Shares of ETSY plunged yesterday on a poor quarterly earnings report. We are not very concerned about ETSY, per se, but its woes tell a lot about the state of the consumer. ETSY is a moderate to higher-priced arts & crafts etailer. ETSY flourished during the Pandemic when consumers were flush with cash and had nothing to do but shop online. Now, consumers are increasingly strapped for cash as wages fail to keep up with inflation.

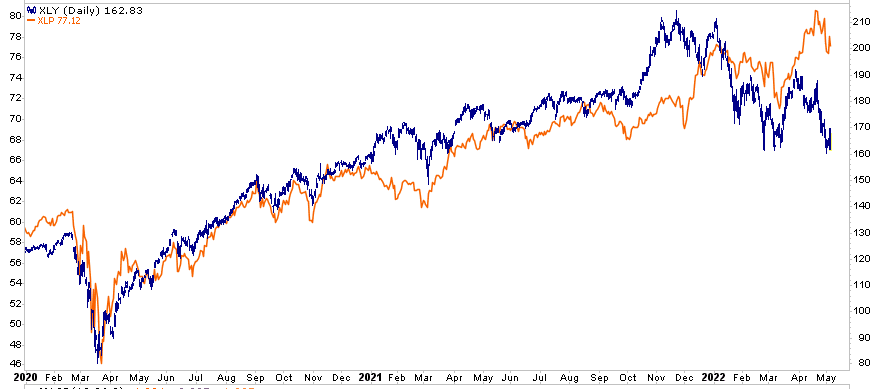

As we saw with Netflix, consumers now have to make hard decisions about what they purchase. Discretionary, non-necessity items, like those sold by ETSY, are the first type of items that consumers often step away from. Investors are picking up on the situation. The graph below shows consumer staple stocks are holding up much better than consumer discretionary stocks.

What To Watch Today

Economy

- 8:30 a.m. ET: Change in non-farm payrolls, April (380,000 expected, 431,000 in March)

- 8:30 a.m. ET: Unemployment rate, April (3.5% expected, 3.6% in March)

- 8:30 a.m. ET: Average hourly earnings, month-over-month, April (0.4% expected, 0.4% in March)

- 8:30 a.m. ET: Average hourly earnings, year-over-year, April (5.5% expected, 5.6% in March)

- 8:30 a.m. ET: Labor Force Participation Rate, April (62.5% expected, 62.4% in March)

Earnings

Pre-market

- Under Armour (UAA) to report adjusted earnings of 7 cents on revenue of $1.33 billion

- Cigna (CI) to report adjusted earnings of $5.18 on revenue of $43.5 billion

- DraftKings (DKNG) to report quarterly results before market open

Post-market

- No notable reports scheduled for release

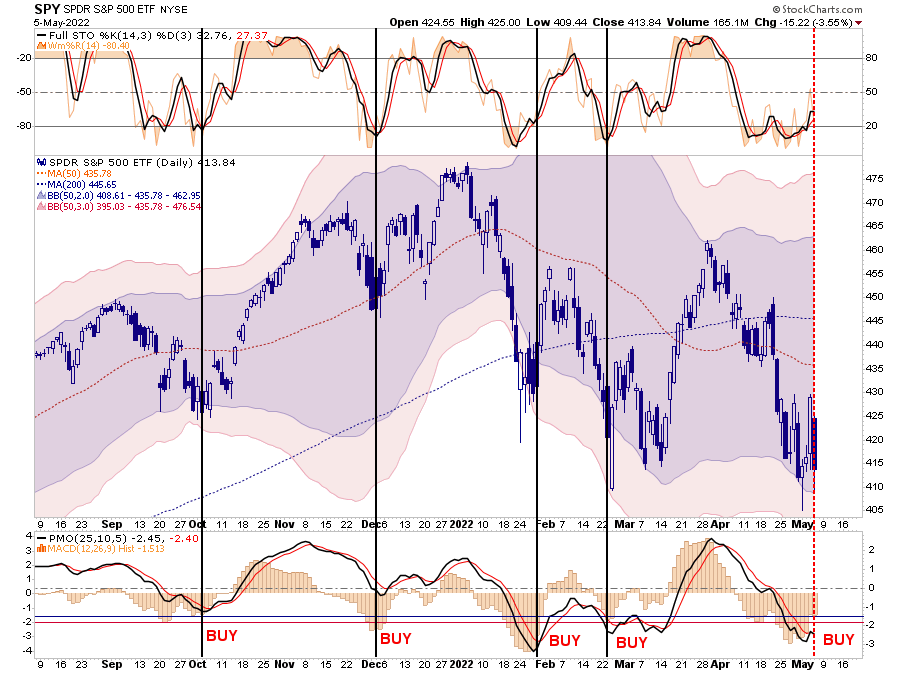

Market Trading Update – A Failed Rally

The market continues to flirt with deep oversold and deviated levels from the 50-dma. As shown, since this consolidation started last September, deeply oversold levels repeatedly led to reflexive rallies of some magnitude. So far, the market remains unable to do that, however, such is usually the case just before it rallies. The markets tend to do things that frustrate the most investors every time.

We suspect the market is likely doing just that and yesterday’s selloff had many of the hallmarks of capitulatory selling. However, without a rally that has some follow-through, the markets will continue to struggle for the time being.

A Very Normal Year

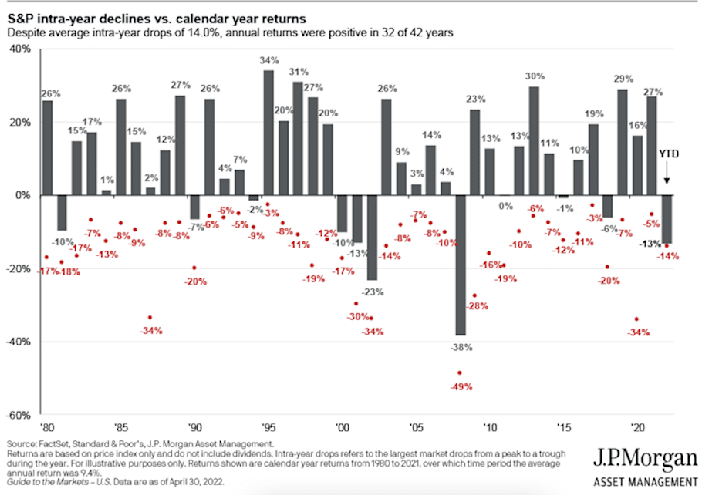

Last year, I wrote that it had been so long since we had a 10% correction, that when it eventually came it would FEEL much worse than it actually was. Such has certainly been the case this year with investors panicking and dumping stocks like ETSY en masse. However, as Sam Ro noted for Yahoo Finance this morning, this is indeed a fairly normal year. To wit:

“It’s been an incredibly unpleasant year for stock market investors.

After setting a record closing high of 4,796 on January 3, the S&P 500 tumbled 13% to 4,170 on March 8. It then rallied to 4,631 on March 29, but then fell again hitting a closing low of 4,146 on Thursday, reflecting a max drawdown (i.e. the biggest intra-year sell-off) of 14%.

However, this year’s moves are nothing out of the ordinary. Since 1950, the S&P has seen an average annual max drawdown of 14%.”

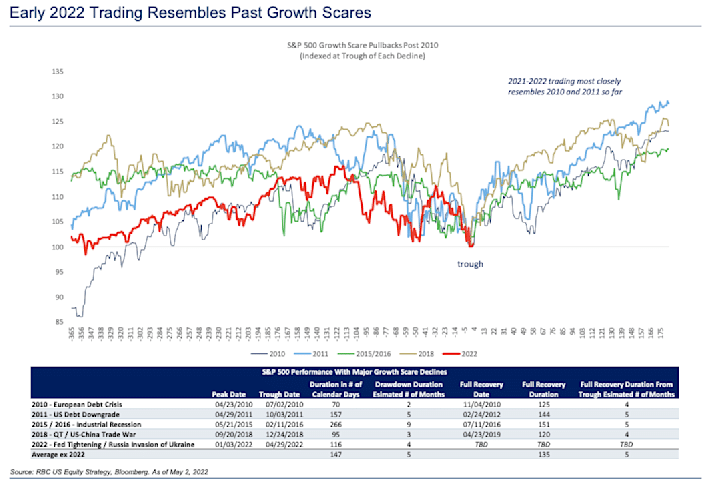

He went on to quote RBC Capital Markets on how markets reacted during four recent growth scares. RBC noted that following market troughs, the six-month returns ranged from 18.2% and 28.6%. The 12-month returns ranged from 26.6% to 32.0%.

While it is easy to find a lot of reasons to be bearish, these data points are useful in retaining perspective and combatting confirmation bias.

Okay, now back to being bearish.

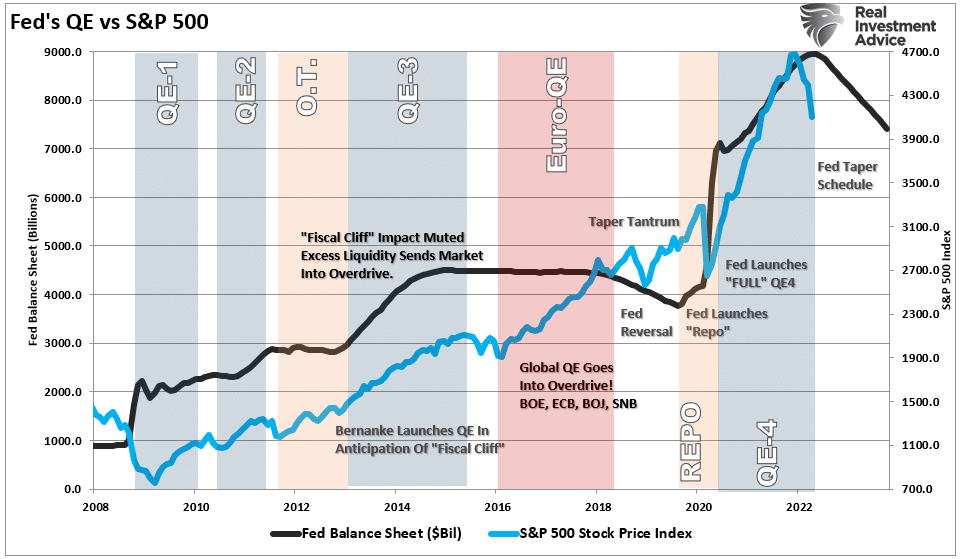

The Fed Taper

The Fed’s taper path is shown in the chart below. I plotted the taper through the end of 2023. Just to show you how gargantuan the Fed’s balance sheet is, at a $95 billion dollar monthly pace, they will only reduce their balance sheet to ~$7.25 Trillion.

Jobs- a Mixed Picture

Today’s BLS jobs report follows Wednesday’s ADP report and will update us on the state of the labor markets. As we noted yesterday, the ADP report was good, but it showed a decline in the number of workers employed by small businesses. While there is little evidence the jobs market is peaking, the ISM manufacturing and services Employment surveys hint this may be changing. The manufacturing survey fell to 50.9, while services fell to 49.5. A reading below 50 points to economic contraction.

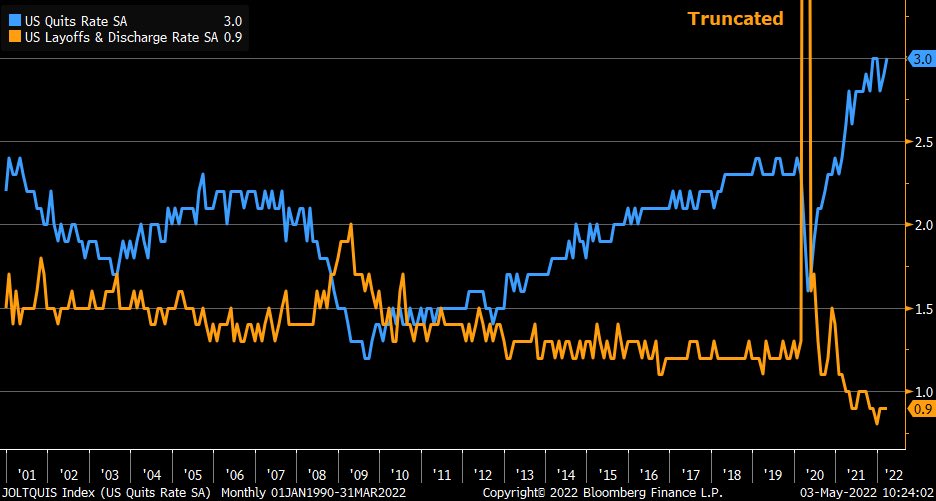

Assessing today’s labor market will be more complicated than in the past. For the last year or two, it was exceedingly hard to hire employees. As such, we think employers will hold onto employees longer than usual despite a slowing in business. This may make it initially difficult to see a declination in the jobs market in the traditional data sources such as initial jobless claims. To this point, the graph below from the latest JOLTS report shows that the layoff & discharge rate is the lowest in at least 20 years. At the same time, employees are still emboldened and willing to quit to find a better job.

The BLS jobs report is expected to show the economy added 400k jobs in April. Of growing importance, expectations are for a .4% increase in monthly earnings. While strong, such a result remains well below the inflation rate and further crimps the ability of consumers to spend.

Value Is Leading the Way

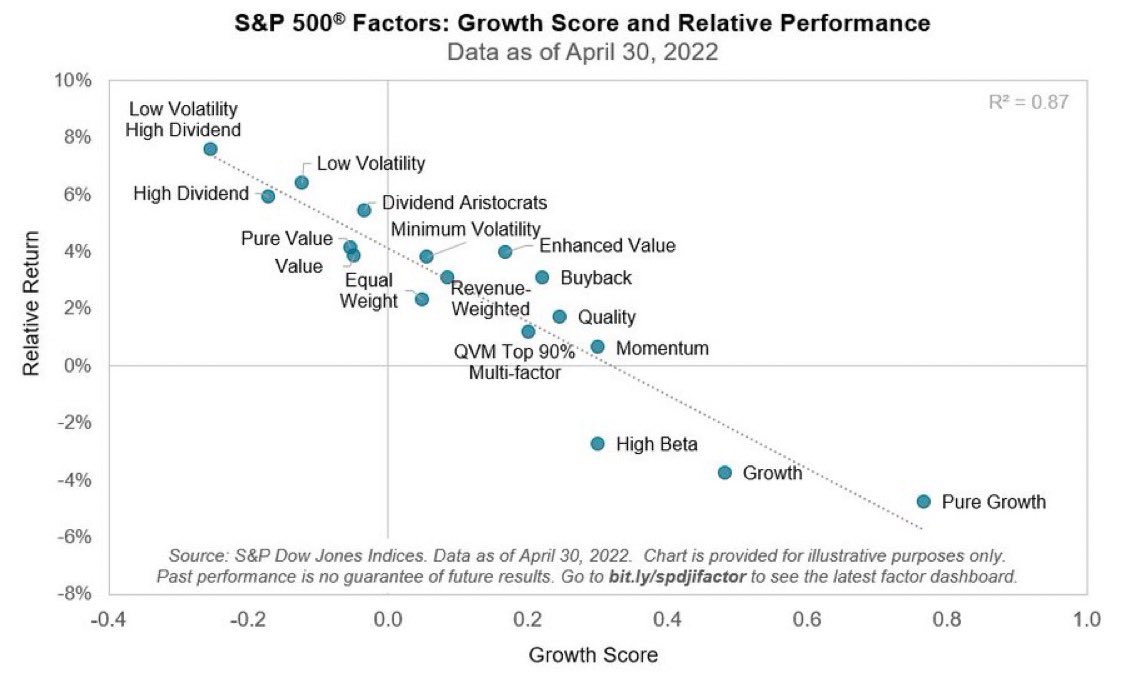

As we think about our investment portfolios, we strongly consider the economic and monetary factors that will likely guide the broader market trends. We then hone in on the stocks, sectors, and factors poised to out and underperform, given our economic and monetary outlooks. Thus far, in 2022, weak/slowing economic growth and tightening monetary policy are our guideposts. We do not see that changing in the near term. In this environment, low volatile, higher dividend stocks have outperformed while higher growth stocks have underperformed.

The graph below shows that the “growth” factor has separated winners from losers. If the same economic and monetary trends continue, as we think they might, the graph below may provide an excellent road map for portfolio allocations.

Expect the Expected- FOMC Recap

On Tuesday we wrote to “expect the expected” from the Fed meeting. We thought there was little chance the Fed or Powell would surprise in a dovish or hawkish manner. Post-meeting, the media considered it dovish that Jerome Powell dismissed raising rates by 75bps at the June meeting. Yes, 75bps was priced into the markets, but Fed members had not previously mentioned such a large increase. In our opinion, the market’s favorable reaction Wednesday was not justified by anything the Fed or Powell said. As such, the reversal on Thursday should not be shocking either.

As far as looking ahead, we must remember that the stock and bond markets remain a hostage to tightening Fed policy and tightening financial conditions. That will not change until inflationary data shows signs of slowing and the Fed starts to back down from its monetary forecasts. That said, there will be opportunities when markets deviate too far from trends.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read