well as Twinkies and CupCakes. Hostess Brands, Inc. is based in Kansas City, Missouri.

As a manufacturer of some of the more discretionary foods in consumer staples, TWNK will likely struggle to pass on cost increases to its customers. TWNK is up 2.2% YTD and is outperforming XLP, but it’s given up some gains in the last week. This is likely in connection with the recent action in commodity prices. Despite the strong upward trend, investors should be cautious going forward.

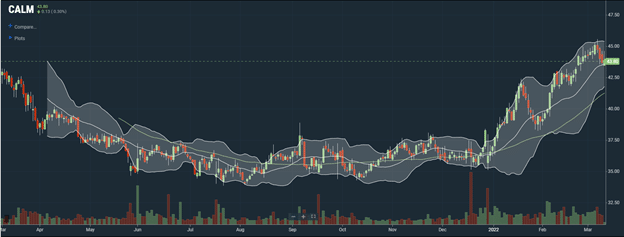

Cal-Maine Foods (CALM)

Cal-Maine Foods, Inc. is primarily engaged in the production, grading, packing and sale of fresh shell eggs, including conventional, cage-free, organic and nutritionally-enhanced eggs. The Company, which is headquartered in Jackson, Mississippi, is the largest producer and distributor of fresh shell eggs in the United States and sells the majority of its shell eggs in states across the southwestern, southeastern, mid-western and mid-Atlantic regions of the United States.

CALM is up 18.4% this year and is outperforming XLP by a wide margin. Besides energy costs, CALM probably won’t see inflation in its direct input costs. However, it’s animal feedstock almost certainly contains a significant proportion of grains. This is likely what the market was keying on as the stock fell over the last few days. With CALM still up over 18% YTD, there could be more pain to come before inflationary pressures are fully priced in.

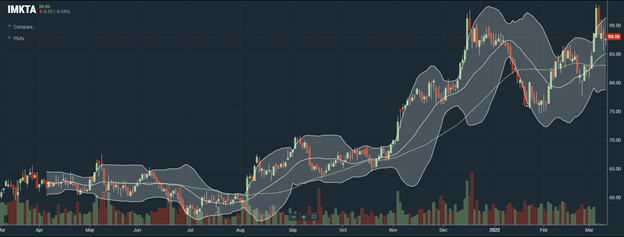

Ingles Markets (IMKTA)

Ingles Markets, Incorporated is a leading supermarket chain with operations in the southeastern United States. Ingles strategy is to locate its supermarkets primarily in suburban areas, small towns and rural communities, where management believes the market may be underserved by existing supermarkets.

IMKTA has seen some large moves so far this year. It significantly underperformed versus XLP through March but is now outperforming by 2.7% YTD. As a supermarket chain, IMKTA has significant fixed overhead costs including electricity and labor. Without pricing power or increasing volumes to offset higher costs, IMKTA will face margin pressures if the trend continues. Investors should remain cautious of IMKTA because a period of underperformance versus the broader sector could be in store.

Five for Friday

Five for Friday uses stock screens to produce five stocks that we expect will outperform if a particular investment theme plays out in the future. Investment themes may be relevant to the current or expected market, industry and/or economic trends. Investment themes may not always represent our current forecast.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)

Also Read