On Thursday, Fed Presidents Bullard and Waller talked down market expectations for a 1% rate hike at the July 27th FOMC meeting. Atlanta Fed President Bostic reiterated the message on Friday. Per Bostic: “75bps was a big move in policy, Fed wants policy transition to be orderly.”

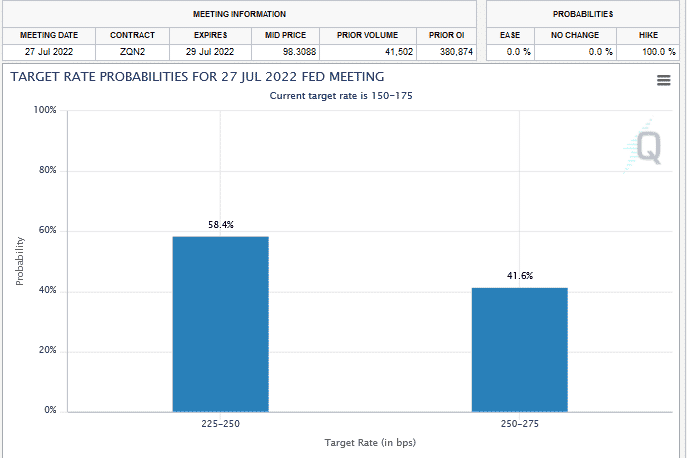

These statements come right before Fed Presidents enter their pre-meeting media blackout period. Barring anything to the contrary from other Fed Presidents early next week, we should assume the Fed will raise rates by 75bps. Despite our opinion and those of the Fed Presidents, Societe Generale expects the Fed to hike by 1%. While the stock market may take solace in the slightly less hawkish rhetoric, we highly doubt the FOMC or individual Fed Presidents will be any less aggressive in their fight against inflation. The graph below from the CME shows that Fed Funds imply a 41.6% chance of a 1% hike.

What To Watch Today

Economy

- 10:00 a.m. ET: NAHB Housing Market Index, July (65 expected, 67 prior)

- 4:00 p.m. ET: Net Long-Term TIC Outflows, May ($87.7 billion prior)

- 4:00 p.m. ET: Total Net TIC Outflows, May (1.3 billion prior)

Earnings

Pre-market

- Bank of America (BAC) to report adjusted earnings of 75 cents on revenue of $22.86 billion

- Goldman Sachs (GS) to report adjusted earnings of $6.65 on revenue of $10.67 billion

- Charles Schwab (SCHW) to report adjusted earnings of 90 cents on revenue of $5.03 billion

- Synchrony Financial (SYF) to report adjusted earnings of $1.45 on revenue of $2.77 billion

Post-market

- IBM (IBM) to report adjusted earnings of $2.29 on revenue of $15.16 billion

Market Trading Update

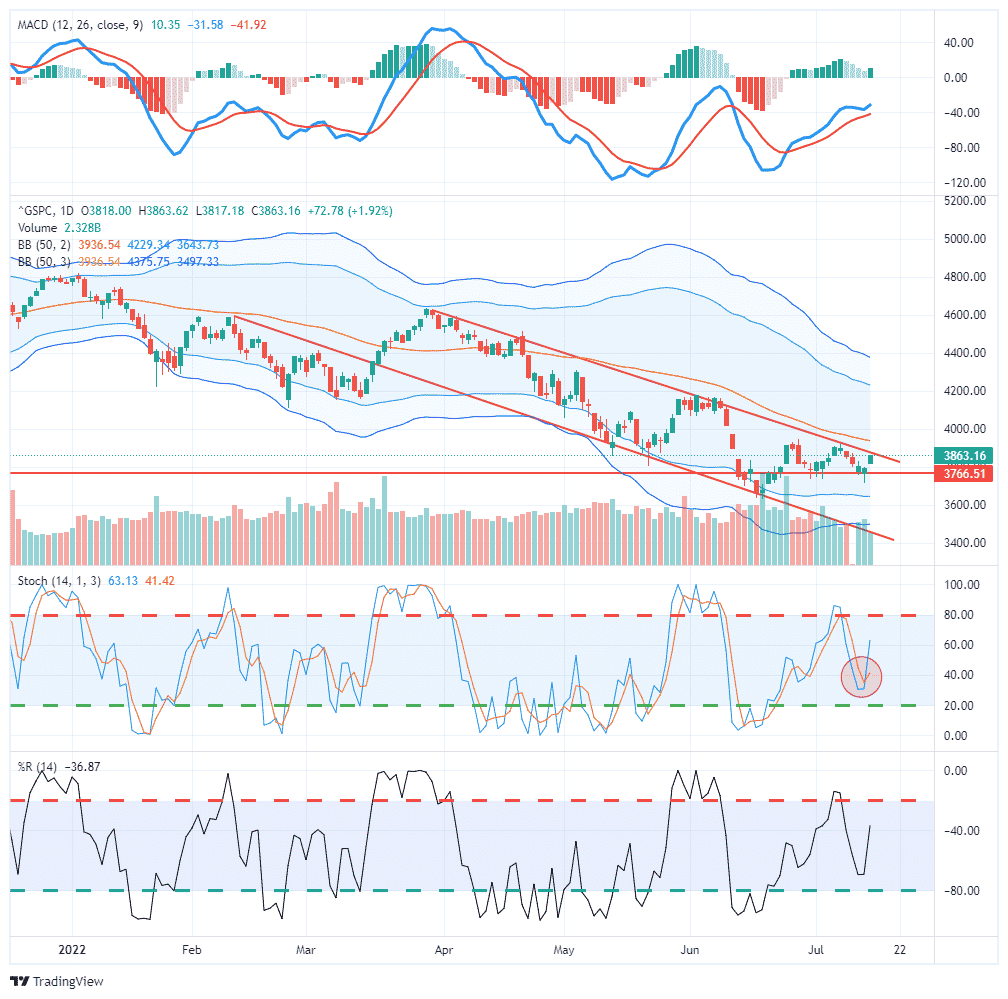

Over the last week, the market remained under pressure as a hotter-than-expected inflation report and a more robust employment report gave the Fed room to hike rates more aggressively next week. While stocks rallied nicely on Friday, these 2%ish-up days remain better for selling than buying as follow-through has been inconsistent.

Nonetheless, the market did hold minor support setting a higher low from the recent bottom. The rally was also strong enough to keep the MACD buy signal intact while shorter-term sell signals reverse back to a “buy” signal, as shown above.

The market is now challenging the downtrend line from the March highs, and with the recent sell-off, this is the best chance we have had as of late to potentially push above that resistance. Unfortunately, the market will almost immediately contend with the 50-dma resistance level.

The market risk currently remains earnings. As discussed last week, analysts remain overly optimistic on earnings and have now begun cutting estimates sharply ahead of earnings season. The risk is the current cuts are not enough to offset incoming reports, which could be worse than expectations. Forward guidance from companies will also be a vital issue for markets.

We will look for companies that announce earnings and give guidance below current estimates, but the stock price remains stable. Such would suggest that much of the bad news has been priced in and could provide opportunities to enter into selective positions.

As noted, the market risk remains high, so we remain cautious for now.

The Week Ahead

This week will be quieter on the economic data front than last week. Housing Starts, Building Permits, and Existing Home Sales will likely show the negative effect of higher mortgage rates. Existing Home Sales are expected to fall by 1.8%. The Philadelphia Fed Manufacturing Index will update us on manufacturing in the mid-Atlantic region. As we have noted, these regional surveys correlate well with national economic activity. Last Friday, the Empire State Manufacturing Index reported that prices paid and received fell sharply. We would like to see further confirmation in this week’s reports.

Corporate earnings will take center stage with the Fed entering its media blackout period before next week’s FOMC meeting. A lot of smaller regional banks will report in the first few days of the week. Also of note will be Abbott Labs, Alcoa, United Air, Verizon, and Sunoco.

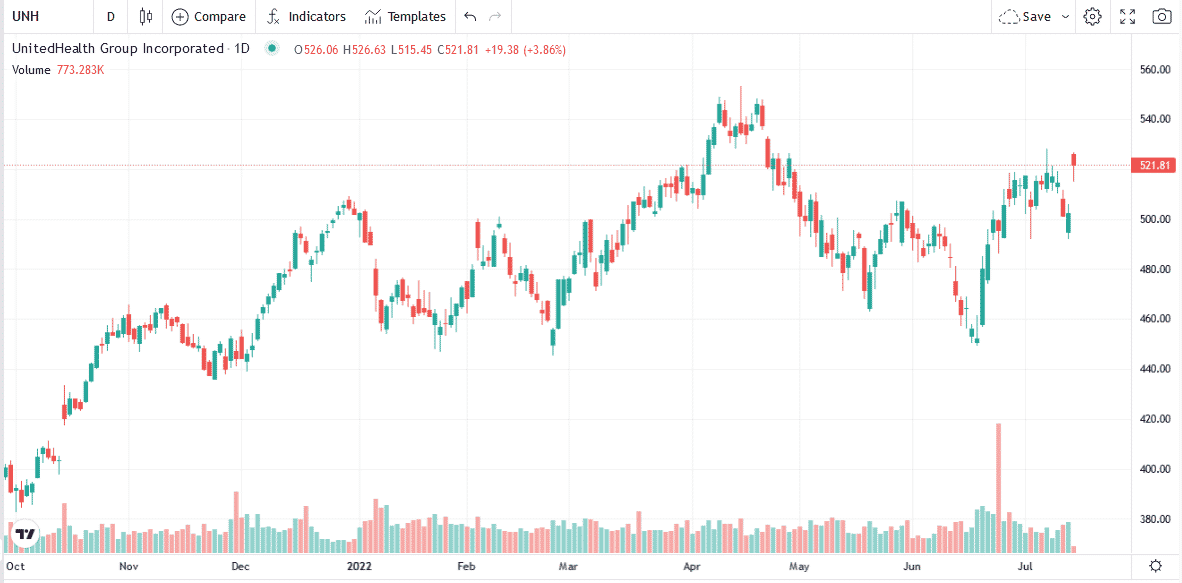

UnitedHealth With Strong Earnings

After a string of lousy bank earnings reports over the last two days, UnitedHealth (UNH) reported strong earnings on Friday. EPS at $5.57 per share handily beat estimates for $5.19. Revenue also exceeds expectations. Further, the company increased its fiscal year earnings outlook. The insurance company claims that keeping its costs “on a tight leash” and strong sales at its Optum Healthcare Services unit were primarily responsible for the beat. Other than rising wages, UNH, a services company, is not nearly as affected by inflation as most goods-producing companies.

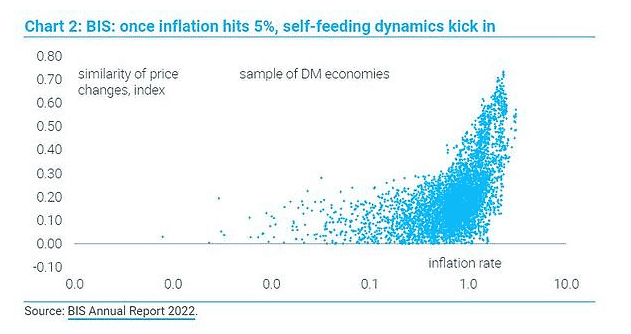

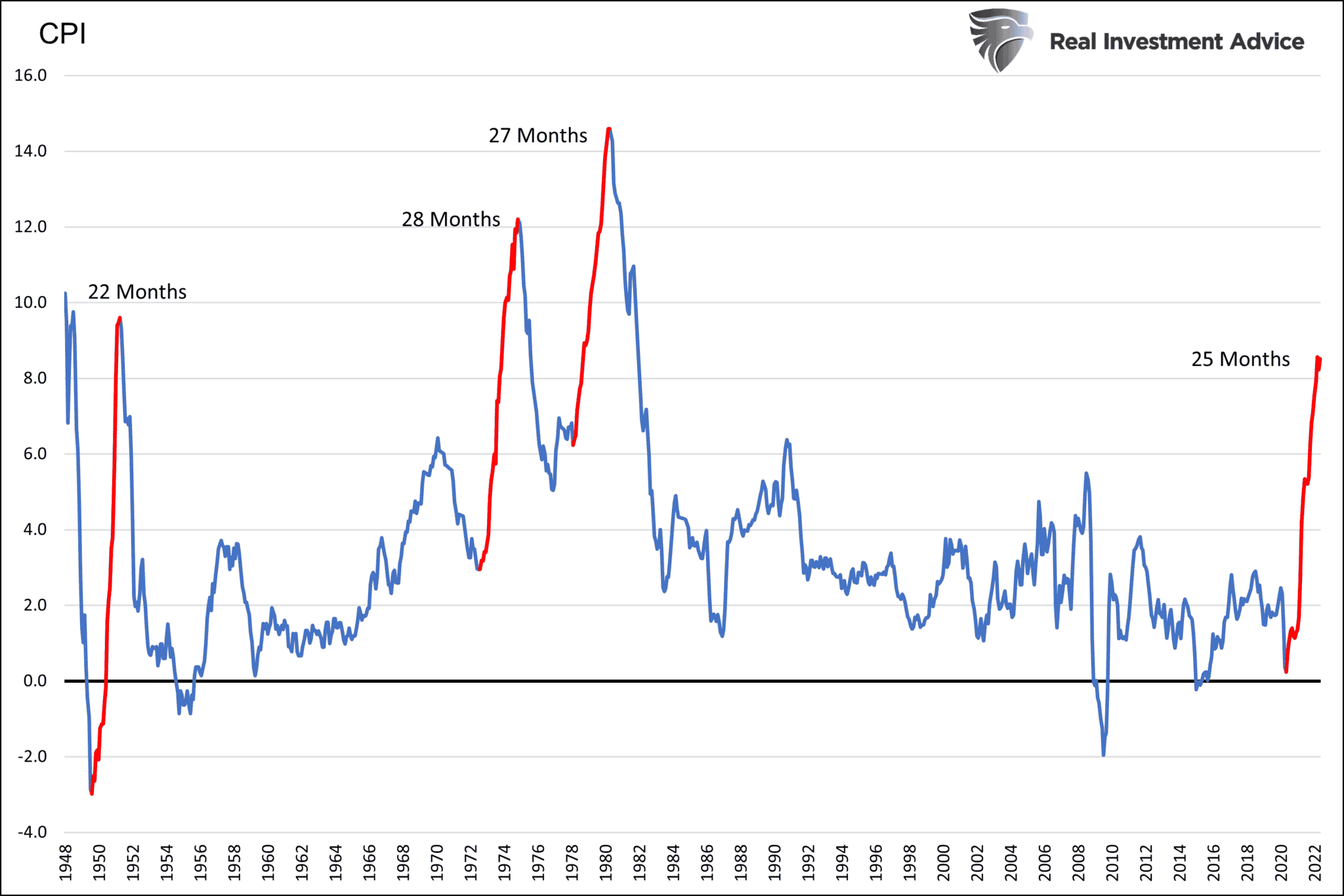

Does Inflation Beget More Inflation?

We often argue the cure for inflation is inflation. Simply, high prices result in demand destruction, normalizing supply/demand price curves, which result in lower prices. The Bank for International Settlements (BIS) recently published Inflation: a look under the hood. One key takeaway from the paper is that high inflation begets high inflation. The first graph below from the report shows that as inflation rises above 5%, “self-feeding dynamics kick in.” In their opinion, price-indexed wages and consumer perceptions keep high inflation persistent.

While the report has great information, we must consider that the only experience with persistent inflation (>5%) was 40 years ago. At the time, there was little debt. Such allowed for a more productive economy and much less reliance on debt and interest rates. After accounting for the stark economic, social, and political differences between today and forty years ago, the second graph below shows that bursts of inflation in the 70s and 80s resulted in equally strong disinflationary periods. That doesn’t mean that prices declined, but the rate of change of prices fell just as quickly as they rose.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read