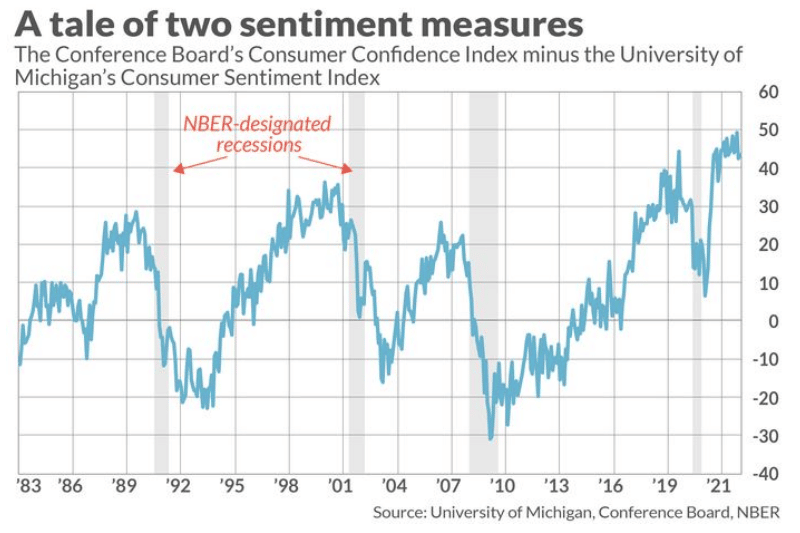

MarketWatch recently pointed out that two well-followed measures of consumer sentiment are diverging and possibly confusing investors. While investors may prefer one index over the other, a more robust economic and market forecast may occur when the indexes are diverging. The MarketWatch graph below shows the difference between the Conference Board (CCI) and the University of Michigan Consumer Sentiment (UM) Indexes. CCI measures broad economic sentiment. On the other hand, UM is more personal, focusing on individuals’ unique financial situations. When CCI was much more optimistic than UM, like today, a recession followed. When the difference is in the highest 10% of readings, the S&P averaged a 5-year annualized return of -3.1%. Conversely, when the divergence was in the lowest 10%, returns over the same period averaged +14.8%.

The article concludes as follows: “The bottom line? It’s not good news, for the economy in general or the U.S. stock market in particular, that consumers are so much more upbeat about the overall economy than they are about their immediate financial circumstances.”

What To Watch Today

Economy

- 8:30 a.m. ET: Trade Balance, October (-$77.0 billion, $73.3 billion expected)

Earnings

Market Trading Update

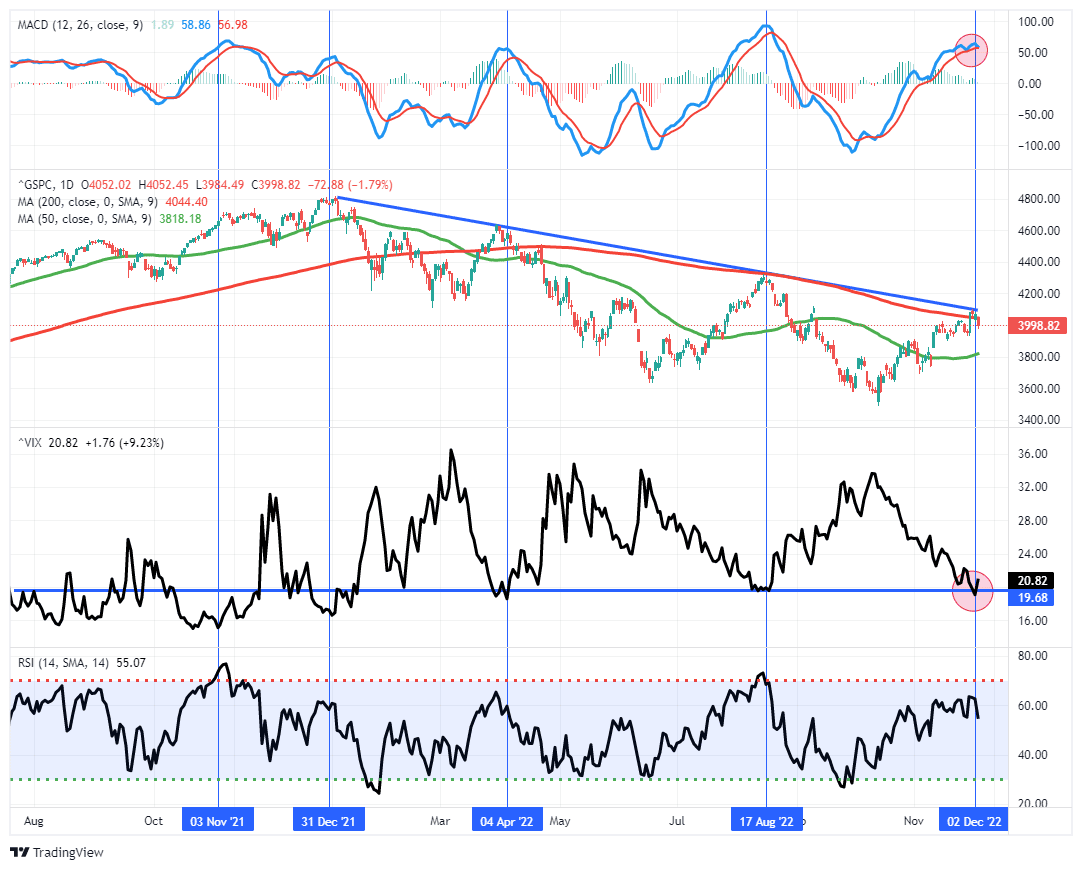

The market opened slightly weaker yesterday morning but sold off after Nick Timiraos for the Wall Street Journal published commentary ahead of the upcoming FOMC meeting. Nick, known as the Fed whisperer, is the official “Fed leak” when the FOMC is in its blackout period ahead of a policy meeting. The comments yesterday were an attempt to jawbone back the market’s dovish perception.

Federal Reserve officials have signaled plans to raise their benchmark interest rate by 0.5 percentage point at their meeting next week, but elevated wage pressures could lead them to continue lifting it to higher levels than investors currently expect.

…brisk wage growth or higher inflation in labor-intensive service sectors of the economy could lead more of them to support raising their benchmark rate next year above the 5% currently anticipated by investors.

Specifically, Timiraos confirms what most Fed speakers have been saying:

They want to guard against raising rates too little and allowing inflation to resurge, or raising them too much and causing unnecessary economic weakness, according to recent public comments and interviews.

Some officials could seek to push through another half-point rate rise in February because they see a greater risk that inflation won’t decline enough next year. Without signs of slower hiring, they could worry that inflation could pick up again.

Not surprisingly, that hawkish language took the “wind out of the bull’s sails,” sending the market back below the 200-dma. The market is holding support at the 20-dma, and the 100-dma is sitting just below that. Importantly, the MACD signal is very close to turning lower, suggesting the market may struggle between now and next week’s FOMC meeting. We remain risk-averse until we get a better opportunity to increase equity risk.

A Second Opinion on the Health of the Jobs Market

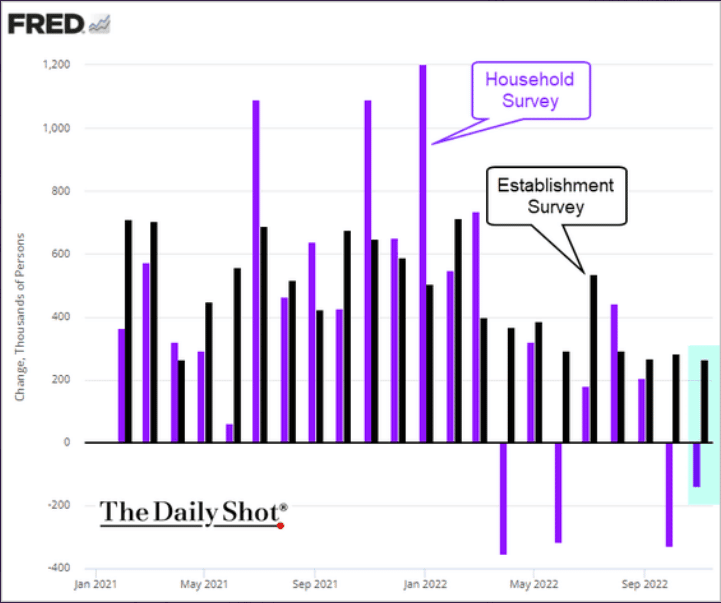

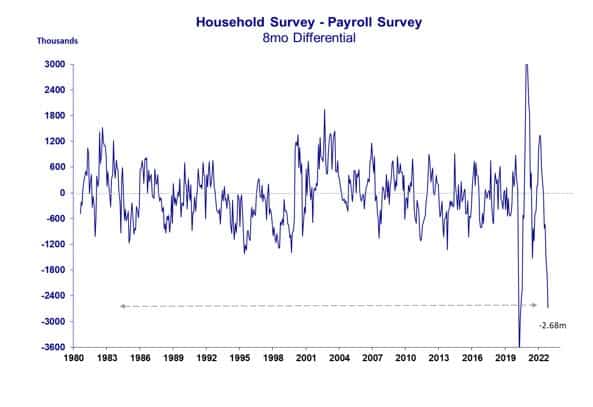

The jobs market is weakening between the JOLTS and the BLS employment report but remains historically strong. However, two recent data points are diverging from the more traditional reports. The first graph shows the BLS survey of household job growth is well below its well-followed establishment survey. Since March, the household survey has shown zero job growth. Over the same period, the establishment survey points to 2.7 million new jobs. The growing gap, as shown in the second graph, is palpable. Of concern, the household survey tends to lead the establishment survey, although not usually to the degree it is today.

The third graph shows a spike in the number of announced job layoffs in November per the Challenger report. Interestingly, a large percentage of the job losses are in the technology sector. Of the nearly 80k pending job losses, 52k are in the technology sector. The next largest sector was consumer products at 4.1k. The Fed will want to see widespread job losses across multiple industries before the employment picture becomes a concern.

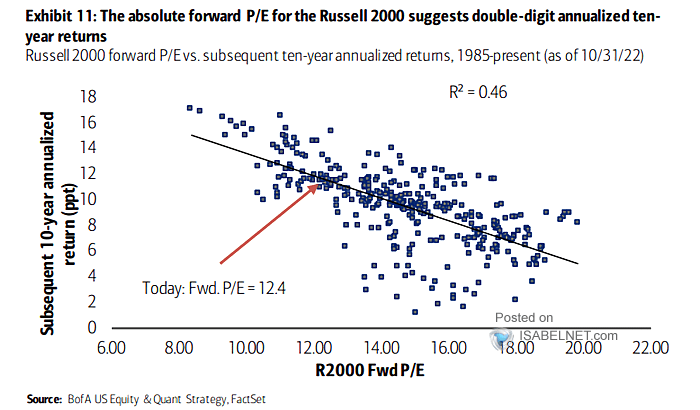

Small Cap Stocks Might Win the Next Decade

The Russell small cap index trades with a forward P/E of 12.4. That compares favorably with 20 for the S&P 500. Using 35+ years of data, forward P/Es provide a decent forecast of forward returns. As the graph shows, we might expect the index to post double-digit annualized returns for the next ten years. That compares very favorably with the forecast for the S&P 500 to return 5% annualized. More importantly, as our friends at Kailash Concepts have been preaching, more promising returns may be possible within the value stocks of the Russell 2000.

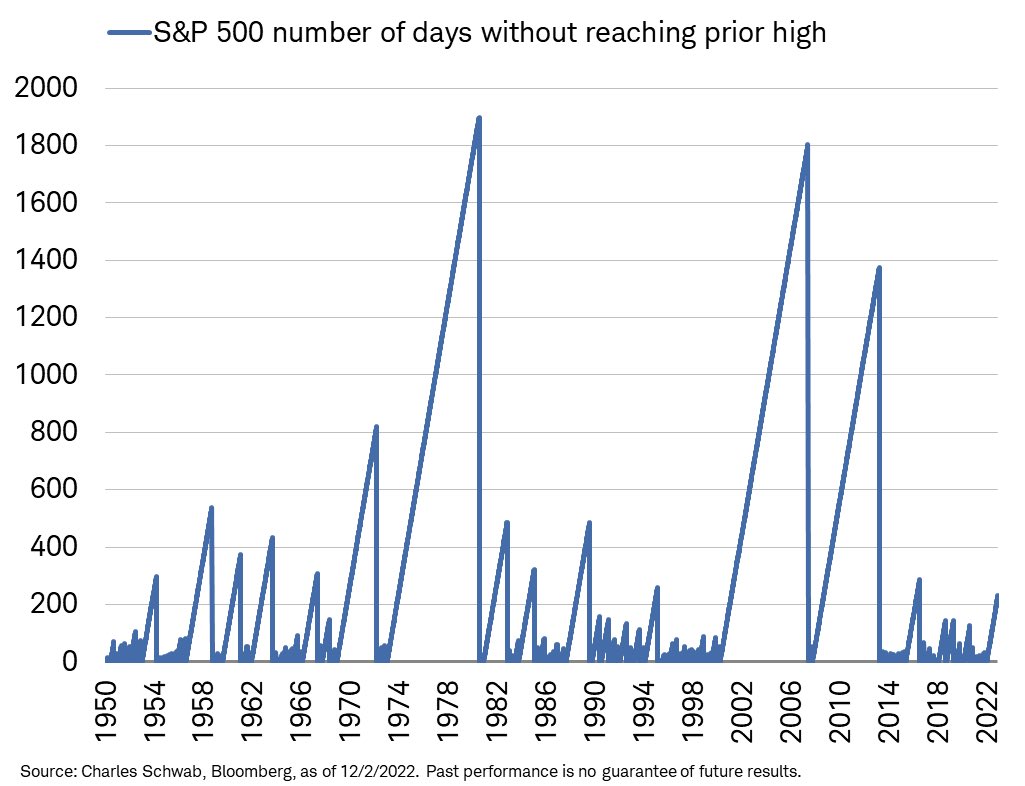

How Much Longer Can the Bear Market Persist

While it may feel like the 2022 bear market is growing long in the tooth, it pales compared to other downtrends. The S&P 500 has gone just over 230 days without returning to its prior high. The last such dip was in 2016. If we enter a recession, the streak may extend considerably longer, as witnessed in the 2000 and 2008 recessions. The recession of 1990 and the short-lived 2020 pandemic recession provide hope this downward trend is closer to an end than the beginning.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read