False narratives are stories market pundits tell to justify market actions. Sometimes, they are factual. Oftentimes, legitimate-sounding false narratives are incorrect. Yesterday’s Commentary took bond market false narratives to task. Specifically, one which claims foreign debt holders, specifically China and Japan, are selling sizeable amounts of U.S. Treasury bonds, which forces Treasury yields higher. We follow with another false narrative: massive Treasury debt issuance is overwhelming the bond market. Consider the following comments we found on Twitter:

- This politician (Yellen) knows yields are ripping because of the debt she’s issuing. Yields are no longer moving up because of the FED, and they’re moving up because of debt issuance & foreign countries are selling.

- Soaring yields, partially driven by insatiable debt issuance by the US Treasury, are tightening conditions so fast.

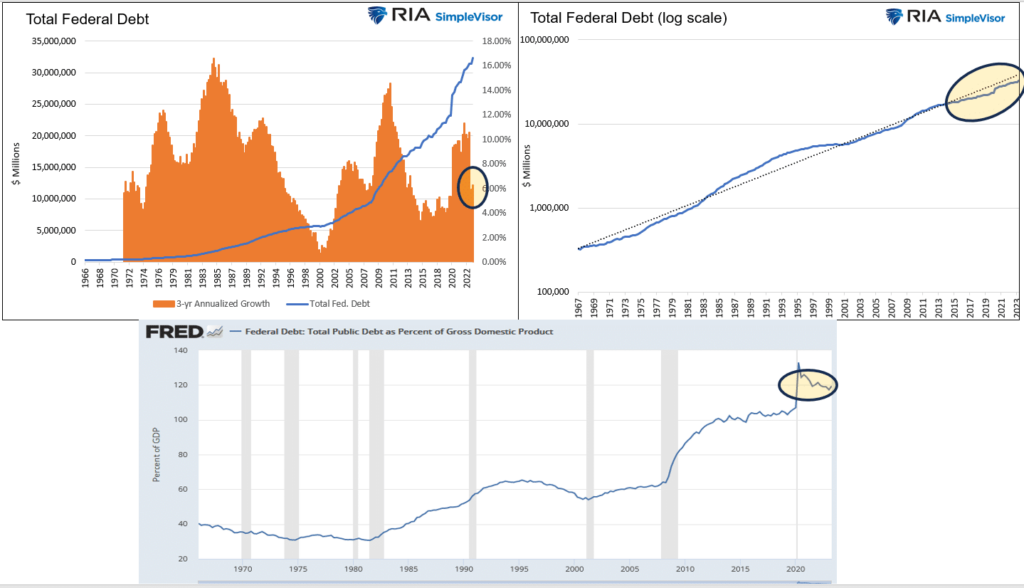

Listening to the media or Twitter, one might think Treasury debt issuance over the last six months is off the charts. Such stories are far from the truth when looked at from the right perspective. Consider the graphs below. The top left graph shows federal debt is growing slightly faster than the pre-pandemic years but well below prior surges. The right chart puts debt growth on a log scale to show the current growth rate is actually slightly below the trend of the last fifty years. Lastly, the bottom graph shows the sharp increase in debt to GDP during the pandemic. However, it has actually declined since. A high debt-to-GDP ratio, as we have, is very problematic. But false narratives claiming recent issuance is well above average are flat-out wrong.

What To Watch Today

Economics

Earnings

Market Trading Update

Yesterday, the market opened higher and then traded off into mid-afternoon, giving up all of its early morning gains. However, as we have discussed recently, institutional buying continues in the late afternoon, pushing the market back to its highs. Interstingly, Healthcare was the big loser sector yesterday, with bonds pushing higher. The market is not overbought yet, and the MACD “buy” signal is firmly intact. We are now positioned for the expected rally over the next few weeks, and dips should be bought. There is immediate resistance overhead at the 50-DMA and 100-DMA, which could limit the upside in the near term. The market has rallied strongly over the past few days, so a bit of a respite would be unsurprising.

If today’s CPI report comes in “hotter” than expected, such could trigger a pullback.

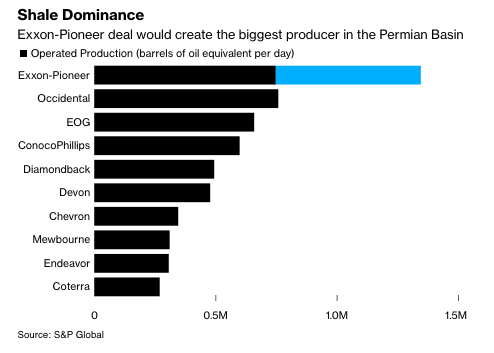

Exxon Buys Pioneer Drilling

ExxonMobil (XOM) is buying Pioneer Natural Resources (PXD) in a deal valued at $59.5 billion. As we show below, the agreement makes Exxon the largest shale producer in the Permian Basin. Shale oil from the Permian Basin is among America’s lowest-costing oil. Their businesses are very complimentary. Accordingly, Exxon sees approximately $1-2 billion annually in cost-saving synergies. Exxon is trading lower by about 4% as Pioneer shareholders are being paid in XOM shares.

PPI Surprises To The Upside

Producer Prices, which had been leading CPI lower, surprised to the upside. The headline PPI number was +0.5%, +.02% more than expected. Core PPI, excluding food and energy, met expectations, rising 0.3%. The well-followed core PPI, including trade services, was up 0.2%. The bond market didn’t seem concerned as they likely realized energy prices greatly impacted the data. Per Reuters:

Wholesale goods prices gained 0.9% last month, with a 3.3% rise in the cost of energy products accounting for nearly three-quarters of the increase. Goods prices jumped 2.0% in August. Gasoline prices rose 5.4%, making up more than 40% of the increase in the cost of goods last month. There also increases in the prices of jet fuel, electric power and diesel fuel.

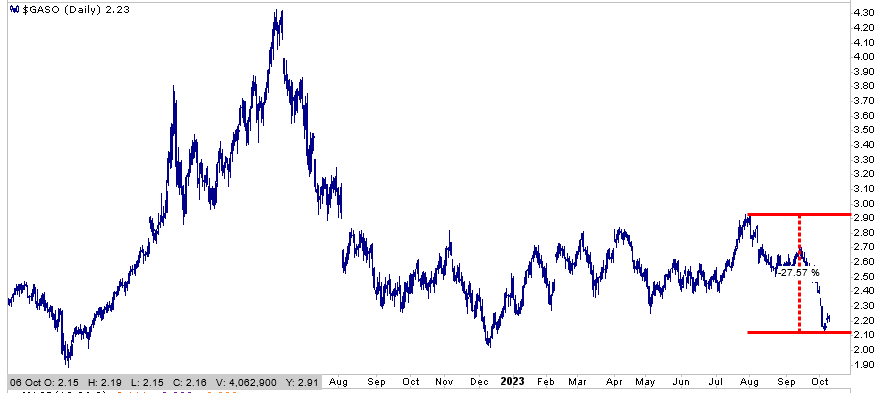

One flaw with the BLS CPI and PPI inflation reports is that the gas prices they use in their models lag the real world. As we show, gas prices have fallen over 25% since early August.

Fed President Waller Joins The Growing Chorus

There seems to be a growing chorus of Fed members alluding that the recent spurt in long-term yields may preclude the Fed from having to hike rates. Over the last few days, we have noted comments from Fed members Logan, Jefferson, and Bostic along these lines. We add another today with Fed Governor Waller. The following is from MarketWatch:

“Financial markets are tightening up and they’re going to some of the work for us,” Waller said in a conversation with former House Speaker Paul Ryan.

The Fed is going to keep a “close eye” on this dynamic “and we’ll see how these higher rates feed into what we’re going to do with policy in coming months,” he said.

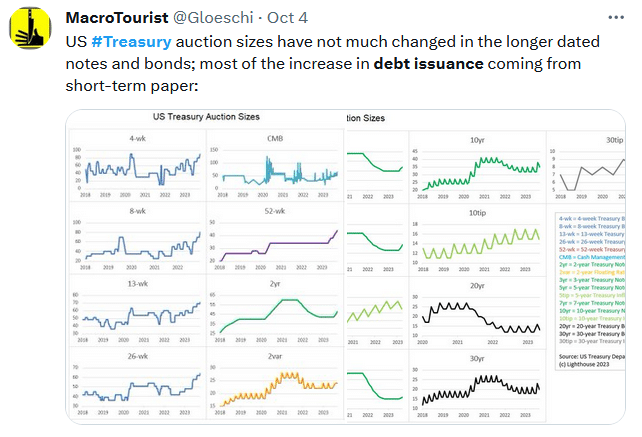

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.