If you think the Fed is hawkish, you ain’t seen nothing yet. In a Bloomberg editorial released on Friday, former New York President Bill Dudley opines that the most effective way to manage inflation is to make investors suffer. In the Bloomberg video below, Bill Dudley explains his thought process. Essentially Dudley is blaming uber-easy financial conditions for the high rates of inflation. Higher bond yields and lower stock prices will make financial conditions stricter and thus temper inflation. Fed Chair Jerome Powell tends to agree. In March, Chairman Powell stated: “Policy works through financial conditions. That’s how it reaches the real economy.”

What To Watch Today

Economy

- No notable reports scheduled for release

Earnings

- No notable reports scheduled for release

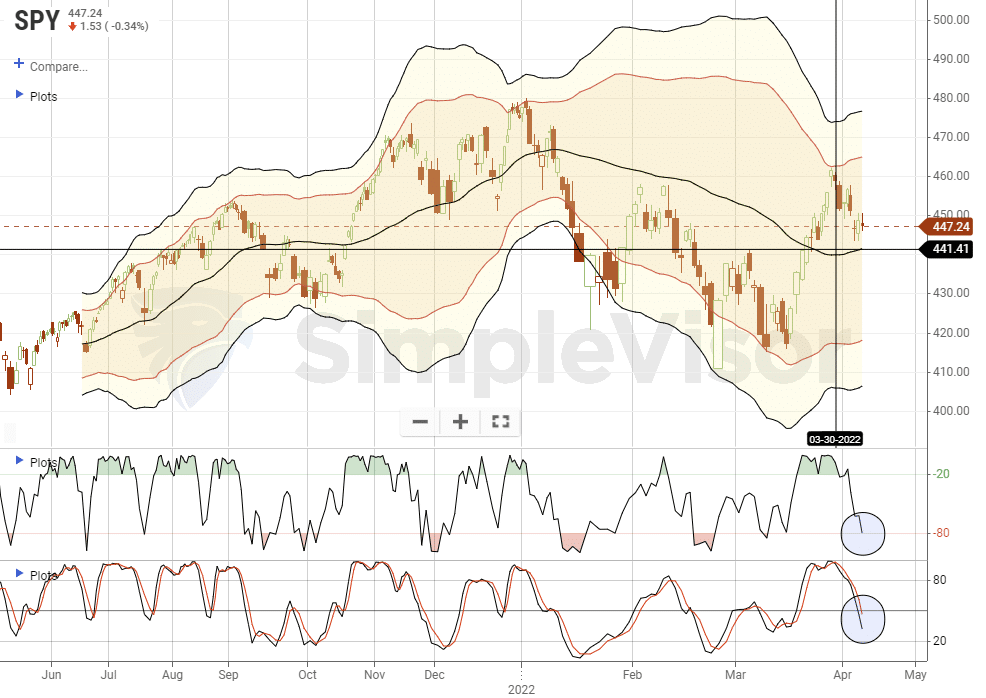

Market Trading Update

During the past week, the message was consistent.

“The continued sloppy action over the last week is doing its job of working off the overbought condition while maintaining critical support about the 50-dma. With both of the technical sell-signals about 50% of the way through a normal reversion, a few more days of consolidation should open up the window for a tradeable opportunity.”

As of Friday, the sloppy action reversed most of the overbought conditions. There was a good bit of rotation between sectors. On Monday, money flows strongly favored the “deflation sectors,” with technology leading the way higher. That flipped later in the week, following the release of the FOMC minutes, with “inflation safety sectors,” like staples, healthcare, and energy outperforming.

However, over the last 10-weeks, there has been no discernable trend in most sectors, except for energy. Sectors have oscillated very tightly around the relative performance of the S&P 500.

This “directionless” market trend makes navigating markets more difficult than usual. Oversold sectors tend to remain oversold, and overbought sectors remain overbought longer than expected.

Longer-term, we are likely at an essential juncture in the market. Like Dudley states, lower prices will impact confidence, creating a recession and taming inflation.

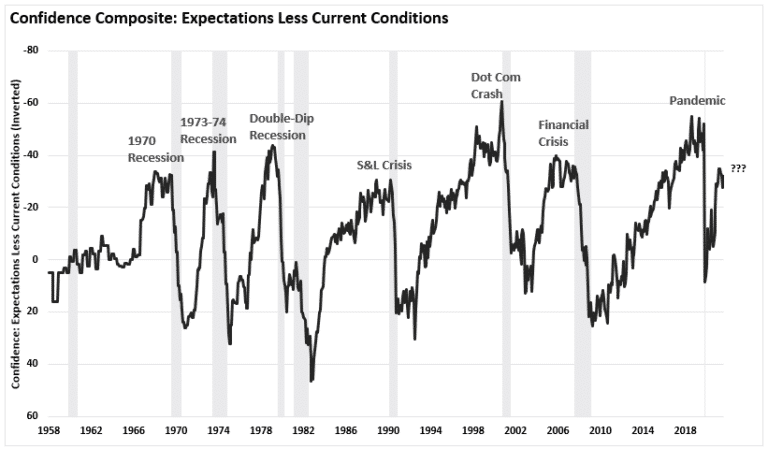

Confidence Already At Dangerous Levels.

In 2010, Ben Bernake stated that QE would boost asset prices in turn improving consumer confidence which would translate into economic growth. That idea proved correct.

With Dudley suggesting the asset price corrections would tame inflation (by reducing confidence) it won’t take many actions from the Fed to get their wish. Our consumer confidence composite index (UofM and Conference Board measures) of expectations less current conditions, is already at levels that previously denoted more severe market and economic outcomes.

In fact, the last time we were at these levels, we were headed into the 2008 “bear market.”

The Week Ahead

After a relatively dull week of economic releases, the market will grapple with CPI on Tuesday and PPI on Wednesday. Year over year CPI is expected to rise from 7.9% to 8.3%. Equally important is the monthly change. It too is expected to pick up from 0.8% to 1%. On top of inflation data, we will get Retail Sales on Thursday. Expectations are for a gain of 0.4%. We caution the results could be much more or less than expectations as inflation boosts the nominal value of sales, but consumers are buying less due to inflation. The Treasury Department will auction 10yr notes after the CPI release and 30yr bonds after PPI. We suspect bonds will trade sloppy going into the auctions as dealers hedge in volatile market conditions.

The major banks and airlines kick off the Q1 earnings season. JP Morgan and BlackRock lead off on Wednesday, with most banks following Thursday. Markets will be closed on Friday for the Good Friday holiday.

Once again, we will need to pay close attention to speeches from Fed members. As we saw last week, the Fed’s tone is hawkish, and it seems to be catching investors off guard. That said, with a proposed schedule for QT floated out by the Fed and discussion of a 50bps rate hike by many members, it does not appear there is much more than can say that would upset markets.

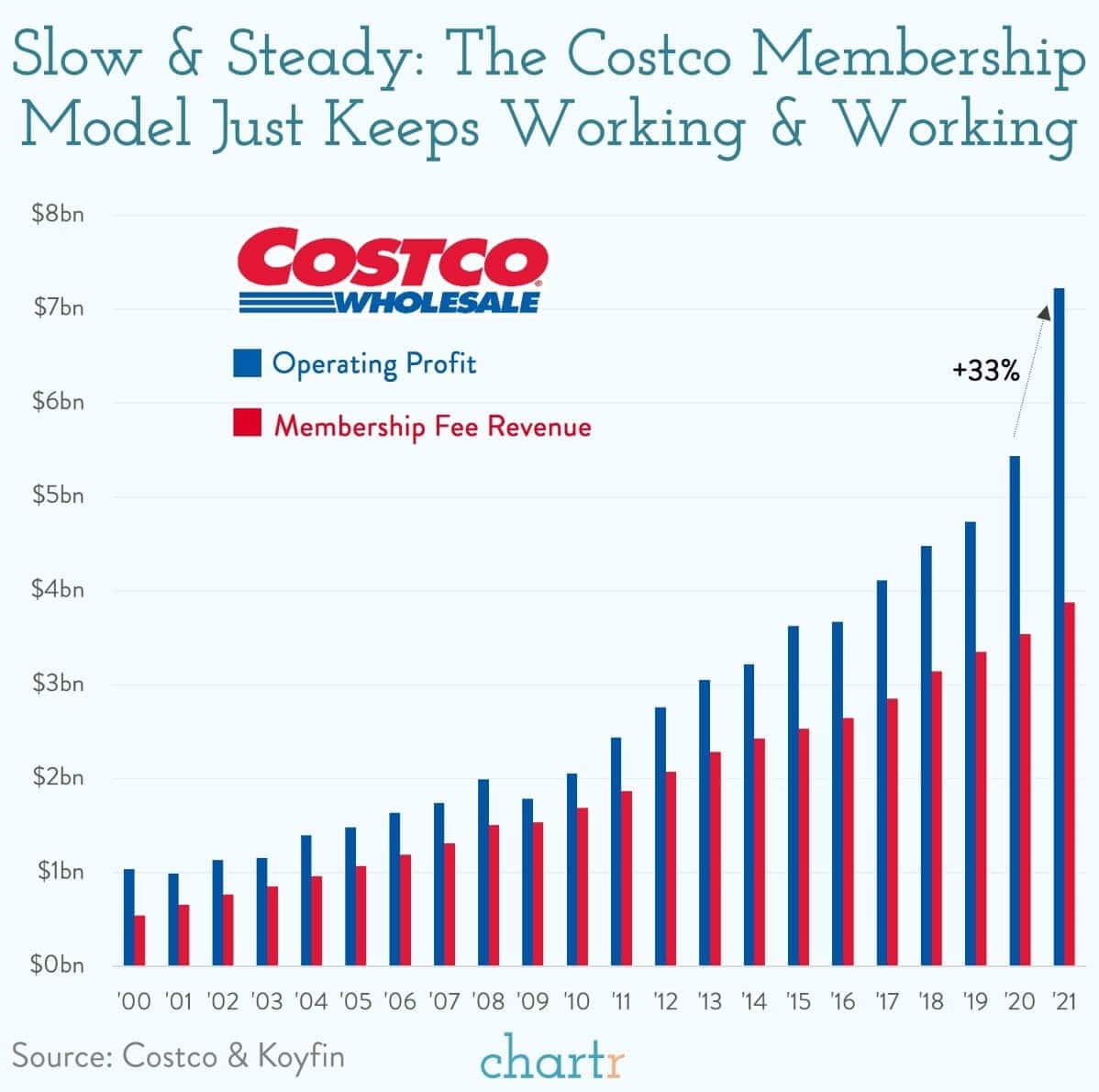

Why We Are Long COST – It’s The $1.50 Hot Dogs

“This week Costco, the membership-only big-box retailer, announced that the company’s revenue had jumped almost 19% in March, relative to the year before. That’s fast growth for a sleepy retailer that doesn’t pay for advertising and is most famous for huge no-frills warehouses and $1.50 hot dogs.

Technically, Costco is a private club. It’s just not a very stuffy one. Shopping at Costco requires a membership, which ranges from $60-120 a year. Once a member, Costco will pretty much sell you anything, at cut prices and preferably in bulk. That means that, like most retailers that compete on price, Costco lives with a slender profit margin, which last year was just over 3%.

Costco’s membership fees are almost pure profit. That smooths things out big time for a business that could otherwise be a bit of a roller coaster. Indeed, if you assume Costco’s membership fees are pure profit then they’ve accounted for 65-70% of the company’s total operating profit over the last 20+ years.

The epitome of Costco’s no-frills strategy is their $1.50 hot dog, which is a staple of the Costco experience and has been keeping customers coming back for 35+ years, charging $1.50 the entire time. Presumably at some point they began losing money with every hot dog sold, prompting the CEO to approach the founder, suggesting they raise the price, to which he was told ‘if you raise the [price of the] effing hot dog, I will kill you. Figure it out.’ — they figured it out.” – Chartr

At least Dudley won’t be able to kill a cheap lunch.

More Dudley

We think there is some merit to Dudley’s mindset discussed in our opening section. As such, we share his summary from the editorial.

Financial conditions need to tighten. If this doesn’t happen on its own (which seems unlikely), the Fed will have to shock markets to achieve the desired response. This would mean hiking the federal funds rate considerably higher than currently anticipated. One way or another, to get inflation under control, the Fed will need to push bond yields higher and stock prices lower. Quote courtesy of Bloomberg.

Financial Stability

The Fed seems intent on aggressively rates and reducing its balance sheet. What might get them to change their mind? The two easy answers are a significant decline in stock prices and a sharp drop in inflation rates. Even though Congress mandates the Fed to manage monetary policy based on employment and prices, the Fed has assumed the job of maintaining “financial stability.” Financial stability, in their minds, is limiting declines in asset prices and stopping non-Treasury bond spreads from widening.

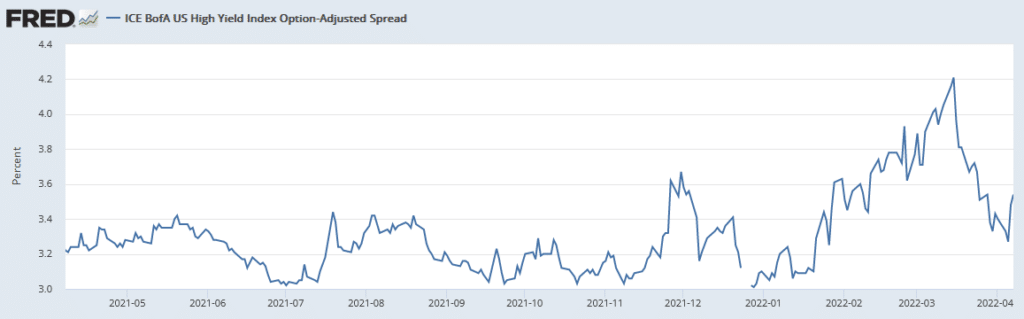

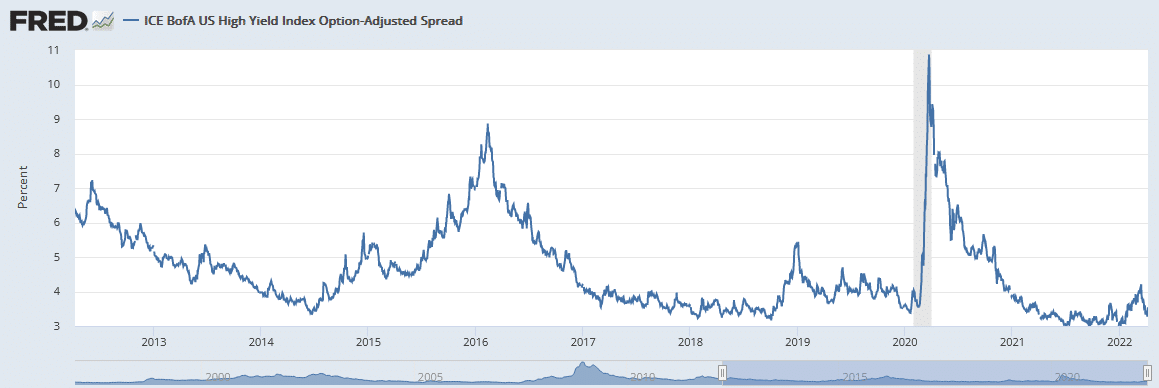

One of the Fed’s critical financial stability measures is the ease with which companies can borrow money. An influential gauge is the spread or difference between junk-rated debt yields and Treasury yields. The first graph below shows that the junk/Treasury spread widened by about 1.25% to start the year but has since cut that in half. While some claim borrowing conditions are tightening, a longer-term view, as shown in the second graph, argues the rise in the first three months is meaningless in the grand scheme of things. The Fed will probably start paying closer attention when the yield spread is 5% or more.

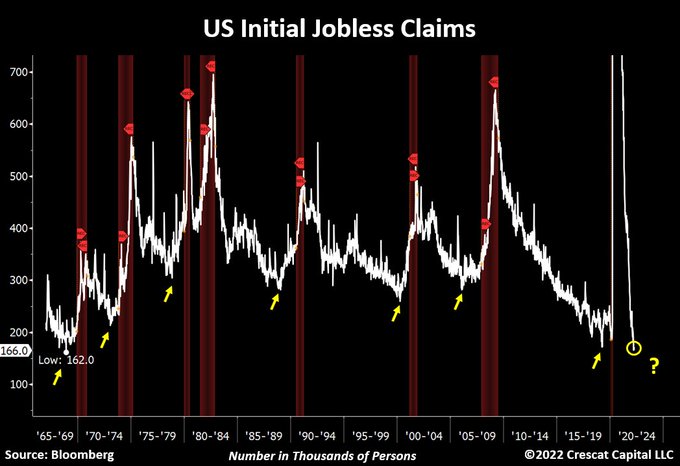

Are Record Low Intial Jobless Claims Bullish

Last week, initial jobless claims registered the second-lowest weekly reading ever. Such a low number is evidence of a red-hot labor market and the lack of available workers. There is another side of the coin, as Otavio Costa points out below. As his graph shows, jobless claims are cyclical. A trough in initial claims preceded each recession. Claims then peak toward the end of the recession and head back lower. Rinse, wash, repeat… Similar to an inverted yield curve and its recession warning, the trough in claims occurs well ahead of the official NBER recession proclamation. The average period is 11 months, but it varies from two months to 18 months.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

Also Read